Japan Flash Memory Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.16 Billion |

| Market Size (2026) | USD 3.25 Billion |

| Market Size (2031) | USD 3.75 Billion |

| Growth Rate (2026 - 2031) | 2.90% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Flash Memory Market Analysis by Mordor Intelligence

Japan flash memory market size in 2026 is estimated at USD 3.25 billion, growing from 2025 value of USD 3.16 billion with 2031 projections showing USD 3.75 billion, growing at 2.90% CAGR over 2026-2031. Government incentives, a disciplined capacity-expansion roadmap, and the migration of data-center and automotive workloads to high-performance solid-state storage underpin this steady climb. At the same time, cyclical pricing swings and rising energy costs temper near-term profitability, especially for fab operators exposed to spot NAND quotations. Technology leadership in 218-layer and higher 3D NAND nodes enables cost reduction that offsets part of the pricing pressure, while emerging non-volatile memory formats such as MRAM begin to capture industrial sockets that demand extreme endurance. Vertically integrated producers that own both wafer output and module assembly secure better margins than pure-play assemblers. As a result, the Japan flash memory market continues to consolidate around a handful of scale players that can fund the transition to 300-layer architectures.

Key Report Takeaways

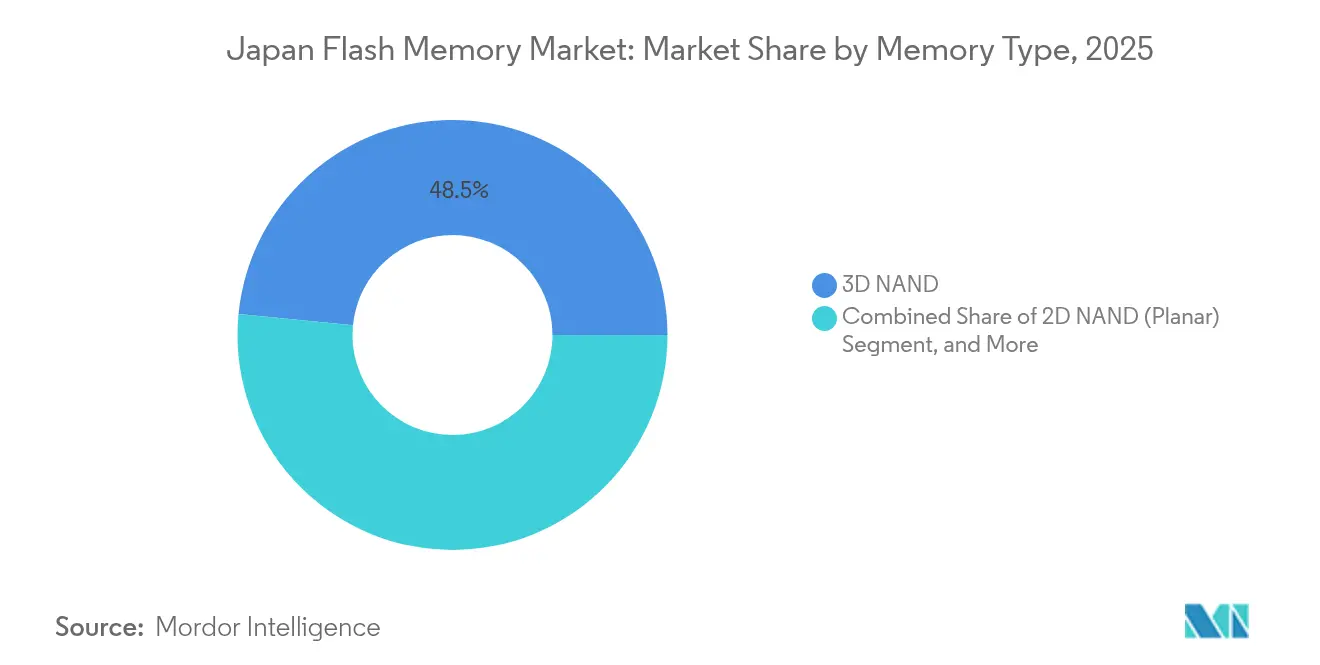

- By memory type, 3D NAND led with 48.45% of the Japan flash memory market share in 2025 while emerging MRAM and other non-volatile memories are forecast to post the fastest growth at a 4.05% CAGR to 2031.

- By density, the 64 Gb–256 Gb band accounted for 37.15% of revenue in 2025 of the Japan flash memory market; the 512 Gb-and-above tier is set to expand at a 3.62% CAGR through 2031.

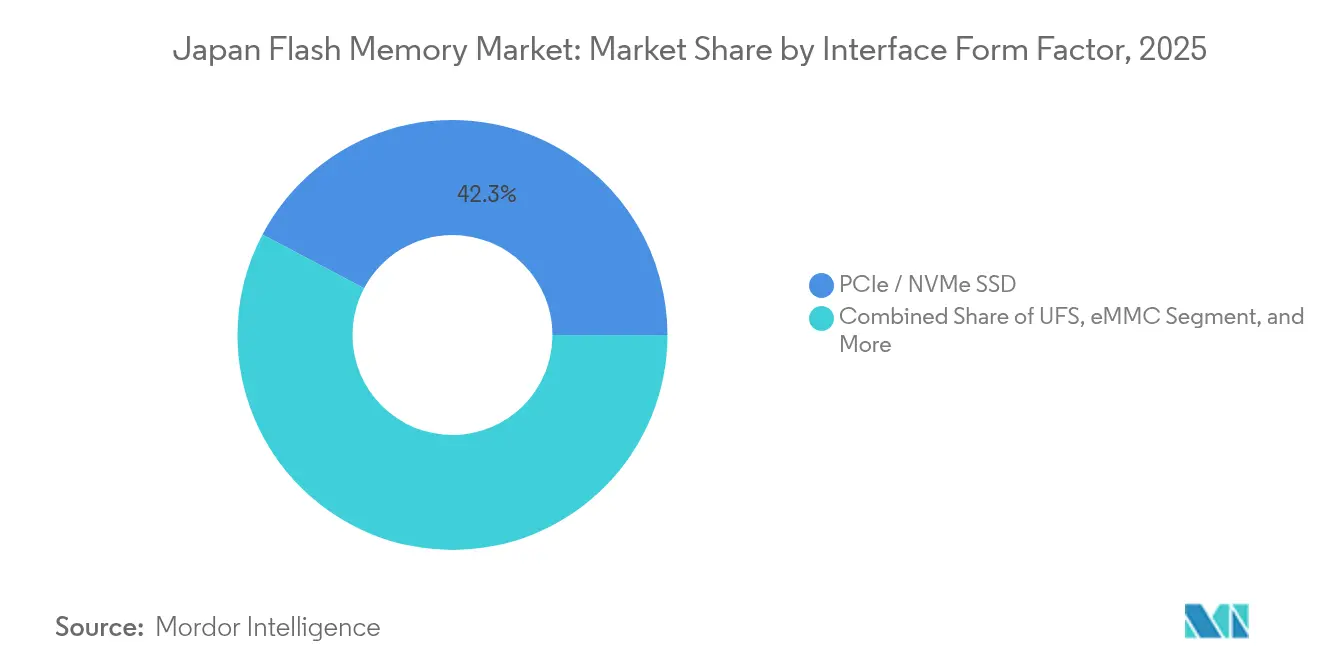

- By interface, PCIe/NVMe SSDs captured 42.25% revenue share in 2025 of the Japan flash memory market, and Universal Flash Storage is projected to rise at a 3.90% CAGR on accelerating automotive uptake.

- By end user, mobile and tablets held 38.20% revenue in 2025 of the Japan flash memory market, while automotive applications are projected to grow at a 3.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Flash Memory Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging adoption of SSDs in consumer and enterprise PCs | +0.6% | Kanto, Kansai (enterprise hubs) | Medium term (2-4 years) |

| Expanding smartphone production with higher on-board storage | +0.5% | Kanto, Kansai (design centers), Kyushu (assembly) | Short term (≤ 2 years) |

| Rapid growth of automotive ADAS and in-vehicle infotainment | +0.7% | Chubu, Kyushu (automotive clusters) | Long term (≥ 4 years) |

| Proliferation of IoT edge devices needing local flash storage | +0.4% | National, with concentration in Kanto industrial zones | Medium term (2-4 years) |

| Government incentives for domestic advanced-flash fabs | +0.5% | Tohoku, Kyushu, Hokkaido (fab sites) | Long term (≥ 4 years) |

| 3D NAND use in metaverse-related Japanese wearables | +0.2% | Kanto (Tokyo metro), Kansai (Osaka metro) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of SSDs in Consumer and Enterprise PCs

Enterprise refresh cycles are shifting decisively toward NVMe storage, which delivers single-digit microsecond latency, thereby reducing rack footprints and power draw in data center clusters located in Tokyo and Osaka.[1]Western Digital Newsroom, “Western Digital Introduces New Datacenter SSD Portfolio Built on 218-Layer BiCS Flash,” westerndigital.com Notebook makers are mirroring this shift as PCIe Gen4 drives become mainstream in mid-range systems. Western Digital’s 218-layer BiCS devices now ship in volume, providing 3 drive writes per day endurance for finance and public-sector workloads. Consumer adoption is accelerating as the 5G rollout drives the need for local caching in routers and base stations. Together, these factors add 0.6 percentage points to overall growth, with peak influence expected between 2026 and 2028.

Expanding Smartphone Production with Higher On-Board Storage

Premium handsets from Sony, Sharp, and Kyocera feature 256 GB and 512 GB storage, enabling 4K video capture and AI-driven imaging.[2]Sony Press Team, “Xperia 1 VI Launch Product Specifications and Features,” sony.com Apple retains a commanding share, but local brands keep niche segments that value ruggedization and high-resolution cameras. Fifth-generation wireless penetration already covers more than half the subscriber base, driving photo and video file sizes higher. These trends deliver a 0.5 percentage-point uplift to the long-term CAGR.

Rapid Growth of Automotive ADAS and In-Vehicle Infotainment

Domestic automakers integrate Level 2+ driver-assistance suites that buffer lidar, radar, and camera data locally on flash modules certified to AEC-Q100 standards. Kioxia’s UFS 4.0 devices supply 4,200 MB/s read throughput, enabling real-time sensor fusion.[3]Kioxia Technical Briefs, “BiCS Flash Roadmap and Market Outlook,” kioxia.com Infotainment head units shift from 32 GB eMMC to 128 GB UFS to accommodate over-the-air map updates and high-definition cockpit displays. The automotive pivot contributes 0.7 percentage points to market expansion and extends beyond 2028 as semi-autonomous functions become widespread.

Government Incentives for Domestic Advanced-Flash Fabs

Tokyo allocated JPY 243 billion in direct subsidies to the Kioxia-Western Digital venture and lined up another JPY 150 billion for next-generation memory R&D.[4]METI, “Comprehensive Semiconductor Strategy,” meti.go.jp Micron committed JPY 500 billion to its Hiroshima site, anchoring a new regional supply cluster. These incentives lower effective capital intensity, allow Japanese fabs to match Korean layer counts, and add 0.5 percentage points to the growth trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclical NAND price volatility and inventory gluts | -0.5% | National, affecting all fab operators | Short term (≤ 2 years) |

| Reliability challenges at sub-1z-nm nodes | -0.3% | Kanto, Kansai (R&D centers), Tohoku (pilot lines) | Medium term (2-4 years) |

| High domestic energy costs pressuring fab economics | -0.4% | National, acute in Kyushu and Tohoku | Long term (≥ 4 years) |

| Supply risk of high-purity HF and photo-resist chemicals | -0.2% | National, with upstream concentration in Chubu and Kanto | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyclical NAND Price Volatility and Inventory Gluts

Contract prices fell 6.2% quarter on quarter in 4Q 2024 and are forecast to dip another 10-15% in 1Q 2025 before a modest rebound. Fab operators face margin compression just as new capacity ramps. Kioxia flagged 90 days of inventory in its IPO prospectus, exposing it to further markdowns. This pricing whiplash subtracts 0.5 percentage points from the projected CAGR and complicates cash-flow planning through 2026.

High Domestic Energy Costs Pressuring Fab Economics

Japan’s grid relies on imported liquefied natural gas, pushing electricity tariffs above those of peer manufacturing hubs. Kioxia alone consumes more than 1 TWh annually across its Yokkaichi and Kitakami sites, prompting the company to set a target of sourcing 30% renewable power by 2030. Micron’s Hiroshima expansion will add another 200 MW load to regional transmission networks. Elevated energy costs shave 0.4 percentage points from growth through the forecast horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Type: 3D NAND Consolidates, MRAM Accelerates

3D NAND captured 48.45% revenue in 2025 on the back of data-center conversions to all-flash arrays and automotive adoption of UFS 4.0 modules. This share anchors the Japan flash memory market through the forecast, with density scaling beyond 218 layers keeping average selling prices competitive. Samsung and SK hynix push toward 300-layer devices, putting cost pressure on incumbents yet widening the total addressable pool as terabyte-class packages proliferate.

Other non-volatile technologies, chiefly MRAM and ReRAM, are forecast to expand at a 4.05% CAGR as automotive and industrial equipment require instant-on capability and million-cycle endurance. Kioxia’s OCTRAM crosspoint design, co-developed with SK hynix, underpins this surge. NOR and planar NAND linger in legacy designs but cede ground as vertical stacking shrinks die costs. These dynamics keep the Japan flash memory market diversified yet tilted toward 3D structures over the forecast window.

By Density: 512 Gb-Plus Tiers Climb

The 64 Gb–256 Gb class held 37.15% revenue in 2025, tied to smartphone bills of materials that favor 128 GB and 256 GB capacities. Rising photo and video file sizes, combined with carrier bundling of unlimited data, nudge consumers toward higher SKUs.

The 512 Gb-and-above bracket is projected to grow at a 3.62% CAGR, lifting the Japan flash memory market size for this density group as AI edge devices and ADAS platforms embed 1 TB storage modules. Kioxia’s new 2 Tb QLC die enables single-package 1 TB UFS parts, accelerating the migration. Lower-density tiers remain vital for microcontrollers and IoT sensors where energy efficiency and tiny footprints outweigh raw capacity.

By Interface / Form Factor: UFS Gains Traction

PCIe/NVMe SSDs delivered 42.25% revenue in 2025 thanks to enterprise rollouts that prioritize throughput and latency. Japan’s hyperscalers retired SATA enclosures in favor of Gen4 and Gen5 NVMe units, locking in performance headroom for AI inference.

Universal Flash Storage is forecast to log the fastest interface growth at 3.90% CAGR as automotive platforms mandate high-speed managed flash with automotive-grade temperature tolerance. eMMC persists in cost-sensitive IoT endpoints, while SATA fades except for niche industrial refreshes. These trends force controller vendors to integrate both NVMe and UFS host compliance into future chipsets, broadening serviceable applications for the Japan flash memory market.

By End User Application: Automotive Outpaces Handsets

Smartphones and tablets accounted for 38.20% of the revenue in 2025, supported by steady premium phone refreshes. The Japan flash memory market size allocated to automotive is, however, forecast to expand at a 3.82% CAGR between 2026 and 2031, overtaking client PCs as the second-largest consumption vertical.

Level 2+ ADAS systems cache multi-sensor data locally, while infotainment head units store HD maps and OTA firmware. Data centers absorb the highest endurance SSDs to serve AI inference workloads that demand a consistent quality of service. Industrial and IoT nodes continue to specify eMMC and low-density UFS where absolute reliability is paramount.

Geography Analysis

Kanto remains the largest contributor to the Japan flash memory market, anchored by Tokyo’s concentration of headquarters and research labs for Kioxia, Sony Semiconductor, and Renesas. Western Digital maintains a major architecture center in Yokohama, collaborating with Kioxia on CXL-enabled memory fabrics. Shin-Etsu expands photoresist output in nearby Gunma, guaranteeing material supplies for local fabs. This cluster effect compresses design-cycle times and sustains the region’s leadership position.

Kyushu is expected to be the fastest-growing area through 2030. TSMC’s Kumamoto facility has already begun production of 28 nm and 16 nm nodes and plans to build a second fab for 7 nm nodes by 2027. Kyushu also hosts photoresist and chemical producers that supply both JASM and Kioxia, creating a supply chain reminiscent of Taiwan’s Hsinchu hub. Proximity to Korean fabs shortens logistical lead times for wafer starts and die shipments.

Tohoku houses Tokyo Electron equipment plants and PSMC’s Sendai line for embedded flash microcontrollers. Chubu generates strong demand through Toyota, Honda, and Denso, which integrate UFS 4.0 modules into new ADAS architectures. Kansai supports Panasonic and Rohm with power-management device fabs embedding on-chip flash. Hokkaido prepares for Rapidus’ 2 nm logic facility adjacent to planned memory-packaging lines. Chugoku and Shikoku remain smaller contributors yet benefit from spillover as the Kyushu complex expands.

Competitive Landscape

Kioxia and Western Digital jointly operate Japan’s largest 3D NAND capacity at Yokkaichi and Kitakami, giving them scale advantages in die output and yield learning. Samsung and SK hynix defend technological leadership with 290-layer and 321-layer stacks, compelling local rivals to accelerate R&D spending. Micron’s Hiroshima expansion underscores a commitment to the Japan flash memory market and aims to win automotive and industrial sockets that prize endurance.

Renesas, Sony Semiconductor, and Panasonic focus on embedded flash for microcontrollers, image sensors, and specialized industrial modules, where reliability outweighs the cost of gigabytes. Controller designers Phison and Silicon Motion integrate AI-driven error correction, extending the life cycles of QLC-based SSDs and adding differentiation beyond raw NAND supply. Startups targeting MRAM and ReRAM exploit whitespace opportunities that require over one million-cycle endurance for factory automation workloads.

Regulatory subsidies reduce capital intensity but also heighten scrutiny on sovereign resilience and supply-chain security. The market structure favors vertically integrated players that can self-qualify wafers, controllers, and finished drives. Standards progress on UFS 4.0 and PCIe Gen5 accelerates commoditization at the interface layer, pushing value capture toward core IP in cell structure and firmware algorithms within the Japan flash memory market.

Japan Flash Memory Industry Leaders

Western Digital Corp

Micron Technology Inc.

Renesas Electronics Corporation

Kioxia Holdings Corporation

GigaDevice Semiconductor Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Kioxia’s corporate strategy meeting confirmed volume output of a 2 Tb QLC die that enables single-package 1 TB UFS parts, outlined a roadmap beyond 300 layers by 2027, and highlighted new partnerships with Toyota, Honda, and Subaru for next-generation sensor-fusion storage

- March 2025: Micron began volume production of 1γ-generation DRAM and NAND at its Hiroshima fab, allocating the first lots of high-bandwidth memory and automotive-grade flash to Toyota, Denso, and Sony for in-vehicle computing platforms and imaging systems

- February 2025: Western Digital and Kioxia launched a joint program to build CXL 3.0 memory modules that pair 218-layer BiCS Flash with controller logic, aiming to supply disaggregated-memory racks for Japanese hyperscalers NTT Data, Fujitsu, and NEC by late 2025

- January 2025: Samsung Electronics added ¥45 billion (USD 310 million) to its Yokohama R&D center, outfitting new cleanrooms and hiring 200 engineers who will develop automotive CMOS image sensors with embedded flash; engineering samples are scheduled for Honda and Nissan in the second half of 2025

Japan Flash Memory Market Report Scope

The Japan flash memory market report is segmented by Memory Type (3D NAND, 2D NAND, NOR Flash, Other Memory Type), Density (Up to 256 Mb, 512 Mb–2 Gb, 4 Gb–32 Gb, 64 Gb–256 Gb, 512 Gb and Above), Interface/Form Factor (eMMC, UFS, SATA SSD, PCIe/NVMe SSD, SPI NOR, USB Flash and Removables), End User Application (Data Center and Enterprise Servers, Mobile and Tablets, Automotive, Industrial and IoT Devices, Client Computing, Consumer Electronics, Other End User Application). The Market Forecasts are Provided in Terms of Value (USD).

| 3D NAND |

| 2D NAND (Planar) |

| NOR Flash |

| Other Memory Type |

| Up to 256 Mb |

| 512 Mb – 2 Gb |

| 4 Gb – 32 Gb |

| 64 Gb – 256 Gb |

| 512 Gb and Above |

| eMMC |

| UFS |

| SATA SSD |

| PCIe / NVMe SSD |

| SPI NOR |

| USB Flash and Removables |

| Data Center and Enterprise Servers |

| Mobile and Tablets |

| Automotive (ADAS, Infotainment) |

| Industrial and IoT Devices |

| Client Computing (PC, Laptop, Client SSD) |

| Consumer Electronics (Gaming, Wearables) |

| Other End User Application |

| By Memory Type | 3D NAND |

| 2D NAND (Planar) | |

| NOR Flash | |

| Other Memory Type | |

| By Density | Up to 256 Mb |

| 512 Mb – 2 Gb | |

| 4 Gb – 32 Gb | |

| 64 Gb – 256 Gb | |

| 512 Gb and Above | |

| By Interface / Form Factor | eMMC |

| UFS | |

| SATA SSD | |

| PCIe / NVMe SSD | |

| SPI NOR | |

| USB Flash and Removables | |

| By End User Application | Data Center and Enterprise Servers |

| Mobile and Tablets | |

| Automotive (ADAS, Infotainment) | |

| Industrial and IoT Devices | |

| Client Computing (PC, Laptop, Client SSD) | |

| Consumer Electronics (Gaming, Wearables) | |

| Other End User Application |

Key Questions Answered in the Report

How large is the Japan flash memory market in 2026?

The Japan flash memory market size reaches USD 3.25 billion in 2026 and is on track for USD 3.75 billion by 2031.

What is the expected CAGR for Japanese flash memory through 2031?

Aggregate revenue is projected to grow at a steady 2.90% CAGR across the 2026-2031 forecast window.

Which application is the fastest-growing consumer of flash memory in Japan?

Automotive electronics, especially Level 2+ ADAS and infotainment systems, are set to expand at a 3.82% CAGR to 2031.

Which interface technology is rising quickest in Japanese flash storage?

Universal Flash Storage is projected to grow at a 3.90% CAGR as automotive and mobile devices adopt UFS 3.1 and UFS 4.0 modules.

How are government incentives affecting domestic flash manufacturing?

Subsidies exceeding JPY 243 billion reduce capital intensity for new fabs and add 0.5 percentage points to long-term market growth.

Page last updated on: