Japan Video Surveillance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

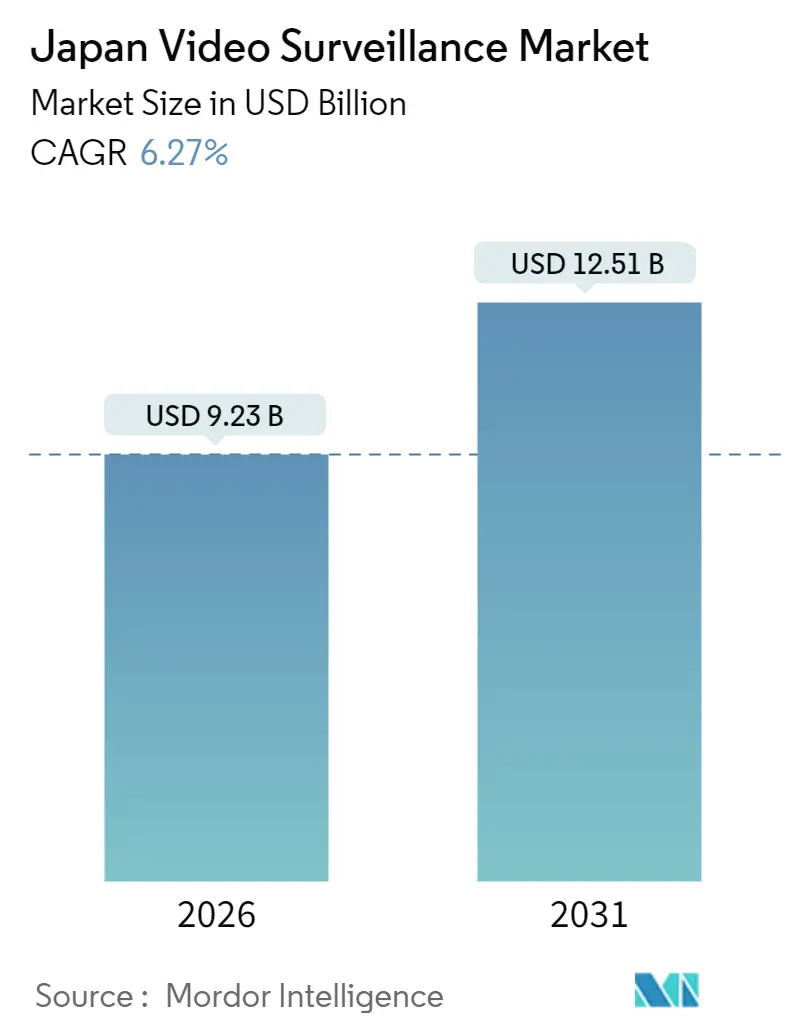

| Market Size (2026) | USD 9.23 Billion |

| Market Size (2031) | USD 12.51 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Video Surveillance Market Analysis by Mordor Intelligence

The Japan video surveillance market size stood at USD 9.23 billion in 2026, and it is projected to reach USD 12.51 billion by 2031, registering a CAGR of 6.27% over the forecast period. Rising urban density, an aging demographic profile, and nationwide infrastructure-modernization mandates are reshaping procurement priorities across public and private sectors, pushing end users toward intelligent cameras, hybrid-cloud storage, and subscription licensing. Local authorities in Tokyo, Osaka, and Fukuoka now embed edge-capable sensors into smart-city platforms that visualize pedestrian flows and traffic anomalies in real time. Enterprises face labour shortages that make automated analytics attractive, while ministries enforce tighter data-protection rules that reward vendors able to anonymize footage on device. Hardware still dominates shipments, yet services are accelerating fastest, signalling a durable shift away from capex-heavy recorder swaps toward Video Surveillance as a Service. Collectively, these forces keep the Japan video surveillance market on a steady mid-single-digit growth trajectory despite component shortages and compliance frictions.

Key Report Takeaways

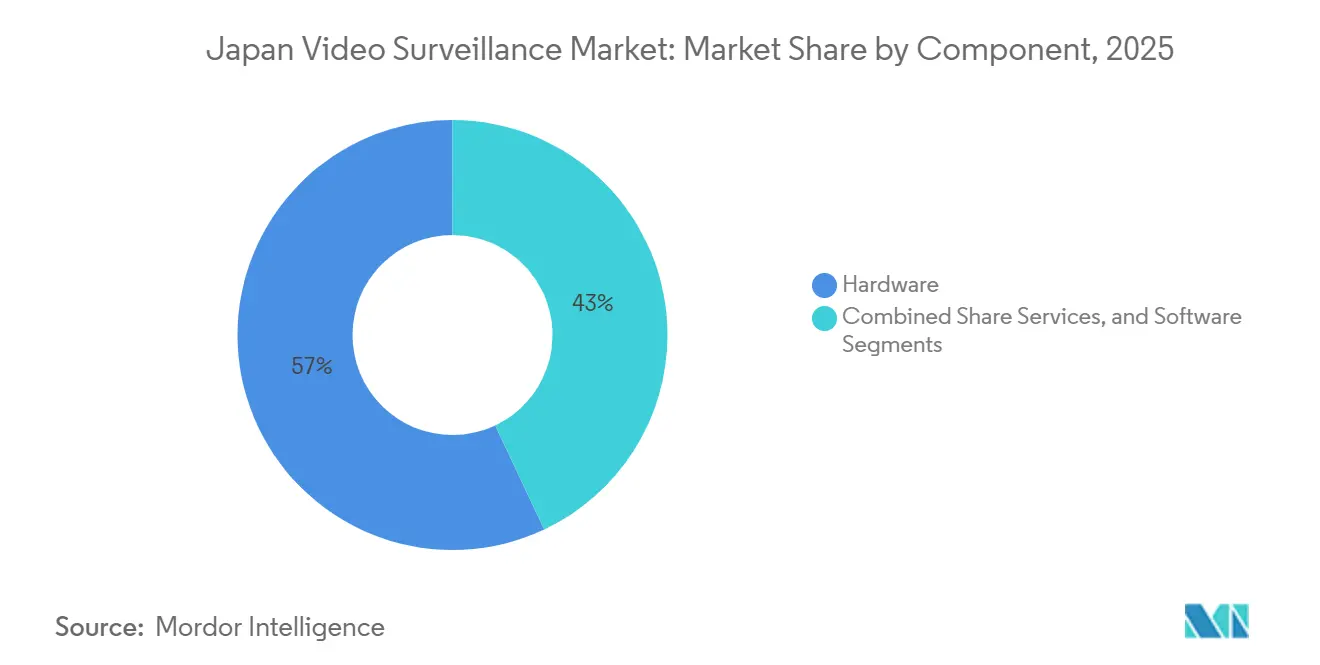

- By component, hardware led with 57.01% revenue share in 2025, while services are forecast to expand at a 7.11% CAGR through 2031.

- By end-user vertical, commercial applications commanded 38.54% of the Japan video surveillance market share in 2025, while residential deployments are projected to grow at a 6.56% CAGR to 2031.

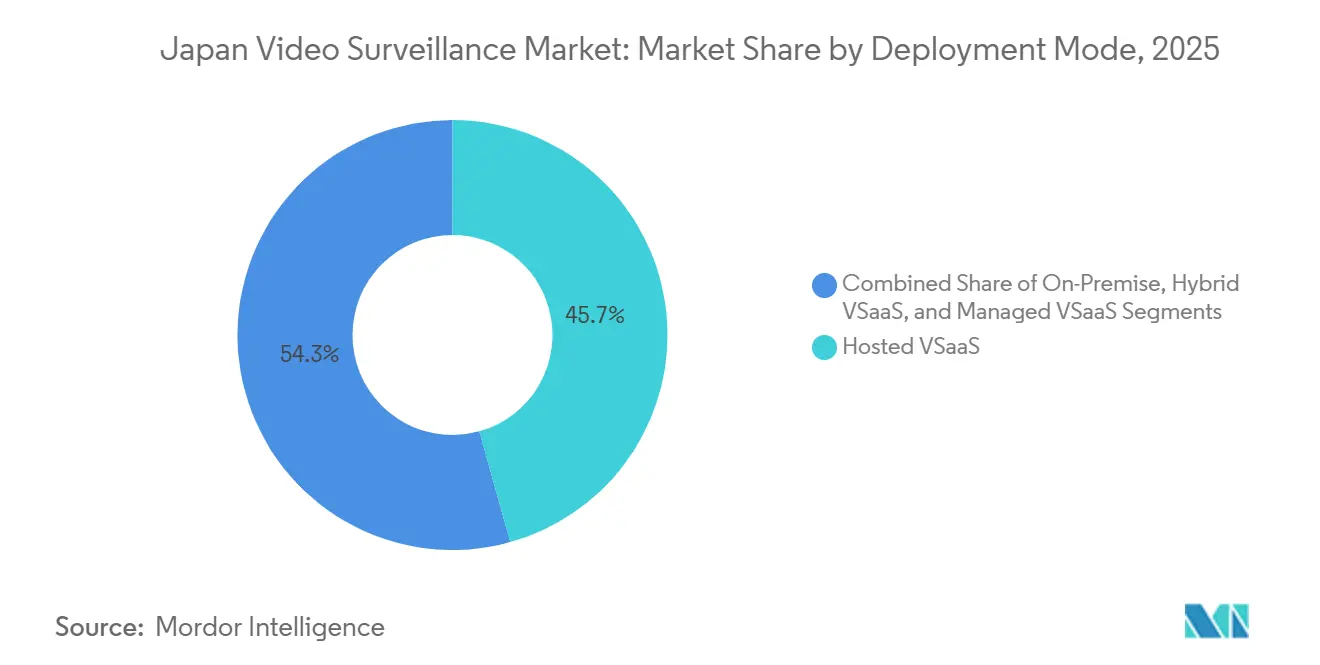

- By deployment mode, hosted VSaaS captured 45.67% of revenue in 2025, and hybrid VSaaS is expected to climb at a 6.89% CAGR over the same horizon.

- By camera resolution, full HD 1080p accounted for 40.67% share of the Japan video surveillance market size in 2025, whereas 4K and above sensors are slated to advance at a 7.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Video Surveillance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Public and Private Investments in Security and Surveillance Systems | +0.90% | National, with concentration in Tokyo, Osaka, and Nagoya metropolitan areas | Medium term (2-4 years) |

| Technological Innovation in Video Surveillance Solutions | +1.10% | National, with early adoption in technology corridors (Kanto, Kansai) | Short term (≤ 2 years) |

| Smart City and Infrastructure Modernization Projects Accelerating Camera Deployment | +1.30% | National, led by Tokyo, Osaka, Fukuoka, and regional smart-city pilots | Medium term (2-4 years) |

| Rapid Adoption of Edge AI Cameras to Reduce Cloud Bandwidth Costs in Dense Urban Areas | +1.00% | National, with highest density in Tokyo, Osaka, and industrial zones | Short term (≤ 2 years) |

| Integration of Video Surveillance with Digital Twins in Manufacturing for Predictive Maintenance | +0.70% | National, concentrated in automotive and electronics manufacturing hubs (Aichi, Shizuoka, Kanagawa) | Long term (≥ 4 years) |

| Aging Population Driving Demand for Elderly Care Monitoring in Smart Homes and Hospitals | +1.20% | National, with acute demand in rural prefectures and urban eldercare facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smart City and Infrastructure Modernization Projects Accelerating Camera Deployment

Tokyo’s 2024 Digital Twin roadmap obliges every new public-works site to stream high-resolution video into a municipal data lake that supports crowd-management dashboards.[1]Tokyo Metropolitan Government, “Tokyo AI Strategy and Digital Twin Initiative,” metro.tokyo.lg.jp Rail operators follow suit: Keisei installed facial-recognition gates in January 2025, and JR Central began real-time overcrowding analytics on Tokaido Shinkansen platforms in January 2026. Airports updated security guidelines in 2024 to specify NEC and Secom biometrics, further enlarging the procurement pool. Collectively, these mandates elevate demand for ONVIF-compliant 4K cameras, low-latency encoders, and cloud-ready VMS. As deployments scale, the Japan video surveillance market benefits from stable multiyear budget allocations that mitigate cyclical spending dips.

Rapid Adoption of Edge-AI Cameras to Reduce Cloud Bandwidth Costs in Dense Urban Areas

NTT’s 4K low-power LSI, announced in 2024, runs object detection on camera boards, cutting upstream bandwidth by up to 80%.[2]NTT Corporation, “4K Low-Power LSI for Edge AI Cameras,” ntt.co.jp i-PRO’s 2024 U-series introduces on-site learning so retailers can train custom classifiers without exporting raw footage. Ambarella chipsets now promise scene-to-text conversion at the edge, enabling natural-language search across distributed fleets. Early adopters include logistics depots and factory floors that require sub-100-millisecond responses to avoid robotic downtime. Because edge inference slashes recurring egress fees, it directly supports subscription uptake, reinforcing the long-term growth profile of the Japan video surveillance market.

Aging Population Driving Demand for Elderly-Care Monitoring in Smart Homes and Hospitals

Japan counted 29% of its citizens aged 65 or older in 2024.[3]Panasonic Corporation, “HomeX and Lifelens Platforms,” panasonic.com Panasonic’s Lifelens couples depth sensors and AI analytics to alert caregivers to falls without transmitting identifiable imagery. Fujitsu prototypes millimeter-wave radars that track motion in private rooms, a design welcomed by regulators wary of intrusive cameras.[4]Fujitsu Limited, “Millimeter-Wave Radar Monitoring,” fujitsu.com Government subsidies rolled out in 2025 lower installation costs in rural prefectures, widening the addressable base. As health-analytics modules plug into existing HomeX hubs, surveillance shifts from perimeter security to wellness assurance, a repositioning that expands value per household and deepens the Japan video surveillance market penetration in residential zones.

Integration of Video Surveillance with Digital Twins in Manufacturing for Predictive Maintenance

NTT and Toshiba demonstrated remote robot control over a 300 km photonic link in 2024, overlaying 4K camera feeds onto real-time 3D plant models. Automotive and electronics giants in Aichi now detect thermal hotspots before machinery fails, trimming downtime and scrap rates. The Beyond 5G white paper of 2024 positions edge cameras as essential to factory digital twins, recommending local preprocessing to satisfy cybersecurity rules. Because predictive maintenance delivers hard cost savings, CFOs approve multi-site rollouts even amid supply-chain volatility, anchoring industrial demand within the Japan video surveillance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and Security Concerns | -0.50% | National, with heightened sensitivity in urban centers (Tokyo, Osaka) | Short term (≤ 2 years) |

| Stringent Data Protection Regulations Limiting Facial Recognition Use | -0.80% | National, enforced uniformly by Personal Information Protection Commission | Medium term (2-4 years) |

| Semiconductor Supply Volatility Increasing Hardware Lead Times | -0.60% | National, affecting all hardware-dependent deployments | Short term (≤ 2 years) |

| Shortage of Skilled Video Analytics Professionals Hindering VSaaS Adoption | -0.40% | National, with acute gaps in regional cities outside Tokyo-Osaka corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Data Protection Regulations Limiting Facial Recognition Use

The 2022 revision of the Act on the Protection of Personal Information, enforced aggressively from 2024, brands facial images as sensitive data that require explicit opt-in or statutory carve-outs. Retailers piloting continuous recognition faced backlash, prompting JR East to pause one line’s trial in April 2025. Compliance now demands anonymization filters, consent dashboards, and audit logs capabilities smaller integrators struggle to fund. These overheads lengthen sales cycles and trim near-term uptake, shaving growth off the Japan video surveillance market until vendors standardize low-friction privacy guards.

Semiconductor Supply Volatility Increasing Hardware Lead Times

Export controls and fab backlogs doubled camera-sensor lead times to 16 weeks in 2024. Premium pixels, such as Canon’s 410-megapixel CMOS launched in 2025, flowed first to defense accounts, leaving volume buyers on allocation. Integrators responded by stockpiling parts, tying up working capital. Vendors like NTT now design proprietary LSIs to hedge external risk, but supply bottlenecks will continue throttling hardware shipments and restraining the Japan video surveillance market until 2027, when capacity expansions at Kumamoto and Ibaraki fabs come online.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Subscription Demand Lifts Services Above Market Average

Services revenue is rising at a 7.11% CAGR to 2031, outpacing both hardware and software as businesses favour predictable operating costs over capex. In 2025, hardware still delivered 57.01% of turnover, reflecting the large installed camera base and the necessity to swap aging analog units. Safie manages 186,000 cloud cameras and posts 31% annual subscriber growth, illustrating the appeal of frictionless onboarding for small retailers. Software sits in the middle, leveraging AI modules that auto-index footage and accelerate incident review. Milestone’s 2025 natural-language plug-in reduces search time by 70% in pilots. As firmware moves to the cloud, hardware vendors embed AI chips and sell licenses per analytic function, blurring category lines. Because these shifts reallocate value capture, the Japan video surveillance market now rewards platforms that bundle upgrade paths across the lifecycle.

The Japan video surveillance market size linked to services is projected to climb from USD 2.9 billion in 2026 to more than USD 4.1 billion by 2031 as VSaaS converts legacy NVR estates. Hybrid bundles that pair on-premises recorders with cloud retention help industrial plants satisfy air-gap requirements without forfeiting remote dashboards. Hardware revenues plateau in unit terms yet stay resilient in value because buyers migrate to 4K sensors with higher ASPs. Software maintains low-double-digit growth as analytics expand from security to business intelligence, such as queue-length detection and merchandising heat maps.

By End-User Vertical: Residential Growth Surges as Smart Homes Mature

Commercial premises generated 38.54% of 2025 revenue, making offices, malls, and hospitality chains the largest buyers of multi-site VMS. Yet residential installations are slated to post the fastest 6.56% CAGR, widening smart-home penetration as homeowners integrate cameras with HVAC and energy dashboards. Panasonic’s HomeX crossed 100,000 users by March 2025, validating bundled ecosystems. Subsidies in the 2025 rural digital-inclusion plan pay up to 30% of device costs, narrowing the affordability gap outside major metros.

Infrastructure applications, including airports, rail, and highways, gain funding through the Tokyo Digital Twin and MLIT airport guidelines. Industrial demand intensifies as factories overlay video onto digital twins for predictive maintenance, reinforcing the Japan video surveillance market share held by manufacturing hubs. Defense and critical-infrastructure clients prioritize encrypted streams and long firmware support, favouring domestic suppliers with local service teams. Across all verticals, integration depth rather than camera count dictates spend, a dynamic that shifts margins toward vendors offering open APIs and analytics libraries.

By Deployment Mode: Hybrid Models Balance Latency and Scale

Hosted VSaaS occupied 45.67% of deployment revenue in 2025 thanks to SMEs that lack on-site IT, yet hybrid VSaaS is forecast to grow at a 6.89% CAGR as larger enterprises combine local storage with elastic cloud archives. VIVOTEK’s VORTEX Connect converts legacy IP cameras to cloud dashboards without rip-and-replace. Genetec reports that 43% of Asia-Pacific clients plan hybrid rollouts, citing bandwidth cost and data-residency rules.

On-premise systems persist where regulation bars external connectivity, such as defense or nuclear sites. Managed VSaaS, staffed by third-party monitoring centers, appeals to chains that want 24-7 response without running SOCs. Edge AI trims backhaul by streaming only events, making cloud use economical even on constrained links. As hybrid adoption widens, the Japan video surveillance market size tied to storage shifts toward subscription object stores, reducing NVR unit volumes yet lifting lifetime revenue per camera.

By Camera Resolution: 4K Adoption Accelerates on Forensic Need

Full HD 1080p retained 40.67% revenue share in 2025, but 4K and above are the fastest segment at 7.35% CAGR, driven by forensic standards requiring readable plates at 30 meters. NTT’s edge LSI compresses 4K streams to 1080p bitrates, alleviating bandwidth fears. Canon’s 410-megapixel sensor allows digital PTZ after the fact, lowering camera count per site.

Standard definition remains only in legacy coax installs scheduled for retirement, while 720p slowly fades where lighting is adequate for 1080p replacements. Buyers increasingly future-proof with 4K as monitor walls migrate to UHD, and as analytics models crave higher pixel density. Bosch’s 3100i and Hanwha’s Wisenet 9 X-series bring 4K and built-in analytics to mid-market price points. Consequently, the Japan video surveillance market size linked to 4K shipments is poised to double over the forecast horizon, even as total camera units grow modestly.

Geography Analysis

Metropolitan Tokyo, Osaka, and Nagoya collectively account for roughly 60% of national expenditure, reflecting dense commercial estates, transit hubs, and high-value assets. Tokyo’s AI Strategy funnels municipal budgets into ONVIF-compliant edge cameras across 23 wards, ensuring steady volume orders. Osaka and Fukuoka replicate the model in park-safety and traffic-monitoring pilots, while Sapporo and Sendai follow at slower pace due to tighter fiscal envelopes.

Industrial belts in Aichi, Shizuoka, and Kanagawa fuel manufacturing surveillance, overlaying live feeds onto digital twins to trim downtime. Coastal prefectures hosting LNG terminals and ports, such as Fukushima, Niigata, and Kagoshima, demand ruggedized, explosion-safe cameras, steering contracts toward domestic vendors with marine certifications. The Japan Coast Guard’s 2024 vessel-detection system merges radar and video to secure territorial waters.

Regional fiber gaps influence architecture choices: gigabit metros adopt cloud-heavy VSaaS, whereas rural districts rely on edge AI to minimize uplink load. The JC-STAR cybersecurity label, mandatory for public procurement from March 2025, standardizes baselines nationwide. Over the 2026-2031 forecast period, the Japan video surveillance market will see convergence, yet geographic nuances in bandwidth, privacy sentiment, and industrial mix will keep vendor go-to-market strategies localized.

Competitive Landscape

Global incumbents Hikvision and Dahua compete alongside Panasonic, Sony, Canon, and NEC, producing a market where no single vendor exceeds a one-third share. Domestic players exploit incumbent building-automation ties, embedding cameras within HVAC, fire, and access suites to elevate switching costs. Cloud-native challenger Safie owns 56.4% of VSaaS subscriptions, proving that frictionless setup and mobile apps trump raw feature lists for SME buyers.

Mitsubishi Electric’s USD 883 million takeover of Nozomi Networks in September 2025 merges industrial intrusion detection with video analytics, signalling that converged OT-IT security stacks are the next battleground. Canon levels up with SPAD low-light sensors that capture colour in near darkness, targeting parking and perimeter sites where IR floodlighting is unwelcome. Verkada’s January 2025 Command 3.0 release offers a mobile-first UX, siphoning digitally native corporates that disdain heavyweight VMS.

Policy shifts also shape competition. The Software Bill of Materials directive issued in August 2024 obliges suppliers to disclose firmware dependencies, adding audit workloads that favour companies with mature engineering governance. Supply-chain volatility sparks vertical integration, with NTT fabricating proprietary chips and Panasonic spinning off i-PRO to accelerate edge-AI roadmaps. As cloud, analytics, and cybersecurity converge, the Japan video surveillance industry rewards platforms that orchestrate cameras, sensors, and network telemetry under one license.

Japan Video Surveillance Industry Leaders

Panasonic System Networks Co., Ltd.

Sony Corporation

Hangzhou Hikvision Digital Technology Company Limited

Bosch Security Systems B.V.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: JR Central began AI video analytics on Tokaido Shinkansen platforms to flag overcrowding and schedule maintenance in real time.

- November 2025: Milestone Systems unveiled a generative-AI plug-in that converts voice queries into forensic searches, trimming investigation time for security teams.

- September 2025: Mitsubishi Electric agreed to acquire the remaining 93% of Nozomi Networks for USD 883 million, integrating OT intrusion detection with surveillance dashboards.

- June 2025: Hanwha Vision released the Wisenet 9 X-series, a 4K-60 fps camera line with on-board license-plate recognition for traffic monitoring.

Japan Video Surveillance Market Report Scope

Video surveillance uses advanced surveillance systems such as security cameras, video recording or video management systems, and various analytics solutions to deter improper behavior or detect unlawful activities at public and private places/buildings.

The Japan Video Surveillance Market Report is Segmented by Component (Hardware including Camera with Analog, IP Cameras, and Hybrid, and Storage; Software including Video Analytics and Video Management Software; Services including VSaaS), End-user Vertical (Commercial, Infrastructure, Institutional, Industrial, Defense, Residential), Deployment Mode (On-Premise, Hosted VSaaS, Managed VSaaS, Hybrid VSaaS), and Camera Resolution (Standard Definition, High Definition, Full HD 1080p, 4K and Above). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Camera | Analog |

| IP Cameras | ||

| Hybrid | ||

| Storage | ||

| Software | Video Analytics | |

| Video Management Software | ||

| Services (VSaaS) |

| Commercial |

| Infrastructure |

| Institutional |

| Industrial |

| Defense |

| Residential |

| On-Premise |

| Hosted VSaaS |

| Managed VSaaS |

| Hybrid VSaaS |

| Standard Definition (SD) |

| High Definition (HD) |

| Full HD (1080p) |

| 4K and Above |

| By Component | Hardware | Camera | Analog |

| IP Cameras | |||

| Hybrid | |||

| Storage | |||

| Software | Video Analytics | ||

| Video Management Software | |||

| Services (VSaaS) | |||

| By End-user Vertical | Commercial | ||

| Infrastructure | |||

| Institutional | |||

| Industrial | |||

| Defense | |||

| Residential | |||

| By Deployment Mode | On-Premise | ||

| Hosted VSaaS | |||

| Managed VSaaS | |||

| Hybrid VSaaS | |||

| By Camera Resolution | Standard Definition (SD) | ||

| High Definition (HD) | |||

| Full HD (1080p) | |||

| 4K and Above | |||

Key Questions Answered in the Report

How big will the Japan video surveillance market be by 2031?

It is projected to reach USD 12.51 billion by 2031, up from USD 9.23 billion in 2026.

What is driving demand for 4K cameras in Japan?

Forensic requirements such as license-plate legibility and digital zoom, plus edge chips that compress 4K streams to manageable bitrates, are accelerating 4K adoption.

Why are services growing faster than hardware?

Enterprises prefer subscription VSaaS that bundles storage, firmware updates, and analytics, reducing upfront capex and IT overhead.

How are privacy laws affecting facial recognition projects?

The 2022 Act on the Protection of Personal Information requires explicit consent for facial recognition, forcing many public pilots to pause or limit scope.

Which deployment model is gaining traction with large enterprises?

Hybrid VSaaS is expanding fastest because it marries on-site recording for low-latency analytics with cloud archives for long-term retention.

What sectors are embracing video-surveillance digital twins?

Automotive and electronics manufacturers use integrated video and 3D models to predict equipment failures and optimize processes.

Page last updated on: