South Korea MLCC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

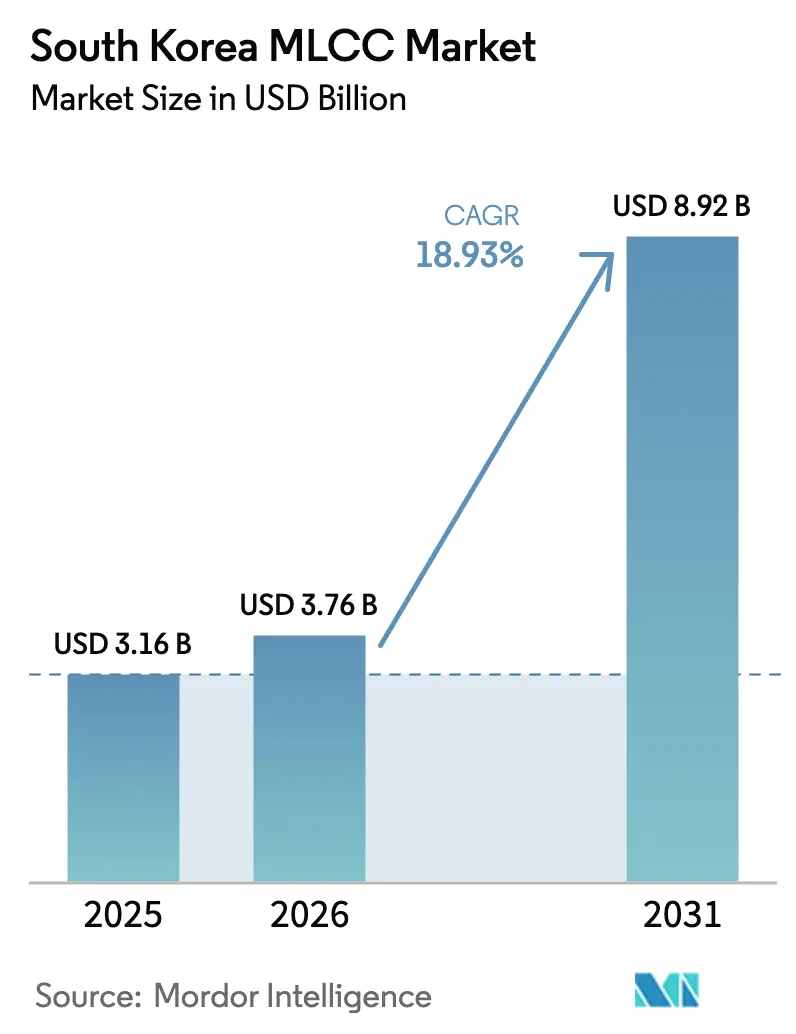

| Base Year Market Size (2025) | USD 3.16 Billion |

| Market Size (2026) | USD 3.76 Billion |

| Market Size (2031) | USD 8.92 Billion |

| Growth Rate (2026 - 2031) | 18.93% CAGR |

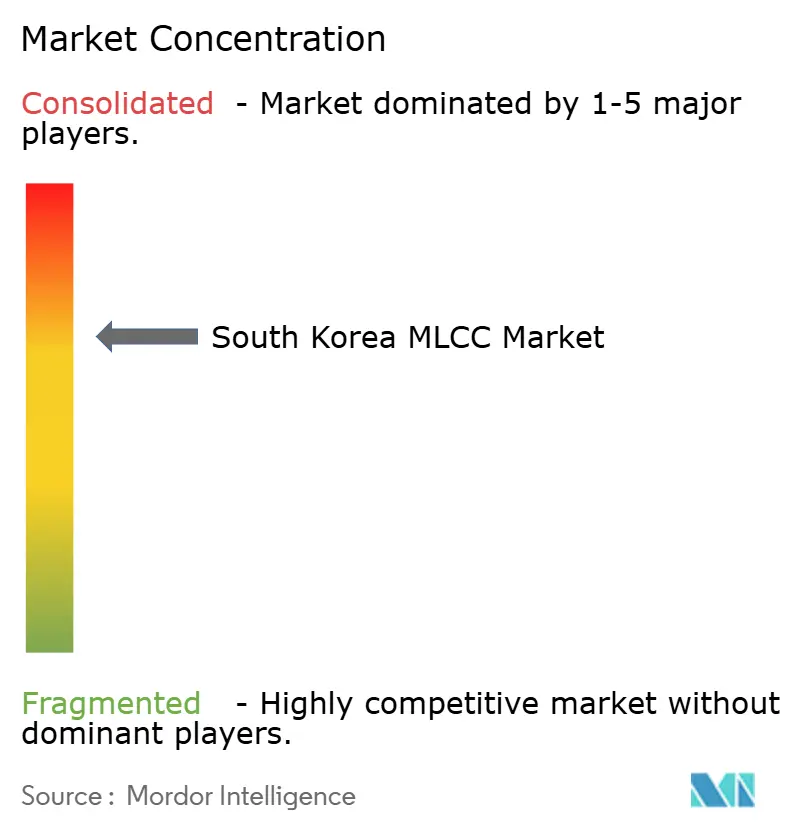

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea MLCC Market Analysis by Mordor Intelligence

The South Korea MLCC market size is expected to grow from USD 3.16 billion in 2025 to USD 3.76 billion in 2026 and is forecast to reach USD 8.92 billion by 2031 at 18.93% CAGR over 2026-2031. The rapid expansion of semiconductor fabrication capacity, sustained momentum in consumer electronics, and a sharp rise in electric-vehicle (EV) production underpin this trajectory. Local policy incentives totaling USD 471 billion are accelerating capital spending on advanced passive-component lines, while the transition to 5G and AI-enabled devices is pushing demand for high-capacitance stacks and ultra-miniaturized formats. Automotive electrification is increasing per-unit MLCC content, and the elevated adoption of glass-ceramic dielectrics is opening up ultra-high-voltage niches. Moderate supplier concentration, persistent raw material volatility, and substitution threats from thin-film polymer capacitors temper the otherwise buoyant outlook for the South Korean MLCC market.

Key Report Takeaways

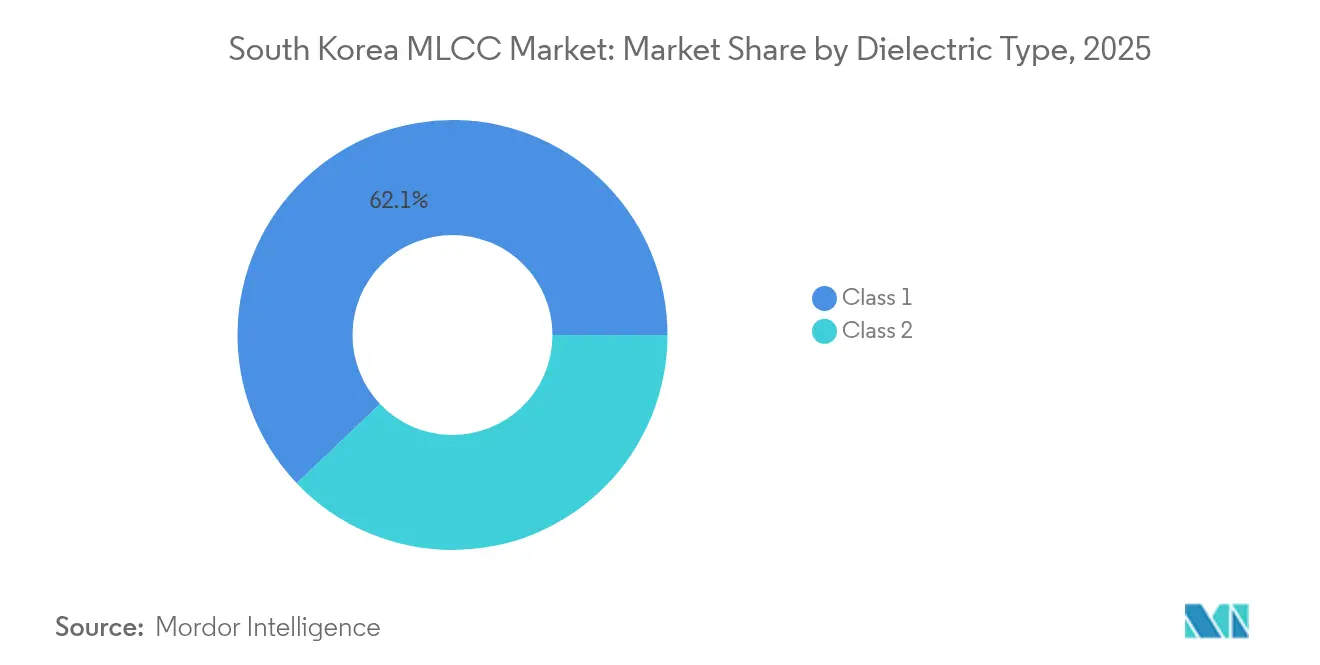

- By dielectric type, Class 1 devices accounted for 62.10% of the South Korean MLCC market share in 2025; this segment is projected to expand at a 20.16% CAGR through 2031.

- By case size, 201 devices accounted for 55.80% of sales in 2025; however, 402 units are projected to post a 19.98% CAGR to the end of the decade.

- By voltage rating, parts with a rating of ≤100 V captured 58.70% of the revenue in 2025 and are poised for a 19.92% CAGR as low-power architectures proliferate.

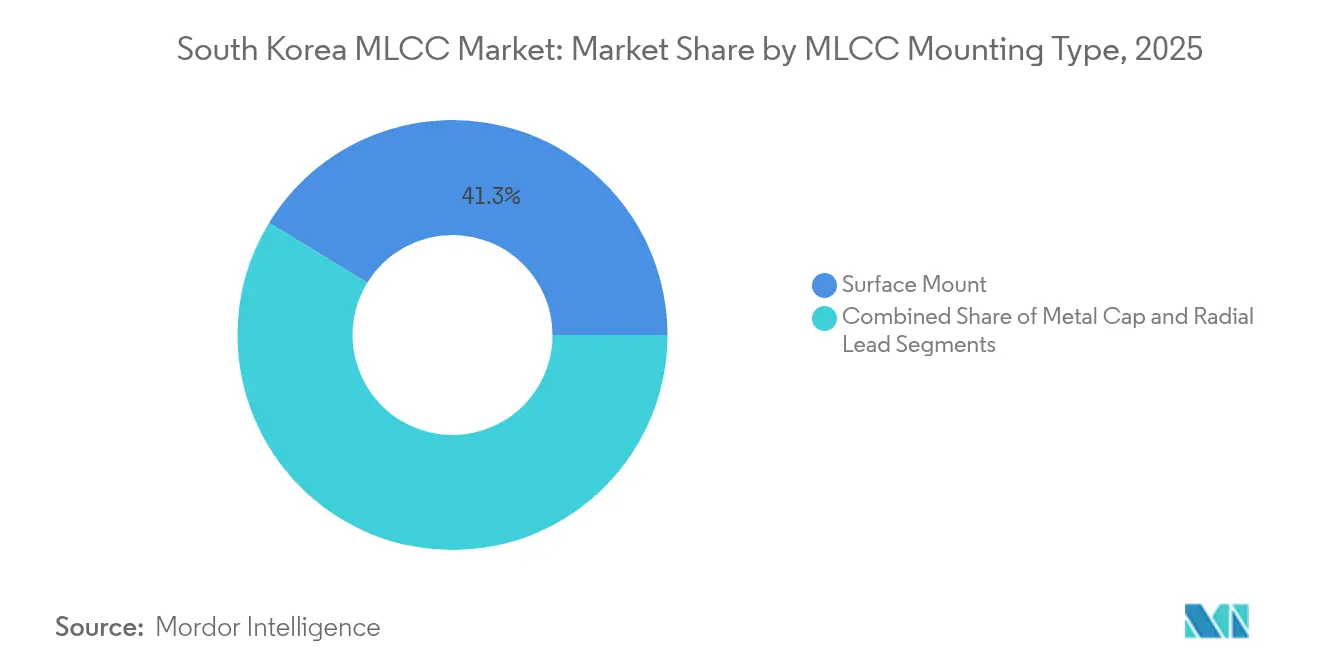

- By MLCC mounting type, surface-mount variants accounted for 41.25% of 2025 revenue, whereas metal-cap formats are forecast to grow at a 19.55% CAGR to 2031.

- By end-user application, consumer electronics led with 50.85% share in 2025, while automotive is advancing at a 20.48% CAGR on the back of EV adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea MLCC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from EV battery-management systems | +4.2% | South Korea and China | Medium term (2-4 years) |

| 5G smartphone transition toward high-capacitance MLCC stacks | +3.8% | South Korea and wider Asia-Pacific | Short term (≤2 years) |

| Government incentives for domestic semiconductor and passive-component fabs | +3.1% | South Korea | Long term (≥4 years) |

| Expansion of SiP modules in consumer electronics | +2.9% | South Korea and Taiwan | Medium term (2-4 years) |

| Reliability-focused MLCC qualification for ADAS and autonomous driving | +2.7% | Global automotive hubs | Long term (≥4 years) |

| Adoption of glass-ceramic dielectrics enabling ultra-high-voltage ratings | +2.4% | Japan and South Korea | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surging Demand from EV Battery Management Systems

Hyundai-Kia’s roadmap for full-battery platforms requires MLCCs that can withstand temperatures of up to 150 °C and voltages of up to 1,000 V, thereby raising the specification thresholds for thermal stability and breakdown strength. Samsung Electro-Mechanics has already scaled its automotive-grade output and signed supply agreements with BYD to support 800V vehicle architectures. [1]Parth Sanghvi, “Samsung Electronics Reports Weaker Q4 Profit Amid Challenges in AI Chip Industry,” digitimes.com Each EV integrates 200–300 MLCCs only in its battery-thermal loop, a fourfold increase versus internal-combustion models, thereby reducing overall unit consumption per car. AEC-Q200 qualification lengthens design cycles by up to 18 months, thereby favoring incumbents that hold pre-certified portfolios. Volume visibility is expected to remain strong through at least 2028, providing a robust medium-term foundation for the South Korean MLCC market. Near-term upside hinges on faster penetration of 400-V to 800-V platforms in mid-segment vehicles.

5G Smartphone Design Transition Toward High-Capacitance MLCC Stacks

Next-generation handsets embed 1,000–1,500 MLCCs, roughly double the count in 4G models, to stabilize power networks feeding millimeter-wave radios and on-device AI accelerators. Samsung’s Galaxy S25 integrates stacked 0201 and 01005 capacitance arrays to preserve slim form factors while delivering higher peak currents. These ultra-small packages require high yield rates-above 85%-to stay profitable, compelling vendors to refine ceramic slurry chemistry and electrode alignment. As 5 nm and below application processors proliferate, power-domain segmentation grows more granular, necessitating tighter decoupling around each voltage island. Consequently, demand for high-frequency, low ESL parts is accelerating, propelling incremental growth in the South Korean MLCC market. Competitive differentiation is shifting toward volumetric efficiency and phase-noise suppression in RF paths.

Government Incentives for Domestic Semiconductor and Passive-Component Fabs

The K-Semiconductor Belt program offers tax credits of up to 25% on capital expenditures, directly subsidizing the installation of new ceramic capacitor kilns, laser-trim lines, and automated optical inspection systems. Samsung Electro-Mechanics has expanded its Busan campus by 40% for automotive-grade production, embedding Industry 4.0 analytics to raise first-pass yields. Policy clauses on critical-mineral diversification encourage local nickel powder synthesis and recycling, thereby easing exposure to overseas palladium markets. Alignment with AEC-Q200 and MIL-PRF-55681 standards equips South Korean suppliers to bid for global automotive and defense contracts. Over the long term, the incentive cadence will determine how quickly the South Korean MLCC market can close the technology gap with Japanese front-runners. Continuity of fiscal support across political cycles remains the main uncertainty.

Expansion of SiP Modules in Consumer Electronics

System-in-Package adoption in wearables and IoT edge devices is creating hotspots for ultra-miniaturized MLCCs that endure multiple reflow passes at up to 260 °C. The Apple Watch Series 10 showcases InFO-PoP stacking, where discrete capacitors must occupy cavities inside the substrate without exceeding the height limit. Vendors are responding with low ESL, reverse-stacked terminations that reduce loop inductance to below 30 pH, enabling sub-nanosecond transient responses. The rise of embedded passives in substrates is a double-edged sword: mid-capacitance ranges risk integration, but high-performance decoupling still favors discrete parts. Co-design partnerships between MLCC makers and packaging houses are becoming standard, locking in bill-of-materials positions early in product conception. This dynamic adds a strategic layer to demand forecasting for the South Korea MLCC market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (nickel and palladium) | -2.8% | Asia-centric supply chains | Short term (≤2 years) |

| Supply–demand cyclicality linked to smartphone production | -2.1% | Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Substitution threat from thin-film polymer capacitors | -1.9% | Global | Long term (≥4 years) |

| Supply-chain bottlenecks in mature semiconductor nodes | -1.7% | Global automotive and industrial hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Nickel and Palladium)

Palladium spot prices spiked 40–60% during recent trade frictions, rapidly eroding capacitor margin structures. [2]Kathryn Ackerman, “The Semiconductor Market Going into 2025,” sourceability.com South Korean manufacturers now hold 90–120 days of powder inventory to buffer shocks; however, longer disruptions can still squeeze their gross profit. Substituting copper or conductive polymers remains technologically feasible but requires three to five years of AEC-Q200 and safety approvals. Strategic sourcing agreements with miners often include price-capping clauses, but force-majeure terms can dilute protection during geopolitical crises. The high-purity powder capacity is geographically concentrated, making supply diversification an ongoing challenge for the South Korean MLCC market. R&D into nickel-free electrode systems is progressing, though cost economics remain uncertain.

Supply–Demand Cyclicality Linked to Smartphone Production

Passive-component demand often fluctuates as handset makers recalibrate finished-goods inventories, resulting in wider swings in MLCC order flows. [3]TDK Corporation, “1st-Quarter FY 2024 Performance Briefing,” tdk.com Tier-1 vendors face idle-line risk when utilization sinks below 70%, yet rapid restarts can introduce quality drifts. Chinese OEM share gains add forecasting complexity because their procurement cadence diverges from that of incumbents. Mature smartphone markets rely on replacement cycles, which slow underlying unit growth and emphasize seasonal launches. Diversifying into automotive and industrial channels is reducing volatility, but it imposes longer design-in horizons and tighter quality audits. Balancing this mix is now central to capacity planning decisions in the South Korean MLCC market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dielectric Type: Class 1 Dominance Drives Premium Applications

Class 1 devices captured 62.10% of the South Korean MLCC market in 2025, reflecting their stable capacitance over the –55 °C to 125 °C range and tight ±5% tolerances. This share is forecast to widen as these parts exhibit a 20.16% CAGR through 2031, reinforcing their role in 5 G radios, precision timing circuits, and ADAS modules. Performance gains stem from BaTiO₃ heterostructures that achieve 19 times higher energy density without sacrificing temperature stability. Suppliers are optimizing sintering profiles and dopant chemistries to mitigate grain boundary diffusion, a key factor in maintaining yield losses below 7%.

The South Korea MLCC market further benefits as glass-ceramic Class 1 formulations unlock ratings above 1,000 V, aligning with 800 V traction inverters and industrial drives. Automotive OEMs impose AEC-Q200 cycling, which stresses insulation resistance after 2,000 thermal swings. A test, Class 1 parts meet this requirement more reliably than Class 2 options. Consequently, premium ASPs offset higher kiln energy costs, protecting supplier margins. Although R&D expenses rise, first movers gain multiyear design-in stickiness, sustaining the leading share of Class 1 offerings.

By Case Size: Miniaturization Pressures Drive 402 Growth

201-size capacitors accounted for 55.80% of revenue in 2025, thanks to robust assembly yields of around 95% and compatibility with legacy SMT lines. Yet, 402 formats are projected to climb at a 19.98% CAGR, driven by smartphones and wearables that require thinner boards without compromising capacitance budgets. The South Korea MLCC market size for 402 packages is thus rising quickly alongside investments in sub-micron screen-printing masks and advanced placement heads.

Yield learning curves are steep: every 1% scrap increase can shave 45 bps off EBIT margins, making process control critical. Automotive boards, by contrast, favor 603 and 1005 cases for their vibration robustness, thereby creating a bifurcation in demand. Ultra-small 01005 units remain niche because optical inspection with pixel resolutions below 8 µm is more costly. However, in high-density SiP assemblies, their adoption safeguards South Korea MLCC market growth by meeting aggressive form-factor targets.

By Voltage: Low-Voltage Segments Balance Performance and Cost

Capacitors rated at 100 V or less accounted for 58.70% of 2025 sales and exhibited the fastest 19.92% CAGR, aligning with sub-1 V core rails in advanced processors. Such dominance highlights the South Korean MLCC market's size advantage in consumer electronics, where the cost-to-performance ratio is a key consideration. Thickness reductions in dielectric layers improve volumetric efficiency, yet they also push dielectric breakdown thresholds closer to operating points, necessitating tighter process windows.

Mid-voltage (100–500 V) categories are growing steadily in LED lighting drivers and industrial control units, while grades exceeding 500 V are increasingly earmarked for silicon-carbide inverters in renewable energy plants. Glass-ceramic stacks with layer counts exceeding 500 are entering pilot runs, targeting 1,200 V ratings for wide-bandgap semiconductor modules. These specialized offerings elevate ASPs, partially hedging against the value-deflation trend in low-voltage mass markets.

By MLCC Mounting Type: Surface-Mount Technology Leads Market Transformation

Surface-mount units accounted for 41.25% of 2025 revenue and remain central to automated assembly flows across Korea’s handset and TV plants. Process innovations—such as plated-termination alloys that resist tin-whisker growth—are improving joint reliability under 125 °C reflow, extending SMT leadership. The segment’s 18.93% CAGR parallels the broader South Korea MLCC market trajectory, fueled by 0201 line-rate upgrades on flagship SMT platforms.

Metal-cap styles, though niche at present, are surging at 19.55% CAGR as EV control boards demand higher vibration resilience and thermal pathways. These caps shield ceramic cores from flexural stress, cutting fracture incidents by up to 80% in field tests. Radial-lead types retain footholds where through-hole soldering offers mechanical assurance—such as grid-tied inverters and rail traction electronics. Yet their share is slipping as designers consolidate on SMT to trim board real estate.

By End-User Application: Automotive Growth Accelerates Market Transformation

Consumer electronics generated 50.85% of the revenue in 2025, primarily from smartphones, tablets, and smart TVs manufactured domestically by Samsung and LG. Model refreshes pivoting to foldable displays, preserving unit counts, though growth moderates as replacement cycles lengthen. Meanwhile, automotive demand is soaring at a 20.48% CAGR, with every battery EV incorporating up to 8,000 MLCCs across traction inverters, BMS, and infotainment subsystems. The South Korea MLCC market, therefore, gains a mitigating buffer as handset cyclicality cools.

Telecommunications infrastructure-the build-out of 5 G small cells and data centers-is another solid pillar, advantaged by glass-ceramic dielectrics that maintain low loss at high frequencies. Industrial automation and renewables deliver steady, specification-heavy orders that lengthen product life cycles and stabilize ASPs. Medical device adoption inches forward, anchored by rigorous biocompatibility and longevity tests, which secure durable, albeit small, revenue streams.

Geography Analysis

South Korea anchors regional demand and supply, leveraging proximity to Samsung Electronics and LG assembly clusters that facilitate rapid design-iteration loops and just-in-time logistics. Domestic policies subsidize advanced packaging nodes, where MLCCs ensure power integrity, thereby integrating component makers into broader semiconductor value chains. Proximity advantages shorten qualification timelines for handset releases that refresh every 12–18 months, reinforcing stickiness between OEMs and local MLCC suppliers.

Cross-border trade with China amplifies the South Korean MLCC market, as finished capacitors are moved into Shenzhen and Chongqing board-stuffing lines before re-entering Korea as complete devices. This circular flow exposes the economy to Chinese economic fluctuations but also opens up volume channels unavailable elsewhere. Japanese rivals Murata and TDK continue to command steep premiums in precision classes, yet the tariff landscape and shipping costs bestow strategic leverage on Korean incumbents.

Northeast Asia’s clustering does, however, accentuate systemic risks from natural disasters and geopolitical frictions-events that can stall powder shipments or port clearances in hours. The 2025 normalization of global semiconductor supply unlocks kiln capacity once reserved for logic back-end, letting passive-component fabs scale. Nevertheless, top Japanese sites still possess leading-edge dielectric formulations, exerting technological pressure on South Korean producers to accelerate their materials roadmaps. These regional dynamics collectively shape both upside and downside scenarios for the South Korea MLCC market.

Competitive Landscape

Innovation and Specialization Drive Future Success

Samsung Electro-Mechanics leads domestic output while contending with Murata and TDK’s entrenched global share. Entry barriers stem from multibillion-dollar kiln networks, decade-long process know-how, and rigorous AEC-Q200 certs that newcomers struggle to attain. Samsung leverages in-house smartphone and TV demand to absorb early-ramp yield losses, cushioning profit volatility. Q4 2024 results showed an operating profit of KRW 6.50 trillion, even amid memory downturns, reflecting resilient MLCC sales to data center and EV clients.

Murata is expanding FY 2026 capex by 49.6% to scale server-grade capacitor lines. TDK is gradually rebalancing its product mix toward automotive inventories, which are expected to normalize by H2 2025. Smaller Asian firms, while agile in commodity classes, lack ceramics expertise to challenge top-tier precision segments. Strategic collaborations, such as Samsung’s tie-up with BYD, show how Korean makers deepen footprints in Chinese EV ecosystems to diversify away from smartphones.

White-space innovation centers on glass-ceramic dielectrics exceeding 1,000 V and embedded-passive packages that integrate MLCC plates within organic substrates. Disruptive threats also loom from multilayer polymer capacitors launched by Quantic Paktron at 1,200 VDC ratings. The South Korea MLCC market thus hinges on continuous process intensification, powder self-sufficiency, and co-design services that lock customers into multi-year programs.

South Korea MLCC Industry Leaders

Samsung Electro-Mechanics Co., Ltd.

Murata Manufacturing Co., Ltd.

TDK Corporation

Taiyo Yuden Co., Ltd.

Kyocera AVX Components Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Samsung Electro-Mechanics reported Q4 2024 operating profit of KRW 6.50 trillion, expanded automotive MLCC lines, and inked fresh supply pacts with BYD for EV battery-management boards.

- December 2024: Murata Manufacturing lifted FY 2026 capex to ¥270 billion (+49.6% YoY) to boost capacitor capacity for servers and e-mobility demand.

- November 2024: TDK cited prolonged automotive inventory corrections in its Q1 2024 briefing, projecting recovery by H2 2025.

- October 2024: Nature Communications published research on tungsten-bronze ceramics achieving 12.2 J/cm³ energy density, flagging a path for next-generation MLCC dielectrics.

South Korea MLCC Market Report Scope

Class 1, Class 2 are covered as segments by Dielectric Type. 0 201, 0 402, 0 603, 1 005, 1 210, Others are covered as segments by Case Size. 500V to 1000V, Less than 500V, More than 1000V are covered as segments by Voltage. 100µF to 1000µF, Less than 100µF, More than 1000µF are covered as segments by Capacitance. Metal Cap, Radial Lead, Surface Mount are covered as segments by Mlcc Mounting Type. Aerospace and Defence, Automotive, Consumer Electronics, Industrial, Medical Devices, Power and Utilities, Telecommunication, Others are covered as segments by End User.| Class 1 |

| Class 2 |

| 201 |

| 402 |

| 603 |

| 1005 |

| 1210 |

| Other Case Sizes |

| Low Voltage (less than or equal to 100 V) |

| Mid Voltage (100 ? 500 V) |

| High Voltage (above 500 V) |

| Low-Range Capacitance |

| Mid-Range Capacitance |

| High-Range Capacitance |

| Metal Cap |

| Radial Lead |

| Surface Mount |

| Aerospace and Defence |

| Automotive |

| Consumer Electronics |

| Industrial |

| Medical Devices |

| Power and Utilities |

| Telecommunication |

| Other End User Applications |

| By Dielectric Type | Class 1 |

| Class 2 | |

| By Case Size | 201 |

| 402 | |

| 603 | |

| 1005 | |

| 1210 | |

| Other Case Sizes | |

| By Voltage | Low Voltage (less than or equal to 100 V) |

| Mid Voltage (100 ? 500 V) | |

| High Voltage (above 500 V) | |

| By Capacitance | Low-Range Capacitance |

| Mid-Range Capacitance | |

| High-Range Capacitance | |

| By MLCC Mounting Type | Metal Cap |

| Radial Lead | |

| Surface Mount | |

| By End User Application | Aerospace and Defence |

| Automotive | |

| Consumer Electronics | |

| Industrial | |

| Medical Devices | |

| Power and Utilities | |

| Telecommunication | |

| Other End User Applications |

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform