Legacy Modernization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

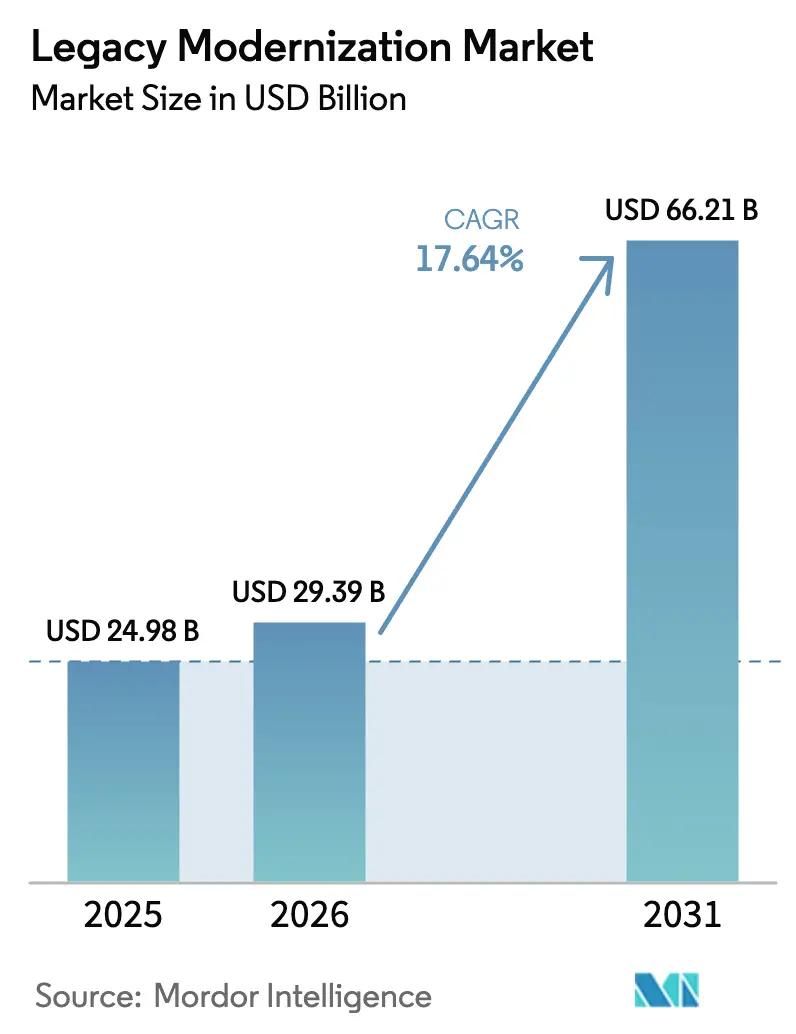

| Market Size (2026) | USD 29.39 Billion |

| Market Size (2031) | USD 66.21 Billion |

| Growth Rate (2026 - 2031) | 17.64% CAGR |

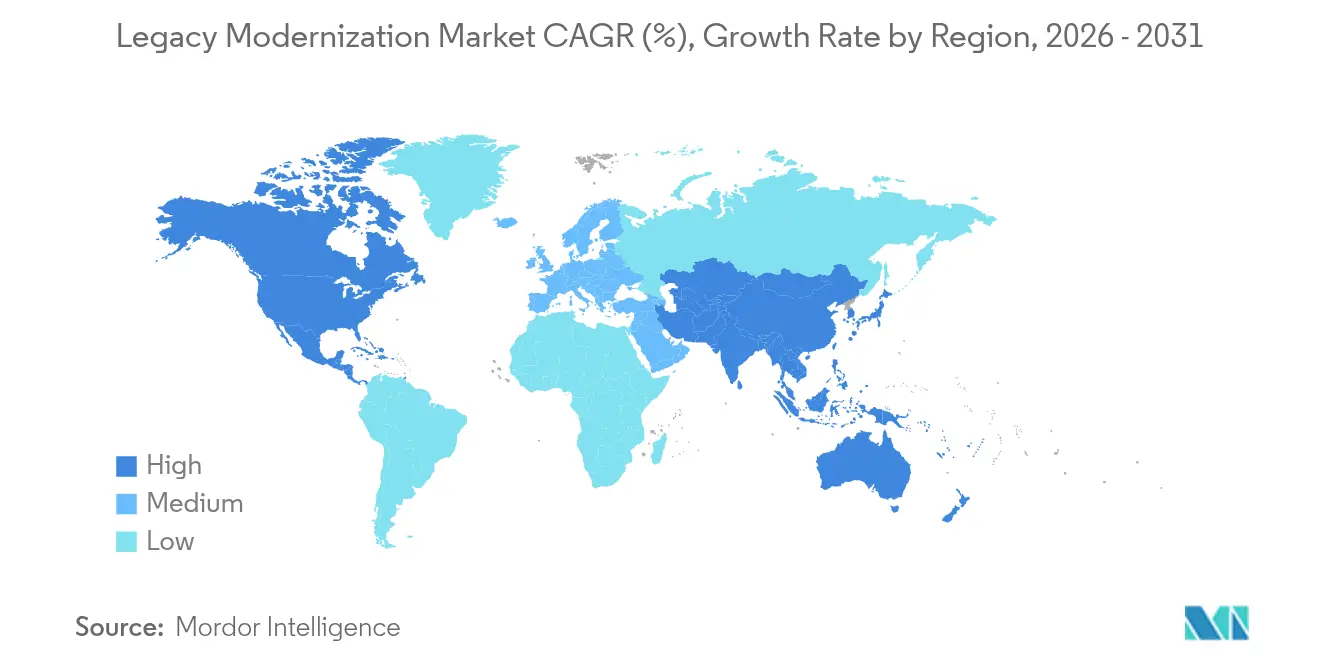

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

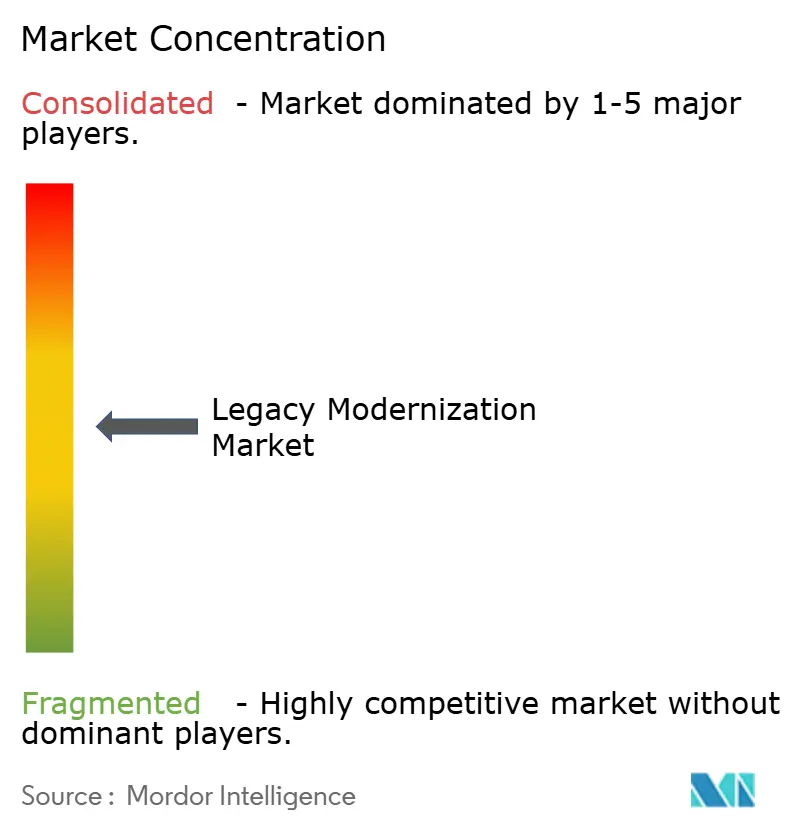

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Legacy Modernization Market Analysis by Mordor Intelligence

Legacy modernization market size in 2026 is estimated at USD 29.39 billion, growing from 2025 value of USD 24.98 billion with 2031 projections showing USD 66.21 billion, growing at 17.64% CAGR over 2026-2031. The sharp rise underscores the urgency to resolve mounting technical debt while unlocking cloud-native agility and artificial-intelligence-driven efficiencies. Regulatory mandates that demand resilient, real-time digital reporting push organizations to act, while competitive pressures reward firms that shift from reactive maintenance to proactive re-architecting. The dominance of cloud deployment, rapid progress in GenAI-assisted code conversion, and the steady inflow of capital toward re-architecting approaches together reshape investment priorities across every major vertical. As modernization accelerates, services-led engagements remain pivotal because enterprises require domain expertise that mitigates business-risk exposure during complex cut-over windows. Partnerships between systems integrators and hyperscale cloud providers further reinforce the momentum by coupling deep industry knowledge with scalable platform capabilities.

Key Report Takeaways

- By component, Services led with 58.05% of the Legacy modernization market share in 2025; software is forecast to post a 16.09% CAGR through 2031.

- By deployment type, Cloud models captured 67.10% revenue share of the Legacy modernization market in 2025, while hybrid and cloud-first architectures together are advancing at an 17.98% CAGR to 2031.

- By modernization approach, Re-platforming held 31.85% share of the Legacy modernization market size in 2025; re-architecting is projected to expand at 22.74% CAGR between 2026-2031.

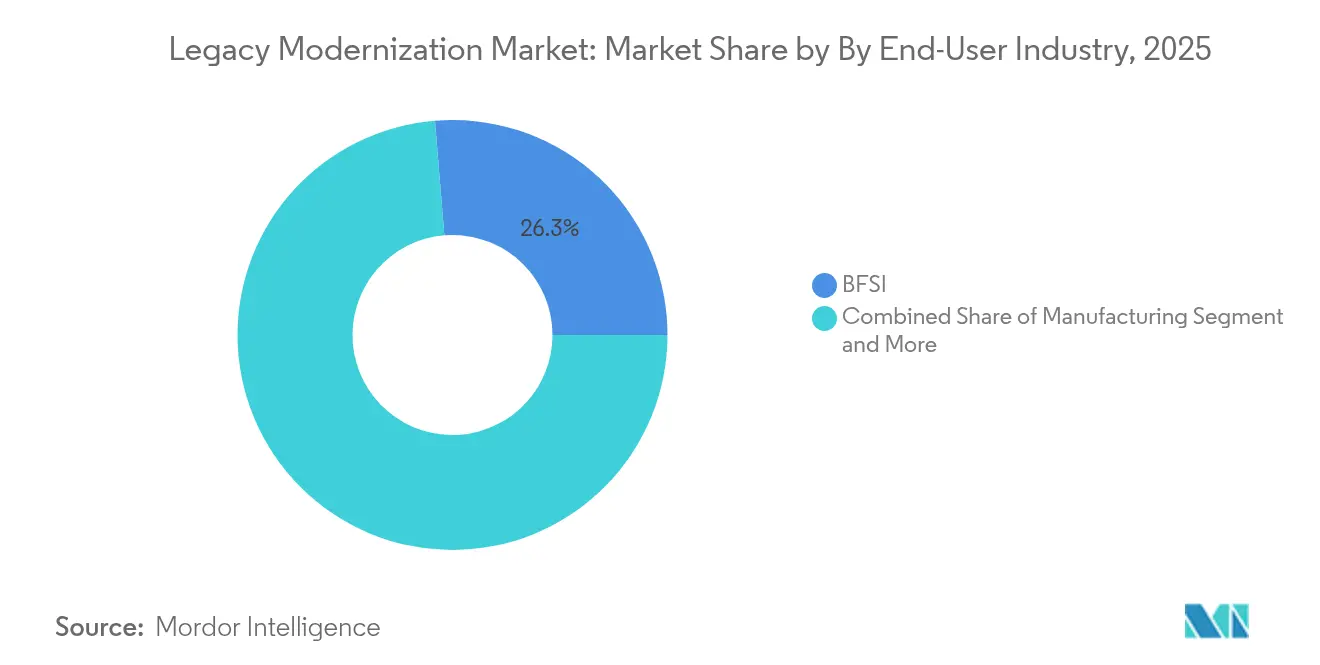

- By end-user industry, BFSI accounted for 26.30% share of the Legacy modernization market size in 2025, whereas healthcare applications are set to grow at 18.19% CAGR through 2031.

- By organization size, Large enterprises retained 65.10% of the Legacy modernization market share in 2025; small and medium enterprises are progressing at a 17.52% CAGR over the same period.

- By geography, North America occupied 37.05% of overall 2025 revenue; Asia-Pacific is the fastest-growing region with a 15.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Legacy Modernization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native agility imperative | +3.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising technical debt of COBOL & mainframes | +2.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Regulatory push for digital resiliency | +2.1% | Global, with EU and US frameworks | Short term (≤ 2 years) |

| Surge in GenAI-assisted code conversion | +4.3% | Global, early uptake in North America & APAC | Medium term (2-4 years) |

| Carbon-reduction mandates on datacenters | +1.8% | EU and California initially, spreading globally | Long term (≥ 4 years) |

| M&A-driven system harmonisation deadlines | +2.5% | Global, concentrated in BFSI and healthcare | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Agility Imperative

Enterprises are steadily abandoning monolithic architectures because such systems cannot deliver the elastic scaling, microservices orientation, or API-first interoperability that customer-facing digital products now demand. A USD 1.1 billion multi-cloud agreement between Microsoft and Coca-Cola exemplifies how global brands fund aggressive modernization to support continuous deployment pipelines and worldwide reach[1]Microsoft Corporation, “Microsoft and Coca-Cola Expand Partnership to USD 1.1 billion,” news.microsoft.com. By adopting container orchestration and serverless execution, firms reduce release cycles from months to days, enabling near real-time personalization and data-driven decision-making. The trajectory intensifies as digital challengers erode incumbent market positions with faster product iteration. Consequently, the Legacy modernization market observes sustained preference for full re-architecting over incremental lift-and-shift movements.

Rising Technical Debt of COBOL and Mainframe Estates

Annual maintenance spending on aging COBOL estates now eclipses modernization investment in many large banks and insurers, a pattern vividly highlighted by Japan’s “2025 cliff” that flags systemic risk as veteran developers retire. Fujitsu’s work with Toyota, which cut system update time by 50% through GenAI-enabled transformation, proves that replacing brittle code bases is far cheaper than perpetuating them. With components and skills both scarce, each year of deferred action compounds operational risk and cost curves. As a result, boards increasingly treat modernization as a core resilience priority rather than an IT project, thereby boosting long-term demand for the Legacy modernization market.

Regulatory Push for Digital Reporting and Resiliency

New supervisory regimes oblige banks, healthcare networks, and public agencies to demonstrate real-time data integrity and disaster recovery. The EU Energy Efficiency Directive, for instance, forces data-center operators to install advanced monitoring that legacy infrastructure cannot support. In parallel, US banking oversight bodies require instant risk reporting, incentivizing cloud-native data lakes and automated compliance workflows. Penalties for non-conformance often dwarf modernization outlays, so many boards accelerate spending to avoid fines. This regulatory tailwind feeds directly into services pipelines within the Legacy modernization market.

Surge in GenAI-Assisted Code Conversion Tools

IBM experiments indicate that GenAI can trim mainframe modernization costs by up to 70% via automated code discovery, dependency mapping, and conversion. NTT DATA’s Smart AI Agent shows similar benefits by elevating legacy RPA bots into self-learning, intelligent agents that slash process latency across healthcare and automotive lines. These platforms preserve embedded business logic while yielding cleaner, cloud-ready code bases, thus shortening timelines and lowering skill-bar requirements. As licensing models get consumption-based, smaller firms now acquire capabilities once reserved for Fortune 500 budgets, widening the addressable pool for the Legacy modernization market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front migration cost and business risk | -2.1% | Global, most acute for SMEs | Short term (≤ 2 years) |

| Scarcity of legacy-language specialists | -1.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Sovereign-cloud and data-residency rules | -1.5% | EU, China, India | Medium term (2-4 years) |

| Licence-lock-in of niche ISV workloads | -1.2% | Global, especially in regulated verticals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Up-Front Migration Cost and Business Risk

Modernization budgets typically cover new infrastructure, tooling, integration, workforce reskilling, and detailed change-management programs. Legal and General committed to a seven-year data-center exit with Kyndryl, underlining capital outlays required even when green energy gains offset operational expense. Any disruption to mission-critical payroll, claims, or trading applications during cut-over can translate into financial penalties or brand erosion. Consequently, the Legacy modernization market must continually package risk-mitigation frameworks, phased deployment blueprints, and outcome-based commercial terms to reassure hesitant boards.

Scarcity of Legacy-Language Specialists

The global pool of COBOL programmers has been shrinking for a decade, inflating consulting day rates and elongating project schedules. Universities rarely teach mainframe-oriented curricula, and knowledge is often embedded in unstructured personal notes. Without structured hand-off, critical logic may be lost during staff transition, jeopardizing modernization timelines. Vendors now record knowledge artifacts and apply AI documentation builders to bridge the skills gap, but scarcity still dampens near-term velocity within the Legacy modernization market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Dominate Complex Transformations

Services controlled 58.05% of the Legacy modernization market in 2025, a lead rooted in the bespoke nature of multi-year transformation programs. Advisory road-mapping, ROI modeling, system integration, and managed transformation all converge to de-risk migrations that touch financial ledgers, patient records, or national tax systems. Automated tooling boosts productivity, yet enterprises still rely on domain specialists to orchestrate phased cutovers that safeguard business continuity.

Software, while smaller, is accelerating at a 16.09% CAGR. AI-augmented code analyzers, dependency discoverers, and automated pipeline generators are now embedded in platform-as-a-service suites. The Legacy modernization market size for software is predicted to broaden as subscription models eliminate large license fees and allow piecemeal adoption. The dynamic fosters tighter bonds between SI partners and ISVs who jointly offer packaged outcomes.

By Deployment Type: Cloud Transformation Accelerates

Cloud models captured 67.10% Legacy modernization market share in 2025. Enterprises favor public or multi-cloud footprints that deliver elasticity, global reach, and managed security services without capex overhead. Regional requirements for sensitive workloads produce hybrid patterns, but even these architectures pipe telemetry into public-cloud analytics engines to unlock data insights.

The Legacy modernization market size associated with pure public-cloud deployments is expanding at an 17.98% CAGR, helped by ever-growing hyperscale regions and interconnect agreements such as the Microsoft-Oracle “database-on-Azure” expansion that now spans 15 global zones. Financial, gaming, and healthcare providers leverage burst capacity for seasonal workloads while ensuring regulatory compliance via sovereign regions or confidential computing enclaves.

By Modernization Approach: Re-Architecting Gains Momentum

Re-architecting outpaces all other strategies with a 22.74% CAGR because enterprises now realize that long-term agility arises only when core logic moves to microservices and domain-driven designs. Although re-platforming retained 31.85% share of the Legacy modernization market size in 2025, it is increasingly a transitional phase toward deeper refactoring.

Tool chains that automate service-boundary extraction and schema decomposition lift re-architecting success rates. Kyndryl’s Mainframe Modernization Center of Excellence, built on Amazon Web Services in Malaysia, pairs these tools with extensive mainframe know-how, reducing elapsed project time while maintaining mission-critical SLAs. Where workloads are non-differentiating, off-the-shelf SaaS replacements cut cost and speed execution, freeing budget for high-value domain logic rewrites.

By End-User Industry: Healthcare Leads Digital Transformation

Healthcare is projected to surge at 18.19% CAGR as electronic health record mandates and telemedicine adoption demand interoperable, real-time platforms. Providers such as Kaleida Health saved USD 5–10 million by consolidating siloed systems and improving patient experience through unified portals. The Legacy modernization market benefits such as compliance frameworks like HIPAA or GDPR require immutable audit trails and fine-grained data-access controls.

BFSI, while expanding more slowly, still accounts for the largest revenue slice because mammoth transaction volumes, geopolitical sanctions screening, and Basel IV risk models compel core-banking and capital-markets modernization. Manufacturing, retail, and telecoms sustain steady pipelines as they roll out digital twins, omnichannel commerce, and 5G-edge orchestration—all reliant on freshly modular back ends.

By Organization Size: SMEs Accelerate Adoption

Large enterprises commanded 65.10% revenue in 2025, yet SMEs are closing the gap by growing at 17.52% CAGR. Consumption-pricing, serverless models, and low-code platforms strip away barriers that once restricted modernization to firms with deep pockets. An SME can spin up a development sandbox, run an automated COBOL analyzer, and pay solely for processing minutes, shifting spend to operating expense. Even so, the Legacy modernization industry observes persistent complexity inside conglomerates whose estates span decades of MandA. Program governance, change-management offices, and board-level steering committees are staples for Fortune 500 clients. Vendors therefore field dual go-to-market motions: fast-cycle SMB toolkits and enterprise-grade, multi-phase programs with outcome-based milestones.

Geography Analysis

North America held a commanding 37.05% revenue share in 2025, reflecting an installed base of mainframes, early cloud adoption, and strict federal oversight that rewards resilient architecture. US regulators such as the Securities and Exchange Commission now impose near real-time reporting for capital markets, forcing cloud-native data warehousing and analytics to the foreground. As a result, the Legacy modernization market continues to enjoy high average contract values and long-term managed-services renewals across the region. Asia-Pacific is advancing at 15.71% CAGR, propelled by Japan’s looming skills cliff, India’s national digital-public-platform initiatives, and Southeast Asia’s greenfield FinTech adoption. NTT DATA’s USD 1.5 billion data-center expansion and Fujitsu’s GenAI-assisted Toyota engagement illustrate home-grown innovation meeting global best practice. Government stimulus around smart manufacturing and digital trade corridors further injects capital into the Legacy modernization market. Europe maintains strong momentum as GDPR, the Digital Markets Act, and sustainability directives overlap. The EU Energy Efficiency Directive obliges datacenters to document power usage effectiveness and carbon emissions, a task achievable only with modern telemetry systems. Sovereign-cloud frameworks in Germany, France, and Spain steer many modernization roadmaps toward hybrid designs that keep sensitive data in-region while exploiting public-cloud analytics at scale. The Middle East and Africa, though smaller today, are accelerating thanks to national diversification agendas that prioritize digital government and cashless commerce.

Competitive Landscape

The Legacy modernization market remains moderately fragmented. Top systems integrators—IBM, Accenture, Cognizant, TCS, and Infosys—anchor global deals, but niche specialists such as Kyndryl and Rocket Software carve out depth around mainframe transformation. These firms reinforce their positions through strategic alliances with hyperscalers; Microsoft’s Azure Mainframe Modernization service, for example, plugs directly into Kyndryl delivery frameworks to assure SLAs across entire application stacks[2] Microsoft Azure, “Mainframe Modernization Service Overview,” azure.microsoft.com.

Hyperscalers are now embedding professional-services units within deal teams, raising competitive intensity. Oracle and Google Cloud emphasize low-latency interconnects that shrink data-transfer fees and simplify hybrid orchestration for regulated workloads. Meanwhile, automation-first disruptors provide outcome-based pricing that ties vendor margin to time-to-value, challenging traditional day-rate engagements common in the Legacy modernization industry.

Tool vendors pursue vertical specialization to escape price compression. OpenText’s Secure Cloud Evolution targets managed service providers that resell modernization bundles to mid-market clients. Rocket Software’s acquisition of OpenText’s Application Modernization unit for USD 2.275 billion strengthened its catalog of compiler emulators and migration accelerators, giving customers more choice among out-of-the-box code converters. Overall, the fluid landscape rewards vendors that blend deep domain IP, AI-assisted automation, and cloud-native delivery.

Legacy Modernization Industry Leaders

IBM Corporation

Accenture plc

Cognizant Technology Solutions Corporation

Infosys Limited

Tata Consultancy Services Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NTT DATA unveiled its Smart AI Agent ecosystem, converting legacy RPA bots into autonomous agents across healthcare, automotive, and financial domains.

- May 2025: NTT DATA agreed to acquire 58.7% of GHL Systems Berhad to deepen omnichannel payment modernization across ASEAN.

- March 2025: Microsoft and Oracle added five new regions to their joint Oracle Database on Azure offering, opening the service to European users.

- January 2025: NTT DATA committed more than USD 10 billion to expand its Global Data Centers footprint, targeting a 20% annual growth rate.

Global Legacy Modernization Market Report Scope

Organizations are undertaking legacy modernization to revitalize outdated software applications and systems. This essential process aligns these technologies with today's industry standards and businesses' evolving needs.

The study tracks the revenue accrued through the sale of the legacy modernization software and services by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

Legacy modernization market is segmented by component (software, services), by deployment type (on-premises, cloud), by end-user industry (BFSI, manufacturing, healthcare, IT and telecommunication, retail, other industry vertical), by geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Software |

| Services |

| On-premises |

| Cloud |

| Re-hosting |

| Re-platforming |

| Re-architecting |

| Re-factoring |

| Replacement / COTS |

| BFSI |

| Manufacturing |

| Healthcare |

| IT and Telecommunications |

| Retail and E-commerce |

| Government and Public Sector |

| Others |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| By Component | Software | ||

| Services | |||

| By Deployment Type | On-premises | ||

| Cloud | |||

| By Modernization Approach | Re-hosting | ||

| Re-platforming | |||

| Re-architecting | |||

| Re-factoring | |||

| Replacement / COTS | |||

| By End-User Industry | BFSI | ||

| Manufacturing | |||

| Healthcare | |||

| IT and Telecommunications | |||

| Retail and E-commerce | |||

| Government and Public Sector | |||

| Others | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current value of the Legacy modernization market?

The market is valued at USD 29.39 billion in 2026 and is projected to grow rapidly at a 17.64% CAGR.

Which deployment model leads the Legacy modernization market?

Cloud deployment holds 67.10% market share, driven by demand for scalable, distributed infrastructure.

Why is re-architecting gaining traction over lift-and-shift strategies?

Re-architecting unlocks long-term agility by enabling microservices and API-first designs, supporting faster release cycles and better resiliency.

Which industry vertical is expanding fastest in modernization spending?

Healthcare is forecast to advance at 18.19% CAGR as digital-health mandates push for interoperable, real-time platforms.

What is the primary restraint hampering modernization projects?

High up-front migration costs and associated business-risk concerns remain the main barriers, particularly for small and mid-sized enterprises.

Which region will add the most incremental revenue by 2031?

Asia-Pacific, growing at 15.71% CAGR, is expected to contribute the largest incremental gains due to leapfrog modernization in Japan, India, and Southeast Asia.

Page last updated on: