Ambulatory Cardiac Monitoring Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

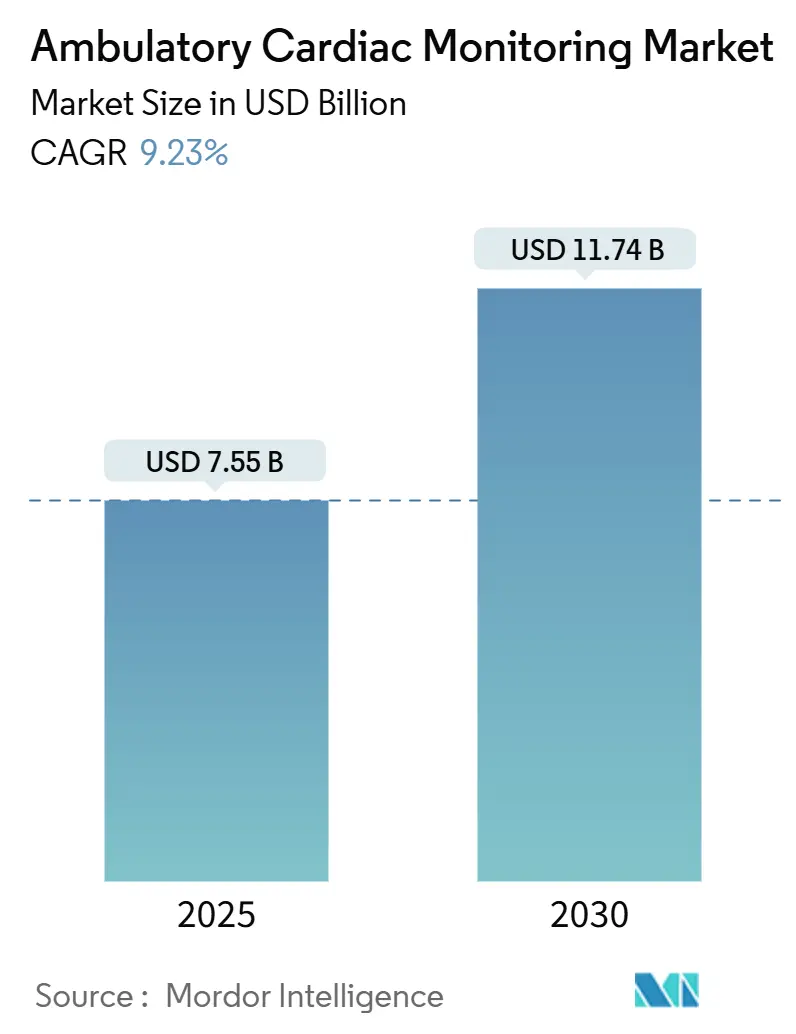

| Market Size (2025) | USD 7.55 Billion |

| Market Size (2030) | USD 11.74 Billion |

| Growth Rate (2025 - 2030) | 9.23% CAGR |

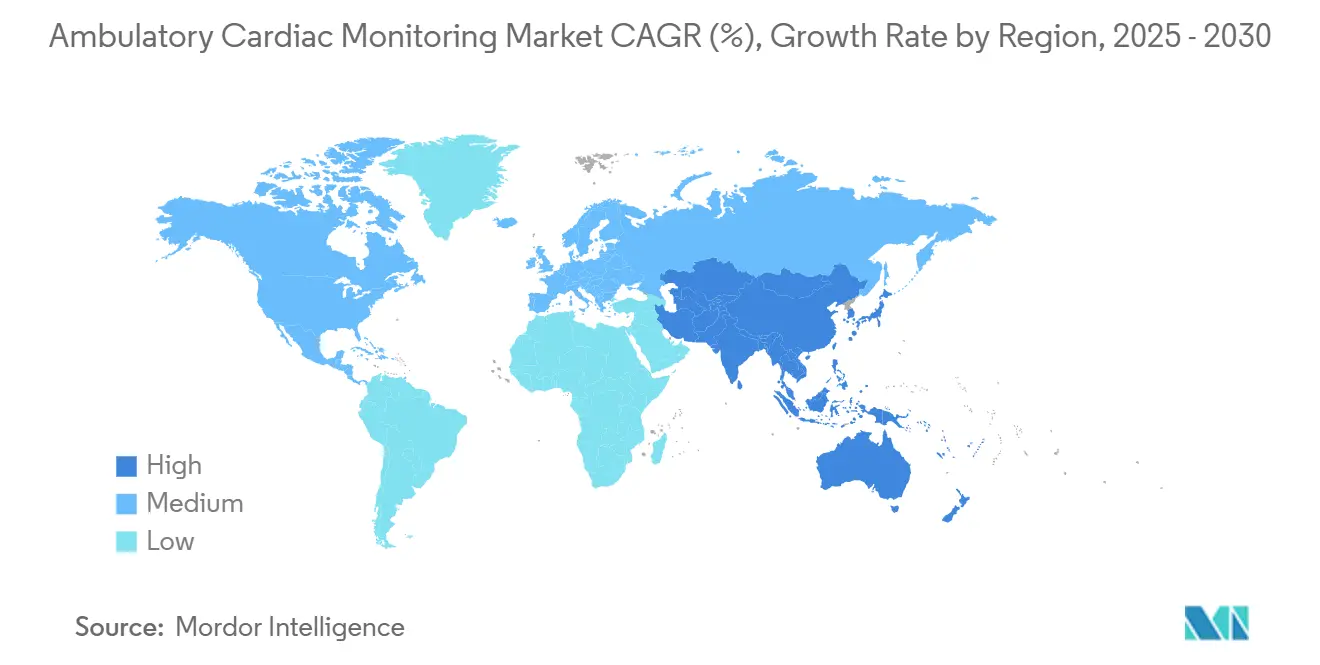

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ambulatory Cardiac Monitoring Market Analysis by Mordor Intelligence

The ambulatory cardiac monitoring market size reached USD 7.55 billion in 2025 and is on track to attain USD 11.74 billion by 2030, reflecting a 9.23% CAGR. Advances in artificial-intelligence diagnostics, the worldwide shift toward preventive care, and expanding reimbursement pathways are reinforcing this growth. Continuous monitoring is replacing episodic checks, while 5G connectivity and edge analytics bring real-time electrocardiogram (ECG) insights to clinicians. Asia-Pacific delivers the fastest regional pace, propelled by Japan’s early adoption of AI-enabled monitors and India’s expanding digital health ecosystem. Device miniaturization, home-care adoption, and hybrid consumer-clinical platforms continue to widen the ambulatory cardiac monitoring market opportunity.

Key Report Takeaways

- By device type, ECG devices led with 37.64% of the ambulatory cardiac monitoring market share in 2024; mobile cardiac telemetry is forecast to grow at 11.02% CAGR through 2030.

- By service provider, OEM remote monitoring held 38.29% share of the ambulatory cardiac monitoring market size in 2024, whereas Independent Diagnostic Testing Facilities are expanding at 9.97% CAGR to 2030.

- By indication, atrial fibrillation accounted for 59.73% share of the ambulatory cardiac monitoring market size in 2024 and is advancing at 9.45% CAGR to 2030.

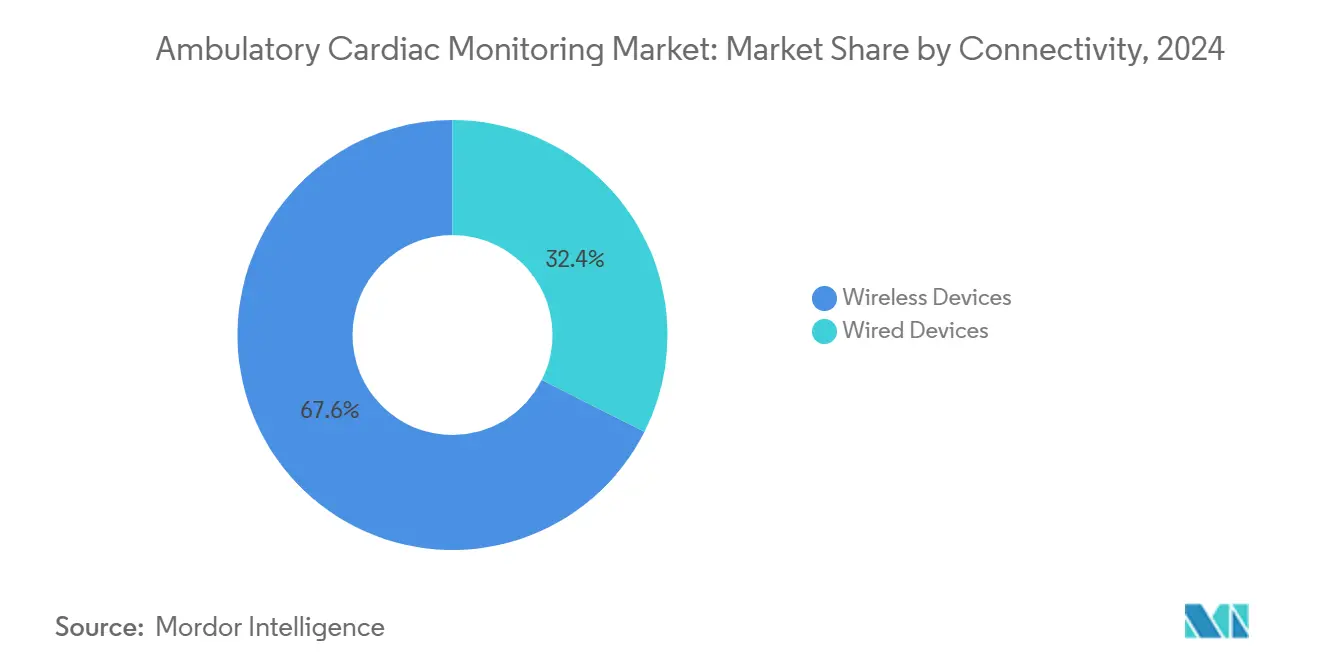

- By connectivity, wireless systems dominated with 67.58% of ambulatory cardiac monitoring market share in 2024 and maintain a 9.68% CAGR outlook.

- By end-user, hospitals commanded 47.01% share of the ambulatory cardiac monitoring market size in 2024; home-care settings post the fastest 10.31% CAGR through 2030.

- By geography, North America led with 43.38% share in 2024, and Asia-Pacific is forecast to be the fastest-growing region, expanding at a 10.24% CAGR to 2030.

Global Ambulatory Cardiac Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CVD & arrhythmia prevalence | +2.1% | North America, Europe, Global | Long term (≥ 4 years) |

| Miniaturization & AI-enabled devices | +1.8% | Asia-Pacific hubs, Global | Medium term (2-4 years) |

| Growth of remote patient monitoring models | +1.6% | North America, European Union, Asia-Pacific | Medium term (2-4 years) |

| Integration with consumer wearables & APIs | +1.2% | Developed markets, Global | Short term (≤ 2 years) |

| Expansion of IDTF reimbursement | +0.9% | North America, European Union | Medium term (2-4 years) |

| Proliferation of 5G & edge-computing | +0.7% | Asia-Pacific core, spill-over to North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising CVD & Arrhythmia Prevalence

Atrial fibrillation already drives 59.73% of monitoring use cases, and more than 33 million people live with the disorder worldwide. Aging populations and lifestyle risks intensify demand for long-term surveillance. Abbott’s CE-marked Assert-IQ insertable monitor, offering six-year battery life, illustrates device responses to this epidemiologic pressure[1]Abbott Newsroom Staff, “Abbott Receives CE Mark for Its Groundbreaking Assert-IQ Insertable Cardiac Monitor, Expanding Availability of Long-Term Monitoring for Irregular Heart Rhythms,” Abbott Newsroom, abbott.com. Continuous data streams underpin the 9.23% CAGR as care models migrate from reactive treatment to proactive detection.

Miniaturization & AI-enabled Devices

Clinical-grade accuracy now fits in patch-based wearables, while machine-learning models interpret rhythms in real time. Medtronic’s AI initiative for heart-disease prediction exemplifies this pivot from rhythm capture to risk forecasting. Embedded analytics also cut false positives that fuel alert fatigue among clinicians, lifting both provider confidence and patient adherence.

Growth of Remote Patient Monitoring Models

COVID-19 cemented remote patient monitoring as standard practice. The American Heart Association’s 2024 statement on data interoperability stresses that device data must flow directly into electronic records[2]Antonis A. Armoundas, “Data Interoperability and Harmonization in Cardiovascular Genomic and Precision Medicine,” American Heart Association Journals, ahajournals.org. Value-based care contracts amplify interest because continuous monitoring reduces readmissions and cost of care.

Integration with Consumer Wearables & Cloud ECG APIs

Diagnostic-grade ECG outputs from consumer devices such as Apple Watch now post 94.8% sensitivity and 95% specificity for atrial fibrillation detection[3]Sufyan Shahid, “Diagnostic Accuracy of Apple Watch Electrocardiogram for Atrial Fibrillation: A Systematic Review and Meta-Analysis,” JACC: Advances, jacc.org. Cloud APIs let physicians pull this data directly into clinical dashboards, broadening coverage while generating rich datasets for algorithm refinement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Implant/patch-related infection & skin issues | -1.4% | Global, higher in humid regions | Short term (≤ 2 years) |

| Price-sensitive procurement & gaps | -1.1% | Emerging economies, selective impact elsewhere | Medium term (2-4 years) |

| Clinician alert fatigue | -0.8% | High-volume systems worldwide | Medium term (2-4 years) |

| Cyber-security & data-privacy risks | -0.6% | Global, stricter in European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Implant/Patch-related Infection & Skin Issues

Contact dermatitis linked to methacrylate-based adhesives remains a well-documented barrier. FDA adverse-event files list pruritus, burning, and allergic responses for multiple wearables. Hypoallergenic polymers are under development, yet patients in humid climates or with sensitive skin still face limited wearing time.

Price-sensitive Procurement & Reimbursement Gaps

Many emerging-market health budgets favor basic care, and reimbursement coding complexity can delay device deployment. Where private insurers require extensive prior authorization, access slows. Providers, therefore, weigh clinical benefit against administrative burden, impacting adoption velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: ECG Supremacy Amid Growing MCT Uptake

ECG devices held 37.64% of ambulatory cardiac monitoring market share in 2024, underpinning diagnostic workflows across care settings. Mobile cardiac telemetry, though smaller today, is accelerating at 11.02% CAGR. The ambulatory cardiac monitoring market size for ECG remains buoyant as AI firmware lifts diagnostic yield, while implantable loop recorders extend surveillance windows to six years. A technology migration toward patch-free sensors signals future disruption but has yet to displace ECG’s volume leadership. Continuous algorithm updates embedded in hardware differentiate vendors and mitigate clinician alert fatigue.

Meanwhile, mobile telemetry combines real-time transmission and cloud analytics, allowing automatic alerting for high-risk events. This immediacy aligns with hospital at-home models that depend on rapid clinical escalation pathways. Suppliers bundling telemetry hardware with interpretation services widen margins and reduce provider onboarding friction, sustaining segment growth.

By Service Provider: OEM Depth vs. IDTF Agility

OEM-linked platforms delivered 38.29% share of the ambulatory cardiac monitoring market size in 2024, reflecting integrated device-plus-service offerings. Independent Diagnostic Testing Facilities chart a 9.97% CAGR by providing cost-efficient interpretations, scalable staffing, and turnkey reimbursement expertise. Hospitals, while still major users, increasingly outsource to specialized providers to curb capital outlays.

Consolidation is reshaping this arena. PaceMate’s pickup of Medtronic’s Paceart Optima workflow tech reinforces IDTF capabilities and positions the firm as a one-stop data-management vendor. As reimbursement clarity strengthens, new IDTF entrants will likely focus on sub-specialty niches such as pediatric arrhythmia monitoring or heart-failure prognostics, elevating competitive differentiation.

By Indication: Atrial fibrillation anchors diagnostic demand

Atrial fibrillation accounted for 59.73% of ambulatory cardiac monitoring market share in 2024, reflecting the arrhythmia’s high prevalence and its established link to stroke prevention strategies. Because guideline-directed therapy now emphasizes rhythm documentation before anticoagulation decisions, clinicians rely on continuous monitoring rather than short office ECGs. The sub-segment maintains a 9.45% CAGR to 2030 as algorithms improve detection of paroxysmal episodes that conventional Holter studies often miss. Unexplained syncope remains a secondary focus, yet its case volume is smaller and growth steadier because diagnosis frequently resolves after shorter monitoring windows.

Manufacturers increasingly embed machine-learning models that separate true atrial fibrillation from premature atrial contractions, reducing false alerts and supporting wider deployment in primary-care settings. Consumer wearables funnel rhythm data into clinical dashboards, creating a blended ecosystem where patients initiate many monitoring cycles themselves. Payers have begun covering extended monitoring periods when stroke-risk assessment is documented, further lifting adoption. Together these forces secure atrial fibrillation’s dominance within the indication hierarchy through the forecast horizon.

By Connectivity: Wireless platforms reshape data workflows

Wireless devices commanded 67.58% of ambulatory cardiac monitoring market share in 2024, and the segment advances at a 9.68% CAGR on the strength of low-power radios, secure cloud links, and nationwide 5G rollouts. Real-time transmission allows care teams to triage actionable arrhythmias within minutes, a capability wired recorders cannot match without patient intervention. Hospitals are integrating edge-analytics gateways that preprocess incoming signals, trimming bandwidth while preserving clinical fidelity.

Improved battery chemistries now support multi-week wear times, eliminating daily charging routines that once hindered adherence. At the same time, cybersecurity frameworks based on zero-trust architectures help providers satisfy stringent privacy rules, especially in regions governed by GDPR. Interoperability standards let wireless patches hand off data to implantable devices or consumer smartwatches, creating continuous longitudinal records that enrich predictive models. As reimbursement codes increasingly recognize connected-care value, wired systems are expected to recede into niche roles such as intensive-care back-ups or rural facilities with limited broadband.

By End-User: Home-care adoption accelerates care decentralization

Hospitals retained 47.01% of ambulatory cardiac monitoring market size in 2024 thanks to established cardiac telemetry units and bundled interpretation services. Even so, home-care settings chart the fastest 10.31% CAGR to 2030 as value-based contracts reward providers for lowering readmissions. Remote monitoring technologies now arrive pre-configured, enabling patients to activate devices without in-clinic training and allowing clinicians to review dashboards during routine telehealth visits.

Third-party service firms supply around-the-clock monitoring centers that escalate only clinically relevant events, relieving hospital staff of data-overload concerns. Payers are broadening coverage for at-home cardiac surveillance when documentation shows reduced emergency visits, which encourages cardiology groups to ship devices directly to patients after virtual consultations. Ambulatory surgical centers and specialized rehab clinics also increase usage, but their growth remains moderate compared with home-care momentum. Collectively, the shift signals an enduring move toward decentralized cardiac care anchored by convenient, patient-managed monitoring.

Geography Analysis

North America commanded 43.38% of ambulatory cardiac monitoring market revenue in 2024, supported by established reimbursement and FDA’s progressive digital-health framework. Early adoption of cloud-based analytics and 5G-enabled telemetry streamlines clinical workflows and secures payer confidence. Canada’s publicly funded model similarly finances long-term monitoring for high-risk patients, and Mexico’s modernization programs are expanding ECG infrastructure across specialty clinics.

Asia-Pacific is projected to record a 10.24% CAGR, the most rapid worldwide. Japan’s 7.29% growth in digital health, paired with approval of iRhythm’s AI monitor, positions it as a regional pioneer. India’s health-tech market aims for USD 25 billion valuation by 2025, and OMRON’s focus on combined blood-pressure and ECG devices targets a hypertensive population exceeding 220 million. China and South Korea utilize robust electronics manufacturing ecosystems and state incentives to accelerate domestic device output.

Europe maintains a stable 9.18% CAGR. GDPR mandates stricter cyber-security controls, increasing development costs but enhancing patient trust. Germany, France, and the United Kingdom integrate ambulatory ECG into primary-care pathways, while the European Society of Cardiology validated 5G-enabled remote diagnostics in 2024, underscoring commitment to telecardiology. Middle East & Africa, at 9.83% CAGR, show rising investments in cardiac centers of excellence amid growing cardiovascular disease burdens.

Competitive Landscape

The ambulatory cardiac monitoring market shows moderate concentration. Abbott, Medtronic, and Boston Scientific dominate through broad portfolios and acquisition-driven expansion. Boston Scientific’s completed deals, culminating with Bolt Medical’s lithotripsy assets in January 2025, deepen cardiovascular breadth. Strategy focuses on embedding predictive analytics into hardware, integrating platforms with hospital information systems, and moving toward therapy-plus-diagnostics hybrids.

Emerging players secure significant venture capital. VitalConnect raised USD 100 million to expand its multi-parameter VitalPatch, while Octagos Health gathered USD 43 million for AI-enabled care coordination.

White-space R&D includes contactless RF sensing that attains clinical-grade rhythm tracking without electrodes, potentially redefining future form factors. Competitive advantage now hinges on algorithm quality, battery life, cybersecurity posture, and turnkey data-management services rather than price alone.

Ambulatory Cardiac Monitoring Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

GE HealthCare

Koninklijke Philips N.V.

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: VitalConnect raised USD 100 million to accelerate commercialization of its VitalPatch wearable heart monitor.

- January 2025: Biotricity partnered with B-Secur to launch a device-neutral cardiac monitoring platform that resolves interoperability limitations.

Global Ambulatory Cardiac Monitoring Market Report Scope

As per the scope of the report, ambulatory cardiac monitoring is a way to watch and record the electrical activity of your heart. It is done for daily activities. Most of the recording devices are about the size of a cell phone. Each ambulatory cardiac monitoring device has features that make them better suited to handle different monitoring needs. The patient's needs will ultimately determine which device will be used to get an accurate diagnosis.

The ambulatory cardiac monitoring market is segmented by device type, service provider, indication, connectivity, end-user, and geography. By device type, the market is segmented into ECG devices, event recorders, implantable cardiac loop recorders, mobile cardiac telemetry, and others. By service provider, the market is segmented into independent diagnostic testing facilities (IDTFs), OEM remote monitoring services, and hospital-based monitoring services. The market is segmented by indication into atrial fibrillation, unexplained syncope, and other arrhythmias. By connectivity, the market is segmented into wired devices and wireless devices. By end-user, the market is segmented into hospitals, ambulatory surgical centers, homecare settings, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| ECG Devices |

| Event Recorders |

| Implantable Cardiac Loop Recorders |

| Mobile Cardiac Telemetry |

| Others |

| Independent Diagnostic Testing Facilities (IDTFs) |

| OEM Remote Monitoring Services |

| Hospital-based Monitoring Services |

| Atrial Fibrillation |

| Unexplained Syncope |

| Other Arrhythmias |

| Wired Devices |

| Wireless Devices |

| Hospitals |

| Ambulatory Surgical Centers |

| Homecare Settings |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | ECG Devices | |

| Event Recorders | ||

| Implantable Cardiac Loop Recorders | ||

| Mobile Cardiac Telemetry | ||

| Others | ||

| By Service Provider | Independent Diagnostic Testing Facilities (IDTFs) | |

| OEM Remote Monitoring Services | ||

| Hospital-based Monitoring Services | ||

| By Indication | Atrial Fibrillation | |

| Unexplained Syncope | ||

| Other Arrhythmias | ||

| By Connectivity | Wired Devices | |

| Wireless Devices | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Homecare Settings | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How are artificial-intelligence algorithms reshaping ambulatory cardiac monitoring?

AI now filters ECG streams in real time, reducing false alarms and helping clinicians prioritize actionable arrhythmias, which improves both workflow efficiency and patient compliance.

Why are home-care settings becoming critical for cardiac monitoring vendors?

Remote monitoring in the home lowers readmission risk and aligns with value-based reimbursement, prompting device makers to design user-friendly wearables that patients can apply without clinical supervision.

What is driving the rapid switch from wired to wireless ECG devices?

Pervasive 5G and edge-computing networks let wireless recorders transmit high-fidelity data instantly, enabling timely physician intervention and seamless integration with electronic health records.

How are independent diagnostic testing facilities (IDTFs) influencing service-provider dynamics?

IDTFs offer turnkey interpretation and billing services, allowing hospitals to outsource monitoring tasks and focus on acute care, thereby accelerating adoption of outsourced cardiac monitoring models.

What material challenges remain for long-term wearable patches?

Skin irritation from certain acrylate adhesives continues to limit wear time for some users, pushing manufacturers to develop hypoallergenic materials and alternative attachment methods.

Page last updated on: