Large Language Model (LLM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.98 Billion |

| Market Size (2031) | USD 24.92 Billion |

| Growth Rate (2026 - 2031) | 20.08% CAGR |

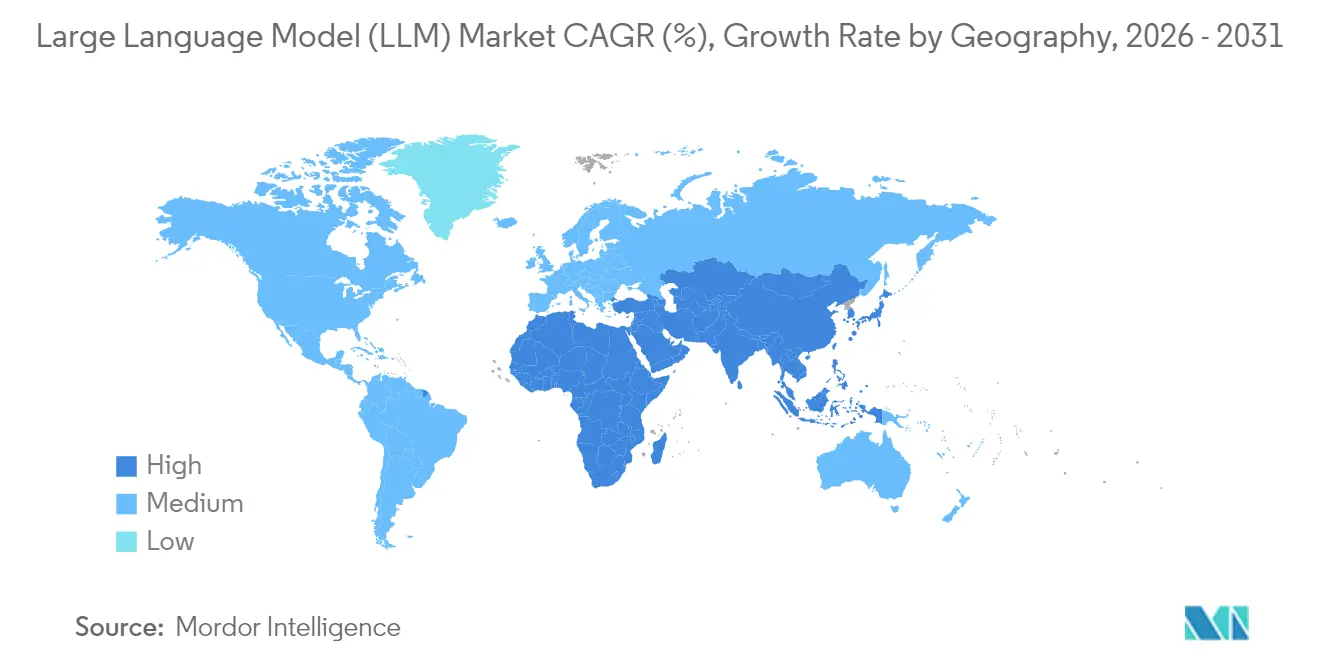

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

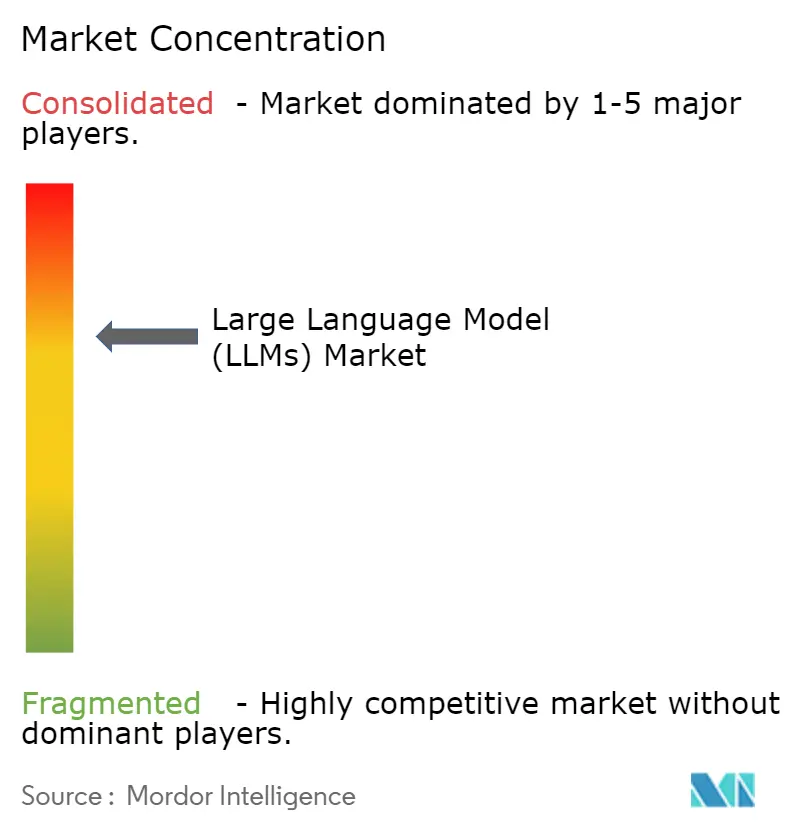

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Large Language Model (LLM) Market Analysis by Mordor Intelligence

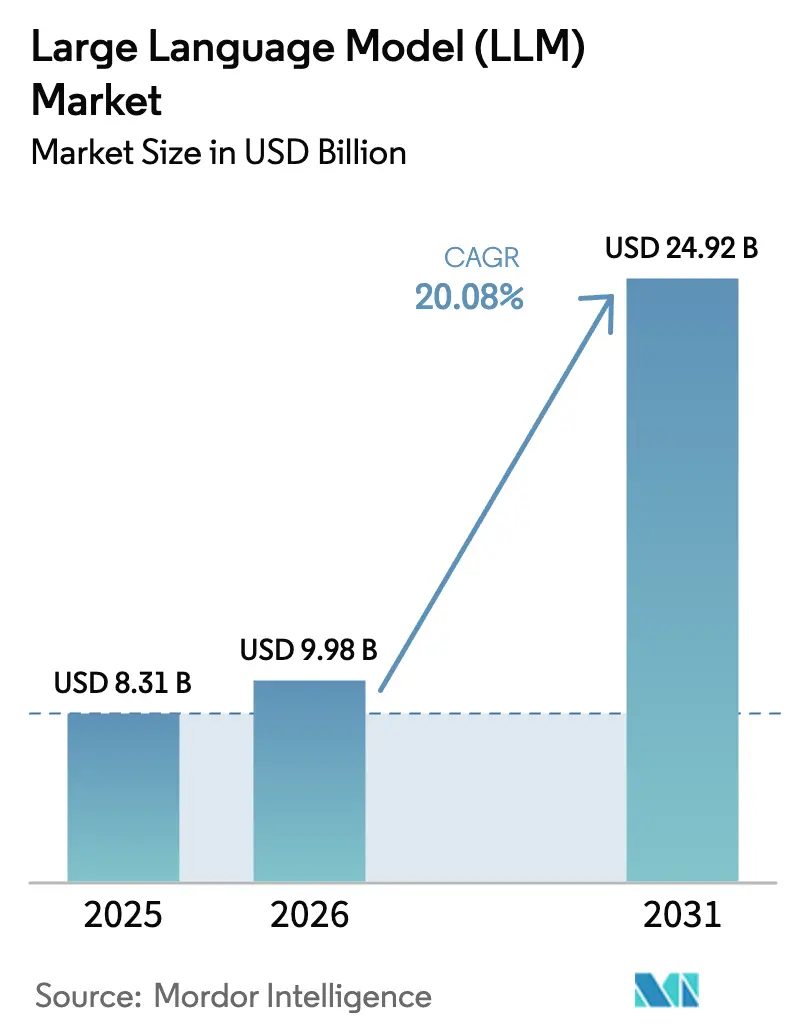

The large language model market size was valued at USD 8.31 billion in 2025 and estimated to grow from USD 9.98 billion in 2026 to reach USD 24.92 billion by 2031, at a CAGR of 20.08% during the forecast period (2026-2031). GPU innovations such as Nvidia’s Blackwell platform and AWS Trainium2 are compressing ownership costs and removing scale barriers, prompting enterprises of all sizes to pilot in-house or managed LLM initiatives.[1]Nvidia Corporation, “NVIDIA Blackwell Platform Arrives to Power a New Era of Computing,” nvidianews.nvidia.com Multimodal architectures that process text, image and audio in one pipeline are moving from research benches to commercial offerings, widening adoption beyond conversational AI into design, diagnostics and advertising. National AI regulations are pushing buyers toward regionally trained or on-premise deployments, while domain-specific APIs in banking and healthcare are displacing generic models by lowering hallucination risk and easing compliance. Edge-optimised small language models are reshaping device roadmaps for smartphone, wearables and industrial OEMs, opening fresh revenue streams for chip vendors and inference-as-a-service providers. Together, these forces point to a decade in which the large language model market evolves from concentrated cloud workloads to a tiered, everywhere intelligence fabric.

Key Report Takeaways

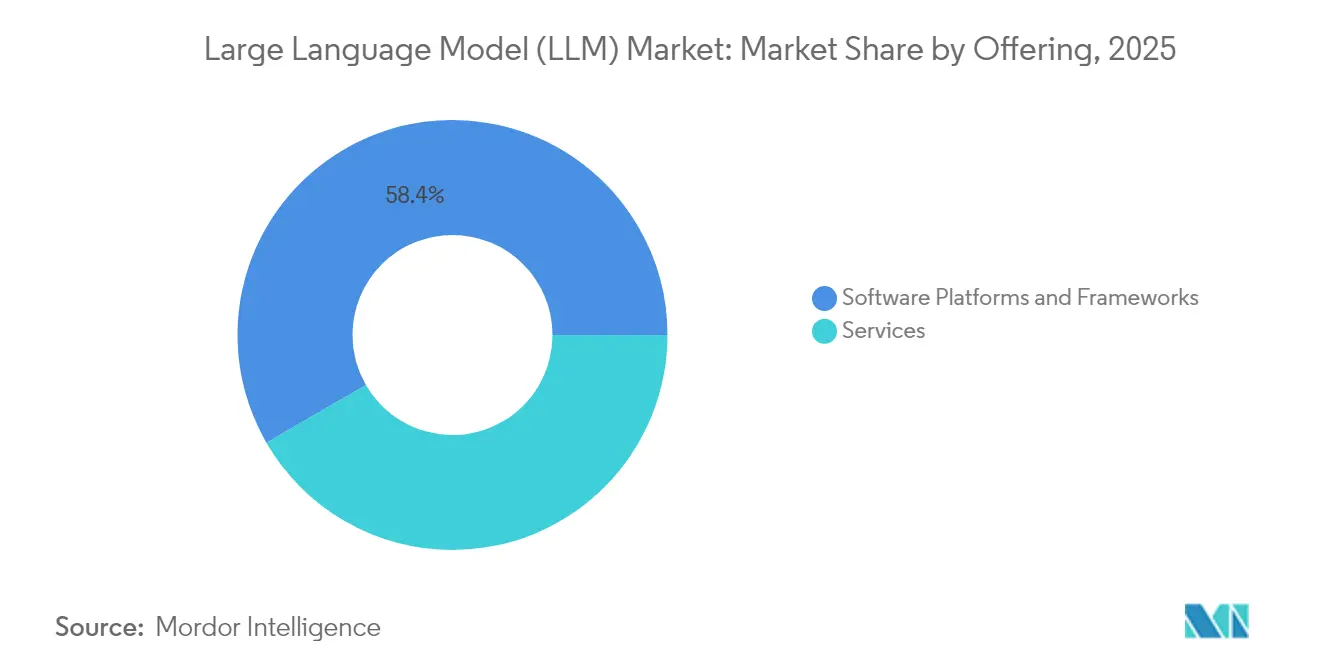

- By offering, software platforms held 58.35% of the large language model market share in 2025; services are set to expand at a 24.26% CAGR through 2031.

- By deployment, on-premise solutions led with 51.85% of the large language model market size in 2025, while edge/device deployments are advancing at a 27.25% CAGR to 2031.

- By model size, sub-100 billion parameter models captured 69.20% of the large language model market share in 2025; models above 300 billion parameters are forecast to grow at a 29.05% CAGR.

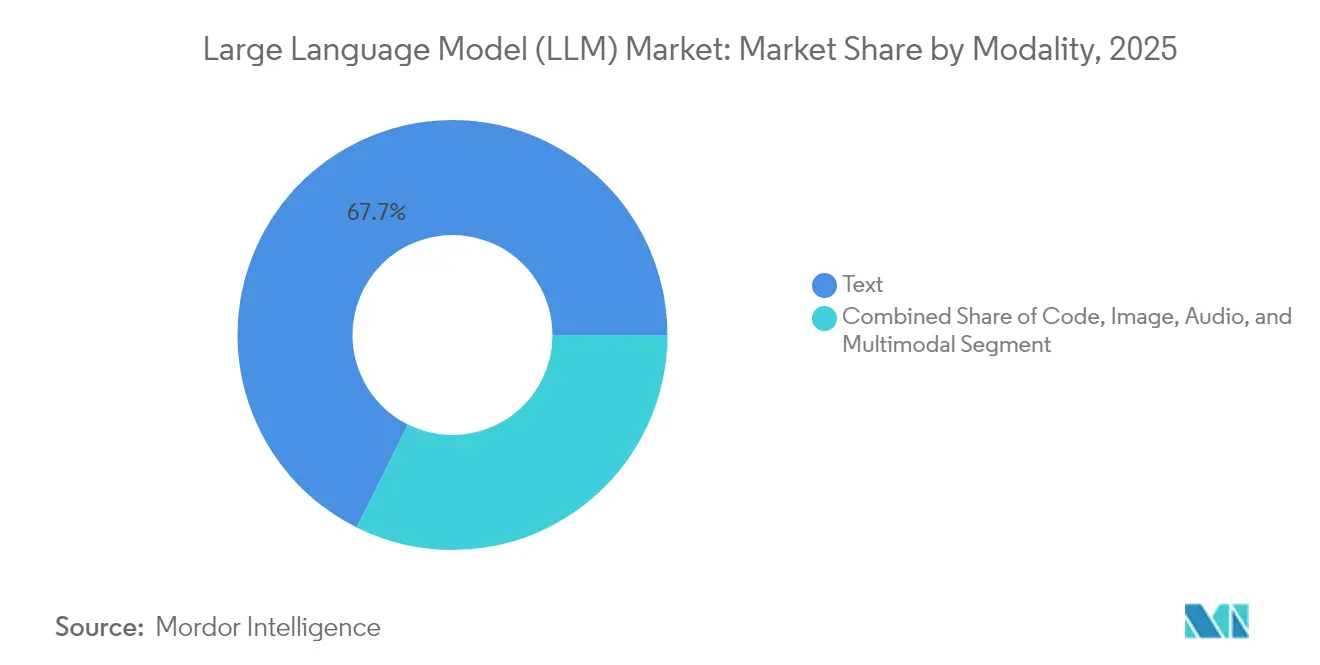

- By modality, text-centric models commanded 67.65% revenue in 2025; multimodal models are projected to post a 28.95% CAGR through 2031.

- By application, chatbots and virtual assistants held 26.35% of the large language model market size in 2025, whereas code generation tools will scale at a 24.75% CAGR.

- By end-user industry, retail and e-commerce led with 26.75% revenue in 2025; healthcare will climb at a 25.95% CAGR through 2031.

- By geography, North America accounted for 31.70% of 2025 revenue, while Asia Pacific is on track for a 31.40% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Large Language Model (LLM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Cost Declines in GPU Compute via Nvidia Blackwell & AWS Trainium2 | +5.2% | Global, with concentration in North America & East Asia | Medium term (2-4 years) |

| Enterprise-grade, Domain-Specific LLM APIs in BFSI & Healthcare (N. America) | +4.3% | North America, with spillover to Europe | Short term (≤ 2 years) |

| National AI Policies Forcing Local Training (e.g., China Interim Rules 2024) | +3.1% | China, EU, with global implications | Medium term (2-4 years) |

| SaaS Upsell Opportunity From Embedded LLM Features (Europe CRM/ERP) | +2.8% | Europe, North America | Short term (≤ 2 years) |

| Multimodal Content Demand Surge From Global AdTech Agencies | +2.5% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Edge-Optimized Small Language Models (<2 B parameters) for Smartphones | +3.7% | Global, with early adoption in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Cost Declines in GPU Compute via Nvidia Blackwell & AWS Trainium2

Nvidia’s Blackwell family, unveiled in 2024, cuts total cost of ownership for large-scale training and inference by as much as 25× relative to the prior generation, lowering both capex and energy draw. AWS Trainium2 extends those savings to managed clouds, giving mid-tier software vendors a cost path to trillion-parameter experimentation. The resulting capital efficiency removes a historical moat enjoyed by large hyperscalers, enabling regional providers and open-source consortia to release competitive checkpoints. Cost elasticity is also amplifying experimentation in parameter-efficient fine-tuning approaches that boost accuracy without line-item hardware upgrades. Collectively, these economics accelerate roll-outs across sectors ranging from precision manufacturing to personalised education, swelling the addressable large language model market.

Enterprise-Grade, Domain-Specific LLM APIs in BFSI and Healthcare

Banks are integrating finance-tuned models for credit risk triage, sanctions screening and tailored client advice, cutting manual review cycles while meeting audit standards. Healthcare networks are piloting clinically aligned assistants that parse medical notes and literature to improve diagnostic decisions, patient triage and drug discovery. Vendors emphasise tight prompt grounding and retrieval-augmented generation to suppress hallucinations and pass regulatory muster. Subscription models that meter tokens or outcomes fit existing procurement norms, easing sales cycles. With stringent data governance rules in both industries, these specialised APIs are displacing general models and cementing a premium tier in the large language model market.

National AI Policies Forcing Local Training

China’s Interim Measures and the EU AI Act require risk classification, security filings and, in many cases, local model training digital-strategy.[3]European Commission, “Regulatory Framework on AI,” digital-strategy.ec.europa.eu Enterprises now weigh jurisdictional fragmentation against efficiency, leaning toward sovereign clouds or on-prem clusters to safeguard proprietary data. System integrators are responding by launching regional model hubs, often co-financed by telcos or state funds, to ensure linguistic coverage and faster government clearance. The shift is spawning new regional champions and eroding the one-model-serves-all thesis that dominated early large language model market growth. In parallel, local training produces culturally aligned outputs, enhancing user acceptance in sectors such as public services and broadcast media.

SaaS Upsell Opportunity From Embedded LLM Features

CRM, ERP and workplace platforms are layering generative functions-automatic email drafting, deal-risk summarisation, financial close reconciliation-directly into their existing interfaces. Vendors have started moving away from per-seat pricing toward usage-based tiers that better align value with compute consumption.[4]European Commission, “Regulatory Framework on AI,” digital-strategy.ec.europa.eu Upsell strategies hinge on leveraging customer data already sitting in the SaaS stack, delivering context-rich answers competitors struggle to replicate. For buyers, the model minimises integration overhead and realises time-to-value within weeks, prompting allocation of budget previously reserved for discrete AI pilots. This dynamic broadens the total accessible large language model market beyond AI teams to line-of-business stakeholders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Inference Energy Cost ($0.12/1K tokens) Limiting SMB Adoption (S. America) | -2.1% | South America, Africa, Southeast Asia | Short term (≤ 2 years) |

| EU AI Act High-Risk Compliance Overheads | -1.8% | European Union, with global implications for companies serving EU markets | Medium term (2-4 years) |

| Scarcity of Multilingual Training Data for African Languages | -1.3% | Africa, with global implications for inclusive AI | Long term (≥ 4 years) |

| Hyperscaler Control of H100 GPU Supply Constraining On-Prem HPC | -1.9% | Global, with particular impact on emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Inference Energy Cost Limiting SMB Adoption

Running a 20-billion-parameter assistant can consume several kilowatt-hours per million tokens, translating to USD 0.12 in electricity fees for every 1,000 tokens processed in regions with grid tariffs north of USD 0.10/kWh. For small e-commerce or logistics firms operating thin margins in Brazil or Kenya, the math undermines ROI. Cloud providers are co-locating ultra-efficient cooling and renewable power, yet pass-through rates remain volatile. Energy-aware compilers and sparsity techniques are emerging, but few reach production at the budgets typical of SMB IT teams. Until inference density improves, many smaller firms will remain on legacy chatbots, capping a slice of the near-term large language model market.

EU AI Act High-Risk Compliance Overheads

The EU AI Act, effective February 2025, labels many LLM deployments in credit scoring, hiring or medical support as high risk, triggering mandatory impact assessments, human oversight loops and public registries. Penalties of up to EUR 35 million or 7% of global turnover elevate board-level scrutiny. Documentation burdens slow release cycles and demand new tooling for dataset lineage, explainability and bias monitoring. Large enterprises can amortise the expense across product lines, while startups face delayed market entry, nudging them toward less-regulated jurisdictions. Collectively, these frictions shave points off regional growth within the large language model market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platforms Drive Enterprise Adoption

Software platforms anchored 58.35% of 2025 revenue, serving as the scaffolding for experimentation, prompt chaining and fine-tuning workflows. Feature kits that abstract tokenisation, vector search and safety filters let developers integrate generative functions without deep model knowledge. Over the forecast window, advisory and tuning services will expand at a 24.26% CAGR as enterprises seek help aligning outputs with brand tone, risk policy and latency budgets. Managed inference plans are also scaling, allowing firms to sling calls across GPUs, ASICs and CPUs based on real-time cost curves. This service layer pushes the large language model market toward an as-a-service paradigm.

Growing demand for turnkey vertical stacks is encouraging platform firms to add regulatory presets, domain vocabularies and benchmark dashboards. Contract vehicles increasingly bundle licences, usage analytics and compliance reporting, reflecting procurement norms in finance and healthcare. Independent software vendors are embedding these platforms, fuelling a partner ecosystem that broadens channel reach. As a result, the large language model market particularly rewards providers that couple open tooling with curated data connectors and robust governance features.

By Deployment: Edge Computing Reshapes AI Architecture

On-premise installations dominated 51.85% of 2025 spending as banks, hospitals and public agencies prioritised sovereignty and latency control. Regulations requiring in-country data processing further tipped budgets toward private clusters and sovereign clouds. Yet the fastest traction lies at the edge, where quantised 4-GB checkpoints now fit on flagship smartphones and industrial controllers. With a 27.25% CAGR through 2031, edge inference removes round-trip delays and eases bandwidth load, prized in autonomous inspection drones and field service wearables. Early pilots in South Korea and India demonstrate sub-100-millisecond response on 6 W mobile SoCs, highlighting a new chapter for the large language model market.

Hybrid topologies are crystallising: high-accuracy prompts initiate in the cloud, while low-risk continuations occur on-device, slashing cloud egress fees. Chipmakers are shipping NPUs tuned for 4-bit transformers, and firmware updates let OEMs ship value-adding language agents post-purchase. Together, these trends blur the boundary between cloud and product, spreading large language model market intelligence throughout the device stack

By Model Size: Parameter Efficiency Drives Innovation

Enterprises favoured models under 100 billion parameters, which captured 69.20% of 2025 revenue and typically run comfortably on eight-GPU clusters. Parameter-efficient design trims tokens while preserving context windows, evidenced by xLSTM 7B’s recurrent architecture that offers speedy inference on commodity servers. Such footprints align with cost caps in contact-center automation or policy-holder chat in insurance, keeping the large language model market accessible to mid-cap firms.

At the other extreme, >300 billion parameter models will log a 29.05% CAGR, propelled by complex reasoning, scientific discovery and multimodal composition use cases. Research alliances among pharma giants and cloud platforms aim to compress training schedules with curriculum learning and synthetic data, pushing breakthroughs in protein folding and materials design. As tooling to distil knowledge from these behemoths into smaller serving heads matures, value created at the top cascades to everyday business apps, expanding the total large language model market.

By Modality: Multimodal Capabilities Expand Application Scope

Text-first architectures earned 67.65% of 2025 income, powering summarisation, knowledge management and conversational support. However, customer engagement teams, ad agencies and clinicians increasingly require models that ingest diagrams, images and waveforms alongside text. Multimodal stacks will surge at a 28.95% CAGR by 2031, spurred by innovations in visual tokens and joint embedding spaces.Real estate apps now describe property photos in multiple languages, and radiology assistants cross-reference imaging with patient records to flag anomalies, opening fresh lanes in the large language model market.

Audio-augmented inputs push accuracy higher in call-center QA, and gesture-to-code prototypes suggest an impending interface shift. Vendors that master cross-modal alignment and latency optimisation gain a moat, as data pipelines and evaluation protocols become markedly more complex than text-only variants. Consequently, technical depth in multimodal pre-training increasingly determines leadership in the large language model market.

By Application: Code Generation Accelerates Developer Productivity

Chatbots and virtual assistants led 2025 demand at 26.35% share, automating tier-one support, HR helpdesks and virtual concierge services. They remain a gateway drug, but software teams account for the steepest climb. Code generation and review tools will grow at a 24.75% CAGR, accelerating sprints by auto-suggesting functions, catching security flaws and producing test suites. Teams using LLM pair programmers report fewer rollover bugs and tighter release cadences, demonstrating tangible ROI for CFOs and widening the large language model market funnel.

Beyond code, content creation pipelines integrate copy, layout and voice-over generation under one orchestration layer. Autonomous agents fuse retrieval, reasoning and action APIs to navigate complex workflows such as insurance claim triage or supply-chain exception handling. These emergent patterns underline a shift from single-turn prompts to multi-step orchestration, deepening the value captured by the large language model market.

By End-User Industry: Healthcare Innovations Drive Growth

Retail and e-commerce captured 26.75% of 2025 revenue, leveraging real-time product Q&A, ad copy and dynamic search re-ranking. Financial institutions pivoted to anti-fraud analytics and contextual customer advisory, driving cross-selling without ballooning headcount. Yet healthcare will post a 25.95% CAGR through 2031 as clinical LLMs support diagnostic reasoning, literature synthesis and personalised discharge instructions. Early pilots show reduced readmission rates when discharge notes are auto-tailored to patient literacy levels, proving direct outcome impact and reinforcing spend in the large language model market.

Life-science researchers feed lab protocol, omics and patent corpora into fine-tuned models to accelerate target identification. Government and defence outfits experiment with multilingual intelligence summarisation, while education providers test adaptive tutoring that blends concept explanation with Socratic questioning. Across these verticals, data privacy protocols and audit trails have become part of standard RFP checklists, pushing vendors to embed governance primitives deep into product design.

Geography Analysis

North America contributed 31.70% of 2025 revenue, buoyed by venture funding, university talent pools and cloud GPU supply. Enterprises there were first movers in deploying domain-specific assistants for wealth management, oncology decision support and legal research. State-level privacy bills and federal attention to algorithmic bias drive demand for explainability modules, yet overall policy remains innovation-friendly. Continuous rollout of AI-ready data centers by hyperscalers underpins regional throughput, ensuring the large language model market retains a sizable North American nucleus.

Asia Pacific will clock the fastest 31.40% CAGR as governments underwrite sovereign model initiatives and linguistic diversity spurs local checkpoints. China’s Interim Measures mandate on-shore training, stimulating domestic accelerator design and cloud services. Japan incentivises high-impact AI under its 2025 Digital Garden strategy, while India’s IndiaAI Mission opens public datasets and GPU credits to startups. Edge-native small language models resonate in smartphone-centric markets such as Indonesia and the Philippines, expanding rural coverage and swelling the large language model market.

Europe balances ambition with caution under the EU AI Act. Corporations pursue hybrid deployments to reconcile data residency with scalability, using private clusters for sensitive workloads and public clouds for burst capacity. Spain, France and Italy are ramping AI-ready server farms, often powered by renewables to meet sustainability targets. The SaaS upsell wave is pronounced here, with ERP vendors layering multilingual chat and invoice reconciliation features that satisfy local audit standards. Collectively, divergent national enforcement regimes fragment go-to-market plans but also generate advisory and compliance tool demand, keeping the regional large language model market in a steady growth lane.

Competitive Landscape

The top five vendors together control more than 85% of revenue, anchored by integrated stacks that span silicon to software. Nvidia reinforced its footing by acquiring software orchestration assets in early 2025, positioning itself as a one-stop AI platform provider nvidianews.nvidia.com. Microsoft deepened partnerships with both OpenAI and emerging lab xAI, spreading model risk and broadening customer appeal blogs.microsoft.com. Oracle aligned with Microsoft and OpenAI to offer multi-cloud AI regions, marrying compliance with elastic GPU scale.

Open-source challengers and regional specialists are punching above their weight by releasing efficient checkpoints that rival commercial licensing baselines at lower costs. Anthropic’s Claude 4 pushed multi-step reasoning benchmarks, while mix-precision fine-tunes of Meta-derived models dominate community leaderboards. Telcos in South Korea and Germany are spinning up sovereign AI clouds, aiming to capture regulated workloads and claw share from US hyperscalers. Startups that package vertical data, domain evaluation suites and rapid deployment APIs are securing contracts in insurance, logistics and mining, injecting fresh dynamism into the large language model market.

Strategic alliances, not purely model weights, now decide enterprise RFPs. Vendors offering reference architectures, cost simulators and compliance dashboards gain procurement traction. Energy efficiency, supply-chain resilience and transparent usage metrics feature heavily in master service agreements, signalling a maturing buyer playbook. With open weights eroding proprietary moats, incumbents increasingly differentiate on deployment tooling, safety integrations and global distribution capacity.

Large Language Model (LLM) Industry Leaders

-

Alibaba Group Holding Limited

-

Amazon Web Services (AWS)

-

Anthropic

-

Baidu, Inc.

-

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Anthropic launched Claude 4 models with improved multi-step reasoning.

- May 2025: Microsoft integrated technologies from Anthropic and xAI, diversifying its AI stack.

- May 2025: OpenAI introduced Codex, an agent for software development tasks.

- April 2025: Google adopted Anthropic’s interoperability protocol for AI agents.

- April 2025: Nvidia announced acquisitions expanding its full-stack AI control.

- March 2025: EY India unveiled a fine-tuned BFSI LLM built on LLAMA 3.1-8B.

- March 2025: Google invested in Anthropic, strengthening their AI partnership.

- March 2025: Nebius and YTL released Blackwell Ultra GPU instances.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the large language model (LLM) market as revenue generated from software platforms, frameworks, and related integration or fine-tuning services that enable transformer-based models exceeding one billion parameters to be trained, deployed, or consumed on-premise, in the cloud, or at the edge. According to Mordor Intelligence, value is captured at the point software or services reach paying users, whether charged per API call, subscription, or enterprise license.

Scope Exclusion: Stand-alone computer-vision generative models and sales of GPUs, ASICs, or servers are outside this study.

Segmentation Overview

-

By Offering

-

Software Platforms and Frameworks

- General-Purpose LLM Platforms

- Domain-Specific LLM Solutions

-

Services

- Consulting and Systems Integration

- Fine-Tuning and Customization

- Managed Inference and Hosting

-

Software Platforms and Frameworks

-

By Deployment

- Cloud (Public and Private)

- On-Premise/Dedicated AI Clusters

- Edge/Device-Embedded

-

By Model Size - Parameters

- Sub 7 B Parameters

- 7 - 70 B Parameters

- 70 - 300 B Parameters

- Above 300 B Parameters

-

By Modality

- Text

- Code

- Image

- Audio

- Multimodal

-

By Application

- Chatbots and Virtual Assistants

- Code Generation and Review

- Content and Media Generation

- Customer Service Automation

- Language Translation and Localization

- Sentiment and Intent Analysis

- Autonomous Agents and RPA

-

By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Retail and E-commerce

- Media and Entertainment

- Information Technology and Telecom

- Education

- Manufacturing

- Government and Defense

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Rest of Asia-Pacific

-

South America

- Brazil

- Rest of South America

-

Middle East and Africa

-

Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

-

Africa

- South Africa

- Rest of Africa

-

Middle East

-

North America

Detailed Research Methodology and Data Validation

Primary Research

To ground secondary findings, we interviewed AI product leaders, cloud-ops architects, compliance officers, and academic researchers across North America, Europe, and key Asia-Pacific hubs. Structured questionnaires probed pricing models, parameter-count preferences, compute-to-inference cost ratios, and expected upgrade cycles, enabling us to close data gaps and stress-test modeled assumptions.

Desk Research

Mordor analysts gathered foundational data from publicly accessible tier-one sources such as US Patent and Trademark Office filings on new transformer architectures, OECD digital-economy indicators tracking AI adoption, World Trade Organization customs codes covering AI software exports, and policy papers from the EU AI Act working group. We enriched those insights with company 10-Ks, developer conference transcripts, and reputable trade association briefings (for example, the Linux Foundation's LF-AI projects).

Subscription databases that we maintain, D&B Hoovers for financials, Dow Jones Factiva for deal flow, and Questel for patent landscapes, supplied additional quantitative signals on vendor revenue momentum and innovation intensity.

The sources cited illustrate the breadth of material consulted; many additional references supported data collection, validation, and clarification.

Market-Sizing & Forecasting

We employ a blended top-down and bottom-up approach. Global enterprise software spend and public cloud billing data establish the demand pool, which is then validated against sampled average selling prices multiplied by deployment volume from selected vendors. Key variables inside our model include (1) average tokens generated per user per month, (2) share of deployments running on private clusters versus public cloud, (3) average parameter count shipped in commercial releases, (4) growth in fine-tuning service contracts, and (5) regional AI policy incentives. Multivariate regression combined with scenario analysis projects each driver to 2030; analyst consensus from primary research informs the baseline scenario, while sensitivity bands capture volatility. Where supplier roll-ups lack full disclosure, partial values are gap-filled using industry-standard ratios derived from prior audited years.

Data Validation & Update Cycle

Outputs pass anomaly checks against independent metrics such as AI server shipments and cloud inference hours, followed by multi-level peer review. Reports refresh annually, with mid-cycle revisions triggered by material funding rounds, regulatory changes, or breakthrough model releases. Just before delivery, an analyst rereads the file so clients receive the latest view.

Why Our Large Language Model Baseline Commands Reliability

Published estimates often diverge because firms pick different base years, bundle hardware revenue, or assume uniform pricing.

Key gap drivers include narrower scope that omits services, aggressive extrapolation of token growth without parameter-count caps, and currency conversions frozen at older exchange rates before recent dollar strength.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.31 B (2025) | Mordor Intelligence | - |

| USD 6.4 B (2024) | Global Consultancy A | Hardware bundled, older FX rates |

| USD 5.62 B (2024) | Regional Consultancy A | Excludes fine-tuning services |

| USD 5.72 B (2024) | Trade Journal B | Assumes uniform 40% CAGR without validation |

The comparison shows how scope choices, price assumptions, and refresh cadence reshape totals. Mordor's disciplined variable selection, annual updates, and transparent model logic give decision-makers a dependable, balanced starting point for strategic planning.

Key Questions Answered in the Report

What is the current valuation of the large language model market?

The large language model market size is USD 9.98 billion in 2026 and is projected to hit USD 24.92 billion by 2031.

Which region is expanding most rapidly?

Asia Pacific leads growth with a forecast 31.40% CAGR through 2031, underpinned by government investment and multilingual model demand.

Why are edge deployments important for future growth?

Edge models deliver lower latency, stronger privacy and reduced bandwidth costs, leading the deployment segment with a 27.25% CAGR outlook.

Which industry vertical will invest most aggressively?

Ealthcare is expected to grow at a 25.95% CAGR thanks to clinical decision support, research acceleration and patient engagement applications.

How will regulations influence adoption?

Policies such as China’s Interim Measures and the EU AI Act encourage local training, raise compliance costs and steer buyers toward explainable, regionally hosted models.

Are smaller models replacing giant models?

Enterprises favour sub-100 billion parameter models for cost-effective inference, yet ultra-large models above 300 billion parameters still dominate complex reasoning tasks and are growing at a 29.05% CAGR.

Page last updated on: