Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

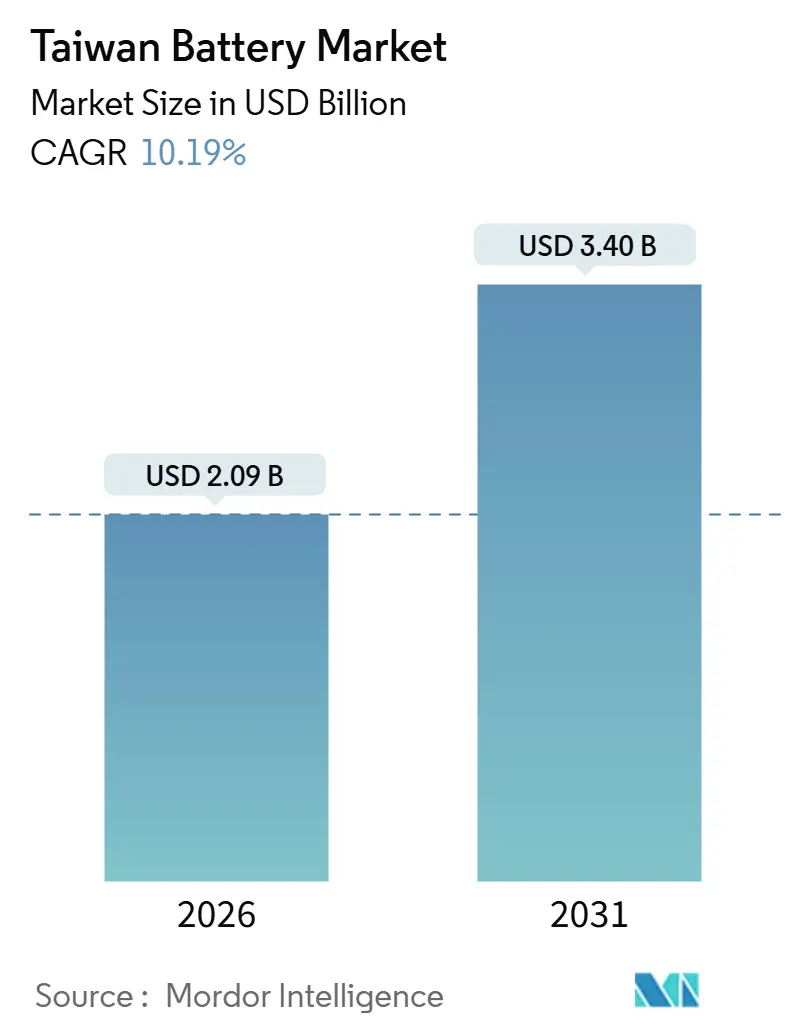

| Market Size (2026) | USD 2.09 Billion |

| Market Size (2031) | USD 3.40 Billion |

| Growth Rate (2026 - 2031) | 10.19% CAGR |

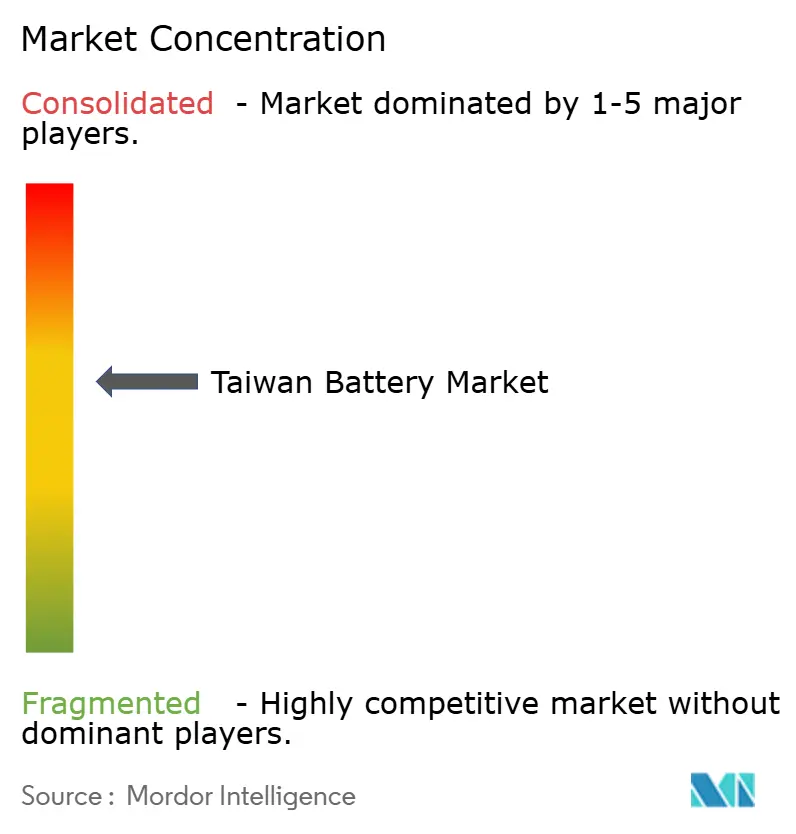

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Battery Market Analysis by Mordor Intelligence

The Taiwan Battery Market size is estimated at USD 2.09 billion in 2026, and is expected to reach USD 3.40 billion by 2031, at a CAGR of 10.19% during the forecast period (2026-2031).

Taiwan’s pivot from mature lead-acid production toward lithium-ion and solid-state chemistries is reshaping domestic supply chains, encouraged by aggressive electric-vehicle (EV) adoption targets and Taipower’s escalating grid-storage procurements. Contract manufacturers, once focused on consumer electronics, are redirecting capital toward automotive-grade modules, while local recycling pilots seek to offset the island’s 85% reliance on imported lithium and cobalt precursors. Rising power-availability quotas and stringent environmental standards are steering new investment into premium niches, solid-state cells for high-end EVs, and vanadium-redox flow batteries for long-duration grid support, where Taiwan can compete on quality rather than cost. Collectively, these trends signal that the Taiwan battery market will grow not only in volume but also in technological sophistication, anchoring the island’s broader energy-transition agenda.

Key Report Takeaways

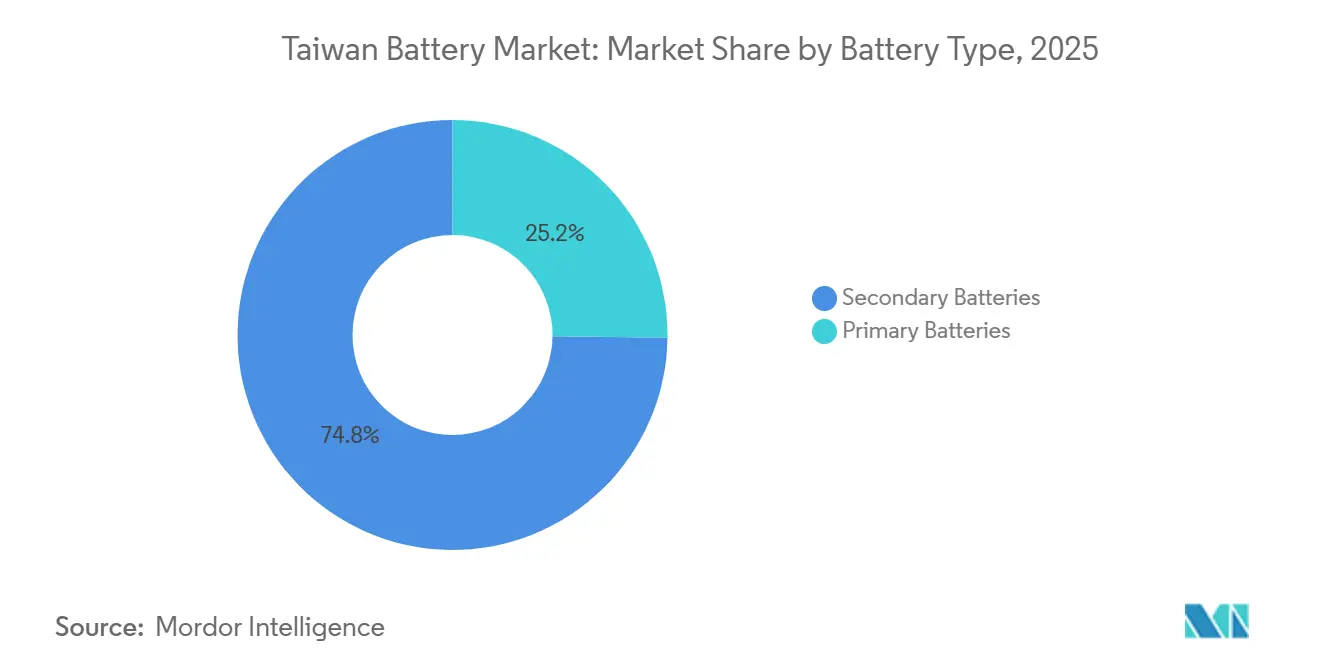

- By battery type, secondary rechargeable batteries held 74.8% of the Taiwan battery market share in 2025, and the segment is forecast to expand at a 14.8% CAGR through 2031.

- By technology, lithium-ion commanded 60.1% revenue share in 2025, while flow batteries are projected to record the fastest growth at 30.1% CAGR to 2031 as Taipower’s tenders reward long-duration assets.

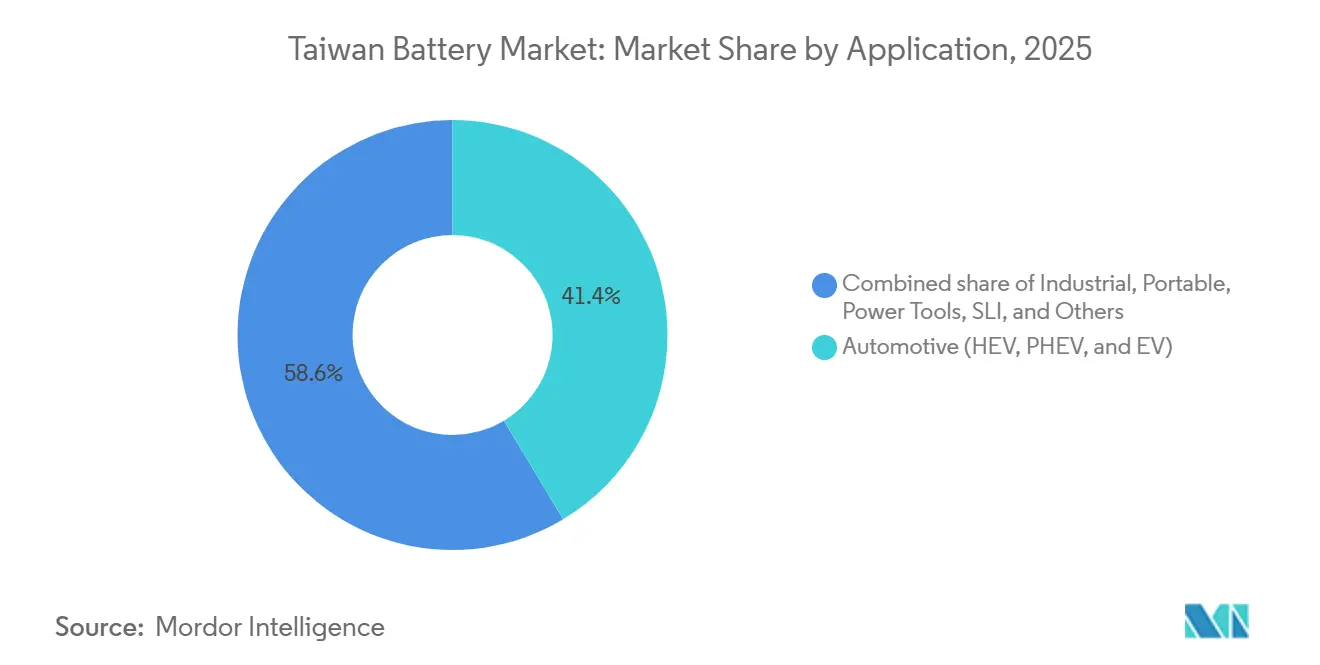

- By application, automotive batteries accounted for 41.4% of the Taiwan battery market size in 2025 and are advancing at a 15.3% CAGR on the back of Foxtron and Gogoro platform scale-ups.

- Gogoro’s battery-swapping network captured 92% of Taiwan’s two-wheeler EV segment in 2024, underscoring the platform’s first-mover advantage and reinforcing network effects that deter late entrants.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Taiwan Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV-led demand for high-energy lithium-ion packs | +2.8% | National, with concentration in Taoyuan, Kaohsiung manufacturing zones | Medium term (2-4 years) |

| Accelerating grid-scale storage tenders from Taipower | +2.1% | National, prioritizing western coastal industrial corridors | Short term (≤ 2 years) |

| Government "Green Battery Made-in-Taiwan" subsidy scheme (2025-2028) | +1.6% | National, targeting firms with >50% local value-added content | Short term (≤ 2 years) |

| OEM-level localisation push by Apple & Asus for battery modules | +1.2% | Northern Taiwan (Taipei, Taoyuan, Hsinchu tech corridors) | Medium term (2-4 years) |

| Commercial adoption of solid-state R&D spin-offs (ITRI, TDK-CPT JV) | +1.4% | National, with pilot lines in Taoyuan and Tainan science parks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging EV-Led Demand for High-Energy Lithium-Ion Packs

Government rebates of up to TWD 70,000 for battery-electric cars and a 2035 gasoline-scooter sunset are accelerating EV registrations. Foxtron’s Model T sedan entered pilot production in late 2024, sourcing modules from a 2 GWh Kaohsiung line that blends imported CATL cells with locally engineered thermal-management systems. This hybrid localization model lets Foxconn badge vehicles “Made in Taiwan” while sidestepping the capital burden of cathode synthesis. Gogoro’s 640,000 subscribers generated USD 310.5 million in revenue in 2024, proving that energy-as-a-service monetizes utilization more predictably than one-time vehicle sales.[1]Gogoro Investor Relations, “2024 Annual Report,” investor.gogoro.com The firm’s Enel X alliance aggregates swapped batteries into a virtual power plant, foreshadowing dual-use mobility and grid services. ProLogium’s fourth-generation solid-state cell, launched in December 2025, delivers 321 Wh/kg and charges to 80% in 12 minutes, narrowing the performance gap with premium Japanese and European tiers.[2]Bloomberg Newsroom, “ProLogium’s Solid-State Bet Reshapes Taiwan Battery Outlook,” bloomberg.com

Accelerating Grid-Scale Storage Tenders from Taipower

Taipower awarded 120 MW of battery-storage contracts in 2024 under its E-dReg ancillary-service program, paying up to TWD 1,200 per MWh for sub-second response times.[3]Taiwan Power Company, “E-dReg Ancillary Service Tender Results 2024,” taipower.com.tw Projects in Longtan and Dongshan deploy 165 MWh of capacity that stabilizes the grid as intermittent solar tops 10 GW. Delta Electronics and Innolux installed a 40 MW system at Southern Taiwan Science Park in May 2025, combining retired display-fab cells with new lithium-iron-phosphate packs, illustrating a cascading-use model that cuts capital bills by extending battery life. Formosa Smart Energy commissioned a recycling pilot recovering 92% of cathode material in July 2025, a move aimed at insulating producers from lithium-carbonate price spikes. Mandatory co-located storage for new renewables further ring-fences demand for domestic suppliers.

Government “Green Battery Made-in-Taiwan” Subsidy Scheme

The Ministry of Economic Affairs earmarked TWD 12 billion through 2028 to reimburse up to 30% of capital equipment for battery firms achieving ≥50% local value-added content. ProLogium secured TWD 1.8 billion in March 2025, enabling expansion from 2 GWh to 5 GWh of solid-state capacity by 2027 and a ceramic-electrolyte pilot line. Subsidies cover cathode-precursor reactors, anode-coating tools, and formation cyclers, but are disbursed against quarterly production audits that have slowed smaller applicants. ITRI and Largan Precision scaled titanium-niobium-oxide output toward 600 tons by 2026, supplying 1.5 GWh of fast-charging anodes. Policy emphasis on advanced materials over commodity cells signals Taiwan’s bid for high-margin niches where Chinese scale advantages erode.

OEM-Level Localization Push by Apple and Asus

Apple’s 2024 Supplier Responsibility Report added three Taiwan module assemblers to its approved list, diversifying away from Guangdong supply chains constrained by U.S. export controls. Simplo lifted renewable-energy usage to 80% via 10.8 MW of rooftop solar, aligning with Apple’s 2030 Scope 3 neutrality goal. Dynapack’s 2024 revenue fell 19% to TWD 13.91 billion, prompting a pivot toward data-center backup units where lithium-ion is displacing lead-acid on cycle-life grounds. Asus formed eMobility & Energy Solutions to embed proprietary battery-management code in gaming laptops, signaling that module-level intelligence is an emerging differentiator. Collectively, OEM localization drives incremental demand for Taiwan battery market modules integrated with advanced software stacks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material concentration risk: >85% Li-ion precursor imported | -1.5% | National, affecting all lithium-ion cell producers | Medium term (2-4 years) |

| Tight power-availability quota for new giga-scale plants | -1.1% | National, most acute in central and southern industrial zones | Short term (≤ 2 years) |

| High recycling cost versus mainland China | -0.7% | National, constraining closed-loop business models | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Concentration Risk

Taiwan sources more than 85% of lithium-carbonate, cobalt-sulfate, and nickel-sulfate from Chinese refiners, exposing producers to geopolitical risk as Beijing tightens critical-mineral export licenses.[4]International Energy Agency, “Critical Minerals Market Review 2025,” iea.org A 2025 stockpile mandate requiring 90 days of inventory lifts working-capital needs by nearly 20% and weighs heavier on small firms lacking trade-finance access. Recycling pilots recover 92% of cathode material but remain sub-scale because the island’s EV fleet is still nascent. Until direct procurement deals with Australian or Chilean suppliers mature, the Taiwan battery market will remain a price-taker in volatile raw-material cycles.

Tight Power-Availability Quota for New Giga-Scale Plants

Summer peak demand from chip fabs and data centers leaves minimal grid headroom, forcing battery projects into multiyear connection queues. ProLogium’s 161 kV substation took 18 months to commission, delaying the Taoyuan expansion to Q2 2026. Renewable-energy compliance rules require new industrial users to source 10% green power by 2026, rising to 20% by 2030, but land scarcity pushes firms toward costly offshore-wind PPAs priced around TWD 5.1 per kWh, roughly double the grid average. Smaller assemblers unable to underwrite long-term power contracts are relocating to Southeast Asia, draining potential capacity from the Taiwan battery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeable Cells Eclipse Disposable Formats

Secondary rechargeable batteries controlled 74.8% of the Taiwan battery market share in 2025 and are forecast to expand at a 14.8% CAGR to 2031. Robust growth stems from mobility electrification, grid-storage mandates, and the phase-out of lead-acid starter batteries in commercial fleets. Gogoro’s subscription model demonstrates that recurring utilization revenue can surpass the value of disposable sales, drawing interest from utilities and ride-sharing operators alike. Meanwhile, primary batteries comprised 25.2% of 2025 revenue but face a secular decline as USB-C charging and sealed-back designs remove user-replaceable compartments.

Policy signals reinforce the transition: Taiwan’s subsidy scheme excludes primary-cell makers, while extended-producer-responsibility fees under the Waste Disposal Act penalize single-use formats. ProLogium’s solid-state roadmap targets 3,000-cycle durability and shelf life that narrows historic advantages enjoyed by primaries, further eroding their addressable demand. As recycling pilots mature, closed-loop economics will favor chemistries amenable to material recovery, adding structural momentum to rechargeable adoption across the Taiwan battery market.

By Technology: Lithium-Ion Leads, Flow Batteries Accelerate

Lithium-ion technologies accounted for 60.1% of 2025 revenue, reflecting entrenched positions in EVs, consumer electronics, and short-duration grids. Yet flow batteries are projected to expand at a 30.1% CAGR, the fastest rate among chemistries, because Taipower’s tenders prioritize four-hour discharge under its ancillary-service framework. The Taiwan battery market size for flow systems is expected to climb sharply once vanadium-redox suppliers secure local electrolyte sourcing.

Solid-state remains in pilot but notable: ProLogium shipped 500,000 cells in 2024 and plans to triple capacity by 2027, targeting premium segments where safety and fast-charging matter more than unit cost. Hybrid deployments, such as Delta’s lithium-iron-phosphate plus second-life-cell configuration, illustrate capital-efficient ways to match duty cycle with chemistry. Lead-acid persists for low-rate backup, but its share declines each year as lithium-ion’s cost curve sinks below USD 100 per kWh, a milestone the island’s assemblers aim to reach by 2028.

By Application: Automotive Leads, Industrial Storage Gains Momentum

Automotive platforms generated 41.4% of 2025 revenue and are forecast to grow at 15.3% CAGR through 2031, supported by Foxtron’s 2 GWh local module line and Gogoro’s nationwide swap network. Foxtron’s hybrid localization balances cost and branding, while Gogoro’s Enel X virtual-plant tie-up turns mobility assets into grid resources, reinforcing demand for swappable packs.

Industrial storage ranks second, propelled by Taipower’s 120 MW awards and factory micro-grids that hedge against brownouts. Delta and Innolux’s 40 MW project showcases how retired display batteries extend life in stationary roles. Portable consumer electronics face slowing growth as energy-efficient processors dampen capacity needs, causing Dynapack to diversify into telecom backup units. Power-tool and SLI segments remain niche or in decline, together representing less than 10% of the Taiwan battery market.

Geography Analysis

Manufacturing clusters around Taoyuan–Hsinchu in the north, Taichung in the center, and Kaohsiung–Tainan in the south. ProLogium’s 2 GWh solid-state complex and Simplo’s laptop-battery lines anchor the northern corridor, supported by ITRI’s materials labs at Hsinchu Science Park. Southern Kaohsiung hosts Foxtron’s module line and Formosa Smart Energy’s lithium-iron-phosphate plant plus recycling pilot, offering proximity to petrochemical feedstocks. Central Taichung remains smaller but benefits from electronics subcontractor networks that feed automotive harness suppliers.

Cluster advantages - skilled labor, precision tooling, and seaport access - offset higher electricity tariffs yet also magnify exposure to grid bottlenecks during summer demand spikes.

Competitive Landscape

Roughly 20 players vie in a moderately fragmented field where no company exceeds 15% share. ProLogium leads solid-state commercialization, extracting 30-40% price premiums from safety-critical segments. Gogoro controls 92% of two-wheeler battery swapping, leveraging dense station networks and a subscriber lock-in that deters new entrants. Simplo and Dynapack defend portable-electronics franchises by greening power supply and diversifying into data-center modules.

Material localization represents an emerging battleground: ITRI–Largan’s titanium-niobium-oxide joint venture aims to displace Chinese graphite, while Formosa Smart Energy’s recycling pilot seeks to close the LFP loop. The government’s subsidy scheme lowers entry barriers, enticing foreign OEMs to establish Taiwan lines if they meet 50% value-added thresholds. Nevertheless, high grid tariffs and power-quota hurdles constrain mass-market cell projects, nudging the Taiwan battery industry toward specialty chemistries where R&D depth and stringent quality standards create defensible moats.

Taiwan Battery Industry Leaders

E-One Moli Energy (Molicel)

Dynapack International

Kung Long Batteries

Amita Technologies

Simplo Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Saft has secured a contract with Foxwell Power (FWP), an energy trading company, to provide a battery storage solution for a 356MWh project in Taiwan.

- August 2025: ProLogium Technology, a global frontrunner in solid-state battery innovation, unveiled its latest 4th-generation Superfluidized All-Inorganic Solid-State Lithium Ceramic Battery and detailed its strategic roadmap for large-scale commercialization.

- March 2025: Formosa Smart Energy Tech Corporation (FSET) has completed and commenced mass production at its 2.1GWh battery cell and module plant in Changhua Coastal Industrial Park. The plant, built with an investment exceeding tens of billions of NTD, is now the largest lithium iron phosphate (LFP) battery cell production base in Taiwan.

Taiwan Battery Market Report Scope

A battery can be defined as an electrochemical device (consisting of one or more electrochemical cells) that can be charged with an electric current and discharged whenever required. Batteries are usually devices that are made up of multiple electrochemical cells that are connected to external inputs and outputs.

The Taiwan battery market is segmented by battery type, technology, and application. By battery type, the market is segmented into primary batteries and secondary batteries. By technology, the market is segmented into lead-acid, Li-ion, nickel-metal hydride, nickel-cadmium, sodium-sulfur, solid-state, flow battery, and emerging chemistries. By application, the market is segmented into automotive, industrial, portable, power tools, SLI, and other applications. For each segment, market sizing and forecasts have been done based on revenue (USD).

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications |

Key Questions Answered in the Report

How fast is the Taiwan battery market expected to grow through 2031?

It is forecast to expand from USD 2.09 billion in 2026 to USD 3.40 billion by 2031, advancing at a 10.19% CAGR.

Which segment contributes the most revenue today?

Automotive platforms generated 41.4% of 2025 revenue, led by Foxtron sedans and Gogoro's scooter battery-swapping network.

What technology is growing fastest in Taiwan's storage sector?

Vanadium-redox and other flow batteries are projected to rise at a 30.1% CAGR because Taipower's tenders reward long-duration discharge.

How dependent is Taiwan on imported battery materials?

More than 85% of lithium-ion precursors (lithium, cobalt, and nickel compounds) are imported, mostly from China.

What government support exists for local battery manufacturing?

The "Green Battery Made-in-Taiwan" scheme reimburses up to 30% of capital costs for firms achieving at least 50% local value-added content through 2028.

Which company dominates two-wheeler battery swapping in Taiwan?

Gogoro holds 92% of the segment, serving 640,000 subscribers with its island-wide network of swap stations.

Page last updated on: