Leak Detection And Repair Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 21.25 Billion |

| Market Size (2030) | USD 26.88 Billion |

| Growth Rate (2025 - 2030) | 4.81% CAGR |

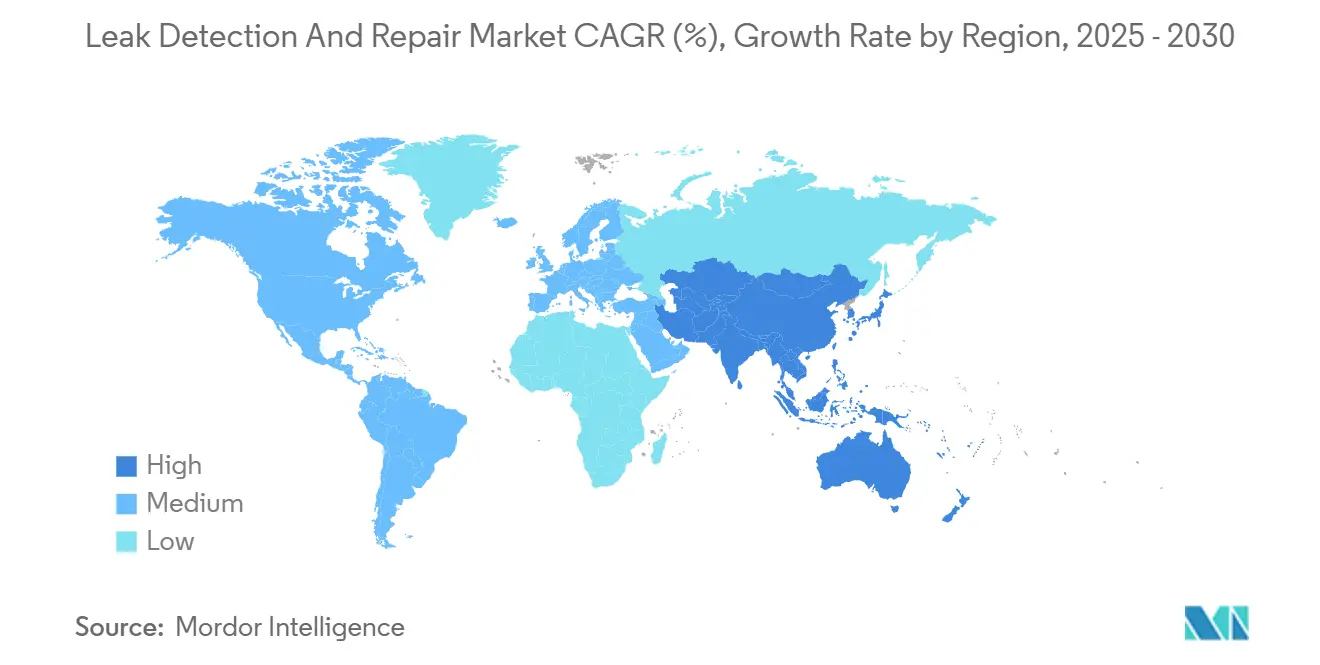

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Leak Detection And Repair Market Analysis by Mordor Intelligence

The leak detection and repair market size stood at USD 21.25 Billion in 2025 and is forecast to reach USD 26.88 billion by 2030, reflecting a 4.81% CAGR over 2025-2030. Robust growth stems from tighter air-quality mandates, rising insurance incentives, and a structural shift from periodic inspections to always-on emissions monitoring. Oil and gas operators remain the primary buyers, yet residential and commercial buildings increasingly install connected sensors as insurers reward early adoption with lower premiums. Hardware upgrades now integrate edge analytics, while new service models wrap data interpretation, compliance reporting, and repair execution into turnkey bundles. Strategic acquisitions by large instrumentation firms underscore a maturing value chain that prizes integrated solutions over point products.

Key Report Takeaways

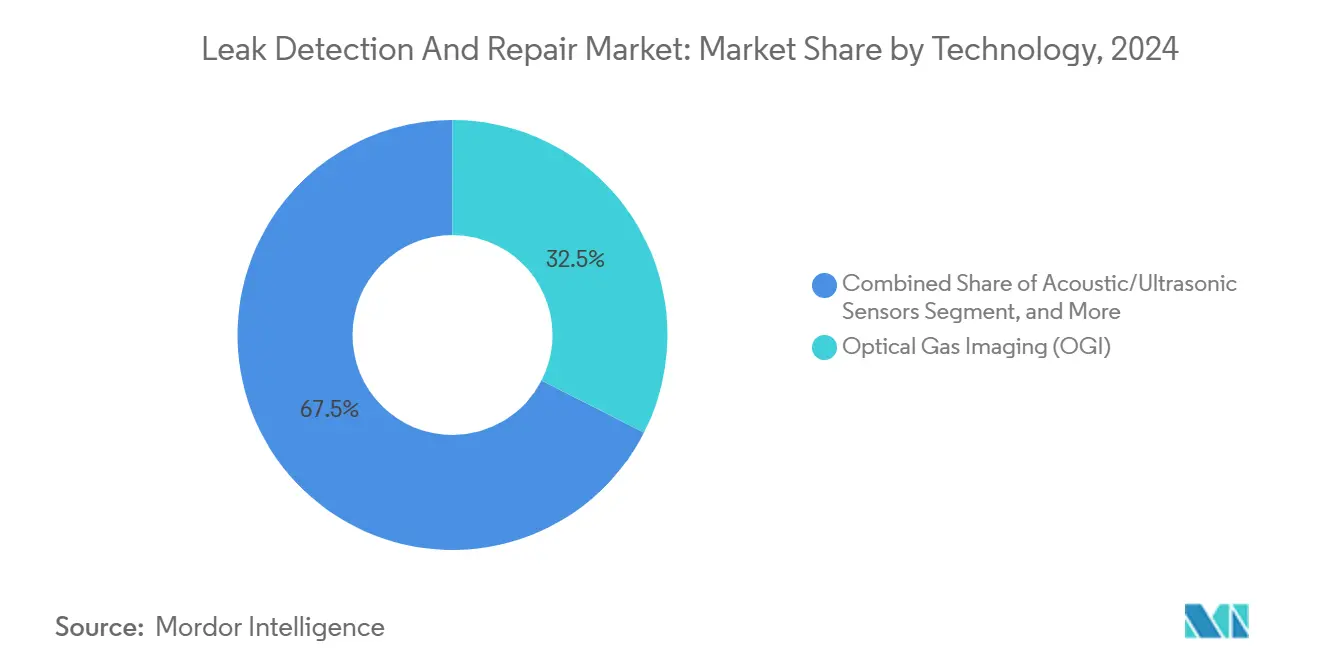

- By technology, optical-gas-imaging commanded 32.5% of the leak detection and repair market share in 2024, whereas fiber-optic and distributed sensing is projected to expand at a 4.7% CAGR through 2030.

- By component, hardware accounted for 64.4% of the leak detection and repair market size in 2024, while services are set to advance at 4.0% annually to 2030.

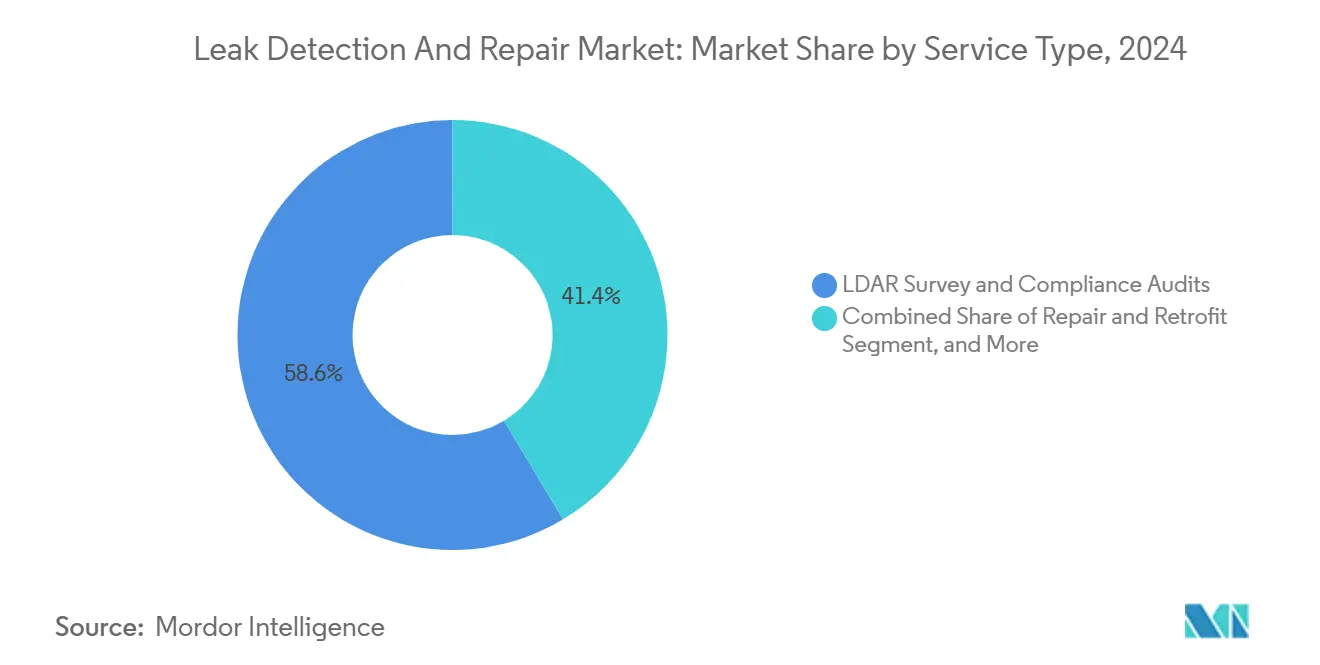

- By service type, LDAR survey and compliance audits captured 58.6% of the leak detection and repair market share in 2024; continuous monitoring-as-a-service is poised for a 4.8% CAGR over the same period.

- By end-use, oil and gas held 46.1% of the leak detection and repair market share in 2024, whereas residential and commercial buildings are forecast to grow at 4.2% CAGR to 2030.

- By geography, North America led with 37.2% of the leak detection and repair market share in 2024; Asia-Pacific is anticipated to post a 4.1% CAGR between 2025-2030.

Global Leak Detection And Repair Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of OGI cameras | +1.2% | Global, led by North America and EU | Medium term (2–4 years) |

| Shift from periodic to continuous methane monitoring | +0.8% | Global, Asia-Pacific accelerating | Long term (≥ 4 years) |

| Drone-enabled LDAR for hard-to-reach assets | +0.6% | North America and EU core | Medium term (2–4 years) |

| EU-2024/1787 methane regulation enforcement | +0.9% | EU primary, global LNG chain | Short term (≤ 2 years) |

| Insurance-driven installation of smart water sensors | +0.7% | North America and EU, expanding Asia-Pacific | Medium term (2–4 years) |

| AI-based predictive analytics cutting downtime | +0.5% | Global, developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Optical-Gas-Imaging (OGI) Cameras

OGI lets technicians scan nearly 3,600 components per hour versus fewer than 200 using Method 21, slashing survey time and labor costs.[1]U.S. Environmental Protection Agency, “Small Entity Compliance Guide for Oil and Natural Gas Sector,” epa.gov Recent EPA Appendix K revisions broaden OGI’s scope to greenhouse-gas leaks, driving uptake beyond hydrocarbons. Insurers such as Chubb now discount premiums for OGI-equipped sites, monetizing compliance and risk mitigation benefits.[2]Chubb, “Optical Gas Imaging: An Effective LDAR Method,” chubb.com Integrated temperature and quantification features help operators prioritize high-volume leaks, boosting repair ROI. Although technician scarcity slows deployments in emerging economies, global training programs are ramping up to meet demand.

Shift from Periodic to Continuous Methane Monitoring

Colorado documented a 75% cut in detected methane releases after moving from quarterly to continuous LDAR programs. The EPA’s Super-Emitter Program now obliges rapid response to third-party alerts, prompting operators to install real-time sensors.[3]Bridger Photonics, “EPA’s Methane Rule Decoded,” bridgerphotonics.com Fiber-optic systems cover up to 20 km without onsite calibration, making them attractive for remote pipelines.[4]OnePetro, “Fiber-Based Methane Leak Detection,” onepetro.org Honeywell’s offshore suite illustrates continuous monitoring’s value where leak rates can reach 66% compared with 3.7% onshore. Subscription models lower capital hurdles for small operators and align costs with performance gains.

Drone-enabled LDAR for Hard-to-reach Assets

Unmanned aircraft survey pipelines at up to 55 mph, detecting methane from 600 ft while circumventing ground-access issues. Kairos Aerospace inspected 260,000 km² and eliminated 43.6 bcf of methane in three years, delivering USD 128 million in client savings. Compliance with EPA and European flight protocols legitimizes drone data for regulatory use. AI-enabled post-processing turns imagery into actionable repair orders, shrinking leak-to-fix cycles.

EU-2024/1787 Methane Regulation Enforcement

The EU now mandates LDAR at every oil and gas site and sets methane-intensity ceilings for imports by 2030. Exporters must demonstrate equivalent monitoring by 2027 or face market exclusion. Penalties can reach 20% of turnover, compelling accelerated investments in detection and recovery systems. The ban on routine venting from 2026 further cements regulatory tailwinds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified OGI technicians | –0.8% | Global, acute in emerging markets | Medium term (2–4 years) |

| High CAPEX for continuous monitoring networks | –1.1% | Global, cost-sensitive regions | Short term (≤ 2 years) |

| Data-ownership disputes in multi-tenant sites | –0.3% | North America and EU | Long term (≥ 4 years) |

| Cyber-security risks in IIoT LDAR platforms | –0.4% | Global critical infrastructure | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified OGI Technicians

Demand for certified OGI operators is outpacing training capacity, especially where new rules stipulate accredited personnel for survey sign-off. Courses require specialized cameras and fieldwork, limiting throughput and inflating wages by 40-60%. Regional bottlenecks enable a handful of service firms to exert pricing power, pushing smaller operators toward alternative detection methods or outsourcing.

High CAPEX for Continuous Monitoring Networks

Fiber-optic lines, power supplies, and ruggedized enclosures drive upfront costs that many small producers cannot absorb. Dual-path redundancy, often required by regulators, doubles spend. Integration with legacy SCADA and security hardening further escalate budgets. Payback hinges on avoided penalties and recovered product, benefits that vary widely by site. Subscription models are emerging but have yet to reach scale in cost-sensitive markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: OGI Dominates, Fiber-Optic Accelerates

The leak detection and repair market size attributed to optical-gas-imaging reached USD 6.5 billion in 2024, equal to 32.5% of total revenue, underscoring its entrenched role in compliance workflows. Real-time visualization, quantifiable emissions, and regulator familiarity sustain demand. Drone and tripod variants are widening use cases from upstream well pads to downstream storage terminals. Fiber-optic and distributed sensing is climbing at a 4.7% CAGR, propelled by continuous monitoring mandates that favor long-range coverage without calibration.

Competitive intensity rises as laser-based TDLAS units improve portability and detection thresholds, nudging into OGI territory for specific hydrocarbons. Acoustic sensors remain essential for pressurized systems, detecting leaks before mass loss. Mass-balance and emerging AI-aided spectrometers occupy niche roles where inventory reconciliation or harsh environments make cameras impractical. Collectively, the breadth of options allows operators to tailor detection stacks to asset class, climate, and risk tolerance.

By Component: Hardware Leads, Services Expand

Hardware contributed 64.4% to the leak detection and repair market share in 2024 as operators purchased sensors, cameras, and ruggedized enclosures for both green- and brownfield projects. Edge processors now reside inside cameras, shrinking latency and bandwidth needs. Services, though smaller, are scaling faster as regulations shift accountability from finding leaks to verifying repairs. At 4.0% CAGR, managed offerings, ranging from calibration and audit prep to third-party data hosting, convert lumpy capex into recurring opex.

Manufacturers bundle multiyear service agreements at the point of sale, locking in lifecycle revenue and ensuring firmware stays aligned with changing standards. Start-ups target midsize operators with cloud-first platforms that integrate multi-vendor hardware, promising neutral analytics and lower total cost of ownership.

By Service Type: Compliance Drives, CMaaS Emerges

LDAR survey and compliance audits captured 58.6% of 2024 spend, reflecting non-negotiable regulatory documentation needs. Providers differentiate on technician availability, report turnaround, and digital chain-of-custody features that withstand enforcement scrutiny. Continuous monitoring-as-a-service (CMaaS) is outperforming at 4.8% CAGR, bundling sensors, connectivity, analytics, and reporting into subscription packages.

Repair and retrofit services monetize the critical “fix” phase, mobilizing crews with sealants, flanges, and replacement parts to cut methane quickly. Training and certification offerings benefit from technician shortages, with online modules and simulator labs boosting throughput without sacrificing rigor.

By End-use Industry: Oil and Gas Leads, Buildings Accelerate

Oil and gas operations generated 46.1% of 2024 revenue for the leak detection and repair market, anchored by expansive infrastructure and the sector’s regulatory exposure. Super-emitter designations and import rules tie market access to measured methane intensity, embedding leak detection and repair deep into capital budgets. Residential and commercial buildings, spurred by insurance incentives, exhibit the fastest growth at 4.2% CAGR through 2030.

Chemicals and petrochemicals invest in multi-gas detection given complex process streams, while power generation shifts focus to natural gas turbines and emerging hydrogen blends. Water utilities deploy AI-driven acoustics to curb non-revenue water, achieving classification accuracy above 90%. Cross-industry momentum solidifies a diversified demand base resistant to commodity swings.

Geography Analysis

North America generated 37.2% of 2024 revenue, anchored by stringent EPA methane fees that could cost onshore producers USD 750 million per year if emissions exceed thresholds. Provincial rules in Canada complement U.S. federal policy, building a harmonized market for compliant technologies. OEMs located in the United States leverage domestic reference sites to export solutions globally, reinforcing regional leadership.

Europe follows closely, galvanized by Regulation 2024/1787 that bans routine venting from 2026 and sets import equivalence rules that ripple across LNG supply chains. Germany and the United Kingdom spearhead adoption due to industrial density and aging North Sea infrastructure. EU-wide alignment fosters economies of scale for service firms, while penalty risk accelerates corporate procurement cycles.

Asia-Pacific, driven by China’s methane action plan and rapid urbanization, is forecast to post a 4.1% CAGR. China’s gas-sector emissions, 70% tied to production and distribution, create immense potential for continuous monitoring rollouts. Japan’s CLEAN Initiative and a regional METEC in Malaysia underscore governmental commitment to technology validation. South Korea’s forthcoming ESG disclosures by 2026 add compliance pressure, and India’s pipeline build-out embeds detection requirements from day one. Diversity in regulatory maturity invites both global incumbents and local innovators to tailor offerings by jurisdiction.

Competitive Landscape

The leak detection and repair market features moderate fragmentation as legacy instrumentation giants compete with niche AI and drone specialists. Teledyne FLIR, Honeywell, and Emerson extend portfolios with cloud dashboards and service agreements. Concurrently, specialists such as Kairos Aerospace and Picarro leverage differentiated sensing modalities to capture high-growth niches. M&A activity is intensifying: MSA Safety’s USD 200 million purchase of M&C TechGroup broadens gas-analysis reach, while Crane Company’s USD 1.06 billion take-over of Baker Hughes’ Precision Sensors unit signals appetite for scale.

R&D pipelines emphasize sensitivity, miniaturization, and PFAS-free materials, evidenced by nine patents filed by Montrose Environmental in 2023. Satellite analytics and machine-learning dashboards lower detection thresholds and bring basin-wide context to asset-level findings. Regulatory certification, EPA protocols, EU verifications, acts as both barrier and moat, favoring vendors with proven compliance data. Insurers emerge as gatekeepers in residential segments, steering demand toward platforms that feed loss-avoidance analytics into underwriting models.

White-space opportunities include CMaaS bundles and retrofits for aging city gas grids. Regions with technician shortages invite turnkey mobile units and remote-training solutions, while data-sovereignty concerns open pathways for on-premises analytics appliances. As regulations tighten globally, competitive advantage tilts toward firms that can integrate detection, quantification, and automated reporting in one workflow.

Leak Detection And Repair Industry Leaders

Teledyne FLIR LLC

Honeywell International Inc.

Emerson Electric Co.

Schneider Electric SE

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: JOGMEC issued a joint statement at LNGPCC2025 expanding the CLEAN Initiative to 27 companies and detailing verification mechanisms for methane reduction across LNG supply chains.

- May 2025: MSA Safety closed its USD 200 million acquisition of M&C TechGroup, strengthening process-safety gas analysis capabilities.

- March 2025: Schneider Electric committed USD 700 million for U.S. plant expansion and microgrid testing to advance leak detection and energy automation.

- October 2024: Montrose Environmental secured a USD 249 million U.S. Army Corps contract covering air and water compliance, bolstering its integrated services presence.

Global Leak Detection And Repair Market Report Scope

| Optical Gas Imaging (OGI) |

| Acoustic/Ultrasonic Sensors |

| Tunable Laser Absorption Spectroscopy (TDLAS) |

| Fiber-Optic and Distributed Sensing |

| Mass / Volume Balance |

| Other Technology |

| Hardware |

| Services |

| LDAR Survey and Compliance Audits |

| Continuous Monitoring-as-a-Service (CMaaS) |

| Repair and Retrofit |

| Training and Certification |

| Oil and Gas |

| Chemicals and Petrochemicals |

| Power Generation |

| Water and Waste-water Utilities |

| Residential and Commercial Buildings |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Technology | Optical Gas Imaging (OGI) | ||

| Acoustic/Ultrasonic Sensors | |||

| Tunable Laser Absorption Spectroscopy (TDLAS) | |||

| Fiber-Optic and Distributed Sensing | |||

| Mass / Volume Balance | |||

| Other Technology | |||

| By Component | Hardware | ||

| Services | |||

| By Service Type | LDAR Survey and Compliance Audits | ||

| Continuous Monitoring-as-a-Service (CMaaS) | |||

| Repair and Retrofit | |||

| Training and Certification | |||

| By End-use Industry | Oil and Gas | ||

| Chemicals and Petrochemicals | |||

| Power Generation | |||

| Water and Waste-water Utilities | |||

| Residential and Commercial Buildings | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the global revenue of the leak detection and repair market in 2025?

The market generated USD 21.25 Billion in 2025.

How fast is the leak detection and repair market expected to grow through 2030?

It is projected to expand at a 4.81% CAGR between 2025-2030.

Which technology currently leads in adoption?

Optical-gas-imaging held 32.5% revenue share in 2024.

Why are insurers interested in connected leak detection sensors?

Deploying smart-water devices cuts average claim costs by USD 4,000 and reduces incident frequency by 96%.

Page last updated on: