Japan Vehicle Emission Standards And Impact Analysis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

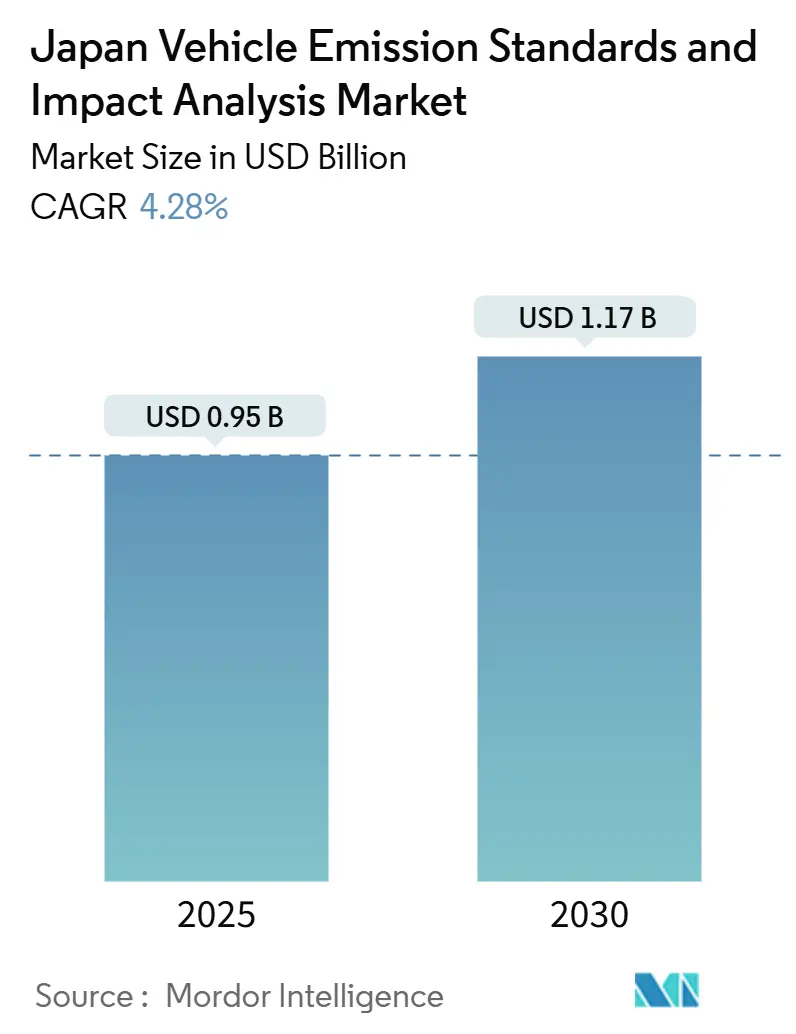

| Market Size (2025) | USD 0.95 Billion |

| Market Size (2030) | USD 1.17 Billion |

| Growth Rate (2025 - 2030) | 4.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Vehicle Emission Standards And Impact Analysis Market Analysis by Mordor Intelligence

The Japan vehicle emission standards and impact analysis market size is valued at USD 0.95 billion in 2025 and is forecast to reach USD 1.17 billion by 2030, expanding at a 4.28% CAGR. Growth is driven by stricter post-New-Long-Term (PNLT) limits for heavy-duty vehicles, a 2035 target for 100% zero-emission light vehicles, and rising demand for Real Driving Emissions (RDE) and Portable Emissions Measurement Systems (PEMS) testing. Investments in next-generation benches, remote on-board diagnostic (OBD) monitoring, and monetization of fleet-level CO₂ data are expanding service portfolios even as flat domestic vehicle sales temper volume growth. Established equipment makers leverage proprietary analyzers while independent laboratories scale specialized field capabilities. Opportunities are concentrated in urban prefectures where low-emission zones accelerate compliance cycles and where EV charging build-out intensifies battery performance validation needs.

Key Report Takeaways

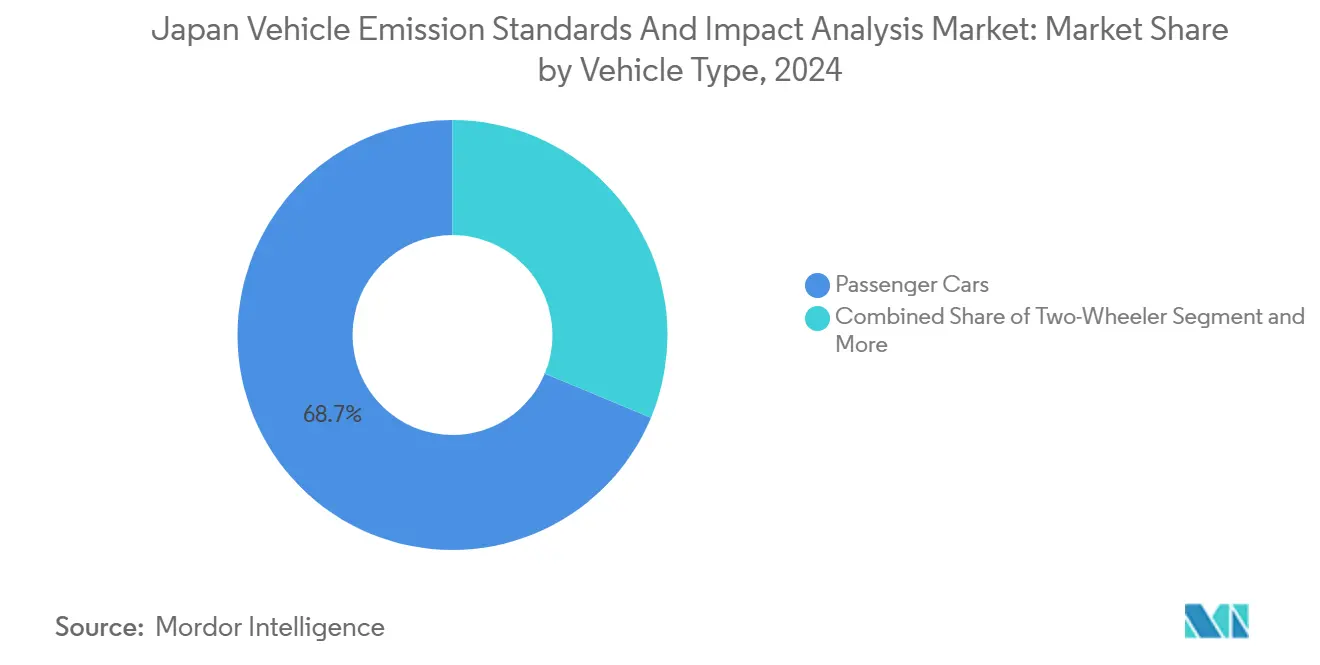

- By vehicle type, passenger cars led with 68.72% of Japan vehicle emission standards and impact analysis market share in 2024; the segment is also advancing at a 7.29% CAGR to 2030.

- By propulsion type, internal combustion engine vehicles held 87.47% share of the Japan vehicle emission standards and impact analysis market size in 2024, while battery electric vehicles record the fastest projected CAGR at 7.28% through 2030.

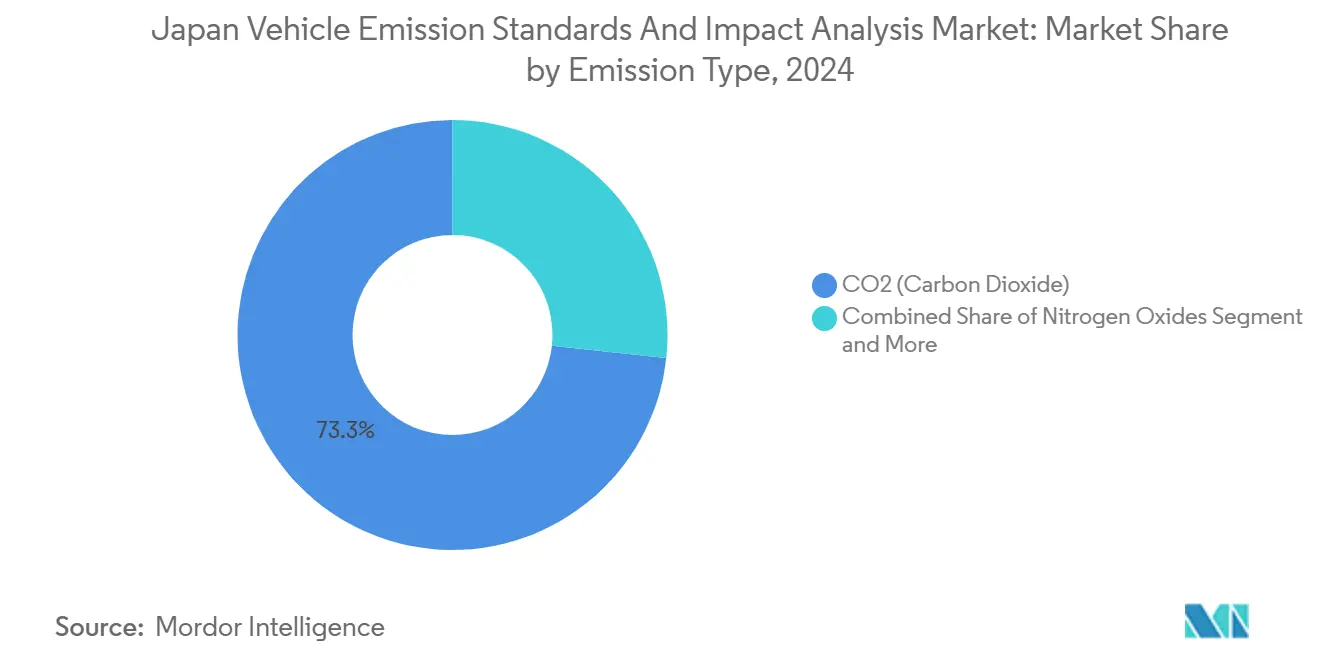

- By emission type, CO₂ testing commanded 73.29% share of the Japan vehicle emission standards and impact analysis market size in 2024, yet NOx testing is set to expand at an 8.35% CAGR between 2025-2030.

- By end-user, OEMs accounted for 54.37% share of the Japan vehicle emission standards and impact analysis market size in 2024, whereas independent laboratories are growing quickest at an 8.63% CAGR to 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Japan representing one among them. The global report on vehicle emission standards and impact analysis market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Japan Vehicle Emission Standards And Impact Analysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening 2030 PNLT Limits for HDVs | +1.2% | Kanto and Chubu regions | Medium term (2-4 years) |

| 2035 100% ZEV Target for Light Vehicles | +0.9% | Tokyo, Osaka, Nagoya metros | Long term (≥ 4 years) |

| Adoption of RDE and PEMS Testing | +0.8% | Nationwide pilot prefectures | Short term (≤ 2 years) |

| Prefecture Low-Emission Zones | +0.5% | Tokyo, Osaka, Kyoto, others | Medium term (2-4 years) |

| Remote OBD and Telematics Compliance | +0.4% | Urban corridors | Short term (≤ 2 years) |

| Fleet CO₂ Data Monetization | +0.3% | Corporate hubs in Kanto | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening 2030 Post-New-Long-Term Limits for Heavy-Duty Vehicles

Japan’s forthcoming PNLT standards require expanded NOx and particulate testing under real-world cycles, pushing per-model compliance budgets. Commercial OEMs clustered in Kanto and Chubu have scaled R&D benches and adopted HORIBA MEXA analyzers to meet the heavier test load. Laboratories benefit from repeat validation programs that stretch through 2030 alongside national goals to cut transport greenhouse gases 46% from 2013 levels[1]“Roadmap to 46% Reduction by 2030,”, Ministry of the Environment Japan, env.go.jp. Sustained demand for integrated chassis dynamos and high-flow PEMS units is reshaping capital plans for both private and public test centers.

2035 100% Zero-Emission Vehicle Target for Light-Duty Vehicles

The switch to full zero-emission light vehicles adds new layers of battery efficiency, hydrogen stack durability, and life-cycle carbon validation[2]“Green Growth Strategy 2025,”, Ministry of Economy Trade and Industry, meti.go.jp. Electric-specific benches cost approximately USD 2-3 million each, prompting joint ventures between equipment makers and labs to amortize the spend. Early adopter prefectures prioritize charging corridors, making urban labs the first to install high-power DC cycling rigs. Major OEMs such as Toyota align internal targets with the national 2035 milestone, integrating mixed-fleet validation of hybrids, BEVs, and fuel-cell models.

Adoption of Real-Driving-Emissions and PEMS Testing

Japan's requirement that new type approvals pass RDE cycles under UN ECE protocols by 2026 has shifted testing from controlled cells to on-road measurement. PEMS kits will deliver continuous CO, CO₂, NOx, and PM data across urban and expressway routes, demanding new technician skill sets. Service providers with mobile teams gain an edge, and HORIBA's established track record in emissions testing helps it secure public contracts. Field enforcement is already increasing in pilot prefectures.

Prefecture-Level Low-Emission Zones Pilot Programs

Local ordinances in Tokyo, Osaka, and Kyoto impose standards stricter than national rules, fragmenting compliance schedules. Vehicles require dual certification, national and local, thereby raising test frequency and boosting independent lab workloads. Tokyo alone drives higher repeat tests, and similar zones are under study in Saitama and Aichi. The decentralized model accelerates demand hot spots that larger national centers cannot always serve, opening room for niche providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flat Domestic Vehicle Sales | -0.7% | Rural regions | Long term (≥ 4 years) |

| High Capex for Next-Gen Benches | -0.5% | Nationwide | Medium term (2-4 years) |

| Technician Shortage | -0.4% | Kyushu and Tohoku | Medium term (2-4 years) |

| Telematics Data-Privacy Costs | -0.2% | Corporate-dense Kanto | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Flat Domestic Vehicle Sales Volume Growth

Annual registrations remain trapped, limiting fresh model certifications[3]“2024 New Vehicle Registration Facts,”, Japan Automobile Dealers Association, jada.or.jp. With fewer new launches, OEMs stretch product cycles, compressing traditional lab revenues. Rural prefectures suffer most as aging populations migrate to urban areas, cutting personal car demand and, by extension, periodic inspection volumes. Labs diversify into retrofit testing, yet these services only partially offset the lost pipeline of new-model validations.

High Capital Expenditure for Next-Generation Emission Test Benches

Advanced benches combining RDE simulation, PEMS correlation, and EV powertrain cycling require USD 2-5 million upfront and annual maintenance. Smaller independents face financing gaps that encourage sector consolidation. Equipment lifespans of seven to 10 years force continuous reinvestment, raising barriers for new entrants. HORIBA’s 2025 Kyoto Vehicle Test Cell illustrates the scale, featuring climate-controlled chambers and electromagnetic shielding that few rivals can match

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Drive Market Expansion

Passenger cars captured 68.72% of the Japan vehicle emission standards and impact analysis market in 2024 and are forecast to post a 7.29% CAGR through 2030, reflecting the high complexity of hybrid and battery electric validations. This segment fuels the demand for RDE, energy-consumption, and battery degradation tests. SUVs and multi-utility vehicles further amplify workloads because of larger battery packs and diverse duty cycles. Sedans and hatchbacks show lower growth but remain steady revenue anchors.

Commercial vehicles contribute sustained heavy-duty dynamometer hours as the 2030 PNLT standards tighten. Two-wheelers and three-wheelers form a niche, governed by dedicated emission norms that necessitate miniature bench setups but yield lower absolute revenues. The spread of mandatory OBD inspections since October 2024 pushes continuous monitoring services for fleets, adding another layer of post-market engagements in the Japan vehicle emission standards and impact analysis market.

By Propulsion Type: ICE Dominance Amid Electric Transition

Internal combustion engine vehicles still own 87.47% of the market share in 2024, ensuring steady demand for tailpipe and evaporative testing. Hybrid powertrains create dual-path workloads, requiring simultaneous combustion and electric performance checks. Although battery electric vehicles remain small in volume, their 7.28% CAGR to 2030 positions them as the fastest-expanding propulsion class.

BEV testing focuses on JC08 and WLTC cycles for energy consumption, regenerative braking, and thermal stability, demanding high-capacity powertrain dynos costing USD 2-3 million. Government purchase incentives of up to JPY 850,000 (USD 6,100) and a plan for 300,000 public chargers by 2030 underpin rapid lab upgrades. As a result, the Japanese vehicle emission standards and impact analysis market size tied to EV validation is set for outsized growth relative to its current baseline.

By Emission Type: CO₂ Testing Leads, NOx Growth Accelerates

CO₂ (Carbon Dioxide) compliance accounted for 73.29% of testing revenues in 2024 as life-cycle greenhouse-gas assessments became mainstream. Labs run extended drive cycles and fuel-upstream simulations to generate corporate ESG metrics. Particulate matter and hydrocarbon checks remain core for diesel and gasoline models, with steady if slower expansion.

NOₓ (Nitrogen Oxides) testing is the breakout category, projected to rise at an 8.35% CAGR through 2030, fueled by heightened RDE enforcement. Portable analyzers now follow vehicles on urban and alpine routes to catch spikes beyond lab settings. Comprehensive pollutant coverage increases operational complexity yet enables integrated providers to bundle multi-gas packages and deepen footprints within the Japan vehicle emission standards and impact analysis market.

By End-Users: OEMs Lead, Independent Labs Surge

OEM in-house centers retained 54.37% revenue share in 2024, reflecting their obligation for type approval and development tests. However, independent laboratories are growing at 8.63% CAGR as regulations diversify. They win contracts for specialty RDE, fuel-cell stack, and telematics compliance work that internal teams find uneconomical.

Government agencies broadened surveillance programs after the Volkswagen scandal, commissioning market surveillance retests and defeat device hunts. Fleet operators increasingly contract CO₂ data analytics to monetize emission credits, widening the client mix. The mix shift supports capacity expansions among global networks such as SGS and Intertek, which integrate equipment sourcing, regulatory consulting, and certification within the Japan vehicle emission standards and impact analysis industry.

Geography Analysis

Kanto hosts a significant part of the national test demand due to Tokyo’s density of vehicles, regulators, and OEM R&D centers. Local ordinances mandate stricter limits than federal rules, pushing test frequencies 25% higher. The region’s cluster of HORIBA, Shimadzu, and global inspection firms creates an innovation loop that feeds rapid equipment refresh cycles within the Japanese vehicle emission standards and impact analysis market.

Chubu, anchored by Nagoya, is rapidly emerging in the market. Toyota's diverse electrification strategy fuels year-round prototype validations. Continuous cell occupancy, essential for high-volume production, incentivizes labs to adopt flexible shift operations. Facilities adept at concurrently handling ICE and BEV productions boast utilization rates exceeding 90%, bolstering margin growth.

Kansai holds a significant share, buoyed by mixed commercial truck and motorcycle production lines. Low-emission zones in Osaka add localized compliance layers, though financial outlays remain more moderate than in Tokyo. Lower vehicle density shifts opportunity toward mobile PEMS teams and cloud OBD solutions that minimize travel time yet retain regulatory fidelity across the Japanese vehicle emission standards and impact analysis market.

Mordor Intelligence provides coverage of the vehicle emission standards and impact analysis market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to China incorporating local coverage and market participation, as required.

Competitive Landscape

The market is moderately concentrated. HORIBA commands a significant share of global emissions-equipment sales and pairs hardware dominance with contract testing, giving it pricing leverage. Shimadzu pursues similar vertical integration, while SGS Japan and Intertek compete on multi-region expertise. Mandatory OBD inspections in October 2024 spurred scan-tool sales and technician-training programs, broadening revenue pools.

Technology leadership hinges on RDE and EV energy-consumption capabilities. HORIBA’s 2025 Kyoto Vehicle Test Cell integrates high-flow PEMS calibration bays, battery cyclers, and climate-stress chambers in one footprint, raising competitive thresholds. Smaller independents respond by specializing in remote OBD analytics or regional low-emission zone compliance to avoid head-to-head capital races.

Partnerships proliferate: equipment makers align with labs to co-fund benches, while telematics vendors team with fleet managers to monetize CO₂ credits. The race to integrate analytics, certification, and ESG reporting is redefining service bundles within the Japan vehicle emission standards and impact analysis industry. As capital outlays climb, consolidation remains likely, with cash-rich incumbents acquiring niche RDE specialists to round out offerings.

Japan Vehicle Emission Standards And Impact Analysis Industry Leaders

HORIBA Ltd.

Shimadzu Corporation

SGS Japan Inc.

Intertek Group plc

Applus+ IDIADA Japan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: HORIBA Techno Service opened a Kyoto Vehicle Test Cell with integrated Internal Combustion Engine (ICE) and Electric Vehicle (EV) systems.

- April 2025: Asuene added GX League reporting to its CO₂ visualization cloud, covering 747 firms. Asuene's platform, designed for companies to measure, report, and mitigate their greenhouse gas emissions, has recently integrated features to align with the GX League's reporting mandates.

Japan Vehicle Emission Standards And Impact Analysis Market Report Scope

| Two-Wheeler | |

| Three-Wheeler | |

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUV & MUVs | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles | |

| Buses & Coaches |

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| CO₂ (Carbon Dioxide) |

| NOₓ (Nitrogen Oxides) |

| PM (Particulate Matter) |

| HC (Hydrocarbons) |

| Others (CO, SO₂, etc.) |

| Government Regulating Agencies |

| OEMs |

| Independent Testing Labs |

| By Vehicle Type (Value) | Two-Wheeler | |

| Three-Wheeler | ||

| Passenger Cars | Hatchbacks | |

| Sedans | ||

| SUV & MUVs | ||

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium & Heavy Commercial Vehicles | ||

| Buses & Coaches | ||

| By Propulsion Type (Value) | Internal-Combustion Engine Vehicles | |

| Hybrid Electric Vehicles | ||

| Battery Electric Vehicles | ||

| By Emission Type (Value) | CO₂ (Carbon Dioxide) | |

| NOₓ (Nitrogen Oxides) | ||

| PM (Particulate Matter) | ||

| HC (Hydrocarbons) | ||

| Others (CO, SO₂, etc.) | ||

| By End-Users (Value) | Government Regulating Agencies | |

| OEMs | ||

| Independent Testing Labs | ||

Key Questions Answered in the Report

What is the current value of the Japan vehicle emission standards and impact analysis market?

The market is valued at USD 0.95 billion in 2025 and is projected to reach USD 1.17 billion by 2030.

How fast is the market expected to grow?

It is forecast to expand at a 4.28% CAGR between 2025 and 2030.

Which vehicle type generates the highest testing demand?

Passenger cars contribute 68.72% of 2024 revenues and remain the fastest-growing segment at a 7.29% CAGR.

Why is NOx testing gaining importance in Japan?

Stricter PNLT standards and nationwide adoption of Real Driving Emissions testing are lifting NOx workloads at an 8.35% CAGR through 2030.

How are independent laboratories positioned in this market?

They are the fastest-growing end-user group, expanding at an 8.63% CAGR as OEMs outsource specialized RDE and EV energy-consumption validations.

Page last updated on: