Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

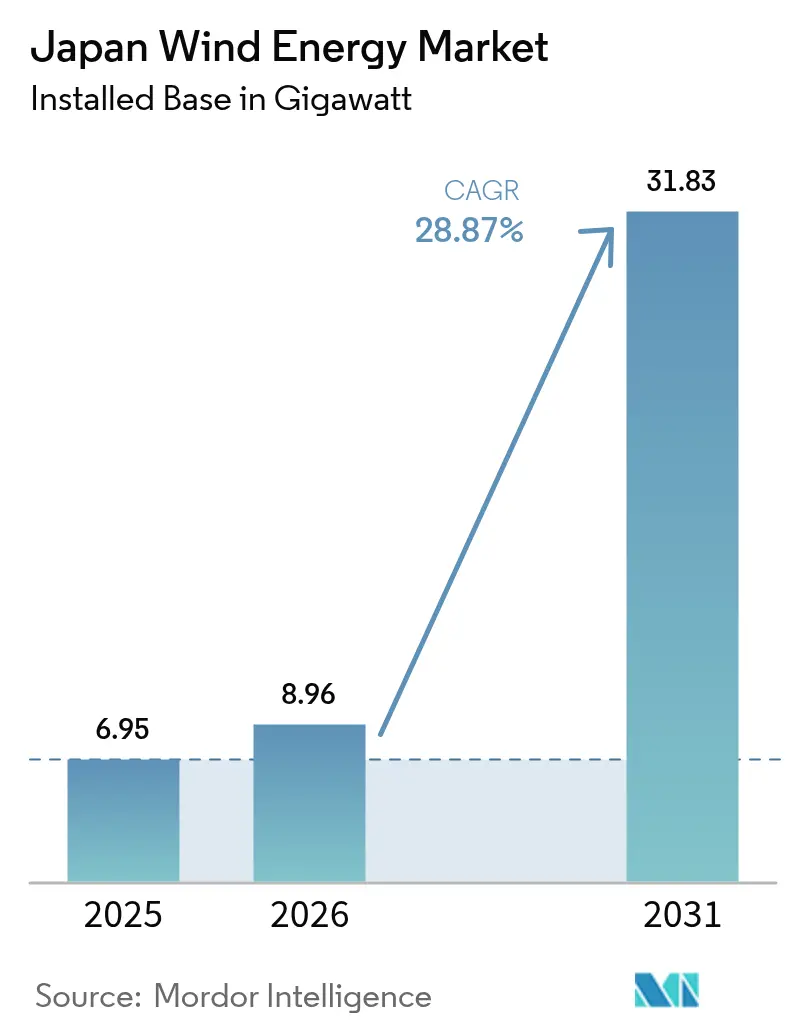

| Base Year Market Size (2025) | 6.95 gigawatt |

| Market Volume (2026) | 8.96 gigawatt |

| Market Volume (2031) | 31.83 gigawatt |

| Growth Rate (2026 - 2031) | 28.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Wind Energy Market Analysis by Mordor Intelligence

Japan Wind Energy Market size in 2026 is estimated at 8.96 gigawatt, growing from 2025 value of 6.95 gigawatt with 2031 projections showing 31.83 gigawatt, growing at 28.87% CAGR over 2026-2031.

Growth rests on Japan’s policy commitment to curb fossil-fuel dependence and achieve carbon neutrality by 2050, supported by the 7th Strategic Energy Plan that targets 40-50% renewables in the national power mix by 2040. Offshore wind auctions, sovereign transition bonds, and corporate power-purchase agreements (PPAs) channel new capital, while domestic component alliances reduce import risks and shorten project timelines. Floating-platform breakthroughs enlarge the area available for development by a factor of ten, unlocking deeper waters for future capacity. At the same time, grid congestion in wind-rich northern regions and stakeholder opposition in fishing communities temper short-term installation rates.

Key Report Takeaways

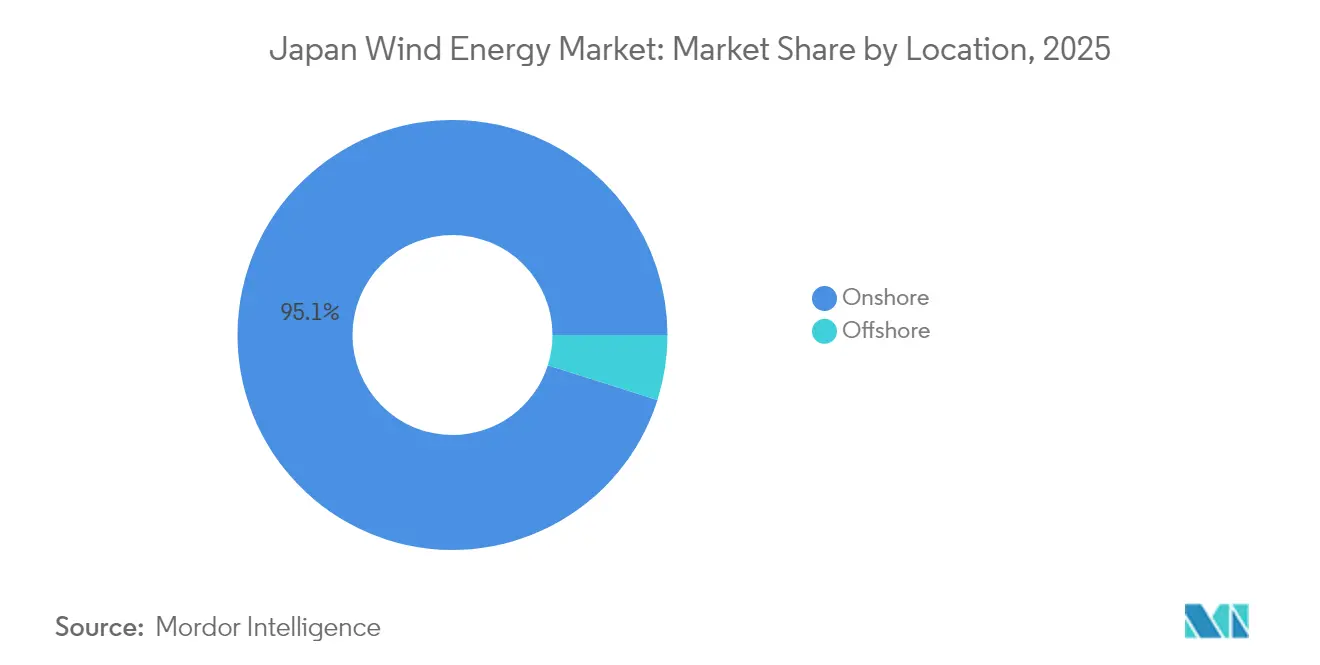

- Onshore projects captured 95.12% of Japan's wind energy market share in 2025, while offshore installations are forecast to grow at a 67.1% CAGR through 2031, signaling an impending realignment in the location mix.

- The 3-6 MW turbine segment held 47.65% share of Japan's wind energy market size in 2025; turbines above 6 MW are set to expand at a 32.93% CAGR on the back of 15 MW platforms specified for Round 3 offshore awards.

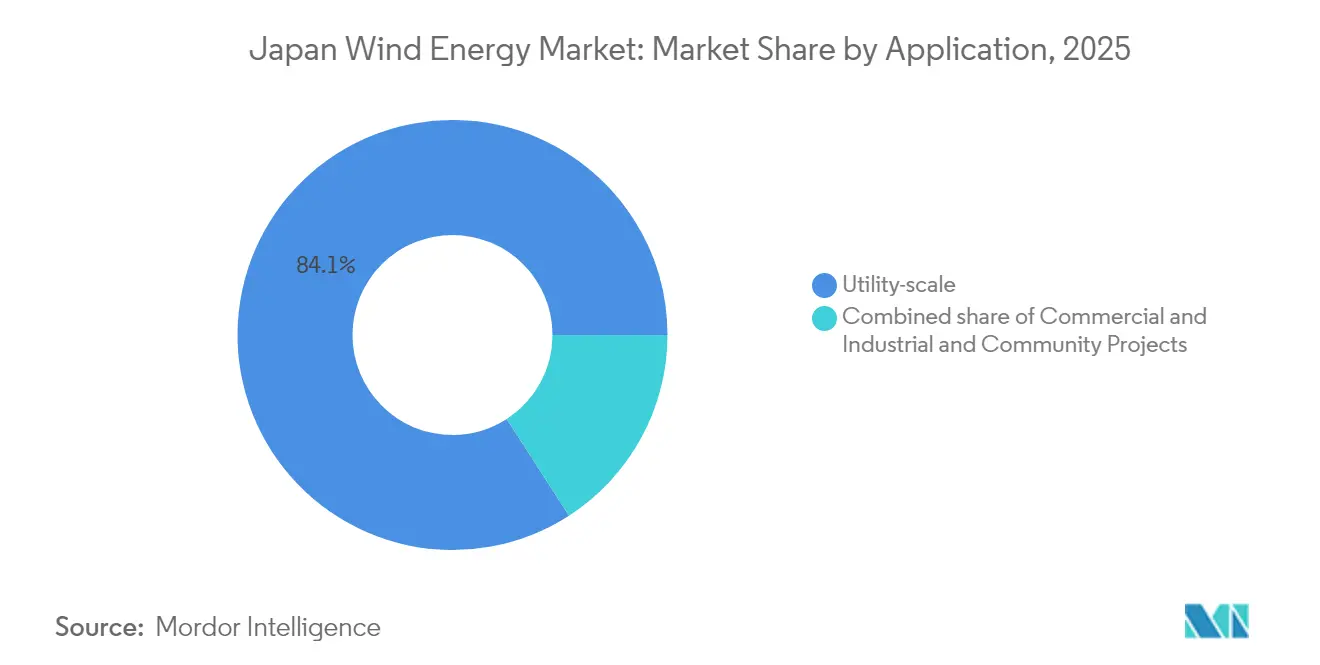

- Utility-scale applications accounted for 84.12% of the Japanese wind energy market in 2025, whereas community projects are poised to advance at a 34.8% CAGR to 2031 as municipal partnerships leverage streamlined permitting.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in offshore-wind auction rounds | +12.50% | National, concentrated in Tohoku, Hokkaido, Kyushu coastal zones | Medium term (2-4 years) |

| Declining onshore LCOE and turbine upgrades | +4.20% | National, with highest adoption in Hokkaido, Tohoku | Short term (≤ 2 years) |

| Capital inflows from green-bond issuances | +3.80% | National, with institutional demand from Tokyo financial centers | Medium term (2-4 years) |

| Corporate PPAs from data-centre & semiconductor clusters | +2.90% | Regional, concentrated in Kumamoto, Hokkaido, Tohoku | Short term (≤ 2 years) |

| Opening of Japan's EEZ for floating wind | +5.10% | National, focused on Sea of Japan and Pacific deep-water tracts | Long term (≥ 4 years) |

| National hydrogen-ammonia strategy boosting wind demand | +1.80% | National, with pilot hubs in Aichi (Hekinan), Fukushima | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Offshore-Wind Auction Rounds

Round 3 auctions in December 2024 awarded 1 GW across Aomori South and Yuza at JPY 3/kWh with mandated start-up by June 2030. Revised auction rules in January 2025 introduced price-indexation and early-operation incentives to offset cost-inflation risk.[1]Reuters, “Japan Tweaks Offshore Wind Auction Rules to Spur Bids,” reuters.comThese changes signal regulatory agility that preserves competitive pricing while broadening bidder participation. Round 4, slated for 2025, will test whether rule refinements can accelerate capacity awards without compromising local-content requirements. The approach positions auctions as a predictable growth engine for the Japan wind energy market.

Declining Onshore LCOE and Turbine Upgrades

The 147 MW Abukuma wind farm, commissioned in April 2025 with 46 GE Vernova 3.2 MW units, shows how larger turbines cut balance-of-plant costs per megawatt.[2]GE Vernova, “Abukuma Wind Farm Commissioned,” gevernova.com Domestic switchgear and semiconductor tie-ups between Vestas, Mitsubishi Electric, and Fuji Electric deepen the supply chain and lower import exposure. NEDO-funded floating vertical-axis prototypes extend cost reductions into deep-water environments, supporting broader deployment. Together, these factors lift project internal rates of return and quicken the shift toward larger, more efficient machines, advancing the Japan wind energy market.

Capital Inflows from Green-Bond Issuances

Japan’s JPY 20 trillion sovereign transition-bond program sets a benchmark for climate finance, with the February 2024 tranche of JPY 800 billion attracting strong demand under the Climate Bonds Standard. Lower coupon spreads cascade to corporate issuers, enabling attractive funding for offshore arrays and grid upgrades. Utilities are now layering fifty-year tenors into capital structures, reducing refinancing risk for complex floating-wind assets. Ample liquidity narrows the cost gap versus gas-fired alternatives and expands the Japan wind energy market.

Corporate PPAs from Data-Centre & Semiconductor Clusters

Microsoft’s virtual PPA with Shizen Energy and Equinix’s 30 MW contract with Trina Solar Japan Energy typify surging digital-sector demand for long-term green electricity. Government plans for a 300 MW Hokkaido offshore wind farm aligned to semiconductor output illustrate policy-industry coordination. JERA’s off-site PPA with East Japan Railway demonstrates transferable contract frameworks, reducing transaction costs and driving wider adoption. Corporate appetite for cost-stable wind capacity enlarges offtake certainty, anchoring new build-outs across the Japan wind energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gas-fired capacity additions under the GX roadmap | -2.70% | National, with new CCGT plants in Kanto, Kansai | Medium term (2-4 years) |

| Grid congestion & curtailment risk in Tohoku/Hokkaido | -3.40% | Regional, concentrated in Tohoku, Hokkaido | Short term (≤ 2 years) |

| Typhoon-driven O&M cost inflation | -1.90% | National, with highest impact in Kyushu, Shikoku coastal zones | Short term (≤ 2 years) |

| Fishery & local-stakeholder opposition delaying permits | -2.10% | Regional, affecting Akita, Aomori, Nagasaki offshore zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion & Curtailment Risk in Tohoku/Hokkaido

Renewable curtailment reached 1.76 TWh in FY 2023, with Kyushu recording a 6.7% rate.[3]Renewable Energy Institute, “Curtailment Trends FY 2023,” renewable-ei.org Wind-rich Hokkaido and Tohoku lie far from demand hubs, and high-voltage upgrades to Honshu will not finish before 2030. Priority dispatch for nuclear reactors squeezes available capacity in peak-wind seasons. Although Marubeni’s 25 MW/103.7 MWh battery system in Hokkaido offers partial relief, statewide storage needs exceed 2 GW. Persistent congestion threatens revenue stability and delays financing for new entrants in the Japan wind energy market.

Typhoon-Driven O&M Cost Inflation

Japan averages 11 typhoons making landfall annually, stressing turbine blades and subsea cables.[4]Japan Meteorological Agency, “Annual Typhoon Landfalls,” jma.go.jpInsurance premiums and contingency reserves add 9-12% to total O&M budgets for offshore sites. Developers now specify reinforced leading-edge protections and remote structural-health monitoring, but these upgrades raise upfront costs. While such measures extend asset life, near-term expenditure spikes pressure project economics within the Japan wind energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Offshore Surge Reshapes Deployment Mix

Offshore capacity is forecast to climb from a negligible base to roughly 12.1 GW by 2031, raising its Japan wind energy market share from 4.88% in 2025 to nearly 39% at the end of the decade. Round 3 awards totaling 1.065 GW cleared at grid-parity prices and specified 15 MW turbines that compress balance-of-system costs by roughly one-fifth. Commercial floating wind receives a legal boost from March 2025 EEZ legislation, which unlocks 150 GW of deep-water potential in the Sea of Japan and Pacific trenches.

Developers still prize onshore repowering opportunities: 1.2 GW of 1990s-era turbines can be swapped for 4-5 MW machines without adding new land footprints, and grid taps are already in place. Yet local moratoriums in Akita and Aomori and environmental reviews on migratory-bird routes hold the onshore pipeline at 800 MW. Offshore projects must contend with a domestic shortage of heavy-lift jack-up vessels; only 3 are available versus 25 in Europe, pushing developers to charter Korean or Chinese assets at premium day rates.

By Turbine Capacity: Gigawatt-Scale Platforms Dominate Offshore

Turbines above 6 MW will command more than 60% of Japan's wind energy market size at the turbine-segment level by 2031 as the country leapfrogs directly to 15 MW machines for sea-based arrays. The 3-6 MW class maintains relevance for repowering and community projects, but new onshore builds are now standardizing on 4-5 MW units that balance Class T resilience with road-transport limits.

Rotor expansion is constrained by typhoon engineering. Reinforced 70-meter blades add USD 50,000-80,000 per MW versus European equivalents. Direct-drive architectures eliminate gearboxes and trim O&M by 10-15%, but nacelles surpass 500 tonnes and need specialized vessels to lift. Repowering older 1.5 MW machines with modern 4.5 MW units can lift site capacity factors from 23% to 35%, offering a short-cycle route to volume gains.

By Application: Community Projects Gain Traction Amid Offtake Diversification

Utility-scale ventures still dominated 84.12% of installed capacity in 2025, yet community projects, defined as 10-50 MW and municipally sponsored, are running a 34.8% CAGR through 2031. Municipal schemes avoid the 3-4-year environmental impact assessments required above 50 MW and can tap local green-bond programs at below-market coupons.

Corporate PPAs underpin this rise. Invenergy’s 60 MW VPPA with Honda fixed a 15-year price that de-risked construction debt by 200 basis points. Semiconductor fabs and hyperscale data centers in Kumamoto and Kanto are evaluating similar contracts to secure baseload renewables. Balancing cost exposure and battery adders remains a hurdle, but regulatory tweaks that extend offshore lease terms from 30 to 40 years could further reduce unit costs and widen the addressable market.

Geography Analysis

Hokkaido and Tohoku supplied 67.45% of 2025 capacity additions thanks to 7-8 m/s average winds and abundant land parcels. Yet the 600 MW HVDC link to Honshu is saturated, producing curtailment rates near 20% in shoulder months. A 6-8 GW replacement line costing at JPY 2.5 trillion (USD 16.7 billion) will not alleviate pressure before the early 2030s. Wind farm valuations now hinge on grid access: sites with existing taps sell at 30-40% premiums to greenfield projects still waiting for interconnection.

Kyushu and Shikoku trail in absolute volume but host promising deep-water zones unlocked by the EEZ reform. The 16.8 MW Goto floating pilot, targeting January 2026 start-up, serves as a baseline for commercial scale-up off Kyushu’s western coast. Typhoon frequency inflates O&M by up to 35% versus Hokkaido, yet higher wholesale prices in Kyushu partially offset cost inflation.

Kanto and Kansai, despite consuming 60% of national electricity, accounted for under 10% of 2025 wind builds due to weak resource profiles and land scarcity. Corporate VPPAs bridge this mismatch: Honda’s PPA for Hokkaido wind energy supplies Kanto manufacturing, proving financial contracts can overcome geographic distance. The JPY 7 trillion grid-upgrade plan spreads spending over 10 years, so curtailment risk in the north will linger into the next decade.

Competitive Landscape

International turbine manufacturers, Vestas, Siemens Gamesa, and GE Vernova, lead on technology reliability, while domestic conglomerates such as Mitsubishi Heavy Industries and Hitachi Energy emphasize grid-compatibility services tailored to Japanese standards. Vestas’ 134 MW Inaniwa contract and its supplier MOUs with Mitsubishi Electric and Fuji Electric illustrate how foreign firms localize components to meet procurement guidelines. Siemens Gamesa and J-Power pursue hybrid service agreements bundling blade-repair drones and predictive maintenance, cutting downtime for typhoon damage.

Joint ventures deepen competitive intensity. JERA Nex bp, formed in December 2024, pools 13 GW of global offshore targets with USD 5.8 billion committed through 2030. The entity leverages JERA’s domestic customer base and BP’s North Sea expertise to bid aggressively in Round 4. Parallelly, the Floating Offshore Wind Technology Research Association (FLOWRA) aligns 18 marine-engineering firms to standardize anchors and moorings, reducing procurement prices by an expected 20% by 2028. This collaboration simultaneously incubates proprietary designs, preserving competitive differentiation.

Financial innovations also distinguish players. Itochu and Marubeni structure back-leverage deals combining sovereign transition-bond proceeds with export-credit guarantees, lowering project equity hurdles from 25% to 15%. Smaller developers counter by aggregating feed-in-premium contracts through virtual-power-plant platforms, achieving scale economies in balancing markets. These moves collectively reinforce a moderately fragmented but rapidly professionalizing field inside the Japan wind energy market.

Japan Wind Energy Industry Leaders

Japan Renewable Energy Co., Ltd.

Marubeni Corporation

Eurus Energy Holdings

Electric Power Development (J-Power)

JERA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: J-Power and Mitsubishi Heavy Industries signed a basic agreement for J-Power to acquire MHI's domestic onshore wind business, including approximately 300 MW of operating assets and development pipeline, with transaction completion targeted for April 1, 2026. The deal marks MHI's exit from wind-asset ownership following JPY 52.2 billion (USD 350 million) in losses on offshore projects, while positioning J-Power to consolidate onshore market share and pursue repowering opportunities for aging 2-3 MW turbines.

- December 2024: JERA and BP announced the formation of JERA Nex BP, a 50:50 joint venture committing up to USD 5.8 billion through 2030 to develop a combined ~13 GW offshore wind portfolio across Japan, Northwest Europe, and Australia. The JV consolidates JERA's 1 GW of operating capacity and 7.5 GW development pipeline with BP's 4.5 GW of secured leases, creating one of Asia-Pacific's largest renewable platforms with expected completion in Q3 2025.

- December 2024: Japan's Ministry of Economy, Trade and Industry awarded Round 3 offshore wind auction results: JERA's consortium secured 615 MW in Aomori (41 Siemens Gamesa SG-DD236 turbines, June 2030 COD) and BP's consortium won 450 MW in Yamagata (June 2030 COD), both bidding at JPY 3 per kWh (USD 0.02 per kWh), the first zero-premium auction in Japan's offshore wind history.

- February 2024: Japan's Ministry of Finance issued JPY 1.6 trillion (USD 10.7 billion) in Climate Transition Bonds, the world's first sovereign transition instrument, with explicit allocations for offshore wind infrastructure and grid upgrades. The issuance provided sub-1% yields, enabling utilities to refinance construction debt at rates 150-200 basis points below commercial loans.

Japan Wind Energy Market Report Scope

Wind energy is a form of renewable energy that harnesses the power of the wind to generate electricity. It involves using wind turbines to convert the turning motion of blades, pushed by moving air (kinetic energy) into electrical energy (electricity). The Japan Wind Energy Market is segmented by location, turbine capacity, and application. By location, the market is segmented into onshore and offshore. By turbine capacity, the market is segmented into up to 3 MW, 3 to 6 MW, and above 6 MW. By application, the market is segmented into utility-scale, commercial, and industrial, community Projects. The report also covers the market size and forecasts for Japan. For each segment, the market sizing and forecasts have been done based on the installed capacity (GW).

By Location

| Onshore |

| Offshore |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| By Location | Onshore |

| Offshore | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System |

Key Questions Answered in the Report

How fast is capacity expected to grow in the Japan wind energy market to 2031?

Installed wind capacity is projected to climb from 6.95 GW in 2025 to 31.83 GW by 2031, reflecting a 28.87% CAGR driven mainly by offshore projects.

Which region faces the highest curtailment risk?

Hokkaido experiences curtailment rates near 20% because its 600 MW HVDC link to Honshu is fully constrained during windy months.

What is driving the surge in floating wind interest?

March 2025 EEZ legislation opened deep-water zones, unlocking 150 GW of technical potential and spurring consortium-led R&D to cut floating-foundation costs.

How are corporate PPAs influencing project financing?

Long-term PPAs with data centers and semiconductor fabs provide revenue certainty, enabling community-scale projects to secure debt at spreads 200 basis points below utility benchmarks.

Why did some international developers exit Japan?

Ørsted and Shell cited high typhoon engineering costs, protracted stakeholder negotiations, and escalating grid-connection deposits that eroded projected returns.

What impact will new gas plants have on future wind deployment?

Approximately 4 GW of CCGT capacity entering service by 2028 could suppress wholesale prices during early renewable ramp-up years, trimming projected wind revenue streams.

Page last updated on: