Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Japan Surveillance Camera Market Report is Segmented by Type (Analog, IP, Hybrid HD-Coax), Form Factor (Dome, Bullet, Box, and More), Resolution (HD ≤1080p, Full HD 2MP-4MP, 4K & Above), Sensor Type (CCD, CMOS), Connectivity (Wired, Wireless Wi-Fi/5G), Component (Camera Hardware, Video Storage, and More), End-User Industry (Government and Public Safety, BFSI, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

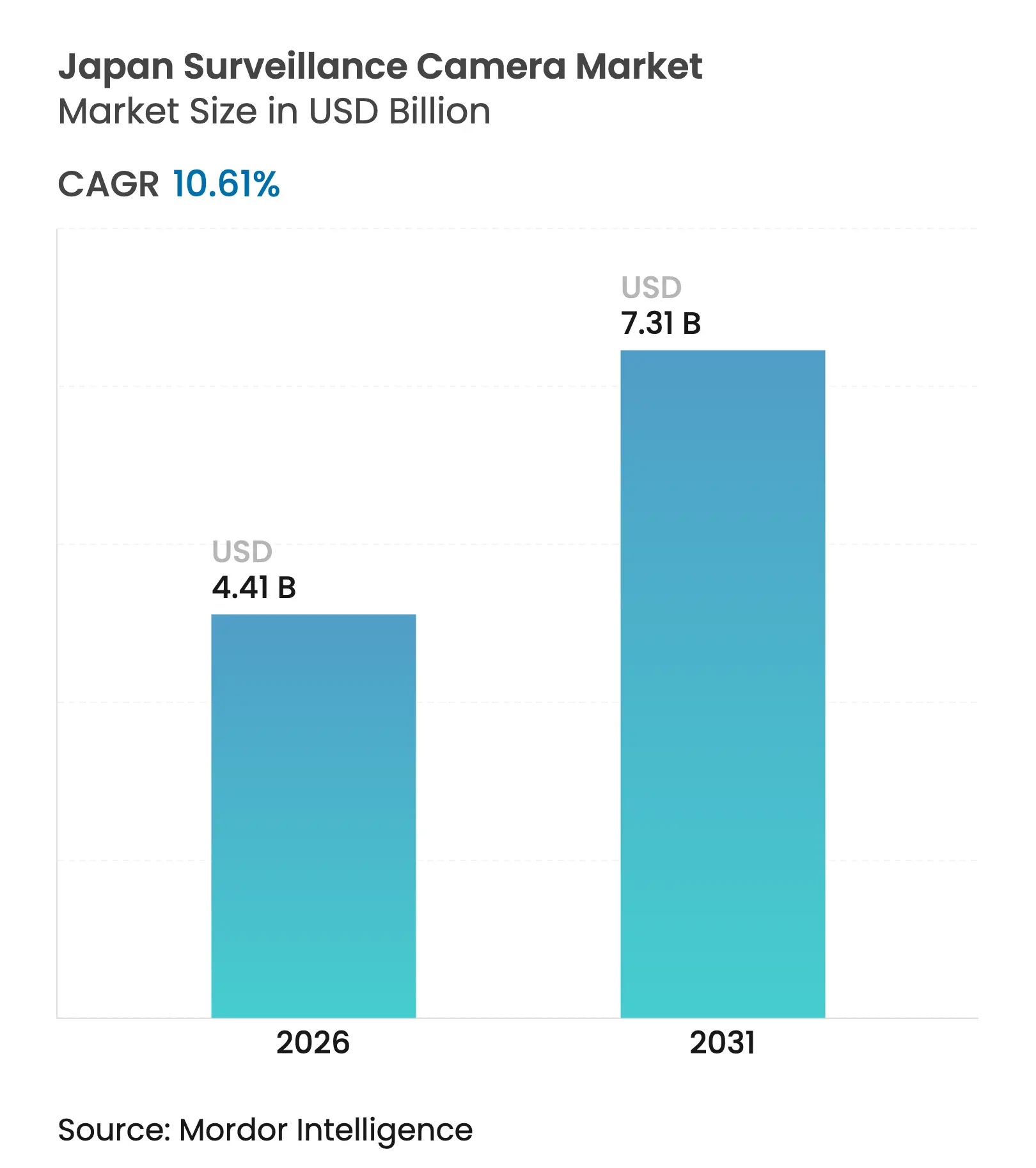

| Market Size (2026) | USD 4.41 Billion |

| Market Size (2031) | USD 7.31 Billion |

| Growth Rate (2026 - 2031) | 10.61 % CAGR |

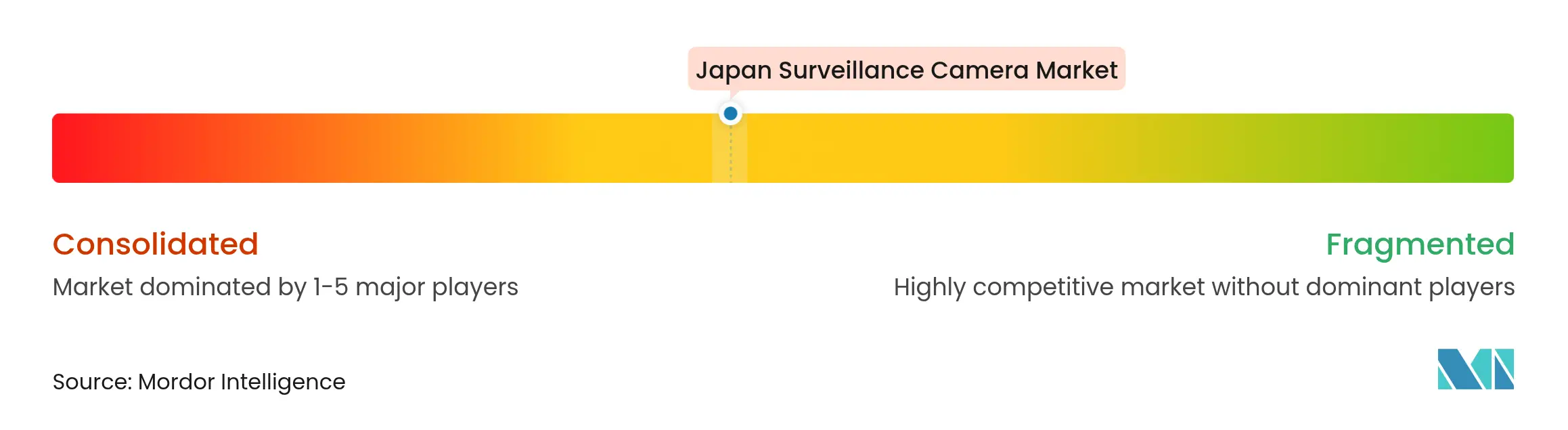

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Japan surveillance camera market size was valued at USD 3.99 billion in 2025 and estimated to grow from USD 4.41 billion in 2026 to reach USD 7.31 billion by 2031, at a CAGR of 10.61% during the forecast period (2026-2031). The strong outlook reflects the Society 5.0 program, which treats cameras as foundational smart-city infrastructure, and aligns with urban security priorities in Tokyo, Osaka, and Fukuoka. Demand also stems from an aging population that requires continuous elder-care monitoring, while enterprises accelerate toward AI-enabled edge analytics for real-time situational awareness. IP cameras, CMOS sensors, and 4K imaging form the technology backbone because they support advanced analytics and integrate smoothly with 5G private networks. Vendors are pivoting from hardware-centric offerings toward software-as-a-service models that promise recurring revenue and rapid feature upgrades.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

AI-enabled edge analytics adoption across public spaces AI-enabled edge analytics adoption across public spaces | +2.8% | National; early uptake in Tokyo, Osaka, Fukuoka | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.8% | Geographic Relevance:National; early uptake in Tokyo, Osaka, Fukuoka | Impact Timeline:Medium term (2-4 years) |

Smart-city & Society 5.0 security projects Smart-city & Society 5.0 security projects | +2.1% | Tokyo, Osaka, Fukuoka metro areas | Long term (≥ 4 years) | |||

Retail shrinkage concerns accelerating video-analytics roll-outs Retail shrinkage concerns accelerating video-analytics roll-outs | +1.4% | National; dense urban retail districts | Short term (≤ 2 years) | |||

Aging-population demand for elder-care & critical-incident monitoring Aging-population demand for elder-care & critical-incident monitoring | +1.7% | National; higher rural penetration | Long term (≥ 4 years) | |||

Logistics hub expansion around Tokyo Bay & Osaka Bay Logistics hub expansion around Tokyo Bay & Osaka Bay | +1.2% | Industrial corridors | Medium term (2-4 years) | |||

Government subsidies for 4K/8K security upgrades at 2025 Osaka Expo Government subsidies for 4K/8K security upgrades at 2025 Osaka Expo | +0.9% | Kansai; national spillover | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

AI-enabled Edge Analytics Adoption Across Public Spaces

NTT and DOCOMO achieved a leap in inference accuracy from 57% to 90% by moving processing to the network edge, proving that distributed intelligence curbs latency and improves real-time detection. [1]NTT DOCOMO Inc., “NTT and DOCOMO Successfully Demonstrates On-Demand Unified Control of Computing Services Through Network and Service Integration,” docomo.ne.jpMunicipal leaders view edge processing as privacy-enhancing because less video leaves the camera, which aligns with APPI mandates. Commercial integrators are bundling edge-ready cameras with micro-NPU boards to reduce server costs and win public tenders. New use cases—such as bear-detection in rural parks—extend value beyond security and encourage multi-departmental funding. As a result, system integrators are shifting R&D toward lightweight, on-device models that operate in bandwidth-constrained environments.

Smart-City & Society 5.0 Security Projects

The Ministry of Land, Infrastructure, Transport and Tourism collects pedestrian flow data in the Otemachi–Marunouchi–Yurakucho district to inform evacuation planning and congestion relief.[2]Ministry of Land, Infrastructure, Transport and Tourism, “人流データを取得する実証実験を行います,” mlit.go.jpOsaka Metro completed network-wide installation of facial-recognition turnstiles ahead of Expo 2025, showcasing frictionless transit and bolstering surveillance coverage. Smart poles on Yumeshima Island integrate cameras, Wi-Fi, and environmental sensors, creating a single mast for multiple municipal services. Foreign technology partners co-develop algorithms with Japanese incumbents and plan export of the jointly-tested solutions. These initiatives elevate Japan surveillance camera market visibility among global investors seeking reference deployments for next-generation smart-city platforms.

Retail Shrinkage Concerns Accelerating Video-Analytics Roll-outs

Shrinkage erodes margins in labor-constrained stores, prompting adoption of 360-degree cameras that combine object tracking, skeletal analysis, and gaze estimation. Retailers pair surveillance with point-of-sale data to flag anomalous transactions instantly. Cloud-native VORTEX, launched by VIVOTEK, allows chain operators to run AI models centrally while pushing updated configurations. The Osaka Expo’s cashless policy is another catalyst; merchants must validate digital payments securely, which spurs camera-to-POS integrations. These dynamics make retail the fastest-growing private-sector adopter in Japan surveillance camera market.

Aging-Population Demand for Elder-Care & Critical-Incident Monitoring

Fujitsu spin-off Ridgelinez pilots gait-analysis algorithms that identify wandering dementia patients and alert caregivers in real time. Elder-care centers retrofit indoor cameras with fall-detection software, reducing nurse rounds and insurance claims. Government dementia strategies provide subsidies for technology that balances safety with privacy, so vendors embed anonymization filters that strip facial data. Rural clinics adopt low-power cameras linked via LPWA networks where fiber is scarce, extending monitoring beyond city centers. Collectively, these applications enlarge total addressable demand and diversify revenue away from security budgets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent personal-data & facial-recognition regulations (APPI) Stringent personal-data & facial-recognition regulations (APPI) | -1.8% | National; stricter urban enforcement | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.8% | Geographic Relevance:National; stricter urban enforcement | Impact Timeline:Long term (≥ 4 years) |

Public opposition to mass-surveillance in urban retail streets Public opposition to mass-surveillance in urban retail streets | -0.9% | Tokyo & Osaka retail districts | Medium term (2-4 years) | |||

Semiconductor supply-chain volatility impacting IP-camera lead-times Semiconductor supply-chain volatility impacting IP-camera lead-times | -1.2% | National; all tech segments | Short term (≤ 2 years) | |||

High retrofit cost for legacy analog infrastructure in municipalities High retrofit cost for legacy analog infrastructure in municipalities | -0.7% | Rural towns, small cities | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Personal-Data & Facial-Recognition Regulations (APPI)

The Personal Information Protection Committee requires disclosure of camera usage objectives and imposes fines up to JPY 100 million (USD 0.94 million) for non-compliance. Retailers must post clear notices and offer opt-out mechanisms, complicating deployment. Vendors respond with on-device redaction and facial-blur plugins that drop biometric data before storage. Procurement cycles lengthen as legal, compliance, and HR teams review impact assessments. Despite these hurdles, compliance-ready solutions command price premiums, cushioning margin pressure.

Semiconductor Supply-Chain Volatility Impacting IP-Camera Lead-Times

Japan relies on imported CIS wafers and SoC chipsets; shortages elongate delivery schedules beyond 20 weeks for select 8 MP modules. The USD 638 million Rapidus fab targets local 2 nm production but will not ease constraints until 2027. OEMs substitute components and redesign boards to secure supply, incurring engineering expenses and quality-control risks. Distributors hoard inventory, raising channel prices and squeezing end-user budgets.

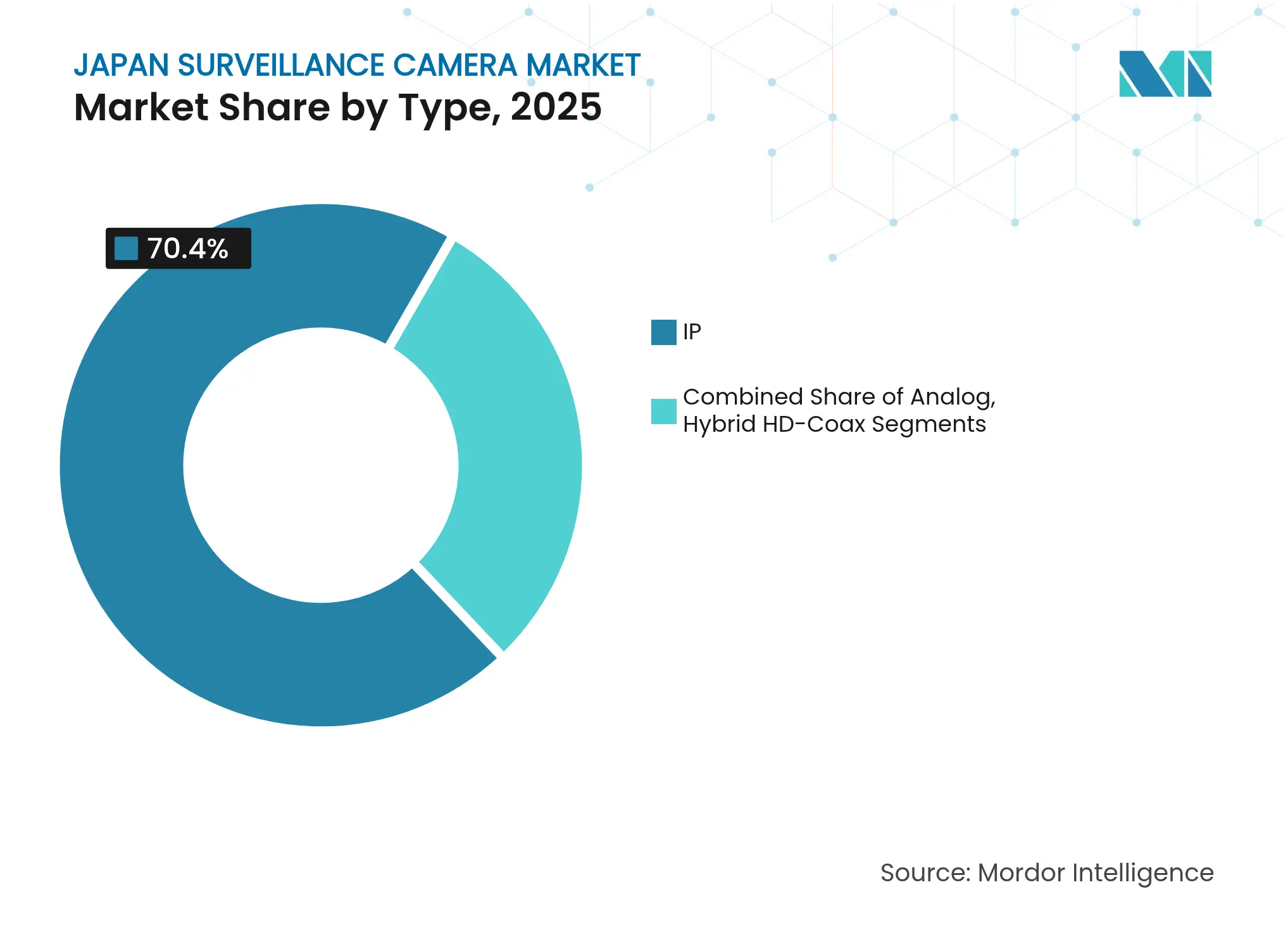

By Type: IP Dominance Accelerates Digital Transformation

IP cameras controlled 70.40% of Japan surveillance camera market share in 2025 as enterprises favored open protocols and cloud integration. This segment, growing at 11.98%, underpins Society 5.0 projects that rely on data interoperability. Analog shipments shrink each quarter because municipalities want future-proofed systems that host edge analytics modules. Hybrid HD-Coax remains a transitional option for sites seeking incremental upgrades without recabling.

IP performance will improve as distributed MIMO under 6 Ghz bands arrives, guaranteeing multi-gigabit links even in high-speed trains. Low-latency backhaul enables AI inference on moving buses, broadening scope for mobile surveillance. As IP endpoints expose APIs, software vendors bundle advanced functions—loitering detection, PPE compliance—through over-air firmware updates, thereby raising switching costs and deepening ecosystem lock-in across Japan surveillance camera market.

Note: Segment shares of all individual segments available upon report purchase

By Form Factor: 360-Degree Innovation Challenges Traditional Designs

Dome units retained a 31.50% revenue slice in 2025 due to vandal resistance in retail and transit stations. Yet 360-degree cameras are advancing at 11.23% CAGR because they cut blind spots and drop total unit counts. Bullet cameras remain the choice for perimeter fences where long-range IR illumination is vital, whereas PTZ models serve stadiums requiring operator control.

Fisheye sensors now pair with de-warping algorithms inside the camera, delivering panoramic streams to VMS platforms without extra compute. Retailers leverage this feature to map shopper journeys, while logistics operators overlay counting zones on warehouse floors to manage congestion. These benefits reinforce uptake, positioning fisheye models as catalyst for higher-margin sales within Japan surveillance camera market.

By Resolution: 4K Adoption Accelerates Despite Full HD Dominance

Full HD devices still command 47.60% of 2025 shipments, balancing bandwidth and clarity in mainstream deployments. Government incentives ahead of Expo 2025 spur 4K adoption, yielding the fastest 13.25% CAGR. HD-only units are relegated to low-risk areas such as parking garages. AI vendors advise clients that higher pixel density lifts detection accuracy for small objects, strengthening the investment thesis.

Technology pipelines include flexible silicon imagers targeting panoramic 8K sensors, which NHK expects to commercialize by 2025. Declining SSD prices reduce storage cost per terabyte, neutralizing one historic barrier to high-resolution rollout. Consequently, premium resolution forms a new differentiation vector for smart-city tenders in Japan surveillance camera market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Sensor Type: CMOS Overwhelming Dominance Reflects Technology Maturity

CMOS captured 92.70% of shipments in 2025, buoyed by superior low-light performance and back-side illumination advances. The segment is expanding 12.65% annually as domestic fabs refine pixel architectures. CCD remains confined to scientific imaging and niche archival projects. Sony’s sensing division logged double-digit revenue growth, highlighting spillover from smartphone innovations to surveillance.

CMOS roadmaps integrate stacked AI inference engines, compressing video and running models locally. This hardware synergy shortens latency and underpins privacy-by-design mandates. As a result, government buyers specify CMOS as a default requirement in tender documents, cementing its leadership in Japan surveillance camera market.

By Connectivity: Wireless Growth Challenges Wired Infrastructure

Wired links account for 67.30% of deployments, prized for deterministic performance in mission-critical venues. Wireless units, however, grow 11.92% annually thanks to local 5G licenses that permit factory-wide private networks. Installation firms quote 25% lower labor costs when cabling is unnecessary, speeding project timelines.

Low-latency 5G slices support real-time analytics at container yards where cameras ride automated cranes. Vendors integrate Wi-Fi 6 and 5G radios into single boards, enabling fallback redundancy. The Ministry of Internal Affairs and Communications reports 153 sub-6 GHz licenses issued, portending wider acceptance.As SLA-backed wireless matures, share gain will continue inside Japan surveillance camera market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

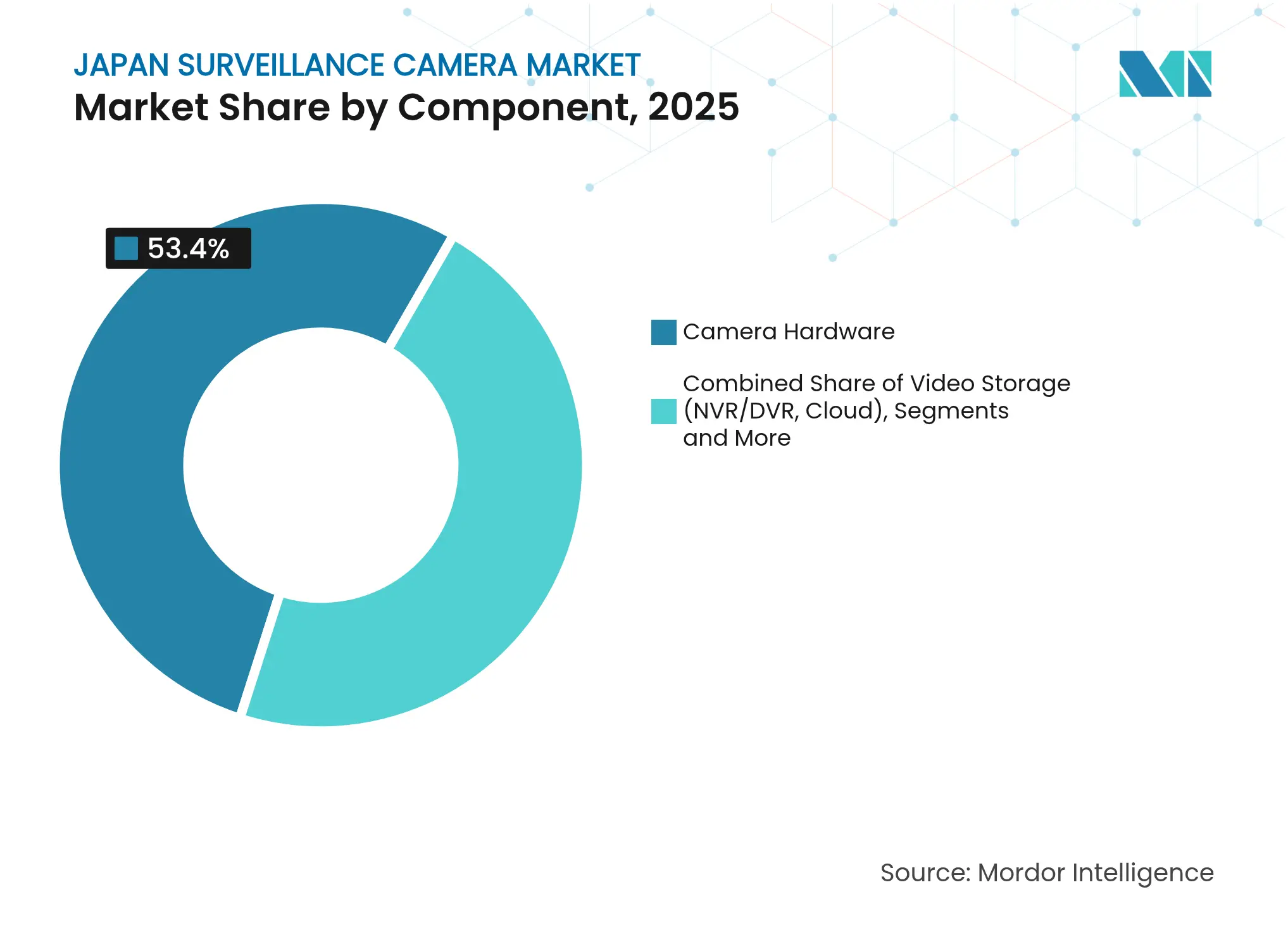

By Component: Software and AI Services Drive Value Creation

Hardware still supplies 53.40% revenue, yet software and AI services climb 12.22% annually. Vendors unbundle analytics into tiered subscriptions—object counting, emotion detection, anomaly scoring—creating predictable ARR streams. Video storage shifts toward cloud NVRs where consumption-based pricing aligns cost with footage retention policies.

LiLz raised JPY 430 million to commercialize AI-as-a-service paired with low-power cameras for industrial inspections. Such moves illustrate the pivot from capex to opex and further entrench software’s role in overall Japan surveillance camera market growth.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Government Leadership with Retail Acceleration

Government and public safety commanded 28.60% share in 2025, underpinned by disaster-response networks and crime prevention. Retail and hospitality produce the highest 10.56% CAGR as multi-store chains adopt cloud VMS and smart checkout. Banking sustains steady demand for tamper-proof evidence storage, while healthcare invests in patient-safety analytics.

Logistics operators embrace license-plate recognition to automate gates; manufacturers leverage vision systems for quality assurance. Education campuses deploy perimeter surveillance tied to emergency-alert apps, balancing safety and privacy. This broadening of vertical use cases cements diversified revenue streams across Japan surveillance camera industry.

Kanto secured 37.70% of Japan surveillance camera market in 2025, reflecting Tokyo’s dense population and concentration of high-value assets. Smart-city pilots, including autonomous-bus corridors, create fertile ground for AI-heavy deployments. The Autoflow-Road conveyor project will add hundreds of roadside cameras for cargo tracking once operational, extending demand across the Kanto–Kansai corridor.

Kansai ranks second and is accelerating as Expo 2025 investments upgrade stations, stadiums, and tourist venues. The region’s cashless initiative means every transaction node requires embedded video verification, intertwining surveillance with fintech back-ends. Port facilities around Osaka Bay also deploy thermal cameras for nighttime cargo inspections, broadening industrial demand.

Kyushu and Chugoku follow as mid-tier regions, adopting surveillance for inbound-tourism safety and aging-population monitoring. Local governments tap national digital-transformation grants to replace analog systems with edge-AI cameras. Rural prefectures focus on cost-effective, solar-powered units that operate on LTE-M networks, illustrating that growth is not confined to megacities but diffuses outward, enlarging overall Japan surveillance camera market footprint.

Market Concentration

Domestic incumbents—Panasonic, Sony, and i-PRO—leverage deep optics expertise and long-standing government relationships to retain key accounts. They accelerate shift toward AI-ready SoCs and emphasize APPI compliance as a trust differentiator. Chinese entrants such as Dahua and Hikvision pursue price-led penetration and partner with local distributors for service coverage. European suppliers Axis and Bosch concentrate on cyber-hardened products and open-platform SDKs to win premium projects.

Start-ups cluster around cloud analytics and vertical-specific algorithms. Patent filings related to observation systems soared, reflecting active R&D and defensive IP strategies. Strategic partnerships proliferate; JR East-MODE align IoT sensors with rail surveillance, while KDDI and NEC integrate telecom security stacks. Taken together, the landscape shifts from hardware share battles to ecosystem positioning within Japan surveillance camera market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Surveillance cameras, also known as security cameras, are video cameras designed to monitor specific areas. Typically, they link to a recording system or an IP network and are monitored, particularly in commercial settings. The study evaluates the trends and dynamics related to different types of surveillance cameras across various end-user verticals in Japan. Furthermore, the study considered the sales of surveillance cameras by major market vendors in Japan as the baseline for market estimation.

The Japan surveillance camera market is segmented by type (analog-based, IP-based) and by end-user industry (government, banking, healthcare, transportation and logistics, industrial, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Deep-Dive Analysis of Feed Probiotics Across Key Regions

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.