Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

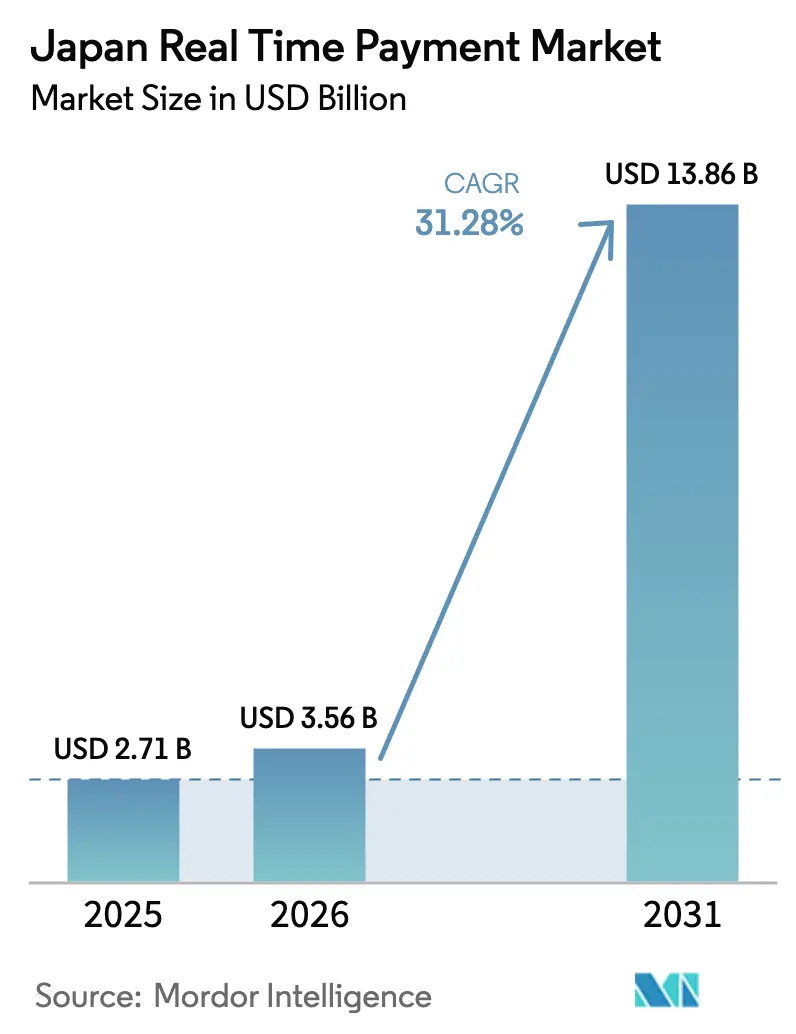

| Base Year Market Size (2025) | USD 2.71 Billion |

| Market Size (2026) | USD 3.56 Billion |

| Market Size (2031) | USD 13.86 Billion |

| Growth Rate (2026 - 2031) | 31.28% CAGR |

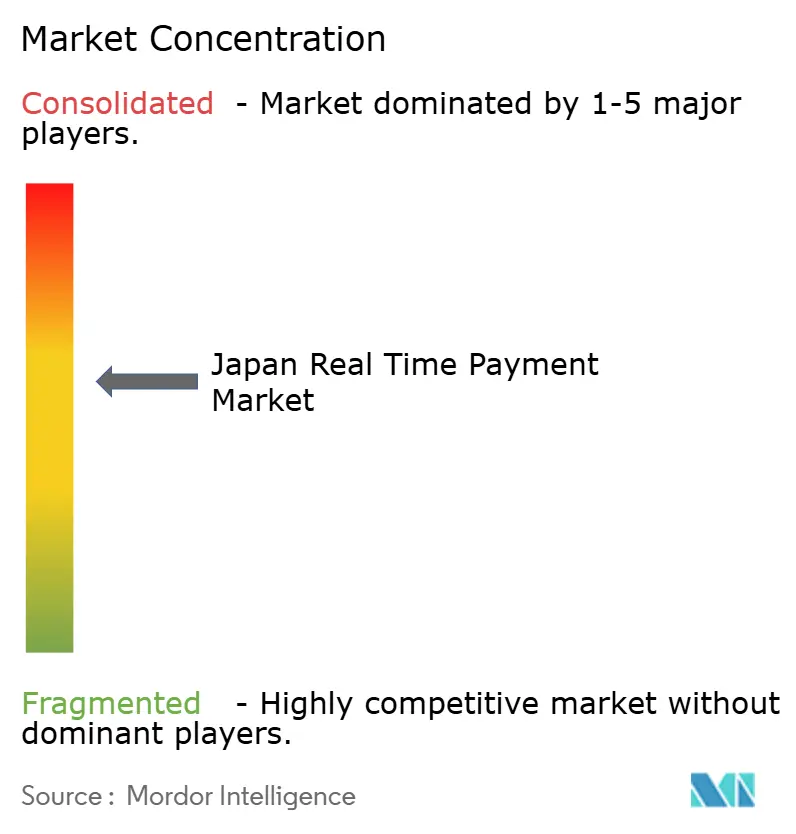

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Real Time Payment Market Analysis by Mordor Intelligence

The Japan real time payment market size was valued at USD 2.71 billion in 2025 and estimated to grow from USD 3.56 billion in 2026 to reach USD 13.86 billion by 2031, at a CAGR of 31.28% during the forecast period (2026-2031). Three structural forces are accelerating this growth: the government’s JPY 100 trillion cashless vision that subsidizes point-of-sale hardware, the November 2025 ISO 20022 cutover of BOJ-NET and Zengin RT-Net, and a super-app rivalry led by PayPay, LINE Pay, and Rakuten Pay. Rapid 5G coverage, which reached 96.6% of the population by late 2024, underpins low-latency authentication, while the Zengin More Time System’s 24/7 settlement window pulls corporate liquidity flows onto instant rails. Merchant interchange caps compress processor margins, yet embedded-finance bundles keep QR acceptance attractive for small retailers despite thin economics. Bank of Japan CBDC pilots and cross-border ISO 20022 linkages with Singapore and Thailand signal a future in which real-time rails extend beyond domestic boundaries.[1]Bank of Japan, “Payment System Modernization,” BOJ, boj.or.jp

Key Report Takeaways

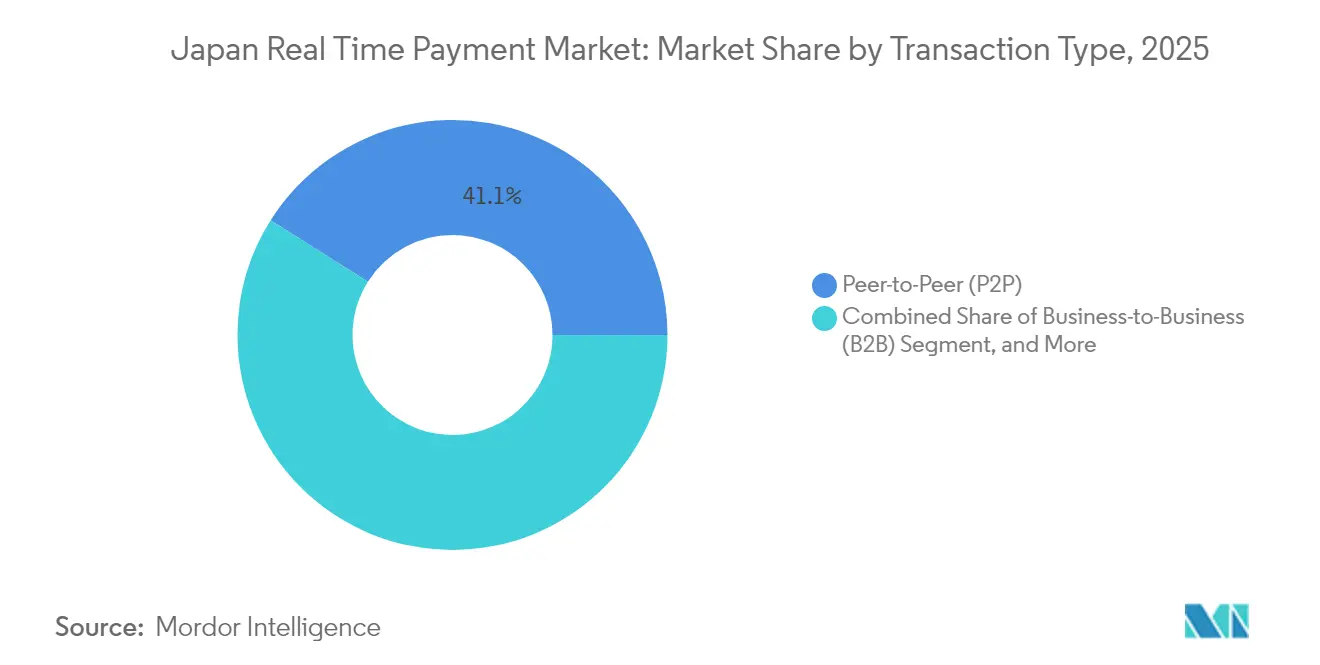

- By transaction type, peer-to-peer transfers captured 41.05% of the Japan real time payment market share in 2025, while business-to-business flows are forecast to grow at a 32.60% CAGR through 2031.

- By enterprise size, small and medium-sized enterprises held 46.10% of the Japan real time payment market share in 2025, whereas micro-businesses are projected to expand at a 32.95% CAGR to 2031.

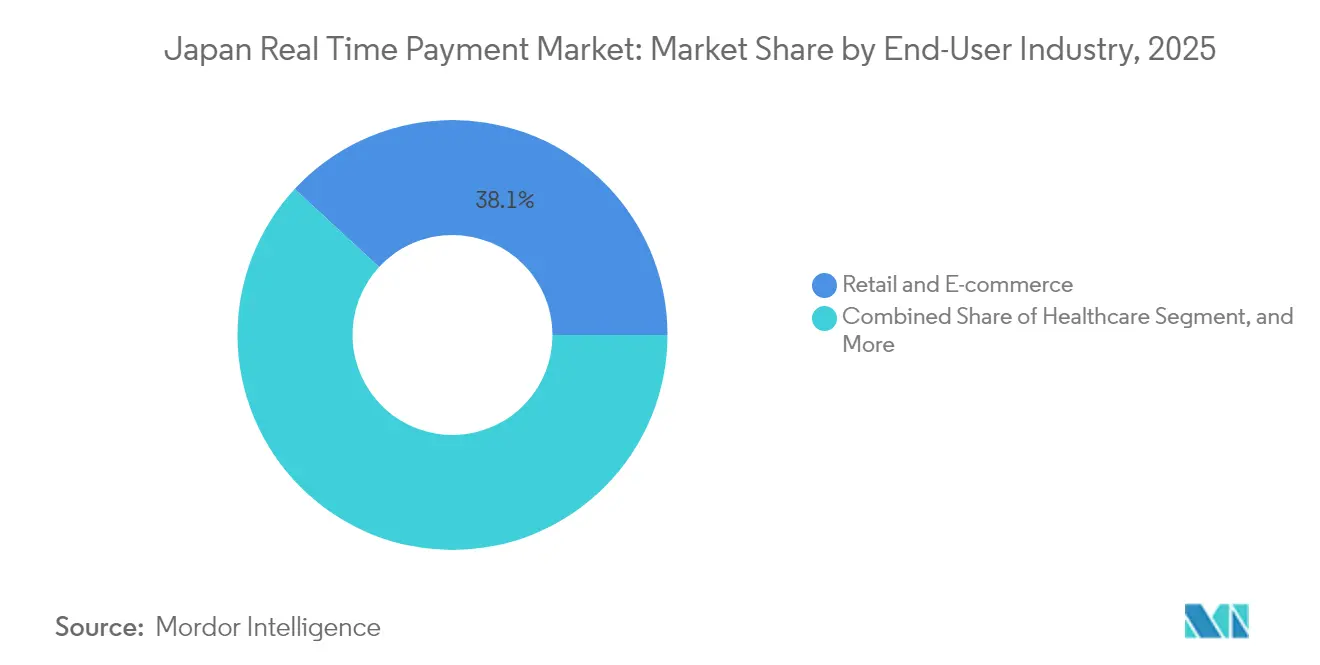

- By end-user industry, retail and e-commerce led with 38.12% of the Japan real time payment market share in 2025; transportation and mobility is set to advance at a 32.50% CAGR through 2031.

- By technology rail, mobile-wallet overlays commanded 52.05% of the Japan real time payment market size in 2025, yet API and ISO 20022 push payments are expected to post a 33.10% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Real Time Payment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising smartphone penetration and 5G roll-out | +6.2% | National, with early gains in Tokyo, Osaka, Nagoya metro areas | Short term (≤ 2 years) |

| Government JPY 100 trillion cashless vision and subsidy schemes | +7.8% | National, concentrated in SME-dense prefectures | Medium term (2-4 years) |

| Migration to ISO 20022 real-time rails (RT-Net upgrade) | +5.4% | National, cross-border spillover to ASEAN corridors | Medium term (2-4 years) |

| E-commerce checkout abandonment pressure on merchants | +4.1% | National, e-commerce hubs in Kanto and Kansai regions | Short term (≤ 2 years) |

| Corporate treasury demand for intraday liquidity | +5.9% | National, multinational treasury centers in Tokyo | Long term (≥ 4 years) |

| Super-app ecosystems (LINE Pay / PayPay) race for users | +8.2% | National, urban youth and commuter segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Smartphone Penetration and 5G Roll-Out

Japan’s 5G footprint covers nearly the entire population, enabling sub-10-millisecond payment authentication and smoother in-app checkout experiences. Enhanced connectivity shifts fraud detection from overnight batch scoring to real-time behavioral analytics, reducing false declines and encouraging cash-centric users to adopt mobile wallets. Amazon Web Services is investing USD 15 billion in local data centers by 2027, guaranteeing low-latency API calls that keep real-time gateways responsive.[2]Amazon Web Services, “AWS Japan Region Expansion,” AWS, aws.amazon.com Despite these gains, households in mountainous Tohoku prefectures still experience network blind spots, prolonging cash reliance among older residents. The continued rollout of rural micro-cell towers and simplified wallet interfaces for seniors remains critical to closing the urban–rural adoption gap.

Government JPY 100 Trillion Cashless Vision and Subsidy Schemes

The Ministry of Economy, Trade and Industry subsidizes up to 75% of terminal costs for retailers earning under JPY 10 million, accelerating merchant enablement in convenience-store and hospitality segments.[3]Ministry of Economy, Trade and Industry, “Cashless Payment Promotion 2024,” METI, meti.go.jp A cross-ministry API framework launched in 2024 connects My Number Card identity verification to payment rails, trimming wallet KYC from three days to minutes. Prefectural cashback campaigns have temporarily lifted QR volumes by 40%, though sunset dates raise sustainability concerns. The Financial GIF now mandates real-time settlement for public-utility bills by April 2026, embedding push payments into monthly household routines. Execution risk lingers, as some municipal billing systems still process fixed-field data formats that cannot parse ISO 20022 tags.

Migration to ISO 20022 Real-Time Rails (RT-Net Upgrade)

BOJ-NET and Zengin transitioned to ISO 20022 messaging in November 2025, enabling the use of structured remittance data and end-to-end identifiers that eliminate the need for manual invoice matching for corporates. Early adopters report a 30% reduction in settlement costs on high-volume payables. Fintechs now initiate transfers via secure APIs instead of screen scraping, thereby reducing the risk of credential theft and accelerating open banking innovation. Cross-border pilot corridors to Singapore and Thailand cut remittance fees by 40%, yet foreign-exchange spreads still deter small-ticket transfers. Domestic SMEs with legacy accounting packages face integration challenges, which slow down universal straight-through processing.

E-Commerce Checkout Abandonment Pressure on Merchants

Manual entry of card details pushes Japan’s cart abandonment rate toward 70%, a pain point that can be resolved when bank-credential APIs prefill checkout fields. Rakuten Ichiba’s one-click checkout has lowered abandonment by almost one-fifth, recovering significant gross merchandise value. PayPay’s mini-app plug-ins cut redirect drop-offs by double-digit percentage points, boosting merchant conversion rates. Live-commerce streams gain traction because instant push payments prevent buyer remorse during flash sales. Nevertheless, the absence of card-style chargeback rights in push-payment schemes fuels consumer complaints when goods are not delivered, prompting regulators to explore the use of mandatory escrow for high-value transactions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High share of small-value cash transactions in rural Japan | -3.7% | Rural prefectures (Tohoku, Shikoku, Hokkaido) | Medium term (2-4 years) |

| Merchant interchange caps limit economics for PSPs | -2.9% | National, acute in low-density retail zones | Long term (≥ 4 years) |

| Cyber-fraud surge in push payments (APP scams) | -4.2% | National, elderly and first-time digital-payment users | Short term (≤ 2 years) |

| Fragmented QR code standards slowing ubiquity | -3.1% | National, merchant adoption bottleneck | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Share of Small-Value Cash Transactions in Rural Japan

Coins and notes still account for 55% of convenience-store purchases outside major metropolitan areas, reflecting patchy network coverage and a cultural preference for tangible money among residents aged 65 and above. My Number Card readers have yet to penetrate mom-and-pop shops, as the costs of firmware exceed the perceived benefits. Depopulation reduces daily sales, making terminal support unprofitable for processors unless it is bundled with higher-margin services. Until offline QR codes or voice-activated prompts reach mass deployment, cash will remain dominant for sub-JPY 1,000 tickets in sparsely populated districts.

Merchant Interchange Caps Limit Economics for PSPs

QR discount rates benchmarked against 3.25% credit-card caps leave processors with roughly 40–60 basis-point net revenue after network fees and fraud reserves. Super-apps can cross-subsidize through advertising, but mono-line acquirers serving rural merchants struggle to break even. GMO Payment Gateway disclosed that many countryside accounts operate at a loss unless bundled with e-commerce hosting. Surcharging is prohibited, so merchants cannot steer to cheaper rails, keeping card networks entrenched even as real-time alternatives proliferate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transaction Type: B2B Liquidity Optimization Drives Fastest Growth

B2B settlements are forecast to climb at a 32.60% CAGR, the quickest among transaction classes, as treasurers exploit the Zengin More Time System to sweep idle balances and automate payables using ISO 20022 references. Peer-to-peer transfers still led 2025 volume, holding 41.05% of Japan real time payment market share, energized by group-payment features in super-apps.

Corporate disbursements such as payroll and insurance claims are migrating from batch ACH to push payments, allowing employees and claimants to receive funds within minutes. Government-to-consumer flows remain nascent but will accelerate once real-time payouts of social-security benefits go live under the Digital Agency’s 2026 mandate. Straight-through reconciliation cuts back-office workload for conglomerates, yet smaller suppliers without ERP plug-ins must still match invoices manually.

By Enterprise Size: Micro-Businesses Leapfrog via Embedded Finance

Small and medium-sized enterprises held 46.10% of Japan real time payment market share in 2025 thanks to low-cost QR adoption. Embedded-finance suites now let even sole proprietors issue invoices and obtain short-term credit inside the same wallet, driving a forecast 32.95% CAGR for micro-business transactions.

Large corporates wield the highest average ticket values and negotiate direct Zengin connections that bypass overlay fees, but they are hampered by legacy accounting systems unable to read ISO 20022 tags. Rural micro-merchants remain hard to serve profitably under capped interchange, though bundling with buy-now-pay-later or loyalty marketing can improve unit economics.

By End-User Industry: Transportation Leads on Account-Based Ticketing

Retail and e-commerce retained the largest 38.12% share in 2025 as super-apps embedded one-click pay buttons. Transportation and mobility, buoyed by JR East’s shift to account-based Suica, is projected to expand at a 32.50% CAGR.

Healthcare is digitizing co-pay collection via telemedicine portals, while utilities must accept real-time push payments by April 2026, onboarding 15 million households. Financial-services firms leverage instant rails for real-time loan disbursement and insurance payouts, compressing settlement windows from days to minutes.

By Technology Rail: API Push Payments Gain on Open Banking

Mobile-wallet overlays controlled 52.05% of 2025 payment-rail volume, but API and ISO 20022 push payments are set to grow at 33.10% CAGR as banks expose secure endpoints. ISO 20022 XML migration underpins straight-through corporate reconciliation and cross-border harmonization, drawing B2B flows from wire transfers.

QR-code overlays remain fragmented due to proprietary standards, while Zengin RT-Net continues to process high-value transfers with sub-10-second confirmations. A potential Bank of Japan CBDC could, in time, replace commercial-bank intermediation for retail transfers if pilots prove technically and commercially viable.

Geography Analysis

Mobile-wallet usage clusters along the Tokyo-Osaka-Nagoya corridor, which generated 61.73% of the national real-time volume in 2025, is driven by dense merchant networks and the headquarters of multinationals that fuel B2B flows. Tokyo’s Kanto region relies heavily on PayPay, whose 4.4 million merchant points saturate urban streetscapes. Kansai consumers exhibit above-average Rakuten Pay adoption, thanks to the firm’s Osaka roots and local retail alliances. In contrast, Fukuoka’s fintech sandbox status has spurred QR volumes in Kyushu, with cashback pilots lifting adoption by 40%.

Rural prefectures lag behind as limited cell coverage and aging demographics sustain cash dominance, with coins and notes used in 55% of convenience store purchases. Terminal subsidies covering 75% of hardware costs have yet to overcome low transaction density in depopulating municipalities. My Number Card penetration hit 70% nationally in 2024, yet card-reader scarcity confines digital ID-based payments to major supermarkets and transit hubs.

Cross-border ISO 20022 linkages reduce remittance fees by 40% for the 2.9 million foreign workers in Japan, but these corridors still account for under 2% of the total volume. The 2025 Osaka-Kansai Expo is expected to catalyze wallet usage among inbound tourists, creating a demonstration effect that could encourage lagging regions to upgrade their acceptance infrastructure.

Competitive Landscape

PayPay leads with an estimated 35–40% share of mobile-wallet volume, followed by LINE Pay at 20–25%, and Rakuten Pay at 15–18%. Meanwhile, megabanks Mitsubishi UFJ, Sumitomo Mitsui, and Mizuho control the underlying Zengin rails without owning consumer-facing front ends. Each super-app pursues ecosystem lock-in: PayPay bundles ride-hailing and securities trading; LINE Pay embeds payments into messenger-based social flows; Rakuten Pay ties loyalty points across a vast retail network. Fintech challengers Kyash and Smartpay target micro-merchants with instant settlement and buy-now-pay-later overlays, cutting time-to-funds from days to seconds.

NTT DATA’s Anser-BX platform achieved sub-50-millisecond initiation latency by deploying edge nodes in 12 prefectures, enabling real-time inventory reservation for flash-sale e-commerce. Regulatory deadlines under the revised Payment Services Act require Confirmation-of-Payee by December 2025, favoring incumbents with deep KYC repositories and raising entry barriers. The Bank of Japan’s CBDC pilot, now involving 64 firms, explores offline-payment cryptography that could disrupt existing PSP revenue streams if the central bank eventually issues wallets directly to consumers.

A Japan Fair Trade Commission probe launched in 2024 examines whether bundling financial services with messaging or e-commerce forecloses competition in adjacent markets such as credit scoring or insurance distribution. Industry observers expect remedies such as mandatory API access for rival wallets rather than structural separation, but supervisory scrutiny may temper cross-promotion practices.

Japan Real Time Payment Industry Leaders

ACI Worldwide

FIS Global

Fiserv, Inc.

PayPal Holdings, Inc.

Mastercard Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Regulatory compliance under the Financial Services Agency's revised Payment Services Act mandates that all licensed providers implement Confirmation of Payee checks by December 2025, a requirement that favors incumbents with existing KYC databases and raises barriers for new entrants lacking identity-verification infrastructure Financial Services Agency.

- November 2025: SWIFT's MT message format was deprecated globally in November 2025, forcing Japanese banks to retrofit core systems and exposing interoperability gaps with regional partners in ASEAN that are still migrating SWIFT.

- November 2025: The upgrade mandates structured address fields for cross-border interoperability and deprecates SWIFT MT globally, forcing Japanese banks to retrofit core systems and exposing integration gaps with ASEAN partners still migrating.

- November 2025: Bank of Japan and Japanese Bankers Association completed migration of BOJ-NET and Zengin RT-Net to ISO 20022 messaging standards, replacing legacy SWIFT MT formats with structured XML that carries remittance data and invoice references, enabling straight-through reconciliation for corporate treasurers and cutting settlement costs by 30% for firms processing over 10,000 monthly invoices Bank of Japan Japanese Bankers Association.

Japan Real Time Payment Market Report Scope

The Japan real time payment market report is segmented by Transaction Type (Peer-to-Peer (P2P), Peer-to-Business (P2B), Business-to-Business (B2B), Business-to-Consumer (B2C), Government-to-Consumer (G2C)), Enterprise Size (Large Enterprises, Small and Medium-sized Enterprises (SMEs), Micro-businesses), End-User Industry (Retail and E-commerce, Banking, Financial Services and Insurance (BFSI), Healthcare, Transportation and Mobility, Government and Public Utilities, Other End-User Industries), and Technology / Payment Rail (Zengin RT-Net (Bank Account-to-Account), QR-Code Overlay Services, Mobile Wallet Overlay, API / ISO 20022 Push Payments). The Market Forecasts are Provided in Terms of Value (USD).

By Transaction Type

| Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Government-to-Consumer (G2C) |

By Enterprise Size

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

| Micro-businesses |

By End-User Industry

| Retail and E-commerce |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| Transportation and Mobility |

| Government and Public Utilities |

| Other End-User Industries |

By Technology / Payment Rail

| Zengin RT-Net (Bank Account-to-Account) |

| QR-Code Overlay Services |

| Mobile Wallet Overlay (e.g., PayPay, LINE Pay) |

| API / ISO 20022 Push Payments |

| By Transaction Type | Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) | |

| Business-to-Business (B2B) | |

| Business-to-Consumer (B2C) | |

| Government-to-Consumer (G2C) | |

| By Enterprise Size | Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) | |

| Micro-businesses | |

| By End-User Industry | Retail and E-commerce |

| Banking, Financial Services and Insurance (BFSI) | |

| Healthcare | |

| Transportation and Mobility | |

| Government and Public Utilities | |

| Other End-User Industries | |

| By Technology / Payment Rail | Zengin RT-Net (Bank Account-to-Account) |

| QR-Code Overlay Services | |

| Mobile Wallet Overlay (e.g., PayPay, LINE Pay) | |

| API / ISO 20022 Push Payments |

Key Questions Answered in the Report

What is the current value of the Japan real time payment market?

The market is valued at USD 3.56 billion in 2026 and is projected to reach USD 13.86 billion by 2031.

Which segment is growing fastest within Japan’s instant-settlement ecosystem?

Business-to-business payments are forecast to rise at a 32.60% CAGR as treasurers leverage 24/7 liquidity.

How many users does PayPay have in Japan?

PayPay surpassed 65 million registered users in October 2024, processing roughly 1.2 billion transactions each month.

What regulatory milestone supports cross-border interoperability?

The November 2025 migration of BOJ-NET and Zengin RT-Net to ISO 20022 structured messages enables seamless international reconciliation.

Why do rural prefectures still favor cash?

Patchy network coverage, aging demographics, and thin merchant economics keep coins and notes dominant for small-ticket purchases outside major metros.

Page last updated on: