Label-free Array Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

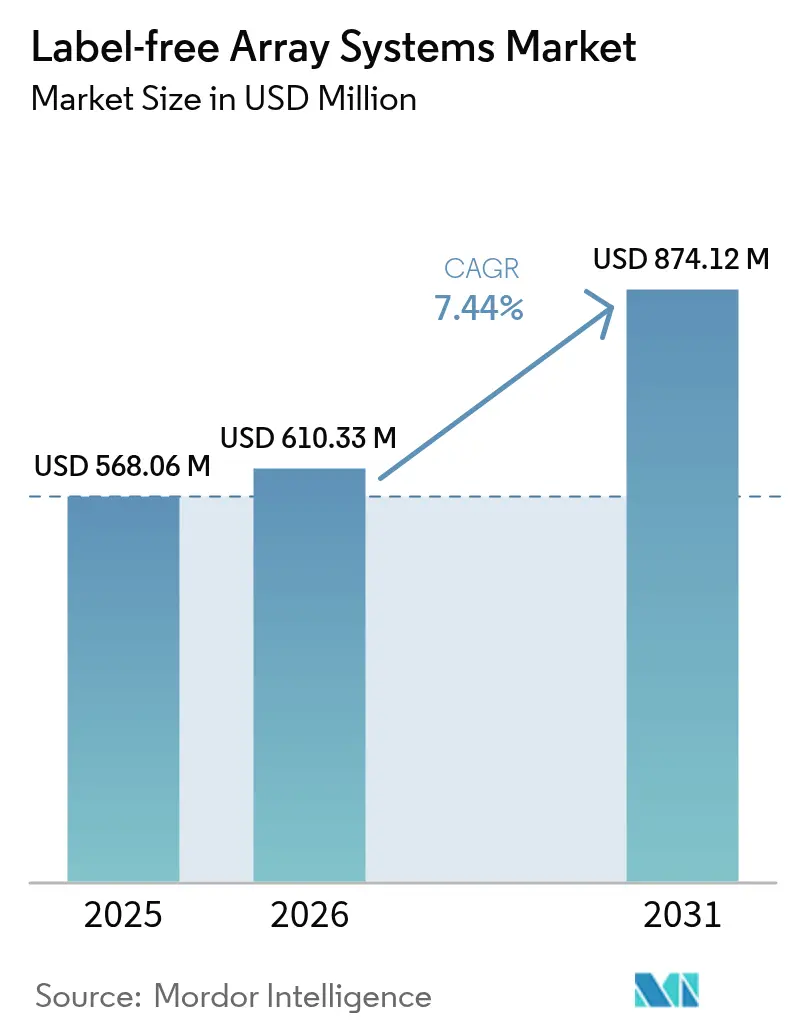

| Market Size (2026) | USD 610.33 Million |

| Market Size (2031) | USD 874.12 Million |

| Growth Rate (2026 - 2031) | 7.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Label-free Array Systems Market Analysis by Mordor Intelligence

The label-free array systems market size is expected to grow from USD 568.06 million in 2025 to USD 610.33 million in 2026 and is forecast to reach USD 874.12 million by 2031 at 7.44% CAGR over 2026-2031. Escalating pharmaceutical R&D budgets, rising demand for real-time kinetic data, and the migration toward complex biologics are solidifying the technology’s role across discovery and development programs. Major sponsors now embed label-free detection early in hit-to-lead cascades to shorten project timelines and improve candidates’ success rates. Consolidation among instrument vendors, coupled with AI-enhanced analytics, is accelerating platform upgrades and lowering data-analysis barriers. Meanwhile, regional funding initiatives in North America, the European Union, China, and India are creating a fertile environment for new applications extending into point-of-care diagnostics and cell-therapy manufacturing. Persistent challenges—chiefly high capital outlays for flagship SPR and BLI platforms and a shortage of trained nano-optics personnel—continue to temper adoption in price-sensitive segments, yet shared-facility models and leasing schemes are starting to offset cost hurdles.

Key Report Takeaways

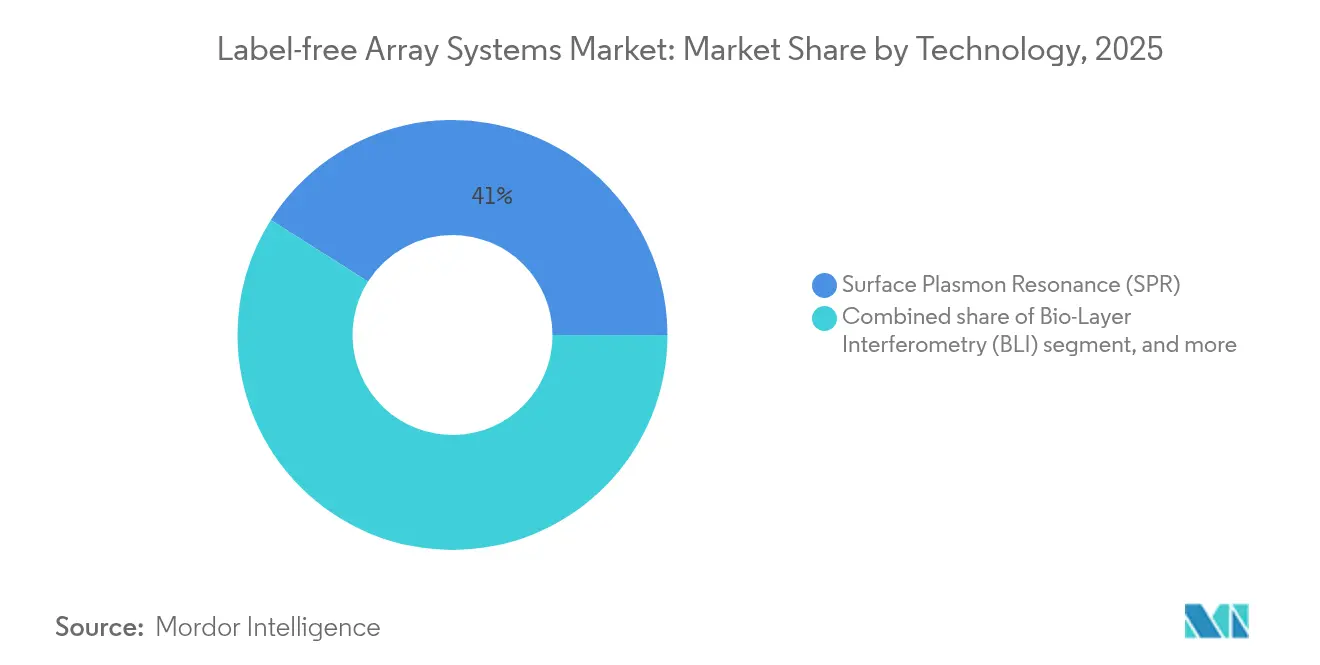

- By technology, Surface Plasmon Resonance led with 41.02% revenue share in 2025, whereas Localised Surface Plasmon Resonance is projected to expand at a 9.56% CAGR to 2031.

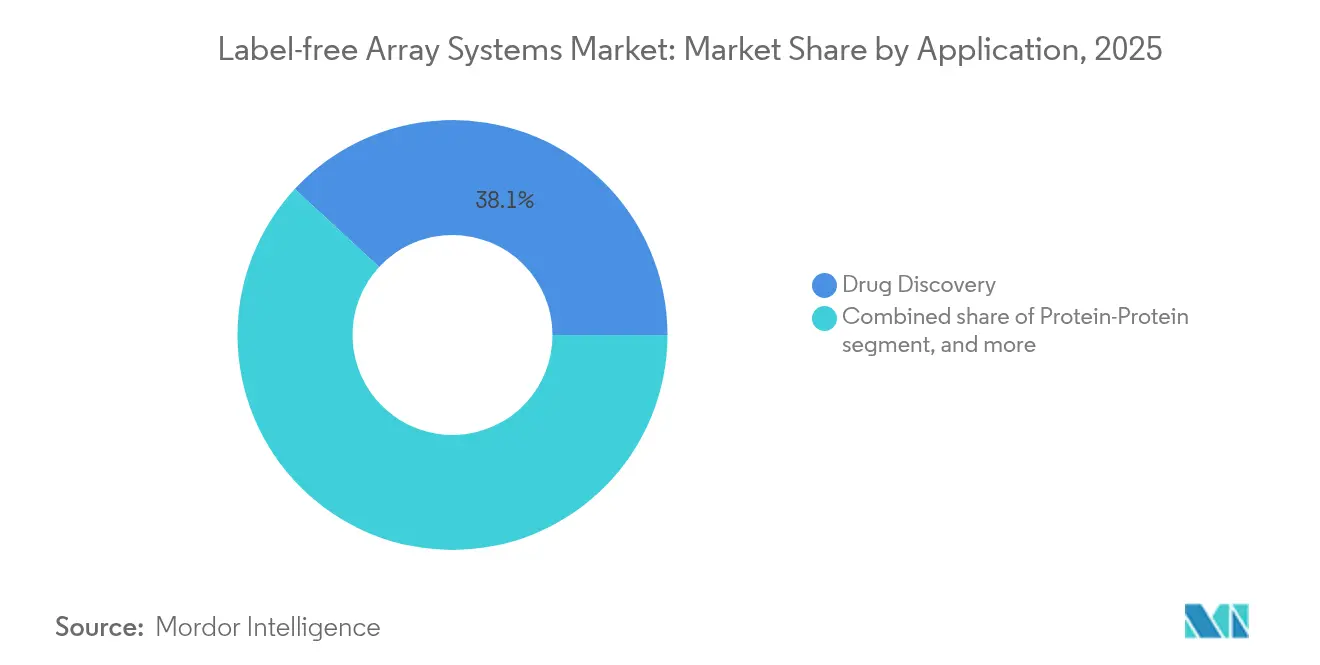

- By application, drug discovery accounted for 38.11% of the label-free array systems market share in 2025, while protein complex & cascade analysis advances at a 9.72% CAGR through 2031.

- By end user, pharmaceutical & biotechnology companies held 49.12% share of the label-free array systems market size in 2025; contract research organizations record the highest projected 10.18% CAGR to 2031.

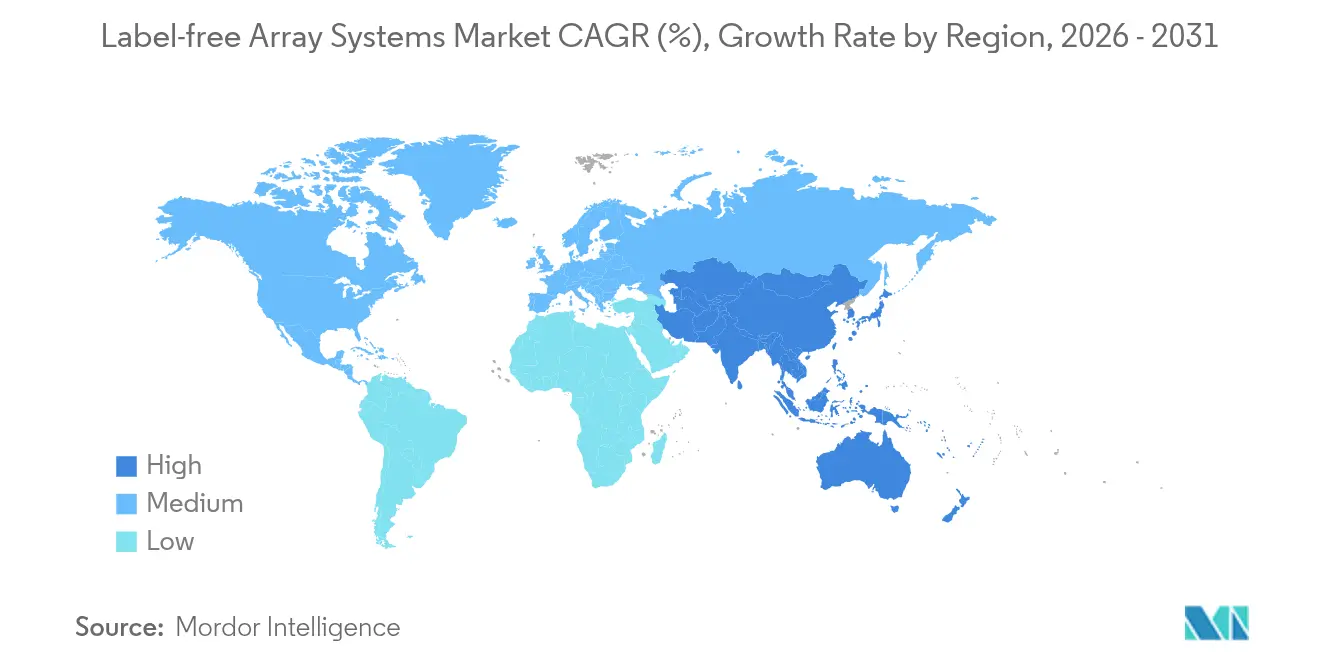

- By geography, North America commanded 44.09% of 2025 revenues, whereas Asia-Pacific is set to post an 8.51% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Label-free Array Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advantages Over Labeled Detection Techniques | +1.8% | Global – strongest uptake in North America & Europe | Medium term (2-4 years) |

| Increase in R&D Spending by Pharma & Biotech Firms | +2.1% | Global – concentrated in North America, Europe, China | Short term (≤2 years) |

| Rapid Technology Upgrades in SPR, BLI & CDS Platforms | +1.5% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Integration of AI Analytics with High-Throughput Label-Free Screens | +1.2% | Global – led by North America and select Asia-Pacific markets | Long term (≥4 years) |

| Adoption in Personalised-Medicine & Cell-Therapy Manufacturing | +0.9% | North America & Europe, emerging in China & Japan | Long term (≥4 years) |

| Nano-Plasmonic & Metasurface Miniaturisation for POC Diagnostics | +0.7% | Global – early adoption in developed markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Advantages over Labeled Detection Techniques

Label-free methods eliminate fluorescent or radioactive tags, thereby preventing steric hindrance and signal quenching that often distort binding kinetics[1]Z. Jasielec et al., “Fragment Screening by Capillary Zone Electrophoresis,” PLoS One, plos.org. Hit rates jump when fragment-based campaigns capitalize on unmodified ligands, as demonstrated by 12.4% primary hits with 92% crystallographic confirmation. Because no secondary reagents are required, assay development time drops 40-60%, freeing medicinal-chemistry teams to iterate rapidly. Stanford University’s SENSBIT platform further highlights durability gains by maintaining 70% signal after one month in serum against 11-hour lifespans for conventional sensors. Collectively, these performance premiums underpin the label-free array systems market’s swift pivot away from legacy labeled assays.

Increase in R&D Spending by Pharma & Biotech Firms

Global pharmaceutical R&D outlays reached USD 288 billion in 2024, up 1.5% year-on-year, and sizeable fractions are earmarked for advanced analytical platforms. Merck alone channelled USD 17.9 billion into discovery programs, explicitly prioritizing label-free screening capacity. As therapeutics portfolios tilt toward multispecific antibodies, gene editors, and cell therapies, high-content kinetic datasets become mission-critical for regulatory dossiers. Daiichi Sankyo’s robotics-enabled San Diego laboratory illustrates this shift, integrating automation and AI-driven label-free analytics to compress bench-to-IND timelines. The resulting uplift in Phase 1 success rates—from 60-70% with traditional screens to 80-90% on AI-paired label-free platforms—reinforces executive commitment to sustained investment.

Rapid Technology Upgrades in SPR, BLI & CDS Platforms

Instrument manufacturers are racing to out-innovate one another on sensitivity, throughput, and ease of use. Sartorius released the Octet R8e in May 2024, doubling sample capacity while boosting data fidelity for low-affinity interactions. Bruker, fresh off its Sierra Sensors acquisition, launched the 32-channel Sierra SPR-32 Pro, driving consolidated revenue to USD 795-800 million in Q1 2025[2]Chromatography Online Staff, “Bruker Debuts Sierra SPR-32 Pro,” chromatographyonline.com. Cellular dielectric spectroscopy systems now deliver label-free, non-invasive cell-quality metrics indispensable for GMP-compliant cell-therapy production. Meanwhile, microfluidic integration is shrinking complete workflows onto disposable chips, mitigating contamination risk and enabling single-use bioprocessing strategies.

Integration of AI Analytics with High-Throughput Label-Free Screens

Deep-learning models such as PAIRWISE from Weill Cornell Medicine and AstraZeneca predict efficacious drug combinations directly from label-free kinetic fingerprints, boasting 95% hit-prediction accuracy. Machine learning also prescribes optimal compound concentrations and flags anomalous curves before costly wet-lab follow-up. Charles River now embeds AI clustering across 1.4 million compounds, accelerating structure–activity insight for clients. Yet data-standardization gaps and talent shortages in chem-informatics limit widespread rollout, sustaining a long-term but gradual CAGR impact.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Instrumentation | -1.4% | Global – most acute in emerging markets & small enterprises | Short term (≤2 years) |

| Limited User-Side Awareness & Training | -0.8% | Emerging markets in Asia-Pacific, Latin America, parts of Europe | Medium term (2-4 years) |

| Data-Integration & Standardisation Hurdles for Phenotypic Assays | -0.6% | Global | Medium term (2-4 years) |

| Shortage of Nano-Optics Fabrication Talent | -0.5% | North America, Europe, and Asia-Pacific photonics hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Instrumentation

Premium SPR systems list between USD 200,000 and USD 500,000, while fully featured BLI rigs exceed USD 300,000 before service contracts. Semiconductor labor shortages that could require 67,000 additional U.S. engineers by 2030 inflate optics-component prices. Export restrictions on gallium and germanium have lengthened lead times, and 75% of photonics manufacturers report hiring challenges. Consequently, smaller biotechs and academic centers defer purchases, nudging them toward shared-core facilities or vendor-financed leasing programs that spread cost over multi-year horizons.

Limited User-Side Awareness & Training

Mastering surface plasmon resonance or bio-layer interferometry can require weeks of hands-on instruction, which many fast-moving startups cannot spare. Asia-Pacific’s sprinting R&D growth has outpaced the region’s training pipeline, leaving gaps in experimental design and data interpretation. Universities rarely include label-free methodologies in core curricula, constraining entry-level talent pools. Japan’s JST initiative now funds workforce programs in multiplex sensing technologies to counteract skill shortages[3]Japan Science and Technology Agency, “Ultra-High-Speed Multiplex Sensing Program,” jst.go.jp, yet near-term awareness remains uneven, restraining the label-free array systems market’s penetration rate in developing clusters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: SPR Dominance Faces LSPR Innovation

Surface Plasmon Resonance contributed 41.02% of 2025 revenue, making it the largest slice of the label-free array systems market. Vendors sustain leadership by pushing sub-nanomolar detection limits and adding multiplex cartridges that measure up to 32 interactions concurrently. The label-free array systems market size attributed to SPR platforms is expected to rise steadily at the overall industry CAGR as pharma customers modernize aging instruments. Localised SPR, however, promises the fastest growth at a 9.56% CAGR because nano-plasmonic metasurfaces deliver superior small-molecule sensitivity and suit portable diagnostics.

National Taiwan University’s pH-responsive DNA nanoswitches achieved 0.57 pM microRNA limits of detection, nudging LSPR closer to clinic-ready assays. Parallel advances in whispering-gallery-mode microlasers offer amplified evanescent fields suited to early cancer biomarker panels. The competition is spurring incumbents to incorporate nano-fabricated chips into next-gen SPR lines, blurring boundaries between bulk-optic SPR and chip-based LSPR. As price differentials narrow, procurement decisions will hinge on throughput, service footprint, and AI-analytics plug-ins rather than on raw sensitivity alone.

By Application: Drug Discovery Leads Complex Analysis Growth

Drug discovery retained 38.11% share in 2025, anchoring the label-free array systems market. Platform vendors have optimized fragment-screening workflows, enabling medicinal chemists to probe weak interactions crucial for PROTAC or molecular-glue campaigns. The label-free array systems market size for drug discovery will remain sizable even as downstream manufacturing applications rise. By contrast, protein complex & cascade analysis is projected to expand at 9.72% CAGR as multi-target and pathway-centric therapeutics demand systems-level kinetic insight.

Lawrence Livermore National Laboratory’s one-pot cell-free synthesis and fluorescence-correlation approach compresses protein expression and binding assays into hours, reinforcing the modality’s appeal for network pharmacology. High-throughput platforms like SAMDI-ASMS now screen millions of compounds label-free, underscoring scalability. As regulators scrutinize mechanism-of-action evidence for novel modalities, demand for cascade-level kinetics will keep this sub-segment on a faster trajectory than legacy single-target screens.

By End User: Pharma Dominance Meets CRO Expansion

Pharmaceutical & biotechnology firms controlled 49.12% of 2025 revenue, reflecting their historical ownership of in-house screening infrastructure. The label-free array systems market share remains high because big pharma budgets absorb multimillion-dollar capital cycles without jeopardizing cash flow. However, CROs are poised for 10.18% CAGR as outsourcing strategies widen.

Charles River’s expansion to 1.4 million curated compounds positions its service arm to capture discovery projects from resource-constrained innovators. CN Bio and Pharmaron’s organ-on-a-chip alliance illustrates how specialty CROs differentiate on emerging assays that integrate label-free detection with micro-physiological models. Academic cores still matter for basic research, yet grant-driven budgets limit their scale-up pace, ensuring that commercial CRO capacity will absorb the incremental demand through 2030.

Geography Analysis

North America led the label-free array systems market with a 44.09% revenue share in 2025, supported by deep capital pools, FDA-aligned validation pathways, and Thermo Fisher’s USD 2 billion domestic expansion plan. U.S. semiconductor and photonics ecosystems, despite skilled-labor shortages, continue to supply critical optics faster than any other region, reducing downtime for instrument upgrades. Capital-intensive biopharma clusters in Boston-Cambridge, the San Francisco Bay Area, and the Raleigh–Durham corridor collectively anchor over 40% of North American label-free install base units.

Asia-Pacific is the fastest-growing territory at an 8.51% CAGR thanks to China’s precision-medicine boom, which topped 2,400 billion yuan in 2023 and is rising 12% annually. India’s 2024 BioE3 policy designates biomanufacturing as a strategic pillar, while Japan’s JST program seeks a USD 1 trillion multiplex-sensing prize. Shimadzu’s new Karnataka factory, due 2027, will localize chromatograph and mass-spec production, trimming import dependencies. Regional growth is further bolstered by biotech parks in Shanghai’s Zhangjiang and Hyderabad’s Genome Valley that offer subsidized core-facility access to start-ups.

Europe holds a meaningful footprint, buoyed by Germany, the United Kingdom, and Switzerland’s legacy pharma majors. Waters Corporation’s new 45,000 sq ft UK machining center triples local capacity for MS components, improving resilience against supply-chain shocks. Nonetheless, industry groups advocate a “Chips Act 2.0” to protect photonics competitiveness as U.S. and Chinese incentives lure wafer-fab investments abroad. Horizon Europe grants and European Innovation Council funds continue to seed university–industry consortia that pilot label-free microfluidic prototypes for decentralized testing.

Competitive Landscape

Global competition is moderate; the top five suppliers collectively account for an estimated 55-60% of 2024 revenue, with Danaher (Molecular Devices/ForteBio), Bruker, Thermo Fisher, Sartorius, and Nicoya Lifesciences occupying leading positions. Bruker’s Sierra acquisition and rapid SPR portfolio refresh intensified rivalry, as evidenced by 10% year-on-year instrument revenue growth. Danaher leverages its global sales network and service contracts to lock in recurring consumables income, while Sartorius integrates BLI readouts into broader bioprocess suites.

Emergent firms focus on niche differentiation: Gator Bio deploys long-lifetime probes to cut consumable costs; Fox Biosystems offers fiber-optic interferometry for crude-sample compatibility; and Nicoya’s Alto uses digital micro-fluidics to miniaturize reagent volumes. AI partnerships are increasingly common: Thermo Fisher embeds cloud-based machine learning for anomaly detection; Quanterix’s planned Akoya acquisition adds multiplex imaging that can feed kinetic data back into in-silico models. Patent filings reveal heightened activity in metasurface fabrication and neural-network-assisted curve fitting, underscoring a shift toward integrated hardware-software value.

Strategic collaborations with CROs, reagent suppliers, and diagnostics start-ups round out competitive tactics. King’s College London’s nanoneedle patch prototype, developed with industrial backing, exemplifies cross-disciplinary ventures that open new clinical frontiers. Vendors also cultivate reagent ecosystems—pre-functionalized sensor chips, validated protein standards—to simplify experiment set-up and lock users into proprietary consumable streams. Taken together, technology leaps, M&A plays, and software ecosystems will continue reshaping market power dynamics through 2030.

Label-free Array Systems Industry Leaders

Corning Incorporated

Danaher Corporation

GE Healthcare

Perkin Elmer Inc.

Thermo Fisher Scientific, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Orionis Biosciences signed a USD 105 million upfront, USD 2 billion milestone alliance with Genentech to apply Allo-Glue™ molecular-glue discovery workflows.

- April 2025: Thermo Fisher earmarked USD 2 billion for U.S. manufacturing and R&D, allocating USD 1.5 billion to capacity expansions and USD 500 million to innovation programs.

- April 2025: CN Bio entered a long-term partnership with Pharmaron to scale organ-on-a-chip technology across ADME and toxicity screens.

- February 2025: Agilent Technologies committed USD 725 million to double therapeutic-nucleic-acid production by 2027.

- January 2024: Daiichi Sankyo opened a robotics-enabled San Diego discovery site focused on AI-driven molecular design.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the label-free array systems market as the total revenue generated by instruments and accompanying consumables that monitor molecular interactions in real time through physicochemical changes, primarily surface plasmon resonance (SPR), bio-layer interferometry (BLI), cellular dielectric spectroscopy, micro-cantilevers, and closely allied optical or acoustic platforms. According to Mordor Intelligence, data services, reagents, and software embedded with these instruments are included when they are sold as integrated packages.

Scope exclusion: handheld lateral-flow tests and generic microplate readers fall outside this framework.

Segmentation Overview

- By Technology

- Surface Plasmon Resonance (SPR)

- Localised Surface Plasmon Resonance (LSPR)

- Bio-Layer Interferometry (BLI)

- Cellular Dielectric Spectroscopy (CDS)

- Other Technologies

- By Application

- Drug Discovery

- Protein-Protein / Interface Analysis

- Antibody Characterisation & Development

- Protein Complex & Cascade Analysis

- Other Applications

- By End User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organisations (CROs)

- Academic & R&D Laboratories

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed procurement leads at drug-discovery CROs, R&D managers in mid-sized biotech firms across North America, Europe, and East Asia, and academic core-facility directors. These conversations clarified fleet size, utilization rates, service contract costs, and upcoming replacement cycles, letting us refine price-volume curves and future adoption assumptions.

Desk Research

We began with publicly available science and policy sources such as US NIH grant databases, the European Patent Office's Espacenet filings, OECD R&D expenditure tables, customs export codes for optical biosensors, and peer-reviewed articles indexed on PubMed that benchmark kinetic sensitivity benchmarks for SPR and BLI. Market context was enriched through annual reports and 10-Ks filed by major instrument vendors, conference proceedings from the Human Proteome Organization, and price lists archived by academic purchasing portals, which reveal prevailing average selling prices.

To cross-verify company revenues and installation footprints, we accessed paid platforms, D&B Hoovers for corporate financials and Questel for patent activity trends. Additional current-awareness pieces were drawn from Dow Jones Factiva and regulatory notices released by the US FDA and EMA. The sources cited above are indicative; many other credible publications were reviewed before numbers were finalized.

Market-Sizing & Forecasting

A disciplined top-down build linking installed instrument base, average throughput, replacement cadence, and projected pharma R&D outlays provided the initial 2024 demand pool, which was subsequently stress-tested with selective bottom-up checks from supplier shipment tallies and sample ASP × volume math. Key inputs included: 1) annual global pharma R&D spend, 2) number of IND filings, 3) installed SPR/BLI platforms cited in academic literature, 4) average five-year replacement interval, and 5) median instrument ASP shifts tied to automation features. Forecasts to 2030 rely on a multivariate regression that blends R&D spend growth, oncology trial starts, and capital-equipment inflation; parameters were vetted with subject experts to ensure realistic uptake ceilings. Data gaps where in-country shipment logs were sparse were bridged by applying regional penetration ratios derived from primary interviews.

Data Validation & Update Cycle

Outputs are passed through anomaly screens, year-on-year variance audits, and a two-level analyst peer review. Models refresh annually, with interim revisions triggered by material events such as a major instrument launch or regulatory change, and we rerun final checks just before report release to deliver the freshest view.

Why Mordor's Label-free Array Systems Baseline Remains Dependable

Published estimates often diverge because each publisher chooses different product mixes, price assumptions, and refresh rhythms. We acknowledge these variations up front so users see exactly where numbers separate.

Key gap drivers include whether accessory reagents are monetized, the breadth of detection modalities counted (some fold wider label-free detection tools into the total), and currency conversion timing. In addition, our annual update cadence contrasts with ad-hoc schedules seen elsewhere, and our ASP projections adjust for automation premiums that some models omit.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 568.06 Mn (2025) | Mordor Intelligence | - |

| USD 564.04 Mn (2025) | Global Consultancy A | Excludes consumables bundling and applies flat ASP, understating mid-term value |

| USD 485.47 Mn (2024) | Trade Journal B | Omits BLI platforms and uses 2019 currency rates, compressing baseline |

The comparison shows that while totals cluster, scope and pricing nuances drive noticeable spreads. Mordor Intelligence delivers a balanced, transparent baseline that traces back to clear variables, reproducible steps, and the latest data checkpoints, giving decision-makers a figure they can trust.

Key Questions Answered in the Report

What is the current size of the label-free array systems market?

The label-free array systems market is valued at USD 610.33 million in 2026 and is forecast to grow to USD 874.12 million by 2031 at a 7.44% CAGR.

Which technology segment leads the market today?

Surface Plasmon Resonance holds the largest share at 41.02% of 2025 revenue, reflecting its widespread use in protein-interaction studies.

What is driving rapid growth in Asia-Pacific?

China’s precision-medicine expansion, India’s BioE3 policy, and Japan’s large-scale sensing programs are generating high demand, pushing the region to an 8.51% CAGR through 2031.

Why are contract research organizations outpacing other end users?

Pharma companies increasingly outsource specialized screening to CROs equipped with advanced label-free platforms, driving a 10.18% CAGR for the segment.

How do label-free platforms reduce drug discovery timelines?

They eliminate labeling steps, provide real-time kinetic data, and integrate with AI analytics, collectively cutting assay development time by up to 60% and improving hit-to-lead efficiency.

Page last updated on: