Japan Lithium-ion Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

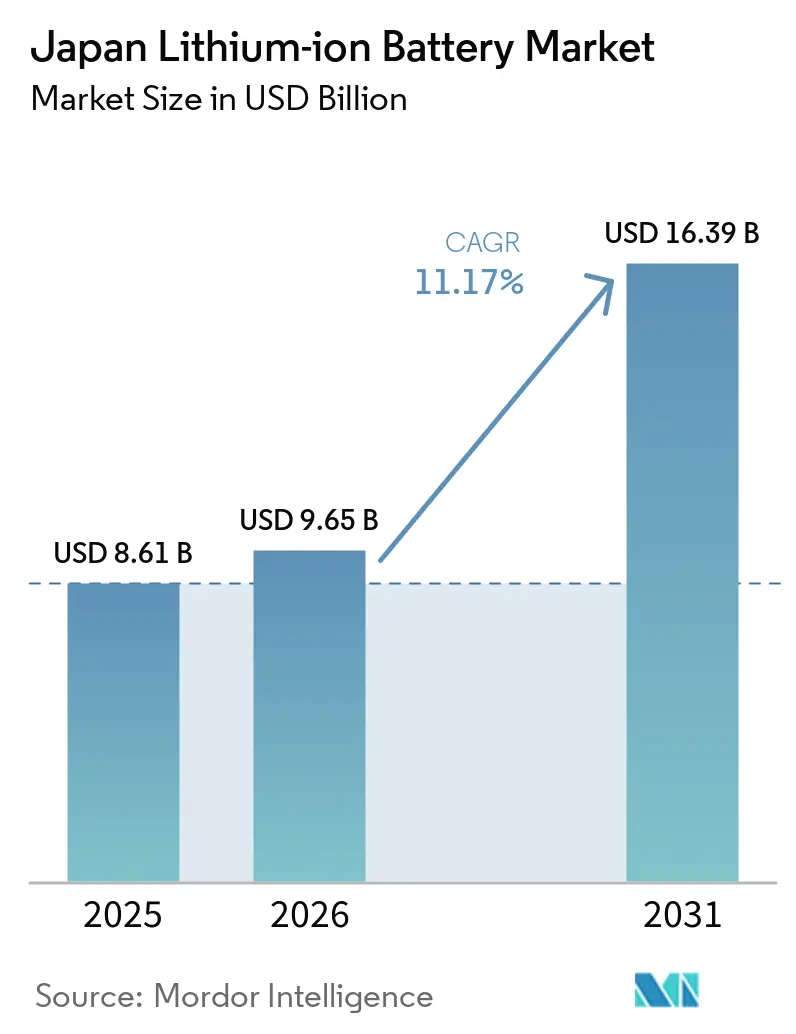

| Base Year Market Size (2025) | USD 8.61 Billion |

| Market Size (2026) | USD 9.65 Billion |

| Market Size (2031) | USD 16.39 Billion |

| Growth Rate (2026 - 2031) | 11.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Lithium-ion Battery Market Analysis by Mordor Intelligence

The Japan Lithium-ion Battery Market size is projected to expand from USD 8.61 billion in 2025 and USD 9.65 billion in 2026 to USD 16.39 billion by 2031, registering a CAGR of 11.17% between 2026 to 2031. Rapid subsidy reform, an aggressive solid-state commercialization roadmap, and the build-out of virtual power-plant programs move batteries from simple energy stores to dynamic grid assets, reinforcing the long-term rise of the Japan Lithium-ion Battery market. Domestic content rules tied to life-cycle carbon disclosures now reward local cell producers that run on Japan’s comparatively low-carbon power mix, while export demand for high-reliability industrial batteries supports margins as global mining, robotics, and marine operators shift to electrified platforms. Solid-state pilots backed by JPY 20 trillion in Green Transformation (GX) support funding promise step-change energy density and charging speed, sustaining investor confidence. Meanwhile, the Japan Lithium-ion Battery market benefits from frequency-regulation revenues under the national capacity market, which shortens payback periods for grid-scale storage projects.

Key Report Takeaways

- By product type, Lithium Cobalt Oxide held 30.9% revenue share of the Japan Lithium-ion Battery market in 2025, while Lithium Titanate is forecast to expand at a 19.8% CAGR to 2031.

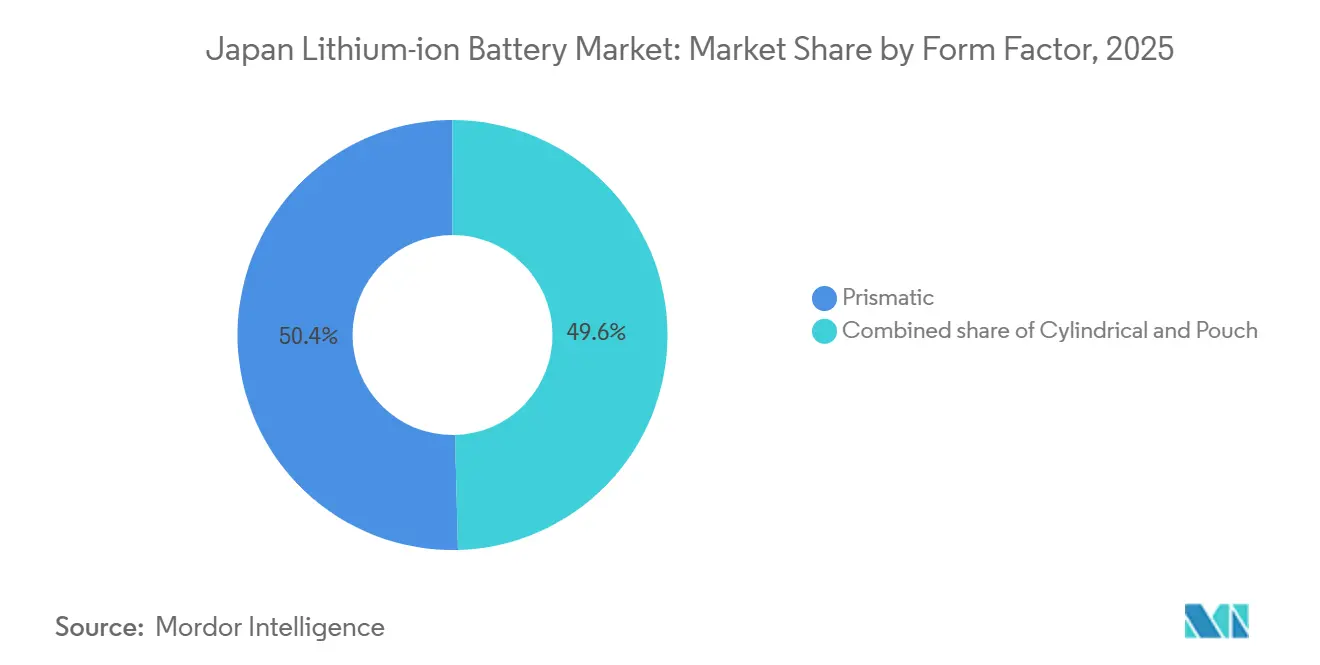

- By form factor, prismatic cells led with 50.4% of the Japan Lithium-ion Battery market share in 2025, whereas cylindrical cells are projected to grow 16.7% annually through 2031.

- By power capacity, cells up to 3,000 mAh accounted for 33.1% of the Japan Lithium-ion Battery market size in 2025, while the above-60,000 mAh band is advancing at a 20.9% CAGR to 2031.

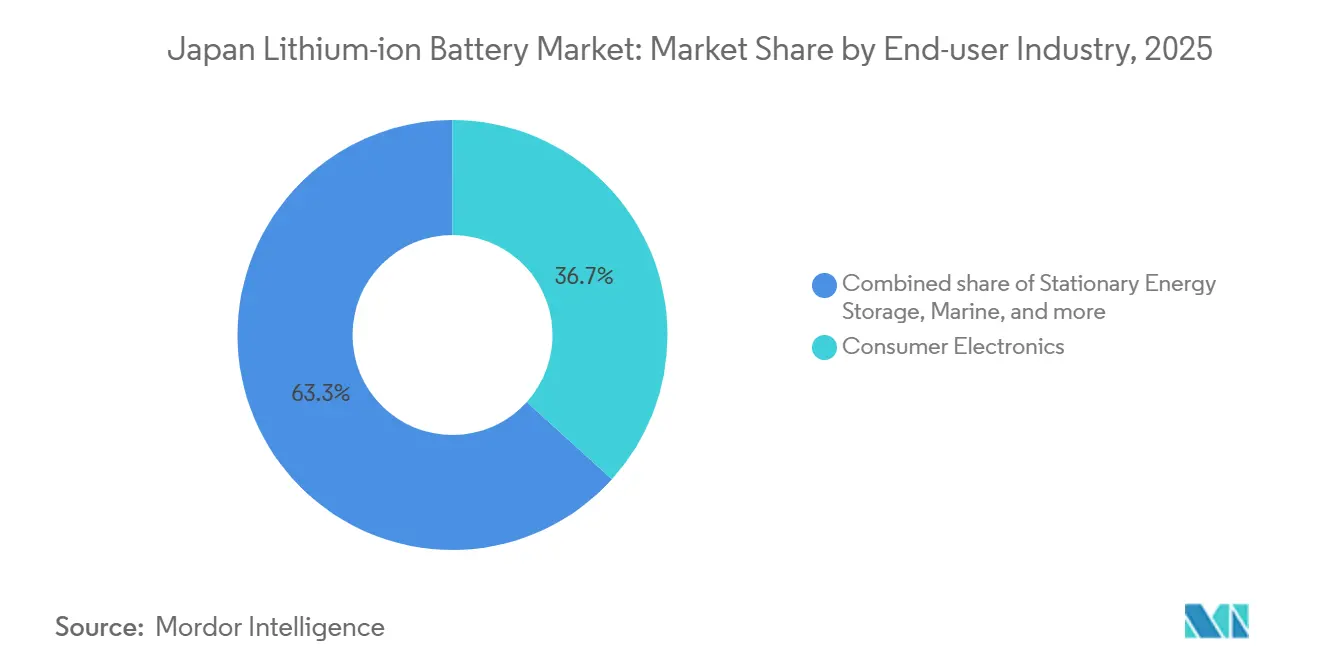

- By end-use industry, consumer electronics retained 36.7% share of the Japan Lithium-ion Battery market size in 2025; stationary energy storage is growing at a 22.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Lithium-ion Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government EV subsidies & corporate carbon-neutral mandates | + 2.30% | National, metropolitan prefectures | Medium term (2-4 years) |

| Accelerated domestic solid-state R&D roadmap | + 1.80% | National, pilot lines in Aichi, Kanagawa, Shizuoka | Long term (≥ 4 years) |

| ESS build-out for virtual-power-plant programs | + 1.50% | National, early pilots in Tokyo, Osaka, Kyushu | Medium term (2-4 years) |

| Export demand for high-reliability industrial batteries | + 1.20% | Global, focus on APAC and Oceania | Short term (≤ 2 years) |

| Corporate fleet electrification of kei-class logistics vehicles | + 1.40% | National, urban logistics hubs | Short term (≤ 2 years) |

| Circular-economy value capture via re-use & recycling hubs | + 0.90% | National, facilities in Ibaraki, Okayama | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government EV Subsidies & Corporate Carbon-Neutral Mandates

Japan raised its electric-vehicle incentive ceiling to JPY 1.3 million in fiscal 2024 but tied eligibility to battery production CO₂ footprints, forcing automakers to source low-emission domestic cells [1]Ministry of Economy, Trade and Industry, “GX Basic Policy and Carbon Pricing Framework,” METI, meti.go.jp. Voluntary emissions trading began in fiscal 2023 and became mandatory in 2026, lifting the cost of carbon-intensive imported batteries. Corporate members of Keidanren must disclose Scope 3 emissions by 2025, so cell suppliers certified under ISO 14067 gain preferential access to procurement lists [2]Keidanren, “Carbon Neutral Action Plan,” KEIDANREN, keidanren.or.jp. The revised Energy Conservation Act also compels large power users to install on-site storage, anchoring demand for stationary systems independent of utility procurements. Collectively, these rules strengthen domestic value capture within the Japan Lithium-ion Battery market.

Accelerated Domestic Solid-State R&D Roadmap (Post-2027 Launch Targets)

Toyota, Nissan, and Panasonic operate pilot lines aiming for 2027-2028 mass production of sulfide or oxide solid-state cells that promise 1,200 km driving range and 10-minute charging [3]Tokyo Metropolitan Government, “Residential ESS VPP Program,” METRO TOKYO, metro.tokyo.lg.jp. Idemitsu Kosan supplies sulfide electrolytes, targeting production costs below JPY 10,000 per kWh by 2030. Government grants under NEDO and GX bonds cushion capital expenditure, while technical challenges such as interface resistance remain. Early volumes will likely serve premium vehicles and aerospace systems, but confidence in the technology accelerates investment throughout the Japan Lithium-ion Battery market.

ESS Build-Out for Virtual-Power-Plant Programs

Since 2020, the national capacity market has allowed aggregated batteries to earn availability payments, stabilizing cash flow for storage projects. Regulatory changes enacted in 2024 allow simultaneous participation in supply-demand adjustment markets, doubling revenue options. Tokyo’s 5,000-unit residential VPP demonstration shows real-time control in 200 milliseconds, validating dispatchable flexibility. Offshore wind targets of 10 GW by 2030 amplify storage demand, positioning the Japan Lithium-ion Battery market for multi-gigawatt annual additions.

Export Demand for High-Reliability Industrial Batteries

Japanese lithium-ion cells deliver cycle life above 10,000 full discharges and operate from -30 °C to 45 °C, attracting mining, robotics, and marine buyers that accept premium prices. Toshiba’s lithium titanate batteries already power autonomous haul trucks in Australia, and GS Yuasa supplies batteries for automated guided vehicles in semiconductor fabs. Margins on these exports run 50-70% above automotive averages, supporting reinvestment even as the Japan Lithium-ion Battery market shifts toward EV volume.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility & China refining dependence | -1.20% | Global supply chains, with acute impact on Japan's import-dependent manufacturers | Short term (≤ 2 years) |

| Lengthy domestic permitting for gigafactory expansion | -0.80% | National, with permitting delays concentrated in rural prefectures requiring multi-year environmental assessments | Medium term (2-4 years) |

| Ageing charger network & high-power upgrade costs | -0.70% | National, with infrastructure gaps most severe in northern Honshu and Hokkaido; urban-rural disparity in charger density | Medium term (2-4 years) |

| Shrinking domestic consumer-electronics production base | -0.60% | National, driven by offshore migration to Vietnam, China, and Southeast Asia; impacts small-format cell demand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility & China Refining Dependence

Lithium carbonate collapsed from USD 80,000 per ton in 2022 to USD 10,000-15,000 in 2024, disrupting mine investments and threatening future supply when demand rebounds. Japan imports nearly all of its lithium and cobalt, while China controls about two-thirds of global refining, exposing cell makers to geopolitical risk. Although long-term offtake deals secure volumes for Panasonic and GS Yuasa, smaller firms lack balance-sheet capacity, widening the cost gap within the Japan Lithium-ion Battery market.

Lengthy Domestic Permitting & Ageing Charger Network

Environmental reviews for factories over 50,000 m² extend to 48 months, double the timelines in South Korea or China. Prime Planet’s Tokushima expansion slipped 14 months owing to water-use objections. Public chargers numbered only 30,000 in 2024 against a 2030 target of 300,000, and 80% are slow AC units unsuitable for commercial fleets. These infrastructure gaps moderate near-term growth in the Japanese lithium-ion Battery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: LTO Surge Challenges LCO Legacy

Lithium Cobalt Oxide captured 30.9% of the Japan Lithium-ion Battery market share in 2025, reflecting entrenched consumer-electronics demand. Lithium Titanate is set to grow at 19.8% per year through 2031 as mining vehicles and frequency-regulation projects value 20,000-cycle durability over energy density. In automotive, Nickel-rich chemistries such as NMC and NCA dominate, with Panasonic’s 4680 cells reaching 260 Wh/kg for Tesla platforms [4]Panasonic Holdings Corporation, “Wakayama Plant Expansion,” PANASONIC, panasonic.com. LFP adoption remains limited because cold-weather range loss impedes sales in northern prefectures, though cost pressure could spur gradual uptake. Manganese-based cells serve hybrids and power tools, benefiting from thermal stability.

Over the forecast horizon, the Japan Lithium-ion Battery market will likely segment along three chemistry lanes: cobalt-rich for premium density, titanate for industrial longevity, and manganese or iron phosphate for cost-sensitive mass markets. Each lane requires distinct precursor supply chains, reshaping procurement among cell makers. As solid-state technology matures, chemistries may reorganize once more, but until then, cell producers must manage complex portfolios to balance margin and volume.

By Form Factor: Prismatic Entrenchment vs Cylindrical Renaissance

Prismatic cells delivered 50.4% of shipments in 2025, favored by Japanese automakers for pack packaging efficiency. Cylindrical output is forecast to rise 16.7% annually as Panasonic ramps 4680 lines in Wakayama and Kansas, offering fivefold capacity gains over 2170 predecessors. Pouch variants stay niche because swelling risks complicate thermal control in long-life industrial settings. The Japan Lithium-ion Battery market thus sees form-factor lock-in, with automakers reluctant to redesign packs mid-cycle.

Format choices influence supplier bargaining power. Automakers embedded in prismatic architectures rely on Prime Planet, reinforcing medium-term stability, while Panasonic’s cylindrical roadmap leverages external EV platforms and export demand. Solid-state breakthroughs could upend this balance by introducing new geometries unbound by liquid-electrolyte constraints.

By Power Capacity: Mega-Capacity Modules Displace Small-Cell Dominance

Cells up to 3,000 mAh represented 33.1% of the Japan Lithium-ion Battery market size in 2025, but the share will erode as smartphone volumes plateau. The above-60,000 mAh tier, which feeds grid-scale storage and heavy-duty EV packs, is growing at 20.9% per year and will outpace smaller classes by 2031. Mid-range capacities serve power tools and passenger EV modules, yet commoditization pressures trim margins.

Manufacturers respond by automating high-capacity module lines and reallocating capital from legacy small-cell plants. Solid-state energy-density gains could shrink physical footprints, allowing the Japan Lithium-ion Battery market to deliver more kilowatt-hours per square meter of factory floor.

By End-Use Industry: Stationary Storage Overtakes Consumer Electronics

Consumer electronics held 36.7% of the Japan Lithium-ion Battery market size in 2025, but growth slowed to low single digits as domestic assembly moved offshore. Stationary energy storage grows 22.3% annually, buoyed by capacity-market payments and VPP aggregation revenues. Automotive demand climbs on the 2035 100% electrification target, led by kei-class logistics fleets that standardize 20 kWh packs.

Industrial, aerospace, and marine segments remain small in volume yet yield premium margins that offset competitive pressure in mass-market EV cells. The Japan Lithium-ion Battery market, therefore, balances high-volume automotive contracts with lower-volume, higher-margin specialty niches.

Geography Analysis

Production clusters in Aichi, Shizuoka, and Kanagawa host integrated battery and vehicle assembly lines that shorten logistics and satisfy domestic-content incentives. Metropolitan prefectures such as Tokyo and Osaka account for 60% of EV registrations, sustaining nearby pack-integration facilities. Northern regions lag in charger density, yet large-scale wind and solar farms in Hokkaido deploy 500 MWh of co-located storage, creating a counter-cyclical source of demand.

Japan exports premium industrial batteries to Australia’s mining sector and supplies tariff-free automotive cells to North America under the critical minerals agreement, anchoring external revenue. At the same time, Korean and Chinese competitors set up Japanese plants to win local contracts, intensifying price pressure. Regional demand gradients within the country and cross-border policy shifts abroad compel manufacturers to optimize factory footprints for both domestic service and export compliance, reshaping geographic strategy in the Japan Lithium-ion Battery market.

Competitive Landscape

Japan Lithium-ion Battery Market is semi concentrated. Panasonic dominates cylindrical NCA supply to Tesla and premium automakers, Prime Planet leads prismatic deliveries to Toyota hybrids and EVs, and GS Yuasa specializes in industrial and aerospace packs. Korean entrants LG Energy Solution and Samsung SDI pursue local production to undercut costs, while CATL and BYD explore partnerships but face brand-loyalty barriers.

Technology transitions are pivotal. Toyota and Panasonic target pilot sulfide solid-state output in 2027, which could obsolete current gigafactory capacity without timely retooling. Recyclers such as Sumitomo Metal Mining integrate upstream into cathode supply, capturing margin as circular-economy rules tighten. Component oligopolies in separators and electrolytes give material suppliers like Asahi Kasei pricing power, shifting differentiation upstream.

Strategic alliances proliferate. Honda joined GS Yuasa to co-develop high-nickel NMC for 2027 EV launches, and Envision AESC invests in a 30 GWh Ibaraki plant to supply Nissan, Renault, and Mercedes-Benz. Competitive intensity will sharpen once solid-state volumes rise, but firms with deep material science capabilities and recycling integration hold structural advantages in the Japan Lithium-ion Battery market.

Japan Lithium-ion Battery Industry Leaders

Panasonic Energy

Prime Planet Energy & Solutions

GS Yuasa International

Envision AESC

Toshiba Corporation (SCiB)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Japan Post launched a JPY 40 billion program to electrify 10,000 delivery vehicles by 2028.

- November 2025: Toyota and Idemitsu Kosan opened a sulfide solid-state electrolyte pilot line in Aichi Prefecture, planning 10 tons of annual output by 2027.

- November 2024: Honda opened a solid-state demonstration line in Sakura City, producing 1,000 cells per month for testing.

- September 2024: Panasonic Energy committed JPY 80 billion to double 4680 cylindrical cell capacity at its Wakayama plant by fiscal 2027, targeting 10 GWh annual output.

Japan Lithium-ion Battery Market Report Scope

Lithium-ion is one of the most popular rechargeable batteries. Lithium-ion batteries power commonly used devices, like mobile phones, electric vehicles, and various other devices. Lithium-ion batteries consist of single or multiple lithium-ion cells and a protective circuit board. They are referred to as batteries once the cell, or cells, are installed inside a device with a protective circuit board.

The Japan lithium-ion battery market is segmented by product type, form factor, power capacity, and end-use industry. By product type, the market is segmented into LCO, LFP, NMC, NCA, LMO, and LTO. By form factor, the market is divided into cylindrical, prismatic, and pouch. By end-user industry, the market is segmented into automotive, consumer electronics, industrial and power tools, stationary energy storage, aerospace and defense, and marine. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion) for all the above segments.

| Lithium Cobalt Oxide (LCO) |

| Lithium Iron Phosphate (LFP) |

| Lithium Nickel Manganese Cobalt (NMC) |

| Lithium Nickel Cobalt Aluminium (NCA) |

| Lithium Manganese Oxide (LMO) |

| Lithium Titanate (LTO) |

| Cylindrical |

| Prismatic |

| Pouch |

| Up to 3,000 mAh |

| 3,000 to 10,000 mAh |

| 10,000 to 60,000 mAh |

| Above 60,000 mAh |

| Automotive (EV, HEV, PHEV) |

| Consumer Electronics |

| Industrial and Power Tools |

| Stationary Energy Storage |

| Aerospace and Defense |

| Marine |

| By Product Type | Lithium Cobalt Oxide (LCO) |

| Lithium Iron Phosphate (LFP) | |

| Lithium Nickel Manganese Cobalt (NMC) | |

| Lithium Nickel Cobalt Aluminium (NCA) | |

| Lithium Manganese Oxide (LMO) | |

| Lithium Titanate (LTO) | |

| By Form Factor | Cylindrical |

| Prismatic | |

| Pouch | |

| By Power Capacity | Up to 3,000 mAh |

| 3,000 to 10,000 mAh | |

| 10,000 to 60,000 mAh | |

| Above 60,000 mAh | |

| By End-use Industry | Automotive (EV, HEV, PHEV) |

| Consumer Electronics | |

| Industrial and Power Tools | |

| Stationary Energy Storage | |

| Aerospace and Defense | |

| Marine |

Key Questions Answered in the Report

What is the projected value of the Japan Lithium-ion Battery market in 2031?

It is forecast to reach USD 16.39 billion, underpinned by an 11.17% CAGR.

Which segment is growing fastest within Japan's battery chemistry mix?

Lithium Titanate is expanding at a 19.8% CAGR by meeting industrial needs for long cycle life.

How are virtual power plants influencing domestic battery demand?

VPP programs let aggregated batteries earn dual revenue streams, cutting payback to under seven years and lifting stationary storage adoption.

What share did prismatic cells hold in 2025?

Prismatic cells accounted for 50.4% of domestic shipments, reflecting their dominance in automotive packs.

Why is recycling seen as strategic for Japanese cell makers?

Mandatory 50% recycling targets by 2030 and 10-15% lower costs for recycled metals improve margin resilience against raw-material volatility.

Page last updated on: