Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

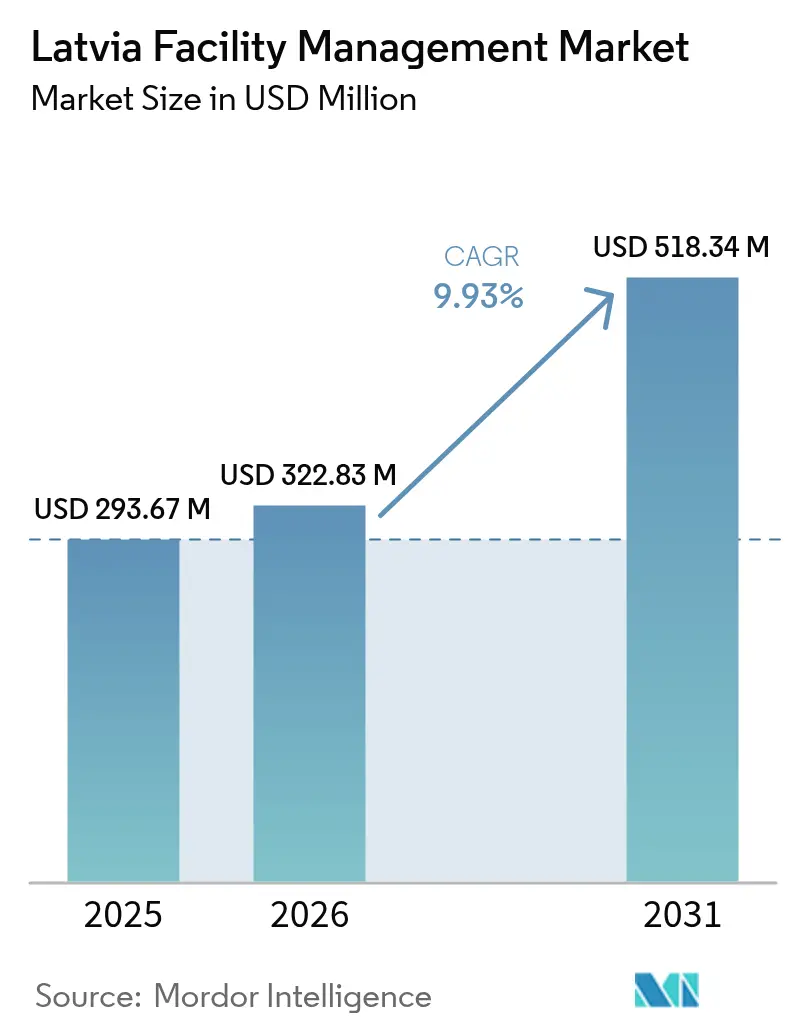

| Base Year Market Size (2025) | USD 293.67 Million |

| Market Size (2026) | USD 322.83 Million |

| Market Size (2031) | USD 518.34 Million |

| Growth Rate (2026 - 2031) | 9.93% CAGR |

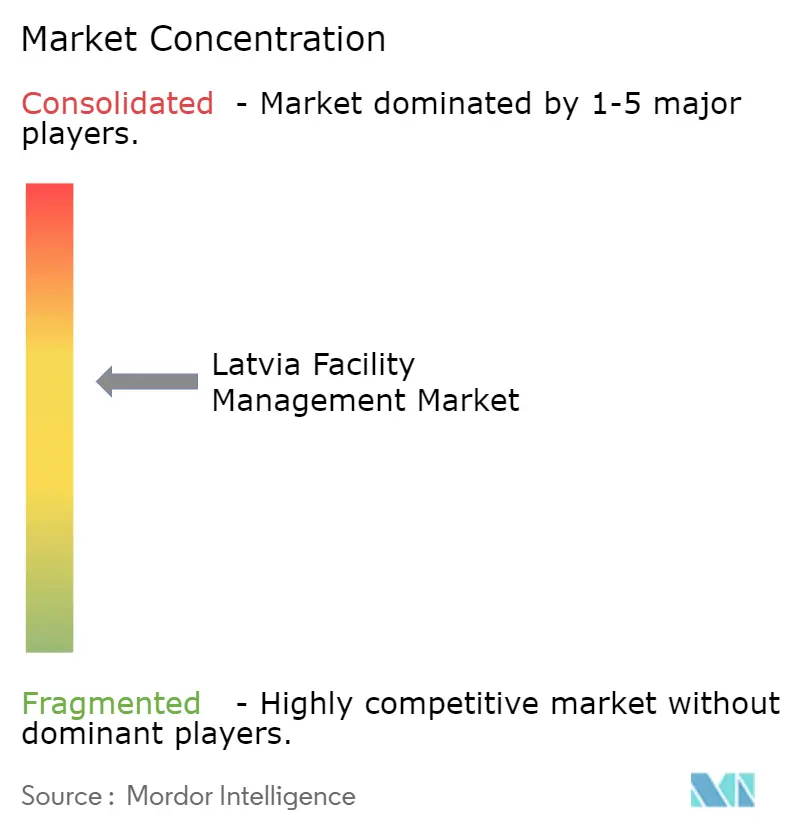

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latvia Facility Management Market Analysis by Mordor Intelligence

The Latvia facility management market size is expected to grow from USD 293.67 million in 2025 to USD 322.83 million in 2026 and is forecast to reach USD 518.34 million by 2031 at 9.93% CAGR over 2026-2031. Sustained outsourcing adoption, mounting ESG disclosure obligations and acute labor shortages are reshaping service delivery models, while energy-efficiency mandates, smart-building investments and large urban regeneration schemes add new revenue streams. Corporate occupiers continue to trade fixed costs for variable service contracts in response to GDP growth that remains below 2% and inflation holding near 3.4%.[1]Latvijas Banka, “Macroeconomic Forecasts | June 2025,” bank.lv Capital-intensive hard services dominate value creation, yet faster expansion in soft-service categories signals rising client preference for integrated workplace experiences. Medium-scale regional providers gain share by pairing local know-how with digital tools, even as global majors use scale, analytics and ESG credentials to win national tenders.

Key Report Takeaways

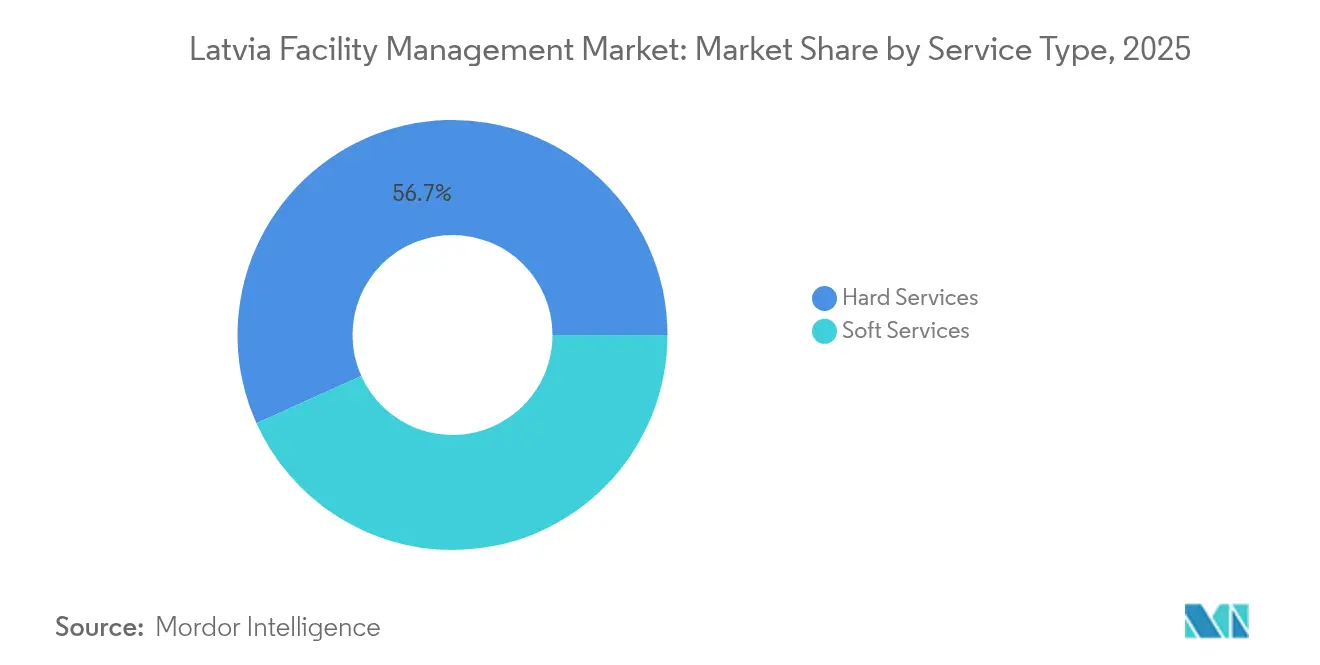

- By service type, Hard Services led with 56.73% revenue share in 2025, while Soft Services is accelerating at an 11.02% CAGR through 2031.

- By offering type, the Outsourced model held 63.62% share of the Latvia facility management market size in 2025 and is expanding at 11.78% CAGR to 2031.

- By end-user industry, Commercial facilities commanded 39.63% of the Latvia facility management market share in 2025, whereas Institutional & Public Infrastructure shows the highest forecast CAGR at 12.16% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Latvia Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Outsourced Facility Management Services | +2.8% | National, with concentration in Riga and Pierīga regions | Medium term (2-4 years) |

| Growing Focus on Energy Efficiency and Sustainability | +2.1% | National, with early adoption in commercial buildings | Long term (≥ 4 years) |

| Increasing Implementation of IoT and Smart Building Technologies | +1.9% | Urban centers, particularly Riga metropolitan area | Medium term (2-4 years) |

| Rising Demand for Integrated Facility Management Solutions | +1.7% | Commercial and institutional sectors nationwide | Medium term (2-4 years) |

| CSRD roll-out forcing large enterprises to hire ESG-capable FM providers | +1.2% | Large enterprises and public interest entities | Short term (≤ 2 years) |

| Corporate occupiers bundling hard and soft services | +1.0% | Commercial office buildings and industrial facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Outsourced Facility Management Services

A sustained shift toward external service provision underpins the Latvia facility management market as organizations counter labor scarcity and cost volatility. The outsourced segment’s 64.26% share in 2024 and 12.02% growth outlook highlight preference for single-partner accountability. Stricter rules on third-country hires imposed in 2025 constrain internal staffing pipelines, tilting procurement toward providers that can mobilize multi-skilled teams nationwide. Public financiers such as Altum booked EUR 26.6 million (USD 28.99 million) profit in 9M 2024, channeling fresh credit to SMEs that outsource non-core functions. Flagship projects like the EUR 3 billion (USD 3.27 billion) Riga Waterfront create long-run pipelines for bundled FM contracts spanning waste, energy and lifecycle asset management.

Growing Focus on Energy Efficiency and Sustainability

Mandatory ESG reporting introduced in 2024 compels more than 200 Latvian enterprises to declare building-level environmental metrics by 2026, propelling demand for measurable energy outcomes. A smart-lighting retrofit in Riga’s Ķīpsala district cut power bills by 79%, saving EUR 4,685 (USD 5,107) annually and proving the payback of sensor-based controls.[2]Tet, “Viedās gaismas Ķīpsalā palīdzējušas pašvaldībai ietaupīt vairāk nekā 4600 eiro,” tet.lv AI-driven HVAC pilots achieved 12.5% energy reduction without sacrificing indoor air-quality targets.[3]MDPI Authors, “Occupancy-Based Predictive AI-Driven Ventilation Control for Energy Savings in Office Buildings,” mdpi.com Military dormitories consume 270 kWh/m², far above theoretical norms, pointing to retrofit potential that could unlock 77.6–79.3% savings. These case studies shift procurement criteria from lowest cost to lowest carbon, altering bid evaluations across the Latvia facility management market.

Increasing Implementation of IoT and Smart Building Technologies

Sensor networks, BIM and data-driven workflows are redefining service scopes in the Latvia facility management market. Riga Technical University’s solar-powered, IoT waste platform automates fill-level alerts and route planning, showcasing the operational benefits of real-time analytics. More than 20,000 micro-generators already feed renewables into the grid, feeding data streams into building-management dashboards that optimize demand response. Rezekne Olympic Centre blends BIM, heat recuperation and PV arrays to shrink lifecycle maintenance budgets. Local patent activity around Modbus-enabled smart switches indicates emerging domestic tech supply chains. Lindström’s deployment of Nortal’s Industry 4.0 suite raised plant productivity, proving the ROI of predictive maintenance across textile service lines.

Rising Demand for Integrated Facility Management Solutions

Hybrid workplace models push occupiers to bundle cleaning, maintenance and workplace technology within one contract, fueling integrated FM uptake. ISS A/S elevated ESG to group-level oversight in 2024, signalling that sustainable operations are now a core component of integrated bids. CBRE’s facilities-management revenue jumped 18% in Q2 2024, buoyed by tech, healthcare and life-science clients seeking portfolio-wide service harmonization. RIX Riga Airport’s EUR 75 million (USD 81.75 million) terminal upgrade, designed for BREEAM certification, exemplifies the need for providers able to integrate hard services, soft services and carbon accounting across critical infrastructure. Latvijas Pasts invested EUR 1.4 million (USD 1.53 million) in automated sorting, demanding FM partners versed in equipment uptime and data security.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortages in Specialized Facility Services | -1.8% | National, with acute impact in Riga and industrial centers | Medium term (2-4 years) |

| Economic Uncertainty and Inflationary Pressures | -1.4% | National, with regional variations | Short term (≤ 2 years) |

| Inflation-driven spikes in energy and materials costs | -1.2% | National, with higher impact on energy-intensive facilities | Short term (≤ 2 years) |

| Stricter 2025 rules on hiring third-country nationals | -0.9% | National, with concentration in urban service centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages in Specialized Facility Services

Seven of ten Latvian employers report difficulties sourcing qualified workers, and 85% struggle to secure competent hires, a pattern that directly constricts technical FM capacity. New compliance inspections intensify the need for certified safety professionals, yet restrictions on foreign labor added in 2025 extend recruitment timelines and costs. Residence permits issued to non-EU nationals more than doubled between 2015 and 2024, but tighter quotas now limit the pool for FM trades such as HVAC technicians. Investors rank workforce scarcity as Latvia’s top business risk, lowering the FICIL sentiment index to 1.9 in 2023, the weakest since 2016. Providers react by automating routine tasks and upskilling existing staff, yet wage escalation squeezes margins across the Latvia facility management market.

Economic Uncertainty and Inflationary Pressures

GDP growth below 2% and consumer-price inflation near 3.4% compress client budgets for non-critical services. The OECD warns that wage-led inflation and slow EU-fund absorption hinder construction pipelines that normally underpin FM demand. Banks such as BluOr highlight higher sanctions-compliance and cybersecurity spend that raise overheads for FM contracts linked to financial institutions. Elevated interest rates temper real-estate starts, though Citadele signals a gradual rebound in sentiment contingent on energy-price stability. These macro headwinds collectively shave more than 1 percentage point from forecast growth in the Latvia facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technical Reliability Sustains Hard-Service Supremacy

Hard Services controlled 56.73% of 2025 revenue within the Latvia facility management market, confirming the strategic role of asset integrity and compliance. Legacy building stock and stringent fire-safety rules keep demand high for mechanical, electrical and plumbing maintenance. Studies on military dormitories reveal 270 kWh/m² actual consumption versus 186 kWh/m² theoretical benchmarks, signaling untapped retrofit scope for energy-oriented hard-service contractors.

Soft Services, however, outpace overall growth at 11.02% CAGR, buoyed by heightened hygiene standards and flexible workplace protocols. The smart-lighting trial in Ķīpsala validates how digital tools can blend cleaning, security and workspace analytics into one data pool, elevating service quality. CleanR Grupa’s revenue gains through 9M 2024 illustrate rising outsourcing of janitorial and waste streams, with ESG dashboards becoming part of service-level agreements.

By Offering Type: Outsourcing Moves from Cost Play to Capability Play

The outsourced delivery model captures 63.62% of Latvia facility management market size and is projected to climb at 11.78% CAGR, reflecting occupiers’ shift from transactional contracting to strategic partnerships. CBRE’s Baltic earnings surge underscores appetite for bundled and integrated FM, especially among technology clusters and life-science parks.

In-house operations persist where critical infrastructure-such as RIX Riga Airport’s EUR 75 million (USD 81.75 million) passenger-terminal project-requires continual knowledge transfer and security sovereignty. Pauls Stradins Clinical University Hospital posted EUR 179.3 million (USD 195.44 million) turnover in 2023, maintaining large internal estates teams while subcontracting niche tasks under tight infection-control protocols. This hybrid adoption pattern balances core-mission focus with risk management in the Latvia facility management market.

By End-User Industry: Commercial Dominance Meets Institutional Acceleration

Commercial assets contributed 39.63% of 2025 revenue, driven by the service-sector orientation of Latvia’s economy. Real-estate data shows EUR 105 million (USD 114.45 million) of Riga apartment sales in Q1 2025, signalling sustained transaction volumes that translate into FM retainer contracts. The EUR 3 billion (USD 3.27 billion) waterfront scheme alone will add 8,000 homes and 1,000 hotel rooms, ensuring a decade-long pipeline for property-management and hospitality FM.

Institutional & Public Infrastructure sites, from government offices to military training grounds, are forecast to grow fastest at 12.16% CAGR. Defense allocations rising to 5% of GDP underwrite the Selonia Training Area build-out across Aizkraukle and Jēkabpils, opening specialized FM mandates for security, logistics and environmental oversight. Parallel upgrades in education and healthcare expand demand for infection-control, energy-retrofit and accessibility services across the Latvia facility management market.

Geography Analysis

Facility demand is heavily concentrated in the Riga metropolitan and Pierīga corridor, reflecting the agglomeration of corporate headquarters, government ministries and modern retail malls. Roughly half of Latvia’s new building permits are issued in this zone, and property deals in Riga alone tallied EUR 105 million (USD 114.45 million) in Q1 2025. Smart-city pilots such as Ķīpsala’s lighting project position the capital as an innovation sandbox that shapes national procurement standards.

Secondary cities increasingly adopt advanced FM tools to support tourism, sports and industrial zones. Rezekne Olympic Centre’s award-winning complex validates that regional authorities value BIM-enabled maintenance and renewable integration. Cesis County promotes circular-economy business models across 5,137 registered firms, creating pockets of demand for waste-auditing and resource-efficiency services.

Distributed energy producers now exceed 20,000 connections, many in peri-urban industrial parks, requiring FM support for inverter upkeep, panel cleaning and grid compliance. The evolving spread reduces dependence on the capital and diversifies growth drivers for the Latvia facility management market.

Competitive Landscape

International majors and nimble local specialists foster a moderately concentrated arena. ISS A/S posted DKK 83.7 billion (USD 12.56 billion) 2024 revenue and launched a DKK 2.5 billion (USD 375 million) share-buyback, signalling firepower to pursue Latvian public-sector tenders. CBRE extends data analytics and workplace-experience apps to differentiate on outcome-based pricing.

Regional champions such as CleanR Grupa deep-link cleaning, waste and landscaping services under Latvian regulatory frameworks, enabling agile contract turnarounds. Civic-owned newcomers win niche lots by demonstrating ESG reporting tools aligned with national disclosure law.

Technology forms the next competitive frontier. Lindström leverages IoT laundry workflows to lift plant productivity, while university spin-offs commercialize Modbus-ready smart-switch platforms that could embed into FM packages. The Latvia facility management market therefore rewards scale in compliance, breadth in service scope and depth in digital capability.

Latvia Facility Management Industry Leaders

Hagberg

Clean House

Elis

Civnity Solutions

City Service

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ISS A/S began a DKK 2.5 billion (USD 375 million) share-buyback to optimize capital structure, evidencing confidence in cash-flow strength and positioning the firm for inorganic Baltic expansion.

- January 2025: Latvia enforced tighter foreign-labor recruitment rules, prompting FM providers to accelerate automation investments and strategic workforce planning to safeguard service continuity.

- November 2024: Development Finance Institution Altum recorded EUR 26.6 million (USD 28.99 million) profit and expanded green-loan guarantees, enhancing SME access to capital for energy-retrofit projects that bolster FM demand.

- October 2024: The Sustainability Information Disclosure Law took effect, compelling 12 public-interest entities to publish ESG reports in 2025 and scaling to 206 firms in 2026, thereby elevating demand for data-driven, ESG-capable FM partners.

Latvia Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology. FMs contribute to the business's bottom line through their responsibility for maintaining what is often an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation. The objective of professional FM as an interdisciplinary business function is to coordinate the demand and supply of facilities and services in both public and private organizations.

The Latvia facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the forecast CAGR for the Latvia facility management market to 2031?

The market is projected to grow at 9.93% CAGR between 2026 and 2031, increasing from USD 322.83 million to USD 518.34 million.

Which service type commands the largest revenue share?

Hard Services account for 56.73% of 2025 revenue due to the criticality of technical maintenance and regulatory compliance.

Why are outsourced models gaining traction?

Outsourcing mitigates labor-shortage risk, supports ESG reporting, and offers single-point accountability, leading to a 63.62% share in 2025.

Which end-user segment is expanding fastest?

Institutional & Public Infrastructure facilities are forecast to grow at 12.16% CAGR because of defense and government infrastructure spending.

How does Latvia’s ESG disclosure law influence FM demand?

The law obliges over 200 companies to publish sustainability metrics by 2026, driving adoption of energy-efficient and data-rich FM solutions.

What technological trends are reshaping service delivery?

IoT sensors, BIM, AI-optimized HVAC and smart-lighting systems are enhancing efficiency and forming competitive differentiators among providers.

Page last updated on: