Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

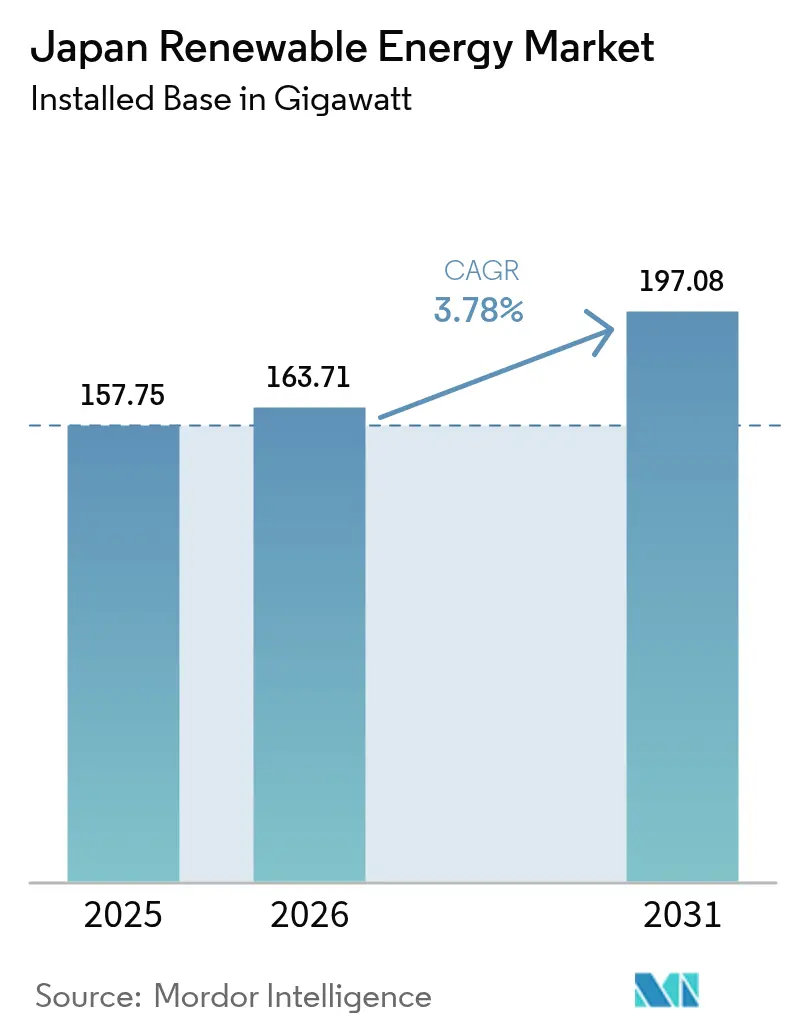

| Base Year Market Size (2025) | 157.75 gigawatt |

| Market Volume (2026) | 163.71 gigawatt |

| Market Volume (2031) | 197.08 gigawatt |

| Growth Rate (2026 - 2031) | 3.78% CAGR |

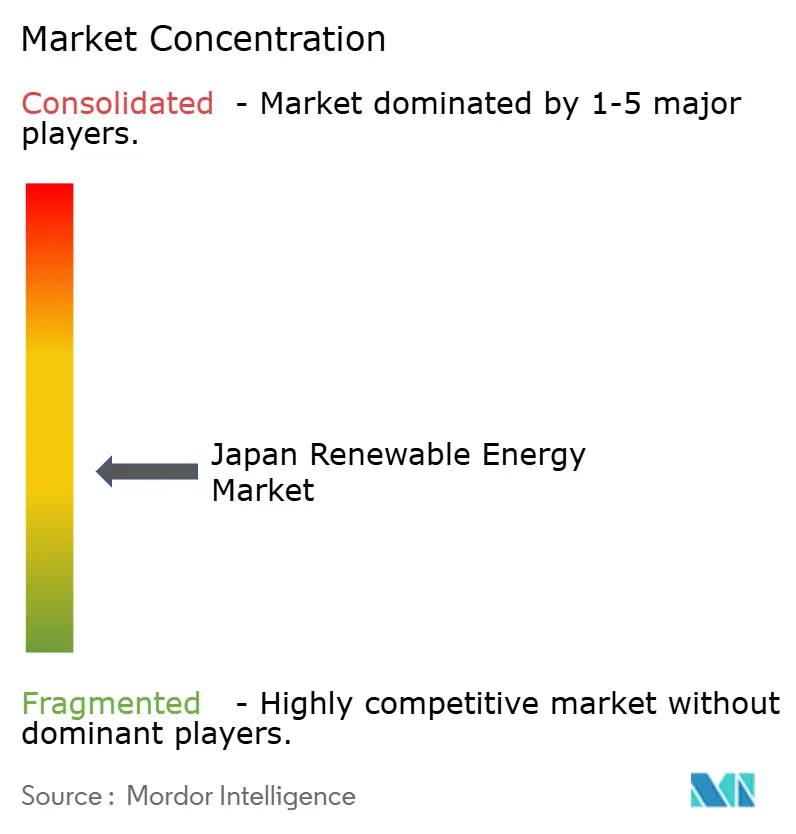

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Renewable Energy Market Analysis by Mordor Intelligence

The Japan Renewable Energy Market size was valued at 157.75 gigawatt in 2025 and estimated to grow from 163.71 gigawatt in 2026 to reach 197.08 gigawatt by 2031, at a CAGR of 3.78% during the forecast period (2026-2031).

The growth is underpinned by incremental policy support, accelerating rooftop adoption, and the roll-out of offshore wind auctions. Solar PV retains the largest installed base, yet grid congestion in Kyushu and land scarcity elsewhere are tilting marginal investment toward offshore wind, battery storage, and agrivoltaics. Merchant exposure introduced by the March 2024 Feed-in Premium (FIP) forces developers to manage price risk, while falling module and battery costs compress paybacks for households and corporates alike. Foreign turbine suppliers and Chinese module makers have intensified competition, prompting Japanese utilities to hedge with hydrogen and ammonia pilots that vie for the same capital pool. Overall, the Japan renewable energy market continues to expand, though its pace is moderated by transmission bottlenecks and lengthy environmental permitting that delay project monetization.

Key Report Takeaways

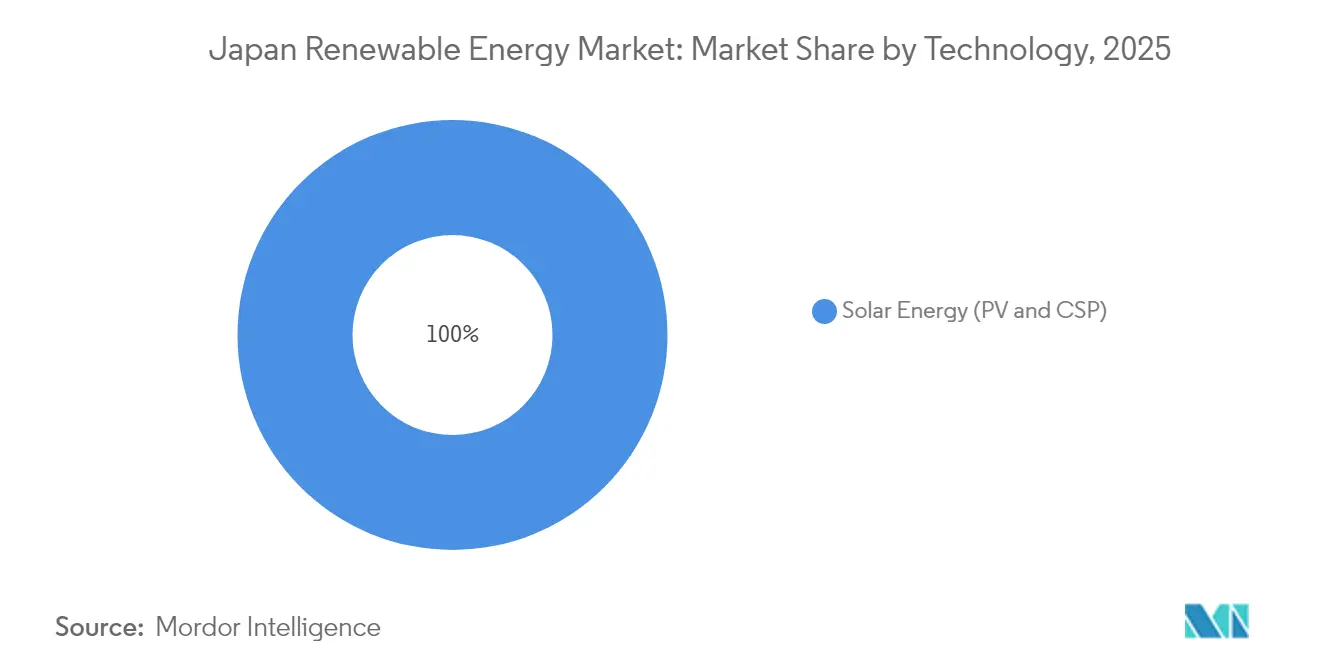

- By technology, solar energy commanded a 59.02% share of the Japan renewable energy market in 2025, while wind energy is forecast to advance at a 28.2% CAGR through 2031.

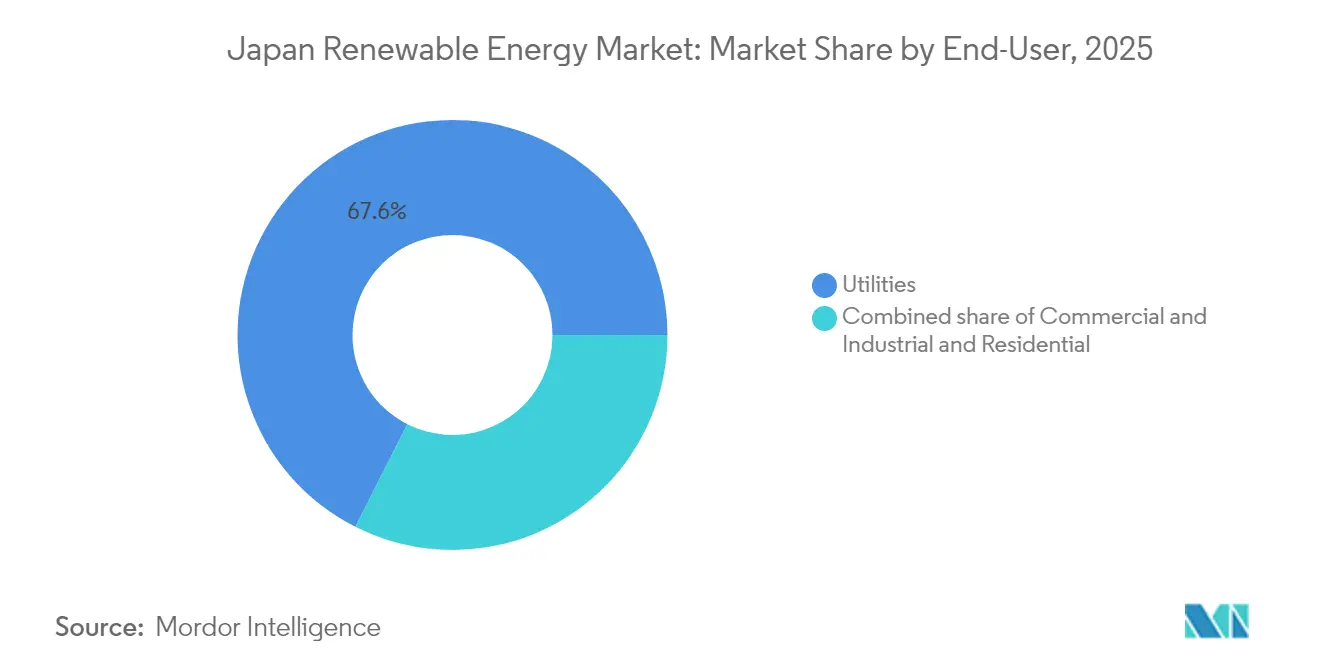

- By end-user, utilities held 67.55% of the Japan renewable energy market share in 2025, whereas the residential segment is poised to grow at a 7.25% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-competitive solar PV and onshore wind | +1.2% | National, Kyushu and Hokkaido clusters | Medium term (2-4 years) |

| Post-Fukushima energy-security mandate | +0.9% | National | Long term (≥ 4 years) |

| Offshore wind auctions and 60% local-content rule | +0.8% | Akita, Aomori, Chiba, Nagasaki | Long term (≥ 4 years) |

| Agrivoltaics unlocking farmland solar potential | +0.5% | Nagano, Yamanashi, Tochigi | Medium term (2-4 years) |

| Corporate PPA boom from tech and automotive majors | +0.4% | Kanto, Chubu, Kansai | Short term (≤ 2 years) |

| Grid-scale battery storage and V2G integration | +0.6% | Kyushu, Kanto | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-competitive Solar PV and On-shore Wind

Sharp’s 610 W TOPCon panels, with a conversion efficiency of 22.58%, and GE Vernova’s 147 MW Abukuma wind farm illustrate how efficiency gains and scale economics have driven levelized costs below fossil-fuel benchmarks.[1]Sharp Corporation, “Launch of 610 W TOPCon Module,” global.sharp Floating PV boosts output by up to 15% as water cooling lowers module temperatures, and Japan now hosts 73 of the world’s 100 largest floating arrays. National wind capacity reached 5,840 MW across 2,720 turbines in 2024, giving developers confidence to treat wind as a quasi-baseload resource.[2]Japan Wind Power Association, “Wind Statistics 2024,” jwpa.jp Competitive costs reduce reliance on feed-in tariffs, drawing institutional investors into the Japan renewable energy market and widening financing avenues.

Post-Fukushima Energy-Security Mandate

Japan’s self-sufficiency ratio climbed to 15.2% in fiscal 2023 as renewables displaced imported fuels. The 7th Strategic Energy Plan aims to elevate renewables to 40-50% of electricity generation by 2040, thereby embedding long-term policy certainty. Fukushima’s green-hydrogen hub in Namie Town highlights how disaster-affected regions are shifting from nuclear dependence to a renewables-led reconstruction. Because the mandate is situated within national security discourse, support remains consistent across administrations, shielding the Japanese renewable energy market from policy reversals.

Offshore Wind Auctions & 60% Local-Content Rule

Round 3 auctions in December 2024 awarded 1 GW at a record-low JPY 3/kWh, while obliging developers to source 60% of their power domestically. The rule has triggered investments in nacelle assembly, blade fabrication, and subsea-cable plants by firms such as JGC Japan and Sumitomo Corporation. TEPCO’s partnership with NEDO on floating-turbine prototypes aims to unlock deep-water sites beyond 50 m. Broader development zones within Japan’s Exclusive Economic Zone (EEZ) expand the viable seabed tenfold, underpinning the potential for multi-gigawatt build-out.

Agrivoltaics Unlocking Farmland Solar Potential

More than 3,000 agrivoltaic arrays now operate nationwide, with regulations requiring crop yields to remain within 80% of baseline yields on comparable farms. Semi-transparent perovskite and organic PV films achieve 5-5.5% light utilization efficiency while preserving photosynthesis, enabling farmers to rent air rights above crops without losing arable acreage. Government-designated “advanced decarbonization areas” across 36 prefectures incentivize dual-land use, adding new revenue streams for rural communities and unlocking significant latent capacity for the Japan renewable energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land scarcity and community opposition | -0.7% | Nagano, Yamanashi, Kumamoto | Short term (≤ 2 years) |

| Grid congestion and curtailment risks | -0.9% | Kyushu, Hokkaido, inter-regional links | Medium term (2-4 years) |

| Slow environmental permitting for offshore wind | -0.5% | Akita, Aomori, Nagasaki | Long term (≥ 4 years) |

| Capital flight toward hydrogen and ammonia pilots | -0.6% | Kanto, Chubu industrial nodes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Land Scarcity & Community Opposition

Large “megasolar” projects can raise local surface temperatures by 2.85 °C and trigger visual-impact complaints, adding to social friction in land-constrained prefectures.[3]ScienceDirect, “Thermal Impacts of Mega-Solar Arrays,” sciencedirect.com End-of-life panel disposal worries and wind-turbine noise concerns fuel resistance, lengthening approval cycles. Developers now deploy early stakeholder dialogues, micro-sitings and benefit-sharing models to tackle acceptance hurdles, yet consent processes still moderate the trajectory of the Japan renewable energy market.

Grid Congestion / Curtailment Risks

Kyushu curtailed 6.7% of renewable output in fiscal 2023 as inter-regional lines hit thermal limits, and nuclear units maintained inflexible baseload dispatch. The nine-area grid structure fragments power flow and complicates economic dispatch. Investments in high-capacity interconnectors, pumped-hydro upgrades, and negative-pricing rules are planned, but near-term bottlenecks persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Offshore Wind Outpaces Solar’s Installed Lead

Wind energy, encompassing onshore and offshore, is forecast to grow at a 28.2% CAGR through 2031, the highest among technologies, propelled by the 10 GW offshore target and the 1.065 GW Round 3 auction award. Fixed-bottom turbines exploit shallow sites, representing 15% of territorial waters, while floating prototypes aim to harvest the deeper 80% share of potential, positioning offshore wind as the next major pillar of Japan's renewable energy market. Transmission bottlenecks in Hokkaido restrain onshore additions, but Vestas and Siemens Gamesa secured 400 MW in 2024 orders, signaling a persistent appetite among developers.

Solar PV maintained a 59.02% portion of the Japan renewable energy market size in 2025, reflecting legacy FIT installations that added up to 91.6 GW. The FIP scheme slows utility-scale roll-out, yet residential and commercial rooftops added 3.8 GW in 2024. Agrivoltaic systems supplied 1.2 GW, leveraging dual-use benefits for land-constrained prefectures. CSP remains negligible due to diffuse isolation and land limitations, while hydropower and geothermal provide valuable baseloads but see modest expansion due to environmental and social hurdles.

By End-User: Residential Gains as Utilities Slow

Utilities accounted for 67.55% of the Japan renewable energy market share in 2025, leveraging balance-sheet strength to absorb merchant exposure under FIP. Yet capital diversion to hydrogen and ammonia, alongside curtailment-induced EBITDA erosion, is tempering incremental utility capacity. The Long-Term Decarbonization Auction reinforced a shift toward grid-service revenue streams, including storage and demand response.

The residential segment is expected to expand at a 7.25% CAGR through 2031, the swiftest among end-users, as net-metering and time-of-use tariffs shorten paybacks to 6-8 years. Battery pairing reached 40% in 2024, with Sharp and Panasonic bundling solar, storage, and heat pumps to raise self-consumption. Commercial and industrial customers, who hold 24.05% of capacity in 2025, continue to adopt onsite generation. However, the absence of a standardized virtual PPA framework constrains utility-scale offtake growth, keeping the Japanese renewable energy industry reliant on bespoke agreements.

Geography Analysis

Regional disparities shape project economics across the archipelago. Kyushu amassed 12 GW of solar capacity by 2024, supplying 40% of its generation at midday; however, curtailment on 97 days resulted in 1.2 TWh being wasted, equivalent to the yearly usage of 350,000 households. Planned inter-regional upgrades worth JPY 800 billion will add 5 GW of transfer capacity by 2030, easing the bottleneck, although completion is expected to stretch to 2032.

Hokkaido’s 1.5 GW wind fleet exploits 7.5 m/s speeds, but export fees of JPY 8-10 per kWh sap returns, capping utilization and limiting fresh build. Tohoku and Akita emerged as offshore wind nodes after the Round 3 auction, which allocated 615 MW to Aomori and 450 MW to Yuza. Orsted’s 139 MW Akita Noshiro commissioning in 2024 validated fixed-bottom economics in sub-50-meter depths despite protracted fishery talks.

Kanto and Chubu have a dense concentration of C&I solar demand, exemplified by Google’s 50 MW PPA, which powers Tokyo and Nagoya data centers. Kansai lags with only 3.2 GW of capacity, as Osaka channels funds to hydrogen hubs instead of distributed generation. Scenic-area setbacks in Nagano and Yamanashi hinder ground-mount growth, while the Goto Islands' floating pilot, delayed until 2026, aims to unlock deepwater wind across southern prefectures.

Competitive Landscape

The Japan renewable energy market features moderate fragmentation. TEPCO Renewable Power, JERA, and Kansai Electric own legacy hydro and sizable solar assets, yet face rising competition from international developers such as Ørsted Japan and Vestas, which pair EPC capability with global supply chains. Sumitomo and Marubeni are redirecting their trading-house portfolios away from coal into wind, PV, and storage, while leveraging their project-finance networks.

Technology differentiation is accelerating. Sharp commercialized high-efficiency n-TOPCon modules, Toshiba deploys AI-based wind-forecasting to reduce balancing costs, and Mitsubishi Heavy Industries tests ammonia-co-firing turbines, deepening vertical integration. Digital aggregators like REXEV bundle EV fleets into virtual power plants, expanding ancillary-service revenues and reshaping competition around software and data rather than mere megawatt ownership.[5]REXEV, “EV Aggregation Platform Enters Capacity Market,” prtimes.jp

Strategic moves include JERA’s joint venture with BP for global offshore wind, Sumitomo’s equity stake in Europe’s EEW turbine-tower group, and Marubeni’s significant investments in large-scale batteries. M&A momentum is expected to intensify as feed-in premium contracts mature and secondary market liquidity improves, pushing the Japanese renewable energy market toward a more consolidated yet innovation-led order.

Japan Renewable Energy Industry Leaders

TEPCO Renewable Power Inc.

Japan Renewable Energy Co. Ltd.

Renova Inc.

Mitsubishi Heavy Industries Ltd.

Orsted Japan K.K.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: GE Vernova turbines started operating at the 147 MW Abukuma wind farm in Fukushima, powering 120,000 homes. The wind farm utilizes 46 onshore 3.2 MW turbines.

- January 2025: Sumitomo Corporation secured financing to expand the Muara Laboh geothermal project in Indonesia to 170 MW, reinforcing its renewable pipeline. This loan is provided as project finance by a syndicate of JBIC, the Asian Development Bank, Mizuho Bank, Ltd., Sumitomo Mitsui Banking Corporation, MUFG Bank, Ltd., and the Hyakugo Bank, Ltd.

- December 2024: METI and MLIT (Ministry of Land, Infrastructure, Transport and Tourism) announced the results of the third offshore wind auction under the Act on Promoting the Utilization of Sea Areas for Marine Renewable Energy Development. In Aomori Prefecture, the Tsugaru Offshore Wind consortium, comprising JERA, Green Power Investment, and Tohoku Electric Power, secured a 615MW project. In Yamagata Prefecture, Yamagata Yuzu Offshore Wind LLC, including Marubeni, Kansai Electric Power, BP Iota, Tokyo Gas, and Marutaka, won a 450MW project.

- August 2024: Tokyo-based Sumitomo Corporation bought a stake in the newly created EEW Offshore Wind Holding. The German family-owned EEW Offshore Wind Holding now has a strong partner with international expertise in the steel market.

Japan Renewable Energy Market Report Scope

Renewable energy is the energy collected from renewable resources, such as sunlight, wind, water movement, and geothermal heat, which are naturally replenished.

Japan's renewable energy market is segmented by Technology (Solar Energy (PV and CSP), Wind Energy (Onshore and Offshore), Hydropower (Small, Large, PSH), Bioenergy, Geothermal, Ocean Energy (Tidal and Wave)), by End-User (Utilities, Commercial and Industrial, Residential). For each segment, the installed capacity and forecasts have been calculated in GigaWatts (GW).

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

How large is the Japan renewable energy market in 2026?

Installed capacity reached 163.71 GW in 2026 and is on track for 197.08 GW by 2031.

Which technology shows the fastest growth?

Wind energy, driven by offshore projects, is forecast to expand at a 28.2% CAGR through 2031.

Why is curtailment a concern in Kyushu?

Solar output exceeded regional midday demand, leading to curtailment on 97 days and 1.2 TWh of wasted generation in 2024.

What role do agrivoltaics play?

More than 3,400 permitted projects converted 1,200 hectares of farmland, offering farmers new lease income while adding 1.2 GW of solar in 2024.

How does the 60% local-content rule affect offshore wind?

Developers must source most components domestically by 2028, extending financial close timelines but nurturing a local supply chain.

What is driving residential solar adoption?

Net-metering credits, falling module costs, and time-of-use tariffs have cut residential paybacks to 6-8 years, fueling 7.25% CAGR growth expected through 2031.

Page last updated on: