Global Leak Detection Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

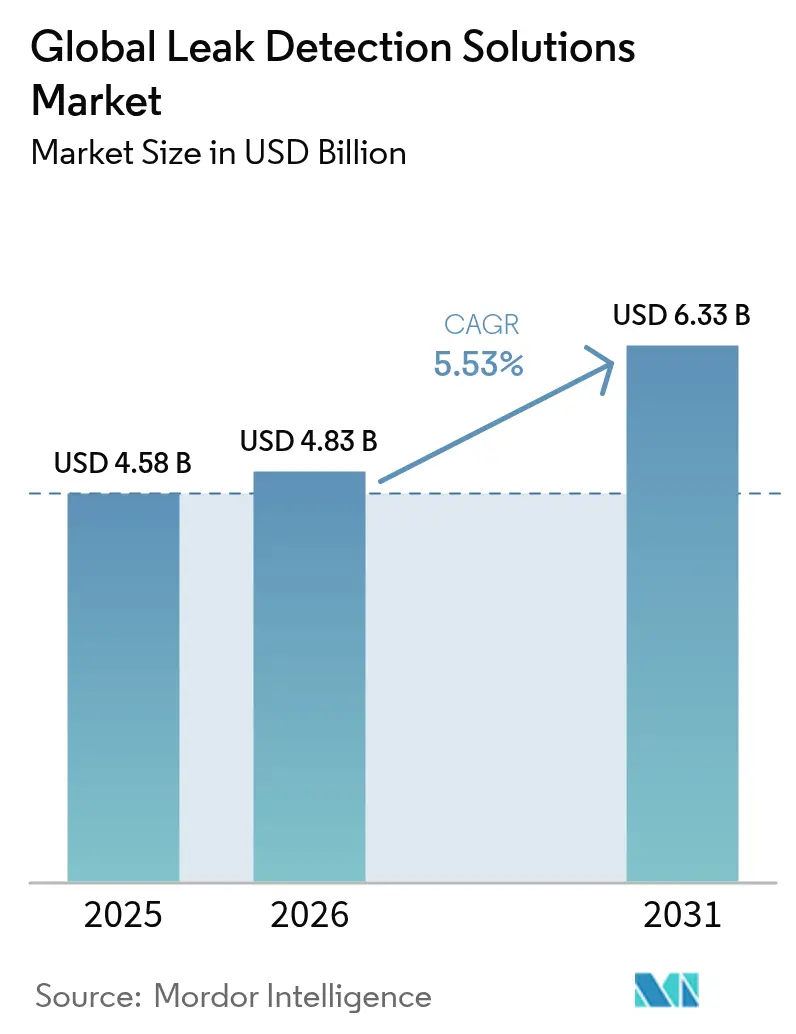

| Market Size (2026) | USD 4.83 Billion |

| Market Size (2031) | USD 6.33 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Leak Detection Solutions Market Analysis by Mordor Intelligence

The leak detection solutions market size was valued at USD 4.58 billion in 2025 and estimated to grow from USD 4.83 billion in 2026 to reach USD 6.33 billion by 2031, at a CAGR of 5.53% during the forecast period (2026-2031). Heightened environmental regulations, expanding energy infrastructure, and rapid sensor innovation underpinned this growth. In 2024, the U.S. Environmental Protection Agency finalized methane-fee rules that imposed charges as high as USD 1,500 per metric ton by 2026, triggering a wave of compliance-driven investments.[1]U.S. Environmental Protection Agency, “Biden-Harris Administration Announces Final Rule to Cut Methane Emissions,” epa.gov Parallel rules from PHMSA that took effect in 2025 required advanced detection programs across U.S. gas pipelines. Laser absorption and LiDAR solutions posted the fastest adoption on the back of high-resolution quantification capabilities, while drone-mounted platforms solved access challenges in hazardous zones. North America commanded the largest regional position, yet Asia-Pacific recorded the most vigorous gains as India and Japan accelerated large-diameter pipeline programs.

Key Report Takeaways

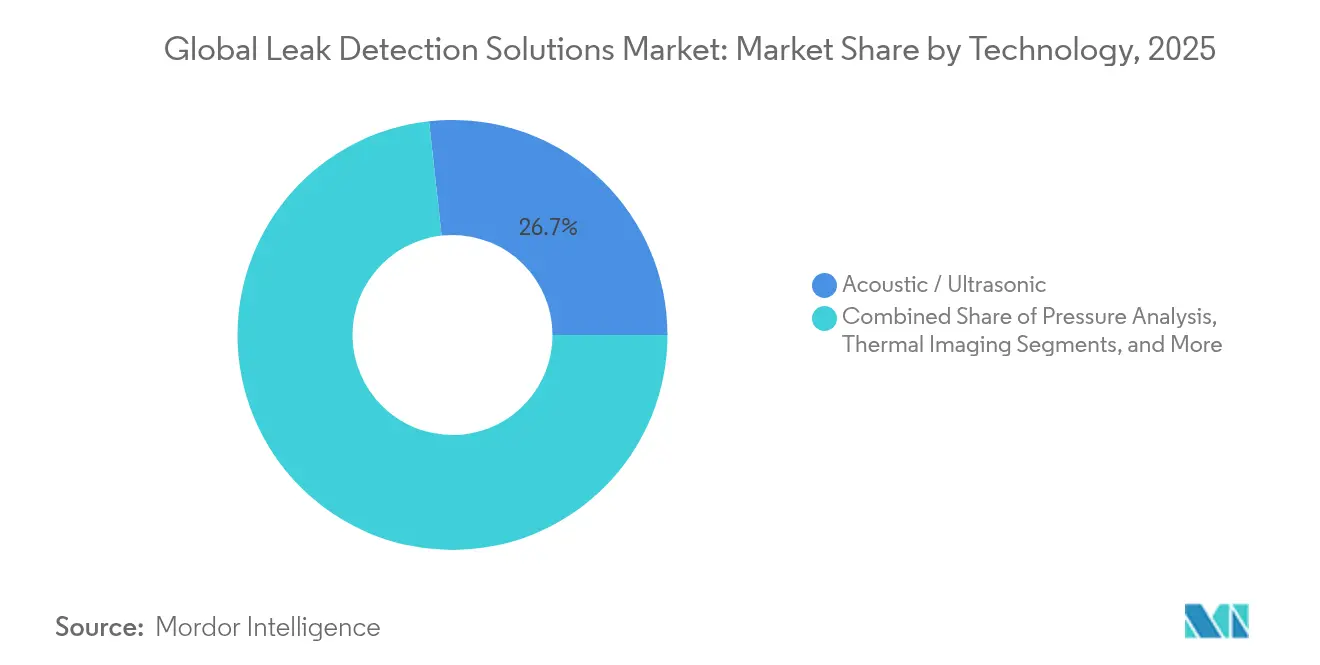

- By technology, acoustic/ultrasonic solutions led with 26.74% revenue share in 2025, whereas laser absorption and LiDAR technologies expanded at an 8.41% CAGR through 2031.

- By end-user industry, the oil and gas segment held 60.35% of the leak detection solutions market share in 2025; water treatment registered the highest projected CAGR at 5.76% over 2026-2031.

- By deployment mode, fixed systems accounted for 65.40% of the leak detection solutions market size in 2025, while drone-mounted solutions grew at a 11.65% CAGR.

- By pipeline stage, midstream operations captured 44.60% of the leak detection solutions market size in 2025; upstream activities advanced at a 7.22% CAGR through 2031.

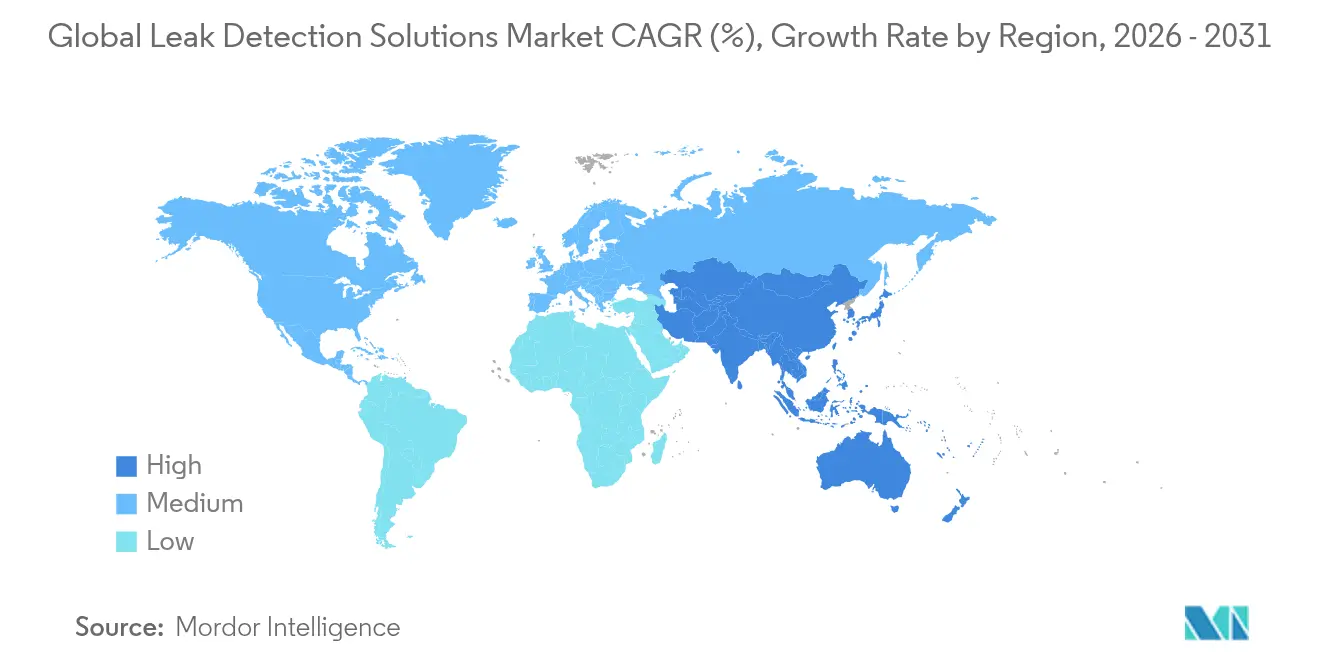

- By geography, North America retained 37.70% regional share in 2025, but Asia-Pacific was the fastest-growing geography at a 7.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Leak Detection Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent fugitive-methane regulations (e.g., U.S. Inflation Reduction Act) | +1.8% | North America, expanding to the EU and Asia-Pacific | Short term (≤ 2 years) |

| Rapid expansion of hydrogen and CCUS pipeline projects | +1.2% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| AI-enabled predictive analytics lowers false positives | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Adoption of leak-detection-as-a-service (LDaaS) business models | +0.7% | Global, with early adoption in North America | Long term (≥ 4 years) |

| Satellite constellations providing high-resolution emissions data | +0.6% | Global coverage with a focus on major oil and gas regions | Short term (≤ 2 years) |

| Mandatory ESG reporting driving proactive leak management | +0.5% | Global, with emphasis on developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent fugitive-methane regulations drive market transformation

The Inflation Reduction Act’s methane surcharge, which started at USD 900 per metric ton in 2024 and climbs to USD 1,500 by 2026, re-shaped project economics by making continuous monitoring cheaper than paying fees. Complementary “Super Emitter” protocols allowed third parties to trigger operator response on leaks above 100 kg/hr, accelerating the adoption of fixed sensors and satellite data feeds. Operators substituted legacy Method 21 surveys with optical gas imaging and fiber-optic arrays to avoid downtime, lifting order volumes for high-resolution camera packages.

Rapid expansion of hydrogen and CCUS pipeline projects

Hydrogen molecules are smaller and more diffusive than methane, demanding detectors that spot leaks below 1 ppm; Raman analyzers demonstrated such sensitivity at several-meter stand-off distances. The U.S. Department of Energy earmarked USD 25 million for hydrogen-specific detection R&D in 2025. India’s state operators, including GAIL, evaluated dedicated hydrogen trunklines, creating follow-on demand for specialized sensors.

AI-enabled predictive analytics lower false positives

Machine-learning algorithms fused multi-sensor data and cut false alarms by differentiating leak signatures from rain, venting, and compressor noise. Honeywell’s collaboration with Google embedded Gemini generative AI into its platforms to deliver context-aware alarms and dynamic maintenance schedules. Academic work showed multi-algorithm fusion improving detection accuracy by 0.15 percentage points, enabling operators to trust autonomous shut-in commands.

Satellite constellations enable global emissions transparency

MethaneSAT, launched in March 2024, started detecting plumes as low as 2 ppb and provided public dashboards that regulators and investors used to benchmark operators. Studies combining data from Sentinel-2 and EnMAP quantified leaks between 1 t/h and 40 t/h with high spatial fidelity, reinforcing pressure on late adopters to install on-ground verification equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for fiber-optic and LiDAR deployments in brownfield pipelines | -1.1% | Global, particularly in mature oil and gas regions | Short term (≤ 2 years) |

| Scarcity of skilled thermography and acoustics technicians in emerging markets | -0.8% | Asia-Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Cybersecurity vulnerabilities in cloud-linked LD systems | -0.5% | Global, with higher impact in digitally advanced regions | Medium term (2-4 years) |

| False alarms in multiphase flow conditions reduce operator confidence | -0.4% | Global, particularly in complex processing environments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX for fiber-optic and LiDAR deployments in brown-field pipelines

Distributed fiber-optic sensing costs USD 50,000-100,000 per kilometer, and retrofits often require trenching or rack modifications that disrupt throughput. LiDAR heads suitable for hazardous zones were priced between USD 200,000 and USD 500,000, restricting adoption when crude prices softened. Operators in lower-margin basins thus favored portable ultrasonic detectors despite narrower coverage.

Scarcity of skilled thermography and acoustics technicians in emerging markets

Ultrasonic detectors needed personnel able to interpret 20-40 kHz signatures, a competency in short supply across Africa and parts of Asia. Thermal image interpretation faced similar gaps, with utility managers noting year-long lead times to hire certified level-II thermographers. The shortage delayed deployments even when funding was available, slowing the leak detection solutions market in high-growth regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Acoustic strength meets laser acceleration

Acoustic and ultrasonic systems held 26.74% of 2025 revenues, making them the largest single technology cohort in the leak detection solutions market. Piezo-electric sensors delivered instantaneous alerts within a 40 m radius and required no calibration, a value proposition that suited onshore gathering lines. Laser absorption and LiDAR platforms, while still smaller in absolute sales, expanded at an 8.41% CAGR, buoyed by regulatory recognition of quantified emission measurement protocols.

Thermal imagers moved from handheld to cloud-connected variants that streamed radiometric data for predictive analytics, broadening appeal among refinery operators. Fiber-optic distributed sensing gained contracts along subsea tiebacks where maintenance access was limited. Analytical modeling showed sub-1% localization error for acoustic-emission-based storage-tank monitoring, validating acoustic dominance in fixed assets.

By End-User Industry: Oil and gas holds sway as water utilities accelerate

The oil and gas sector captured 60.35% of 2025 revenue, reflecting statutory leak fees and the high-consequence nature of hydrocarbon releases. Nevertheless, water treatment utilities logged the quickest expansion at 5.76% CAGR, spurred by aging mains and drought-linked loss-reduction mandates. Utilities deployed AI classifiers that achieved 98.3% accuracy on leak/no-leak differentiation in potable networks. Chemical and power-generation operators adopted clamp-on flowmeters following corporate net-zero policies, while hydrogen developers demanded Raman-based detectors to satisfy safety case requirements.

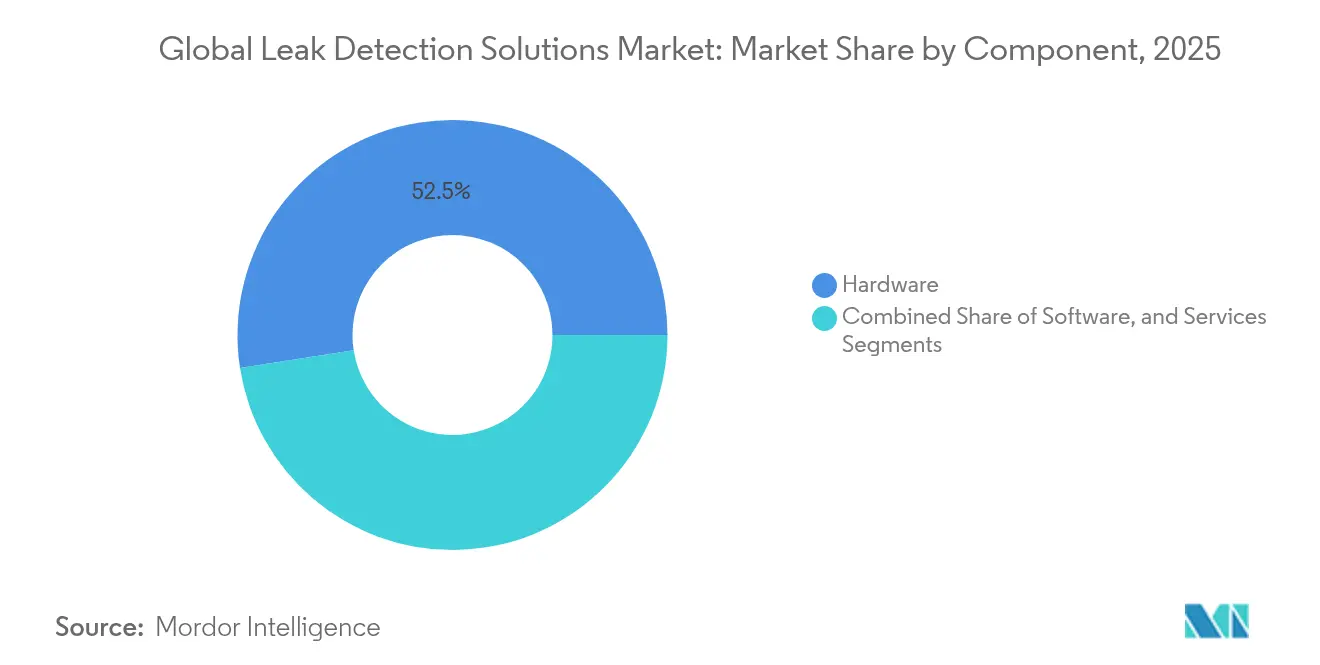

By Component: Hardware dominant, software surging

Sensors, cameras, and cables made up 52.45% of the 2025 spend, anchoring the leak detection solutions market. Yet analytics software, enriched with machine learning, posted a 7.55% CAGR as operators transitioned to predictive maintenance. Deep-learning models on multimode fibers predicted temperatures with 100% tolerance accuracy, pushing adoption in LNG trains. Services, including installation and LDaaS contracts, remained a steady contributor and provided annuity revenue streams for vendors.

By Deployment Mode: Fixed systems rule, drones take flight

Fixed installations delivered 65.40% of 2025 revenue, driven by 24/7 surveillance requirements at compressor stations and tank farms. Drone-mounted platforms, however, expanded at 11.65% CAGR as operators sought rapid reconnaissance after storms or sabotage incidents. ABB’s HoverGuard illustrates sensitivity gains capable of mapping 1 ppm-meter methane at 150 m altitude. Portable detectors played a role in spot checks and confined-space entry.

By Pipeline Stage: Midstream leadership amid upstream uptick

Transmission networks absorbed 44.60% of the 2025 spend, reflecting the vast mileage of regulated pipelines requiring continuous integrity assurance. Upstream wells and flowlines nonetheless grew at 7.22% CAGR as shale, offshore, and enhanced-oil-recovery projects installed corrosion-resistant composites that needed specialized leak surveillance. Downstream sites—refineries, petrochemical complexes, and LNG liquefiers—maintained stable demand for vapor-sensing and infrared cameras to mitigate unit shutdown risks.

Geography Analysis

North America retained 37.70% of global revenue in 2025 owing to methane-fee statutes, enhanced pipeline safety regulations, and the rollout of satellite verification programs such as MethaneSAT that scrutinized shale basins. Canada’s hydrogen roadmap further boosted orders for specialized leak sensors, while Mexico’s cross-border pipeline build created incremental demand for midstream monitoring solutions. The leak detection solutions market size in the region is forecast to advance steadily as refiners digitize aging assets.

Asia-Pacific recorded a 7.62% CAGR through 2031. India commissioned a USD 1.3 billion, 2,800 km LPG pipeline in 2025 and earmarked USD 5 billion for new gas corridors, lifting hardware imports, and local assembly. Japan signed bilateral pacts to curb methane leakage and funded R&D on drone-based inspections for municipal sewer lines. China expanded L-band SAR combined with ground-penetrating radar to detect water-line failures beneath urban arteries, accelerating municipal orders.

Europe maintained momentum as the EU tightened corporate sustainability reporting and methane-intensity disclosure. Operators integrated fiber-optic strings along North Sea interconnectors and invested in LiDAR-equipped helicopters to monitor distribution grids. The Middle East and Africa lagged in skilled labor, but rising CCUS hubs in the Gulf and new crude export pipelines in East Africa unlocked contracts for turnkey leak detection packages. Regional utilities leveraged technology transfer agreements to bridge capability gaps.

Competitive Landscape

The leak detection solutions market displayed moderate fragmentation. Industrial automation majors orchestrated acquisitions to broaden their scope. Honeywell spent USD 2.16 billion on Sundyne and USD 1.81 billion on Air Products’ LNG technology to deepen critical pump, compressor, and process controls portfolios.[4]Honeywell International Inc., “Investor Relations Insights: March 2025 Edition,” investor.honeywell.com The firm then layered Google’s Gemini AI on its platform to deliver dynamic alarm rationalization.

Endress+Hauser absorbed roughly 800 SICK staffers via a strategic partnership that bolstered gas analysis and flow measurement competencies essential for emissions quantification. Emerson purchased Flexim to secure clamp-on ultrasonics used in water and chemical plants. Smaller specialists thrived in niches such as hydrogen-specific sensors and AI-enabled LDaaS; their agility secured pilot wins with national oil companies.

Competitive intensity sharpened as satellite-data start-ups partnered with drone firms to offer basin-wide surveillance subscriptions. Vendors differentiated through end-to-end offerings that bundled sensors, cloud analytics, and regulatory reporting templates. Price competition remained muted in high-consequence applications where performance outweighed cost, sustaining healthy gross margins for incumbents.

Global Leak Detection Solutions Industry Leaders

Honeywell International Inc

Aeris Technologies, Inc.

Bridge Photonics

Schneider Electric S.E

Siemens Gas and Power GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Honeywell acquired Li-ion Tamer, adding off-gas detection for battery storage fires to its building-automation suite.

- July 2025: SICK and Endress+Hauser formed a process-automation partnership; ~800 SICK staff joined Endress+Hauser to strengthen gas-analysis offerings.

- June 2025: Kobe City deployed IBIS2 drones to inspect 600 m of sewer lines, creating a national model for municipal drone use.

- March 2025: Honeywell announced a USD 2.16 billion Sundyne acquisition to expand pumps and compressors integral to leak-detection loops.

Global Leak Detection Solutions Market Report Scope

A leak detection system monitors the flow of oil & gas, chemical, and water through a pipeline and the leakage of other elements. The system cuts off the flow or alerts about the leak when an unusual situation is detected. Leak detection systems are usually installed in the oil & gas, chemical, water treatment, power generation, and other industries. Specific leak detection techniques were created to provide the location of the leak.

The study covers leak detection solutions technology that includes acoustic/ ultrasonic, pressure analysis, thermal imaging, fiber optic, laser absorption, LiDAR, vapor sensing, and E-RTTM, and identifies the leaks across major end-users such as oil & gas, chemical, water treatment, power generation. The study also covers demand across various regions and considers the impact of COVID-19 on the market.

| Acoustic / Ultrasonic |

| Pressure Analysis |

| Thermal Imaging |

| Fiber Optic |

| Laser Absorption and LiDAR |

| Vapor Sensing |

| E-RTTM |

| Other Technologies |

| Oil and Gas |

| Chemical |

| Water Treatment |

| Power Generation |

| Other End-Users |

| Hardware |

| Software |

| Services |

| Fixed / Stationary |

| Portable / Handheld |

| Drone-Mounted / Aerial |

| Upstream |

| Midstream |

| Downstream |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Technology | Acoustic / Ultrasonic | ||

| Pressure Analysis | |||

| Thermal Imaging | |||

| Fiber Optic | |||

| Laser Absorption and LiDAR | |||

| Vapor Sensing | |||

| E-RTTM | |||

| Other Technologies | |||

| By End-User Industry | Oil and Gas | ||

| Chemical | |||

| Water Treatment | |||

| Power Generation | |||

| Other End-Users | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Deployment Mode | Fixed / Stationary | ||

| Portable / Handheld | |||

| Drone-Mounted / Aerial | |||

| By Pipeline Stage | Upstream | ||

| Midstream | |||

| Downstream | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the leak detection solutions market?

The leak detection solutions market was valued at USD 4.83 billion in 2026 and is projected to reach USD 6.33 billion by 2031.

Which technology segment is growing the fastest?

Laser absorption and LiDAR systems are the fastest-growing technologies, registering an 8.41% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

Robust pipeline expansion in India, Japan’s methane-mitigation programs, and China’s municipal infrastructure upgrades are propelling a 7.62% regional CAGR.

How do methane-free regulations affect adoption?

Charges rising to USD 1,500 per metric ton by 2026 have made investing in continuous monitoring cheaper than paying penalties, accelerating deployments in North America.

What role do drones play in leak detection?

Drone-mounted sensors provide rapid, remote coverage of hazardous or inaccessible assets, and this deployment mode is growing at a 11.65% CAGR.

Who are the key players shaping market dynamics?

Honeywell, Endress+Hauser, Emerson, and ABB lead through acquisitions, AI partnerships, and portfolio integration, collectively holding a sizable portion of global revenue.

Page last updated on: