Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Japan Surveillance IP Camera Market is Segmented by Camera Type (Dome, Bullet, and More), Resolution (≤2 MP HD, 3-5 MP Full-HD+, and More), Connectivity and Power (Wired (PoE), Wireless (Wi-Fi, 5G/LTE), and More), Deployment Architecture (Centralized, Decentralized / Edge-AI), End-User Vertical (Government and Defense, Transportation and Infrastructure, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

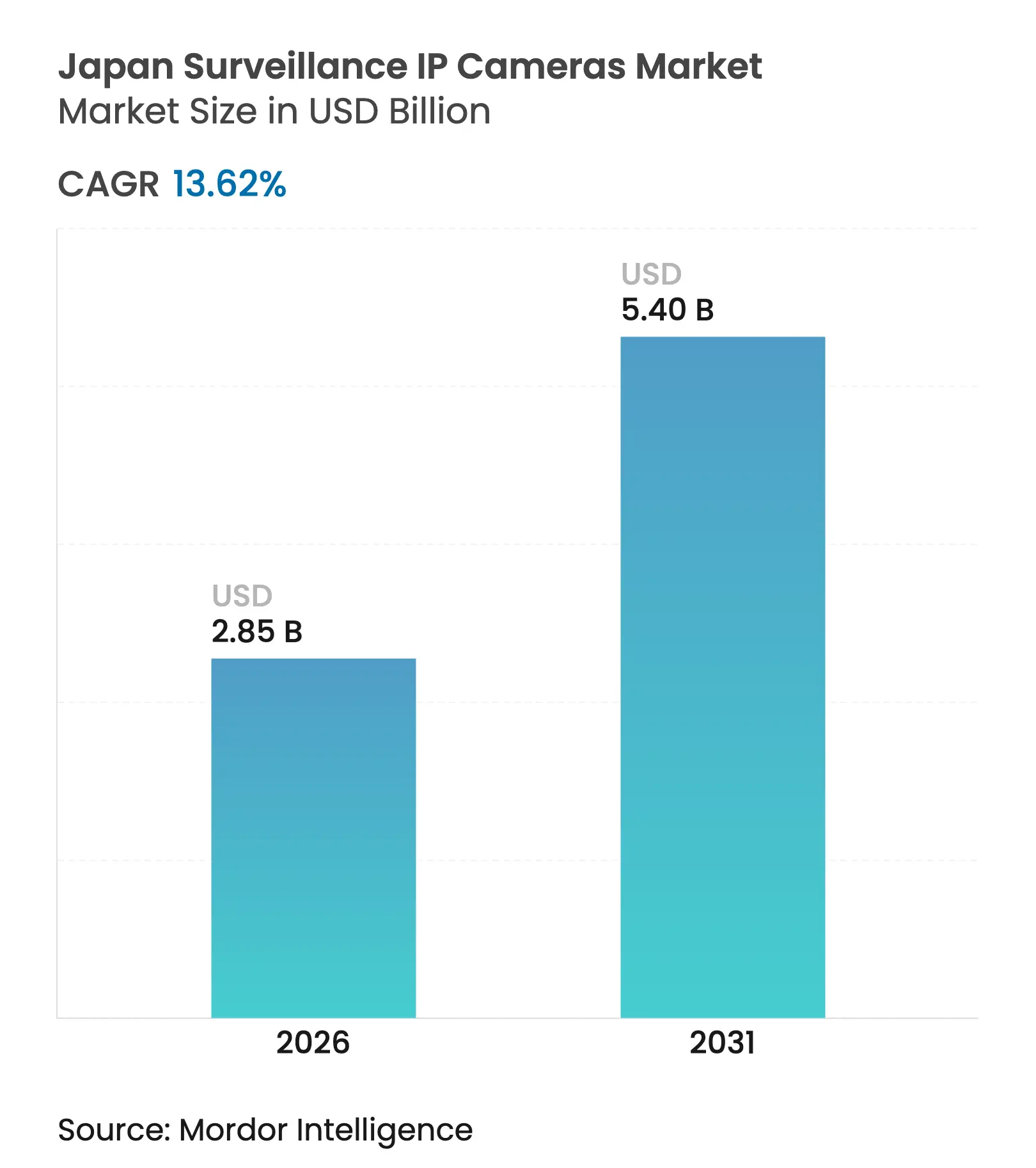

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 5.4 Billion |

| Growth Rate (2026 - 2031) | 13.62 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Japan surveillance IP cameras market size in 2026 is estimated at USD 2.85 billion, growing from 2025 value of USD 2.51 billion with 2031 projections showing USD 5.4 billion, growing at 13.62% CAGR over 2026-2031. Rising public-safety investments, private-sector digital transformation, and nationwide 5G coverage are catalyzing demand for high-resolution, AI-enabled cameras. The market benefits from Japan’s semiconductor leadership, which is lifting sensor performance in low-light environments, while strict data-sovereignty rules are accelerating a pivot from NVR-centric to edge-AI architectures. Labor shortages in policing and facility management are increasing reliance on PTZ and autonomous analytics to maintain security standards without adding headcount. Wireless deployments are expanding rapidly as private 5G and Wi-Fi 6 lower installation barriers for factories, transport hubs, and rural elder-care facilities.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government "Kōban" & Safe-City Upgrade Programs Accelerating Public-Space IP Surveillance Adoption Government "Kōban" & Safe-City Upgrade Programs Accelerating Public-Space IP Surveillance Adoption | +3.5% | National, with concentration in urban centers | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+3.5% | Geographic Relevance:National, with concentration in urban centers | Impact Timeline:Medium term (2-4 years) |

Intensifying Demand for 4K / 8MP Cameras in Rail & Metro Stations Intensifying Demand for 4K / 8MP Cameras in Rail & Metro Stations | +2.7% | Major metropolitan areas (Tokyo, Osaka, Nagoya) | Short term (≤ 2 years) | |||

Rapid Roll-out of Private 5G / Wi-Fi 6 in Smart Factories Enabling Wireless IP Cameras Rapid Roll-out of Private 5G / Wi-Fi 6 in Smart Factories Enabling Wireless IP Cameras | +2.1% | Industrial zones nationwide | Medium term (2-4 years) | |||

Shift from NVR to Edge-AI Cameras to Meet Japan's Strict Data-Sovereignty Mandates Shift from NVR to Edge-AI Cameras to Meet Japan's Strict Data-Sovereignty Mandates | +1.9% | National | Medium term (2-4 years) | |||

Aging Population Driving Remote-Monitoring Cameras in Elder-Care Facilities Aging Population Driving Remote-Monitoring Cameras in Elder-Care Facilities | +1.8% | National, with higher concentration in rural areas | Long term (≥ 4 years) | |||

Surge in SME Cloud-based VSaaS Adoption Backed by Digital Transformation Subsidies Surge in SME Cloud-based VSaaS Adoption Backed by Digital Transformation Subsidies | +1.8% | National | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Government “Kōban” modernization programs

Nationwide upgrades to Japan’s neighborhood police boxes integrate AI-enabled IP cameras that support real-time video analytics and community engagement, reinforcing public trust while boosting situational awareness. The projects standardize hardware across municipalities, simplifying maintenance and lowering lifecycle costs. Camera deployments inside and around Kōban facilities funnel video to regional command centers, enabling rapid incident response and officer safety. Vendors highlighting robust cybersecurity and domestic supply chains gain preference due to public-sector procurement guidelines. The program is estimated to account for roughly one-quarter of total market growth through 2030.

4K/8 MP demand in rail & metro stations

Railway operators are accelerating 4K camera retrofits as part of a government mandate requiring video coverage on all new rolling stock. Fukuoka’s new 4000-series subway trains exemplify the trend, each integrating four high-resolution units for remote monitoring and analytics.[1]Mainichi. "In Japan, Subway 1st, Security Cameras to be introduced in New Train.", mainichi.jp/High pixel density supports facial recognition ticketing pilots and passenger-flow optimization, while edge processing minimizes bandwidth overhead. The upcoming Osaka/Kansai Expo 2025 further boosts capital spending on transportation security.

Private 5G & Wi-Fi 6 rollout in smart factories

Japan has issued more than 2,700 private 5G licenses, enabling manufacturers to deploy ultra-reliable wireless backbones that power high-bandwidth video analytics.[2]Verizon, “Private 5G Country Spotlight,” verizon.comPilot plants operated by SoftBank and Sumitomo Electric achieved 100% detection rates of worker movements via AI analysis of 4K streams. Wi-Fi 6 and emerging Wi-Fi HaLow solutions extend coverage to hard-to-wire areas, reducing cabling costs in legacy facilities and supporting mobile robots equipped with PTZ cameras.

Shift to edge-AI cameras for data-sovereignty compliance

Revisions to the Act on the Protection of Personal Information (APPI) tighten rules governing biometric data, prompting enterprises to process video on-camera to avoid transferring raw imagery offsite.[3]Kazuhide Ishiwaka, “Japan’s Personal Information Protection Legal Framework,” wto.org Edge-AI architectures lower latency and bandwidth, while satisfying regulatory audits that prioritize local data residency. METI’s 2024 budget earmarks significant funds for generative AI development, spurring vendors to embed advanced analytics directly into lenses and chipsets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Strong Personal-Data Protection Act (APPI) Limiting Facial-Recognition Deployments Strong Personal-Data Protection Act (APPI) Limiting Facial-Recognition Deployments | -0.9% | National | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.9% | Geographic Relevance:National | Impact Timeline:Medium term (2-4 years) |

High Premium on Domestic-Brand Cameras Elevates TCO vs. Imports High Premium on Domestic-Brand Cameras Elevates TCO vs. Imports | -1.2% | National | Long term (≥ 4 years) | |||

Fragmented Building Infrastructure Hindering PoE Retrofits in Rural Areas Fragmented Building Infrastructure Hindering PoE Retrofits in Rural Areas | -0.8% | Rural areas and older urban districts | Long term (≥ 4 years) | |||

Semiconductor Supply-Chain Volatility Affecting 4K Sensor Availability Semiconductor Supply-Chain Volatility Affecting 4K Sensor Availability | -1.1% | Global impact with national implications | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Strong APPI limits on facial-recognition deployments

The Personal Information Protection Commission is considering 2025 amendments that would add criminal penalties for misuse of biometric data, forcing operators to adopt risk-based deployment models. Transportation firms testing walk-through gates in the Osaka Metro must demonstrate algorithmic fairness, data minimization, and opt-out mechanisms. These requirements elongate procurement cycles and raise compliance costs, slowing the uptake of analytics-heavy solutions.

Premium pricing of domestic brands elevates TCO

Panasonic i-PRO and Sony command premium price points on the strength of quality control and after-sales support, but SMEs—constituting 99.7% of Japanese enterprises—often lack budgets for large-scale rollouts.[4]Marco Bianchini & Marta Lasheras Sancho, “SME Digitalisation for Competitiveness,” oecd.org While government subsidies exist, low awareness curbs uptake. The cost gap is driving interest in subscription-based VSaaS offerings that shift capital expense to operating expense, though such services must still satisfy data-sovereignty rules.

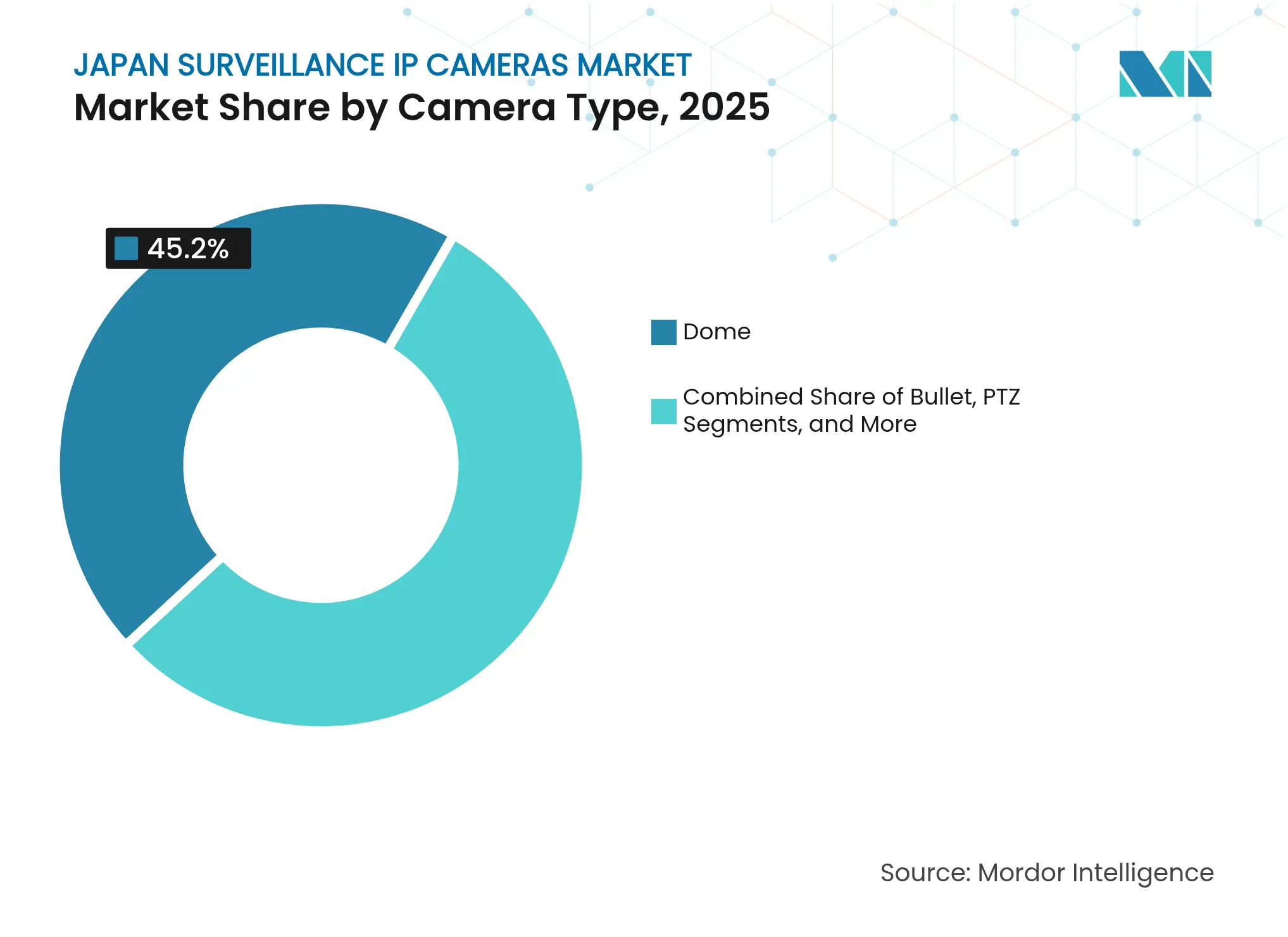

By Camera Type: PTZ Growth Outpaces Dome Leadership

Dome units retained a 45.20% share of the Japan surveillance IP cameras market in 2025, buoyed by vandal-resistant housings and a form factor that blends into public environments. PTZ models, aided by remote-control zoom and tilt, are forecast to expand at a 14.32% CAGR, giving operators labor-saving coverage in large-area sites such as logistics parks.

Sony’s IMX585 4K sensor—with eight-fold dynamic-range improvement—enhances both dome and PTZ performance in back-lit situations. Bullet and box cameras serve perimeter security niches, while covert units support ATM and elder-care observation where discretion is critical. Continuous innovation in AI-enabled corner cameras underscores domestic vendors’ focus on specialty use cases.

Note: Segment shares of all individual segments available upon report purchase

By Resolution: UHD Cameras Accelerate Detail-Driven Adoption

Full-HD+ (3–5 MP) models led in 2025 with 47.10% share, balancing clarity and storage efficiency. The 4K/UHD bracket is set to grow at a 16.02% CAGR as rail operators and municipal authorities demand higher pixel counts for license-plate and facial analytics.

Storage challenges are easing thanks to edge-based compression ASICs and smarter codecs from domestic brands, allowing UHD streams without proportional bandwidth hikes. HD ≤2 MP cameras persist in budget-sensitive deployments, while enterprise clients increasingly specify ≥8 MP sensors for evidentiary-grade footage.

By Connectivity & Power: Wireless Options Gain Momentum

Wired PoE retained 61.10% of the Japan surveillance IP cameras market size in 2025, valued for reliability and straightforward power delivery. Yet wireless SKUs—leveraging private 5G and Wi-Fi 6—are growing at 14.72% CAGR as factories and temporary event venues avoid costly cabling.

Industrial 5G pilots demonstrate frame-perfect analytics at sub-10 ms latency, validating wireless for safety-critical tasks. Battery-solar hybrids fill remote infrastructure gaps such as levees and mountain tunnels, where grid access is limited but monitoring is mandatory.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

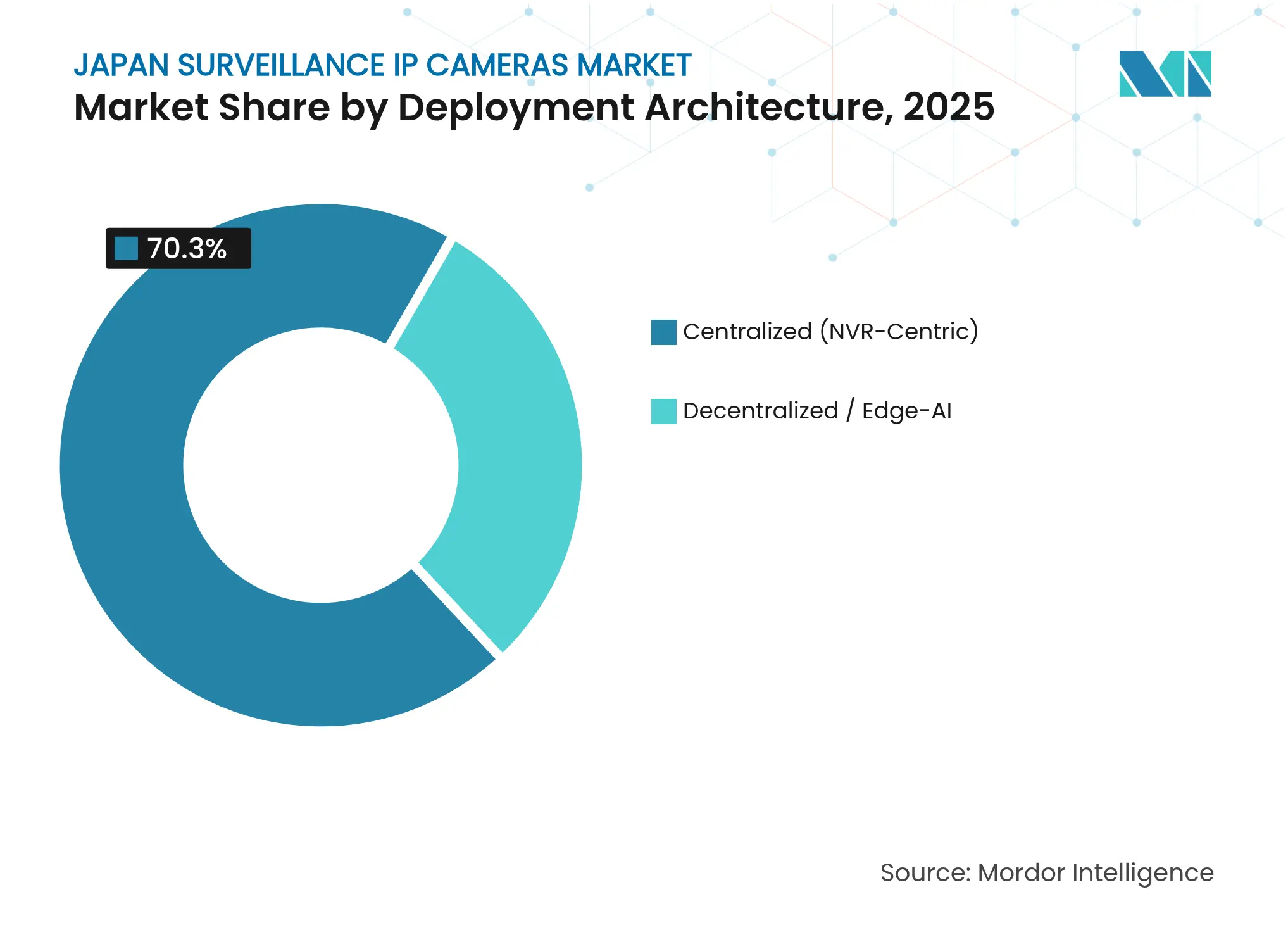

By Deployment Architecture: Edge-AI Reshapes System Design

Centralized NVR platforms still account for 70.30% share, but edge-AI nodes are climbing at 16.65% CAGR to satisfy regulatory and latency requirements. Japan surveillance IP cameras market share is expected to tilt toward decentralized models after 2027, supported by METI grants for generative AI chipsets.

Edge processing reduces attack surfaces by localizing data and lowering traffic to cloud or data centers. Vendors differentiate through proprietary SoCs and containerized analytics that installers can update without replacing hardware, trimming total cost of ownership.

Note: Segment shares of all individual segments available upon report purchase

By End-User Vertical: Residential Smart-Home Leads Growth Curve

Government & Defense represented 20.60% of 2025 revenue, anchored by Kōban upgrades and critical-infrastructure surveillance. Residential smart-home buyers adopt cloud-linked cameras at 14.85% CAGR, driven by aging residents seeking remote check-in capability for health and safety.

Transportation entities embrace onboard video, with Fukuoka’s newest subway cars pioneering in-car 4K coverage. Industrial facilities deploy edge-enabled vision alongside autonomous robots to counter labor shortages, while retail chains layer analytics for shopper-flow and loss-prevention insights.

Greater Tokyo and the surrounding Kanto cluster remain the largest buyers, combining corporate campuses, government ministries, and the country’s busiest commuter lines. Osaka and Nagoya corridors accelerate spending ahead of the 2025 Expo and Shinkansen extensions, focusing on 4K upgrades and facial-ticketing pilots.

In rural prefectures, the aging population drives adoption of cloud-connected cameras in elder-care clinics and private homes, backed by subsidies under the “Digital Garden City” initiative. Private LTE and Wi-Fi HaLow backhaul address connectivity gaps in mountainous terrain.

Northern regions such as Hokkaido demand ruggedized enclosures rated for sub-zero operations and snow load, creating niche opportunities for weather-hardened SKUs. Public acceptance surveys highlight higher trust levels when deployments are transparently communicated, a best practice emulated nationwide.

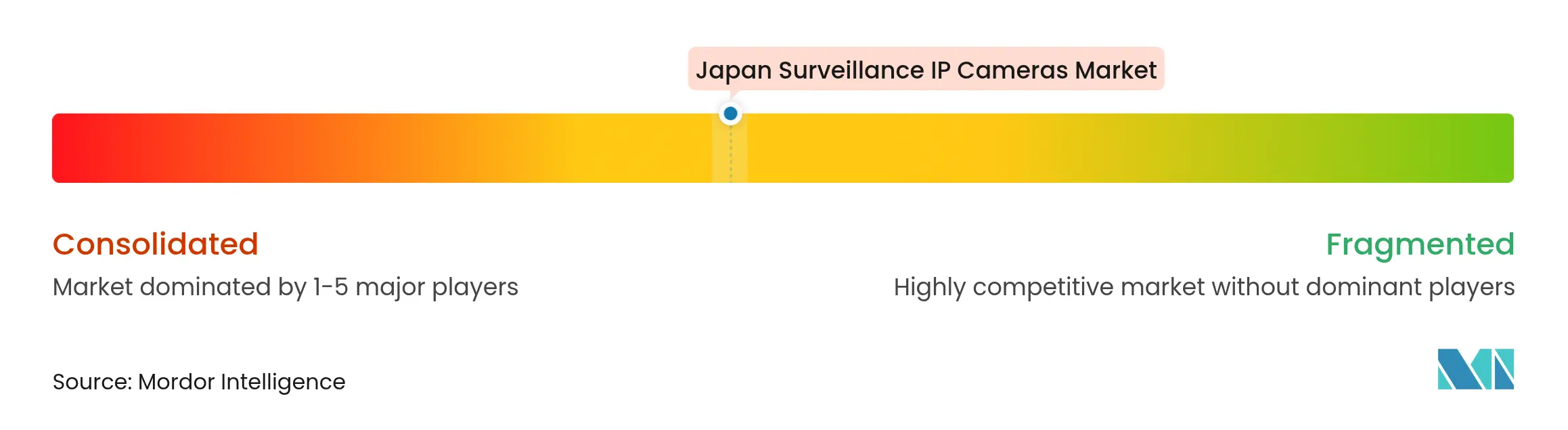

Market Concentration

The Japan surveillance IP cameras market is moderately concentrated. Panasonic i-PRO and Sony leverage domestic manufacturing, stringent quality controls, and alignment with APPI requirements to retain share. Hikvision and Dahua compete on price but face data-security scrutiny, limiting penetration into critical infrastructure.

Strategic partnerships shape differentiation. Yamaman, J MaaS, and Panasonic Connect introduced facial-recognition ticketing, cutting issuance costs by 30%. SoftBank bundles private 5G services with camera analytics in smart-factory engagements to lock in enterprise contracts.

Product roadmaps center on embedded AI. Panasonic’s 2025 corner camera integrates on-device object classification, while Canon harnesses Axis Communications software for scalable VMS offerings. Rising VSaaS players such as Eagle Eye Networks tap SMEs that resist high capital expenditure but still demand sovereign hosting options.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

An IP camera, short for internet protocol camera, transmits and receives video footage over an IP network. Primarily employed for surveillance, it stands out from traditional analog CCTV cameras by eliminating the need for a dedicated recording device, relying solely on a local network. These cameras integrate seamlessly into networks, akin to how phones and computers do.

The Japan surveillance IP camera market is segmented by end-user vertical (banking and financial institutions, transportation and infrastructure, government and defense, healthcare, industrial, retail, enterprise, residential, and others (hospitality and educational institutes)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.