Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

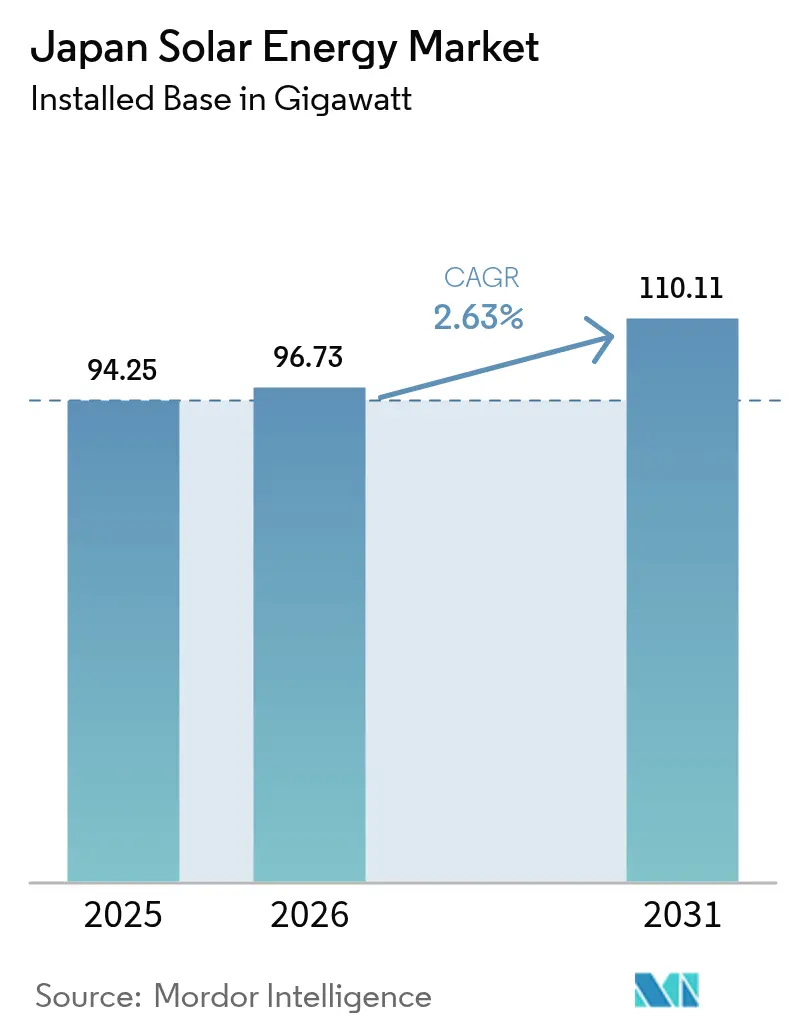

| Base Year Market Size (2025) | 94.25 gigawatt |

| Market Volume (2026) | 96.73 gigawatt |

| Market Volume (2031) | 110.11 gigawatt |

| Growth Rate (2026 - 2031) | 2.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Solar Energy Market Analysis by Mordor Intelligence

The Japan Solar Energy Market size was valued at 94.25 gigawatt in 2025 and estimated to grow from 96.73 gigawatt in 2026 to reach 110.11 gigawatt by 2031, at a CAGR of 2.63% during the forecast period (2026-2031).

Growth continues even after the shift from the Feed-in Tariff to the Feed-in Premium scheme, which encourages developers to follow wholesale price signals, integrated battery storage, and lower consumer levies.[1]Renewable Energy Institute, “Japan Renewable Curtailed Electricity,” renewableenergyinstitute.org Faster permitting for rooftop arrays, mandatory on-site generation rules in Tokyo, and falling module plus battery prices have enlarged the addressable base for distributed systems. Competitive pressure from overseas manufacturers decreases hardware costs, while domestic firms accelerate perovskite research, co-located storage, and energy-management software to retain value. Rising power demand from data centers and corporate decarbonization targets deepens the project finance pool through long-term power-purchase agreements.

Key Report Takeaways

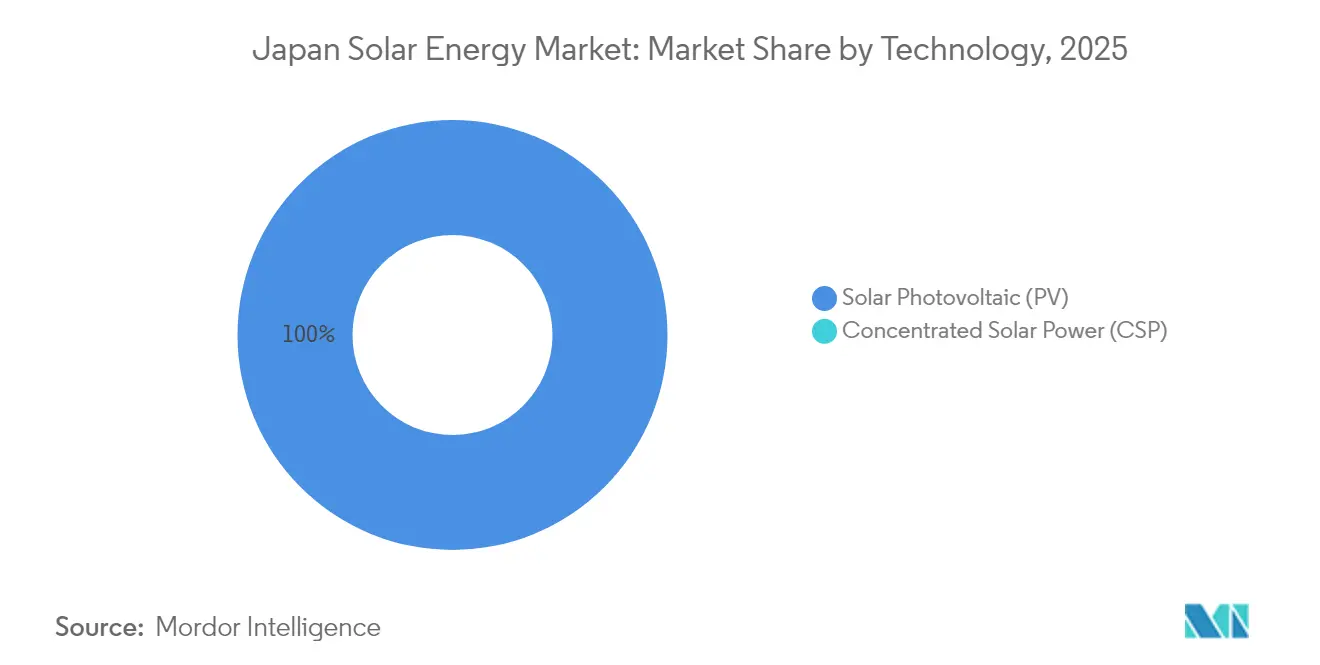

- By technology, solar photovoltaic maintained a 100.00% Japan solar energy market share in 2025 and is forecast to grow at a 2.63% CAGR through 2031.

- By grid type, on-grid assets held 96.35% of 2025 capacity, while off-grid systems are advancing at a 6.95% CAGR through 2031, the fastest among all segments.

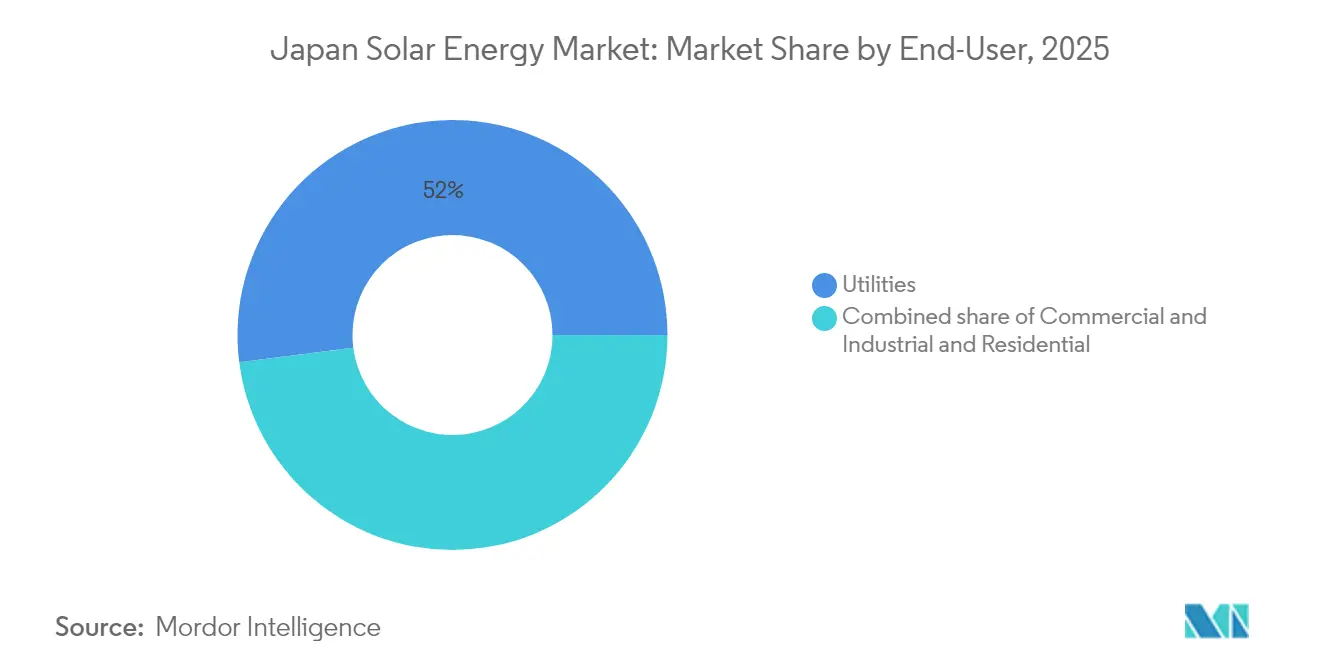

- By end-user, utility-scale projects accounted for 52.02% of installed capacity in 2025; residential rooftop arrays are the fastest-growing segment, with a 6.29% CAGR to 2031.

- By geography, Kyushu led installations, accounting for 22.74% of Japan's solar energy market share in 2025, but faces the highest curtailment risk. In contrast, Tohoku recorded the quickest grid-connection cycle, drawing 2.8 GW of new commitments in 2024.

- Among companies, Shizen Energy became the largest independent power producer after consolidating 758.4 MW of operating assets in March 2024

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Net-zero 2050 roadmap & FIT → FIP incentives | +0.8% | National, with higher FIP auction participation in Tohoku and Kyushu | Medium term (2-4 years) |

| Mandatory rooftop-PV building codes (Tokyo, Kanagawa) | +0.5% | Tokyo, Kanagawa prefectures; potential expansion to Osaka, Aichi | Short term (≤ 2 years) |

| Falling module + battery prices improve project IRRs | +0.6% | National, with strongest impact in utility-scale and C&I segments | Short term (≤ 2 years) |

| Data-center electricity surge spurring corporate PPAs | +0.4% | Greater Tokyo, Osaka metropolitan areas; emerging in Hokkaido | Medium term (2-4 years) |

| Lightweight perovskite PV opens façade & vehicle skins | +0.3% | National, early adoption in automotive (Toyota, Nissan partnerships) and commercial real estate | Long term (≥ 4 years) |

| "Zero-Yen Solar" subscription model unlocks households | +0.4% | Urban prefectures (Tokyo, Kanagawa, Saitama, Chiba); expanding to regional cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Net-zero 2050 roadmap & FIT → FIP incentives

The move from a guaranteed tariff to a premium above the wholesale price has realigned the Japanese solar energy market with standard power-market economics. By February 2024, the FIP program had accredited 1,036 projects, including 518 MW of solar, driving developers to pair modules with batteries to capture peak-price spreads.[2]Vector Renewables, “FIP Accredited Project Database,” vector-renewables.com Government notices released for fiscal 2025 confirm fresh budget lines for early-stage solar investments, signaling ongoing policy commitment. As developers invest in dispatchable capacity to hedge price risk, project structures now integrate forecasting software, virtual power-plant functions, and ancillary service revenues. These adaptations anchor the long-term competitiveness of the Japanese solar energy market while easing public-subsidy exposure.

Mandatory rooftop-PV building codes (Tokyo, Kanagawa)

Tokyo’s regulation that all new buildings above 2,000 m² must include solar panels from April 2025 has changed the baseline for urban construction. Compliance obligations rest with the builder, not the end-owner, simplifying logistics and placing a floor under annual installation volumes. The city’s parallel subsidy of up to JPY 80,000 per kW supports high-efficiency systems, further lifting return profiles. Early site inspection data indicate that builders now embed solar procurement into design workflows, normalizing on-site generation in the capital. Several prefectures are drafting similar ordinances, pointing toward a potential nationwide regulatory cascade that would underpin sustained demand in the Japanese solar energy market.

Falling module and battery prices improve project IRRs

Crystalline-silicon module oversupply has lowered end-user costs to 200,000-400,000 yen per kW, while lithium-iron-phosphate batteries follow a similar downward path. Canadian Solar’s 2024 launch of home batteries designed for the Japanese grid underscores how foreign manufacturers leverage scale to unlock additional cost reductions. As hardware becomes cheaper, integrated solar-plus-storage propositions thrive, allowing homeowners and small businesses to shave demand charges, sell surplus energy, and improve resilience. Economics has improved faster than the 3.35% CAGR headline, reinforcing widespread adoption across the Japanese solar energy market.

Data-center electricity surge spurring corporate PPAs

Digital-economy electricity growth pushes hyperscalers and manufacturers to secure renewable capacity through long-dated contracts. Google’s first 60 MW solar PPA in Japan and Apple’s supplier mandates show how multinational procurement standards are migrating into domestic industrial practice. PPA facilitators now offer one-year rolling contracts tailored to small and medium enterprises, broadening access beyond blue-chip clients. These offtake structures de-risk projects, attract cheaper debt, and build an additional pillar under demand in the Japanese solar energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion & curtailment in Kyushu/Hokkaido | -0.6% | Kyushu, Hokkaido; spillover risk to Tohoku if transmission upgrades delayed | Short term (≤ 2 years) |

| Scarce land / strict zoning for ground-mount projects | -0.5% | National, acute in Kanto, Kansai plains; less severe in Tohoku, Hokkaido | Medium term (2-4 years) |

| PV waste-management liability & recycling cost spike | -0.3% | National, with early impact on projects reaching 20-year end-of-life from 2032 onward | Long term (≥ 4 years) |

| Skilled-labour gap for HV solar-plus-storage installs | -0.4% | National, most acute in rural prefectures with aging electrician workforce | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid congestion & curtailment in Kyushu/Hokkaido

Curtailment jumped to 1.76 TWh in fiscal 2023, with Kyushu hitting a 6.7% rate because limited inter-regional links and inflexible baseload reactors leave little room for midday solar peaks. Utilities are piloting AI-based voltage control that has cut stabilizer activations by up to 70%, showing a technical path forward. Policymakers also draft negative-pricing rules and economic dispatch, but timelines remain unsettled. Until infrastructure aligns, Japanese solar energy market developers must add batteries, reposition plants, or accept revenue cannibalization during oversupply events.

Skilled-labour gap for HV solar-plus-storage installs

Construction-sector employment fell 20% over the past decade, contributing to 350 bankruptcies in 2024, with one-third in construction.[3]PR TIMES, “Construction Industry Bankruptcy Report,” prtimes.jp High-voltage solar-plus-storage projects need licensed electricians familiar with grid protection, but the aging workforce and new overtime caps limit supply. The government plans to double foreign skilled-worker quotas to address structural shortages, yet requires retraining and cultural integration. Therefore, firms in the Japanese solar energy market invest in modular equipment, factory-assembled racks, and augmented-reality guidance to lower onsite labor intensity and shorten commissioning schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Dominance Confirms CSP Non-Viability

Japan's solar energy market size for photovoltaic technology stood at 94.25 GW in 2025, locking in a 2.63% CAGR toward 2031 and retaining a 100.00% segment share as concentrated solar power (CSP) remains commercially absent. Mono-crystalline PERC modules averaged 21.5% efficiency and continued to displace poly-silicon panels across utility and commercial projects. Heterojunction and back-contact cells, though premium-priced, gained mindshare in residential retrofits where roof space is scarce, and efficiency premiums justify higher costs.

Perovskite tandem cells sit on the innovation frontier, with a consortium targeting 20 GW of domestic line capacity by 2040 to reclaim manufacturing competitiveness. Pilot efficiencies of 15.6% and a 60% weight reduction expand viable mounting surfaces to façades and vehicular skins. Commercial uptake hinges on humidity resilience; accelerated aging tests show 15% faster degradation than silicon under coastal conditions, prompting encapsulation R&D. Domestic manufacturers view the technology as a path to recoup value lost to overseas c-Si imports, which captured 68% of the 2024 module inflow.

By Grid Type: Off-Grid Resilience Accelerates but On-Grid Dominates

On-grid systems represented 96.35% of the capacity in 2025, underpinned by feed-in premiums and wholesale market access. However, off-grid installations are forecast to grow at a 6.95% CAGR through 2031, the fastest among all grid types, and a key beneficiary of disaster-resilience mandates, as earthquake and typhoon disruptions have exposed centralized-grid vulnerabilities.

Municipalities, such as Ishikawa, installed 42 MW of standalone microgrids at evacuation centers in 2024, thereby reducing the risk of outages for critical services. Remote islands in Okinawa and Kagoshima have replaced diesel generators with hybrid solar-battery systems. Yonaguni’s 1.2 MW array has cut fuel imports by 680 kiloliters per year, illustrating the economic crossover point for fossil-fuel displacement. Nevertheless, grid-connected plants remain the workhorse for capacity additions, benefiting from economies of scale and merchant revenue streams from the Japan Electric Power Exchange. Rising curtailment risk is nudging on-grid developers toward hybrid designs able to island during negative-price events, blurring traditional segment lines.

By End-User: Residential Rooftops Outpace Utility-Scale Megawatts

Utility-scale projects accounted for 52.02% of Japan's solar energy market size in 2025, but they face land scarcity and a 36-month average grid-access queue in congested regions. Residential arrays are projected to advance at a 6.29% CAGR through 2031, driven by zero-yen solar contracts and rooftop codes covering buildings exceeding 2,000 m². Subscription installers shoulder capex and monetize renewable-energy certificates, enabling households to lock in electricity bills below retail tariffs and meet municipal decarbonization goals.

Commercial and industrial buyers turn to long-term PPAs to mitigate wholesale-price volatility; Microsoft's 50 MW agreement with Shizen Energy exemplifies how investment-grade off-takers unlock financing for merchant projects. Agrivoltaic projects offer supplemental farm income but carry 30% lower panel density, pushing levelized costs above JPY 14 kWh and limiting uptake to cooperatives with diversification mandates. Floating solar arrays on reservoirs and industrial ponds are emerging as a niche utility-scale avenue where grid access is available, yet land is constrained.

Geography Analysis

Tokyo and neighboring prefectures form the single largest node in the Japanese solar energy market, driven by stringent decarbonization targets, premium electricity prices, and policy mandates that require on-site generation in new construction. The metropolitan government’s 7.1 billion-yen subsidy pool further lowers household installation hurdles. Dense load centers and established distribution networks also mean minimal transmission loss and near-real-time self-consumption, improving project economics.

Kyushu boasts excellent solar irradiation yet grapples with the nation’s highest curtailment rate at 6.7%, causing developers to incorporate battery systems, pursue hybrid projects, or stagger new builds until planned interconnections materialize. Hokkaido offers expansive land for utility-scale farms and hosts Japan’s first 30 MW corporate PPA dedicated to a data-center operator, but limited southbound grid capacity caps export volumes. Chubu and Kansai regions provide balanced opportunity sets: industrial demand supports corporate PPAs, and grid-modernization pilots such as AI-enabled voltage control illustrate how congestion risks can be mitigated.

Across 36 prefectures, 73 “advanced decarbonization areas” link renewables, agriculture, and community revitalization in tailored local energy plans. Coastal districts replicate floating-solar prototypes to take advantage of reservoirs and port basins, while rural prefectures adopt agrivoltaic frameworks to preserve farmland yields. These region-specific pathways reinforce the breadth and resilience of growth in the Japanese solar energy market.

Competitive Landscape

The Japanese solar energy market hosts a blend of domestic incumbents and cost-driven global entrants. Sharp, Kyocera, and Panasonic Energy concentrate on premium segments and maintain strong after-sales networks, preserving core customer loyalty. LONGi, Trina Solar, and JinkoSolar penetrate price-sensitive tiers with larger power formats and aggressive discounting. This dual structure sustains downward price pressure while stimulating domestic R&D, such as Sekisui Chemical’s perovskite roadmap targeting mass production by 2027.

The strategic investment underscores competitive repositioning. Mitsubishi Electric will spend USD 500 million to secure silicon-carbide supplies, safeguarding high-voltage module leadership for solar and storage inverters.[4]Energy Global, “Mitsubishi Electric Secures SiC Supply Chain,” energyglobal.com ENECHANGE, West Holdings, and many energy-tech startups deploy bundled financing, installation, and monitoring packages that lock in service revenues beyond initial hardware sales. Partnerships pair complementary strengths: Kyocera works with SolarEdge on optimizers and SafeDC technology, while Sungrow cooperates with local developers on 500 MWh battery projects that reinforce grid flexibility.

Market players increasingly use integrated solutions. Inverters, batteries, software, and asset-management services converge under single brands, raising customer switching costs and opening higher-margin recurring revenue streams. Japanese firms leverage trusted domestic brands and grid-code familiarity, whereas international suppliers import scale economies. This interplay shapes a competitive equilibrium that remains intense yet technologically progressive within the Japanese solar energy market.

Japan Solar Energy Industry Leaders

Sharp Corporation

Kyocera Corporation

Panasonic Energy Co.

Canadian Solar Inc.

Trina Solar Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Equinix signed a 30 MW, 20-year PPA with Trina Solar Japan Energy for a Hokkaido project commencing in 2028.

- February 2025: Sungrow and Sun Village announced the deployment of a 500 MWh battery storage system tied to solar projects.

- December 2024: Sekisui Chemical confirmed mass-production plans for perovskite solar cells by 2027.

- June 2024: Obton and GSSG Solar acquired a 117 MW Japanese solar portfolio, reaffirming foreign investor appetite.

Japan Solar Energy Market Report Scope

Solar energy is the conversion of energy present in the sun and is one of the renewable energies. Once the sunlight passes through the Earth's atmosphere, most of it is visible light and infrared radiation. Solar cell panels are used to convert this energy into electricity. For each segment, the market sizing and forecasts have been done based on installed capacity (GW).

The Japan solar energy market report includes:

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How large is Japan’s solar fleet in 2026 and where is it heading?

Japan operates 96.73 GW in 2026 and is on track for 110.11 GW by 2031, reflecting a 2.63% CAGR over 2026-2031.

Which region faces the highest curtailment risk?

Kyushu records the most curtailment, with 223 days of forced output reduction in 2024 due to grid congestion.

What drives residential rooftop growth after 2026?

Zero-yen solar subscriptions and mandatory rooftop codes in Tokyo and Kanagawa propel residential arrays at a 6.29% CAGR.

How are data centers influencing solar build-outs?

Hyperscale operators in Tokyo, Osaka, and Hokkaido sign multi-MW PPAs, creating long-tenor demand for merchant solar projects.

What technology could reshape module manufacturing in Japan?

Lightweight perovskite tandem cells, targeted for 20 GW of domestic capacity by 2040, aim to reclaim manufacturing share.

How strict are Japan’s recycling rules for PV panels?

Projects commissioned after 2022 must post decommissioning bonds and meet recycling quotas, adding roughly USD 0.03 W to capex.

Page last updated on: