Leuprolide Acetate Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

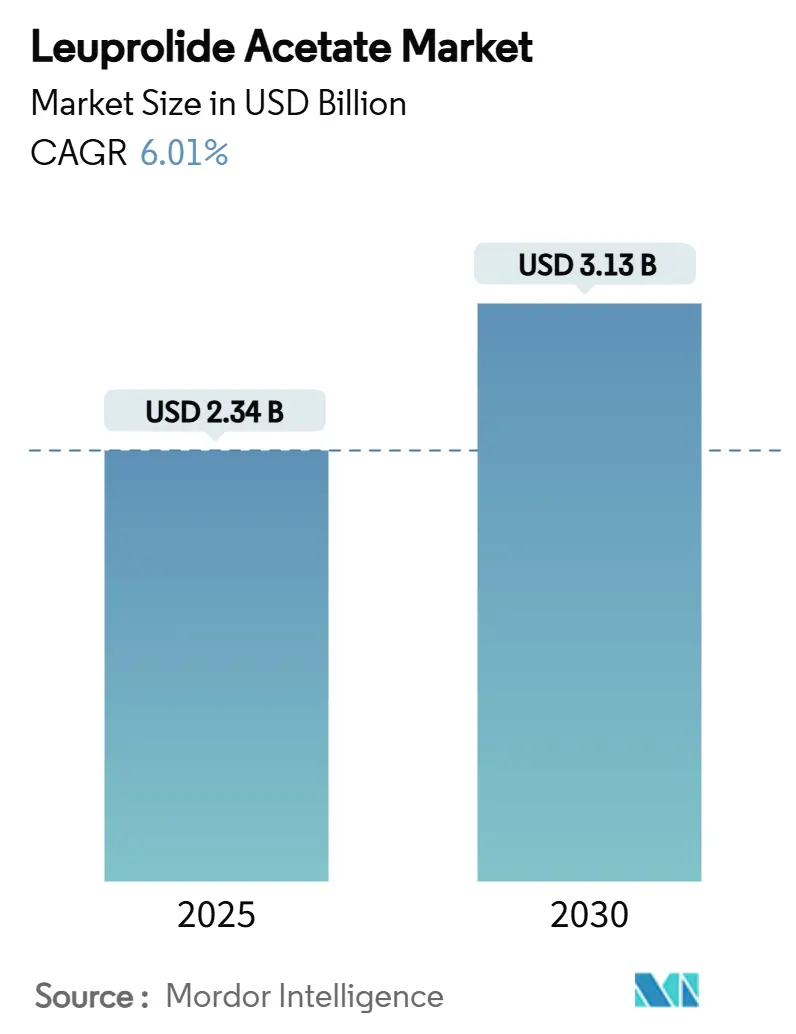

| Market Size (2025) | USD 2.34 Billion |

| Market Size (2030) | USD 3.13 Billion |

| Growth Rate (2025 - 2030) | 6.01% CAGR |

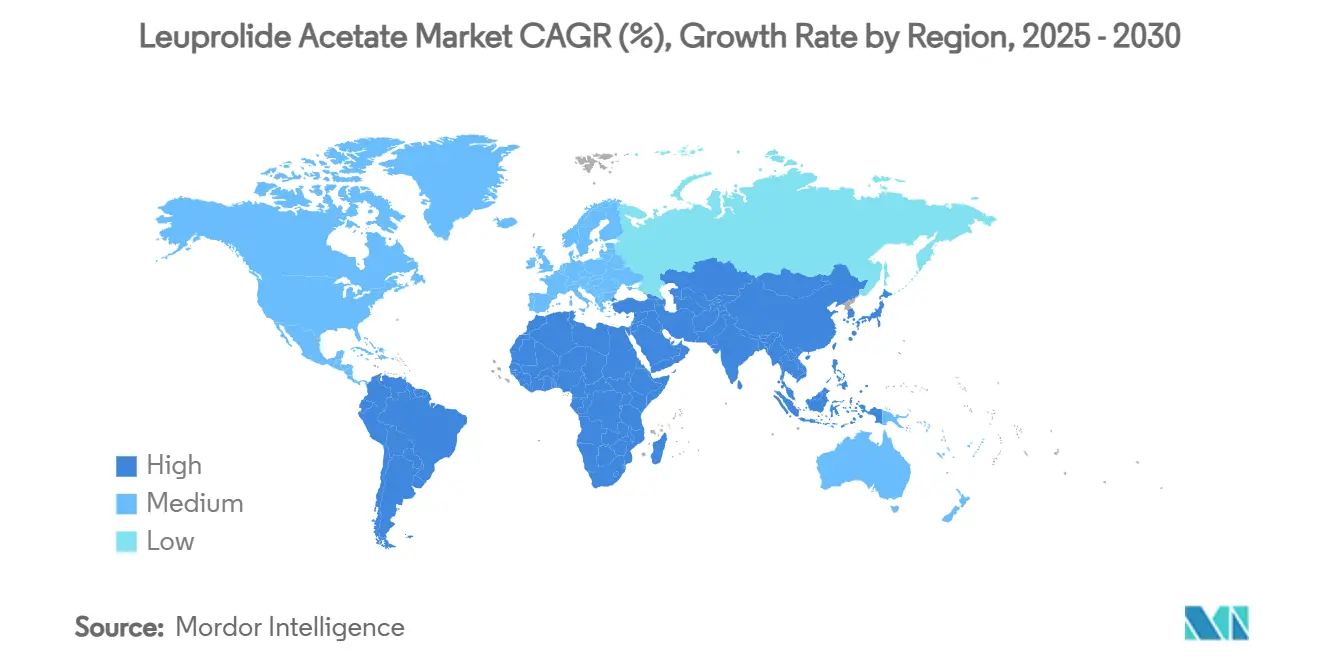

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Leuprolide Acetate Market Analysis by Mordor Intelligence

The leuprolide acetate market size is USD 2.34 billion in 2025 and is set to reach USD 3.13 billion by 2030, advancing at a 6.01% CAGR over the period. Sustained demand for hormone-dependent cancer therapies, growing use in assisted reproductive technology (ART), and continuous product-form innovation keep the leuprolide acetate market on a steady growth path. Intensifying generic entry—signaled by Cipla’s January 2025 Lupron Depot launch—has begun to narrow price differentials and is prompting brand owners to invest in extended-release formulations and combination products. Demand remains anchored in oncology, yet rising infertility treatment volumes, especially in Asia-Pacific, are giving the leuprolide acetate market new momentum. Longer-acting depot variants are capturing physician and payer interest as healthcare systems seek adherence gains and clinic-visit reduction. Meanwhile, stricter environmental rules on solvent emissions and sporadic peptide raw-material shortages are adding cost pressures that favor manufacturers with scale and vertically integrated supply chains.[1]3. U.S. Environmental Protection Agency, “Regulatory Impact Analysis for the Final New Source Performance Standards for the Synthetic Organic Chemical Manufacturing Industry,” epa.gov

Key Report Takeaways

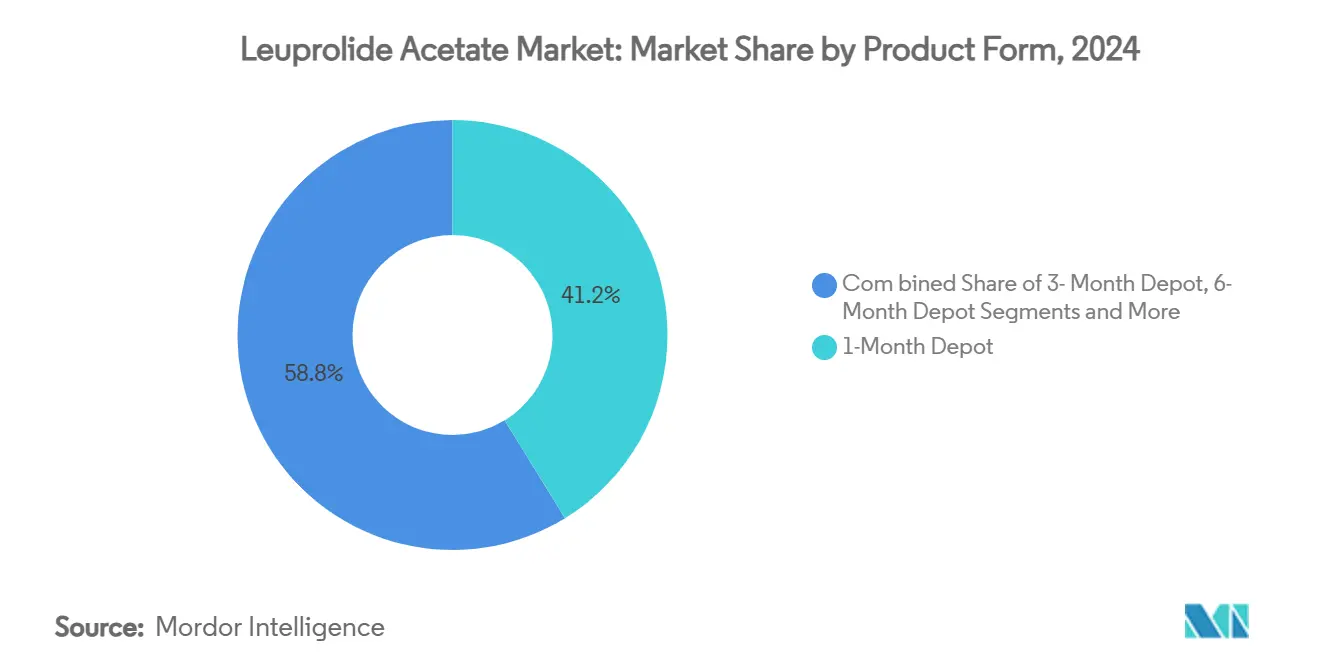

- By product form, the 1-month depot captured 41.23% of the leuprolide acetate market share in 2024; the 6-month depot is advancing at a 9.79% CAGR to 2030.

- By application, prostate cancer led with 46.55% revenue share in 2024, while assisted reproductive technology is forecast to expand at a 10.43% CAGR through 2030.

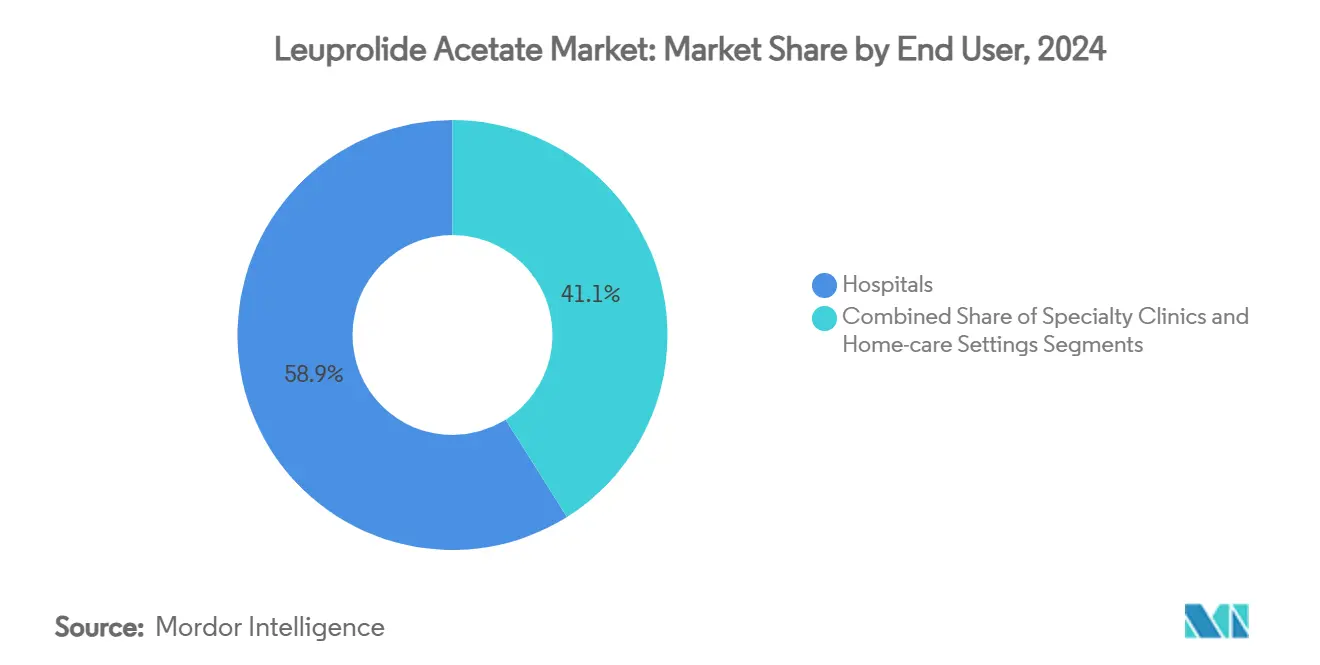

- By end-user, hospitals accounted for 58.93% of the leuprolide acetate market size in 2024 and specialty clinics are rising at an 8.93% CAGR through 2030.

- By distribution channel, hospital pharmacies held 56.72% share of the leuprolide acetate market size in 2024, whereas online pharmacies are growing at a 10.78% CAGR to 2030.

- By geography, North America commanded 33.58% share of the leuprolide acetate market size in 2024 and Asia-Pacific is the quickest-growing region at an 8.66% CAGR during 2025-2030.

Global Leuprolide Acetate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of hormone-dependent cancers | +1.2% | North America, Europe, Asia | Long term (≥ 4 years) |

| Growing adoption of GnRH-agonist therapy | +0.9% | Global | Medium term (2-4 years) |

| Expanding IVF and reproductive-health indications | +1.1% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Long-acting depot formulations boosting adherence | +0.8% | Global | Short term (≤ 2 years) |

| Microsphere delivery technology breakthroughs | +0.6% | North America, Europe | Long term (≥ 4 years) |

| Inclusion in emerging-market reimbursement lists | +0.7% | Asia-Pacific, Latin America, Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Hormone-Dependent Cancers

Prostate cancer prevalence is climbing as populations age, keeping oncology the largest slice of the leuprolide acetate market. The therapy is now routinely combined with next-generation androgen-receptor inhibitors, which raises treatment durations and reinforces demand. Wider screening programs and better diagnostic imaging expand the treated patient pool, while ongoing trials in antibody-drug conjugates create adjunct opportunities that further stabilize volume requirements. Reimbursement clarity across developed markets helps preserve high initiation rates, and guideline updates in Asia-Pacific are narrowing historic treatment-access gaps.

Growing Adoption of GnRH-Agonist Therapy

Healthcare providers continue to select GnRH agonists as first-line choices in central precocious puberty and endometriosis because of robust efficacy data and dosing flexibility. Oral GnRH antagonists have entered the scene, yet their presence boosts overall awareness of the GnRH pathway, indirectly supporting leuprolide uptake. In fertility preservation for oncology patients, the drug is gaining favor due to evidence showing ovarian function protection during chemotherapy, broadening its clinical footprint.[2]Boram Kim, “How to Preserve Fertility in Reproductive-Age Women With Cancer,” Journal of Clinical Medicine, mdpi.com

Expanding IVF & Reproductive-Health Indications

The fertility sector’s swift expansion is a clear tailwind for the leuprolide acetate market. Private-equity backing of 15% of ART clinics drives protocol standardization and technology upgrades that rely on GnRH agonist downregulation. Clinical data indicate improved pregnancy and implantation rates when agonist pretreatment precedes frozen embryo transfers, prompting protocol shifts in high-volume centers.[3]Haoying Hao, “The Effect of Gonadotropin-Releasing Hormone Agonist Downregulation in Conjunction With Hormone Replacement Therapy on Endometrial Preparation in Patients for Frozen–Thawed Embryo Transfer,” Frontiers in Medicine, frontiersin.org Rising infertility prevalence and corporate fertility benefits in Asia-Pacific add regional heft to demand.

Long-Acting Depot Formulations Improving Adherence

Six- and twelve-month depots cut clinic visits and have shown notable adherence gains versus monthly injections. Product pipelines feature self-aggregating microcrystal technology that permits high drug loading through small-gauge needles, easing administration anxiety and reducing injection-site reactions. Payers appreciate the logistics savings, while remote-monitoring add-ons are beginning to tie adherence metrics to outcome-based reimbursement models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent expiries and intensified generic rivalry | -1.8% | North America, Europe | Short term (≤ 2 years) |

| Adverse effects influencing compliance | -0.7% | Global | Medium term (2-4 years) |

| Peptide-grade raw-material supply constraints | -0.5% | Global | Short term (≤ 2 years) |

| Stricter solvent-use environmental regulations | -0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patent Expiries & Intensified Generic Rivalry

Cipla’s generic Lupron Depot launch in early 2025 is setting off a fresh price-erosion cycle. More filings are queued for Eligard generics as its patent fortress gradually weakens. Five dominant injectable generics houses control nearly half of US supply, suggesting coordinated competitive pressure that is hard for single-product originators to counter.

Adverse Effects Impacting Patient Compliance

Typical GnRH-agonist side effects—hot flashes, bone-density loss, cardiovascular risk—continue to prompt discontinuation, even in oncology settings where survival benefit is clear. Oral antagonists such as relugolix, which demonstrate quicker testosterone recovery, are capitalizing on this concern and may capture switch patients over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Extended Formulations Strengthen Adoption

The 1-month depot remains the volume leader and generated 41.23% of leuprolide acetate market revenue in 2024, anchored in well-established oncology dosing cycles. Uptake of the 6-month depot is outpacing the total leuprolide acetate market at a 9.79% CAGR as physicians align with payer goals to cut infusion-center visits and enhance adherence. Immediate-release injections still serve niche roles requiring rapid testosterone suppression, whereas 3-month depots offer a midpoint for patients needing tighter monitoring. Emerging 12-month depots illustrate the direction of innovation but await broader clinical familiarity and regulatory endorsement.

MIT’s microcrystal delivery platform shows that smaller-gauge needles and high drug-loading are realistic, advancing convenience without compromising steady-state exposure. Manufacturers are optimizing PLGA matrices to tailor release curves, paving the way for personalized depot dosing. Those technological dividends should help originators protect share once generics erode price tiers, while giving providers a tangible benefit to justify switch decisions.

By Application: Oncology Dominance and Fertility Upside

Oncology keeps the top spot with prostate cancer delivering 46.55% of 2024 sales thanks to guideline entrenchment and high diagnostic penetration in developed markets. ART is the breakout category, growing 10.43% annually as delayed parenthood and better insurance cover fuel IVF volume, notably in China and India. Endometriosis and uterine fibroid therapy remain mid-pack contributors whose steady uptake stems from rising disease awareness. Central precocious puberty, though a smaller market, secures stable demand through pediatric endocrinology circles.

Clinical studies show that two-to-three-month pre-treatment with leuprolide before frozen embryo transfer pushes live-birth odds higher, expanding its role beyond classic long protocols. For endometriosis-related implantation failure, long-course GnRH agonist therapy yielded 37.50% live-birth rate versus 13.04% in controls, underscoring its reproductive-medicine value.

By End-user: Hospital Foundation with Specialty-Clinic Momentum

Hospitals accounted for 58.93% of leuprolide acetate market size in 2024 due to their central role in oncology infusion and reproductive surgery. Specialty clinics, particularly fertility centers and outpatient oncology hubs, are scaling faster at an 8.93% CAGR because they combine procedure volumes with high-touch patient management. Home-care remains nascent; yet policy moves to reimburse nurse-supervised home injections could nudge adoption.

Private-equity roll-ups in fertility care give large clinic chains stronger procurement leverage, influencing brand-generic mix and accelerating protocol uniformity. Outpatient oncology networks adopting value-based contracts are gravitating toward long-acting depots when adherence data support lower total-care costs.

By Distribution Channel: Institutional Stronghold with Digital Upswing

Hospital pharmacies held 56.72% share in 2024, reflecting on-premise dispensing for in-clinic injections. Online pharmacies, however, are growing the quickest at 10.78% CAGR, helped by e-prescriptions, direct-to-patient shipping, and competitive generic pricing. Retail chains occupy the middle ground, serving both oncology follow-ups and reproductive-medicine patients who self-inject under telehealth guidance.

Specialized distributors are layering nurse hotlines and adherence tracking onto their service stack, turning complex injectable supply into a broader care-coordination offering. The proposed US PPAHI Act, which targets higher home-infusion reimbursement, could unlock wider mail-order uptake for depot kits.

Geography Analysis

North America retains leadership with a 33.58% leuprolide acetate market share anchored in robust reimbursement and prostate-cancer screening programs. FDA review of a new 3-month mesylate formulation, scheduled for decision in August 2025, signals continued product refreshment that can lengthen brand lifecycles. Environmental regulations are pushing some bulk production outside the United States, but domestic fill-finish capacity still secures rapid supply to clinics.

Asia-Pacific is the growth engine, rising at an 8.66% CAGR through 2030. China’s healthcare-expenditure climb and friendlier reimbursement negotiations make it a priority market for both originators and generic entrants. Rising secondary infertility tied to polycystic ovary syndrome is lifting IVF cycles and, by extension, leuprolide demand in controlled ovarian hyperstimulation. Government-run cancer early-detection campaigns in South Korea and Japan are likewise lifting GnRH-agonist prescriptions.

Europe shows steady uptake under universal-care systems that favor evidence-based treatments. Recent data from European clinics validate leuprolide’s role in fertility preservation for oncology patients, an area earmarked for reimbursement expansion. Manufacturers active in the region are investing in greener synthesis lines to align with upcoming solvent-emission caps, positioning sustainability as a competitive differentiator.

Competitive Landscape

The leuprolide acetate market remains moderately concentrated. AbbVie, Takeda, Tolmar, and AstraZeneca dominate brands, yet generics from Cipla, Fresenius Kabi, Viatris, Teva, and Hikma are fast tightening price spreads. Cipla’s US entry in 2025 is a turning point that spurs payer preference for generics and pressures brand contracts. Originators respond with lifecycle-extension moves such as six- and twelve-month depots, combination packs, and digital adherence tools.

Strategic acquisitions underscore the importance of secure supply. Hims & Hers bought a US peptide facility in February 2025 to shore up raw-material access and speed prototype batches. AbbVie is placing longer-term bets on dual-targeted antibody-drug conjugates for castration-resistant prostate cancer, which could become adjuncts to leuprolide rather than replacements. Manufacturers able to prove uninterrupted delivery, solvent-reduced processes, and patient-reported-outcome advantages are best positioned to hold formulary slots.

Barriers to entry stay considerable because depot production demands sterile microsphere expertise and validated cold-chain logistics. Nonetheless, the lure of solid oncology and infertility volumes continues to attract injectables specialists, gradually lowering concentration and amplifying competition.

Leuprolide Acetate Industry Leaders

AbbVie Inc.

Takeda Pharmaceutical Co. Ltd.

Tolmar Inc.

Teva Pharmaceutical Industries Ltd.

Fresenius Kabi AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Avenacy launched leuprolide acetate injection in the United States as a therapeutic generic equivalent to Lupron, expanding advanced-prostate-cancer treatment options.

- August 2024: Meithel Pharmaceuticals introduced a 14 mg leuprolide acetate injection kit, enlarging the immediate-release segment.

Global Leuprolide Acetate Market Report Scope

| Immediate-Release Injection |

| 1-Month Depot |

| 3-Month Depot |

| 6-Month Depot |

| 12-Month Depot |

| Prostate Cancer |

| Endometriosis |

| Uterine Fibroids |

| Central Precocious Puberty |

| Assisted Reproductive Technology (IVF) |

| Hospitals |

| Specialty Clinics |

| Home-care Settings |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Form | Immediate-Release Injection | |

| 1-Month Depot | ||

| 3-Month Depot | ||

| 6-Month Depot | ||

| 12-Month Depot | ||

| By Application | Prostate Cancer | |

| Endometriosis | ||

| Uterine Fibroids | ||

| Central Precocious Puberty | ||

| Assisted Reproductive Technology (IVF) | ||

| By End-user | Hospitals | |

| Specialty Clinics | ||

| Home-care Settings | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current size of the leuprolide acetate market?

The leuprolide acetate market size is USD 2.34 billion in 2025 and is projected to climb to USD 3.13 billion by 2030.

2. Which application area is growing the fastest?

Assisted reproductive technology is the quickest-expanding segment, registering a 10.43% CAGR through 2030.

3. Why are long-acting depot formulations gaining popularity?

Six- and twelve-month depots improve adherence, cut clinic visits, and align with payer preferences for lower total-care costs.

4. Which region will contribute most to future growth?

Asia-Pacific is forecast to deliver the highest incremental growth, advancing at an 8.66% CAGR during the outlook period.

5. How is generic competition affecting prices?

Cipla’s 2025 generic entry has started a price-compression phase as more manufacturers line up to launch bioequivalent products, prompting formulary shifts.

Page last updated on: