Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

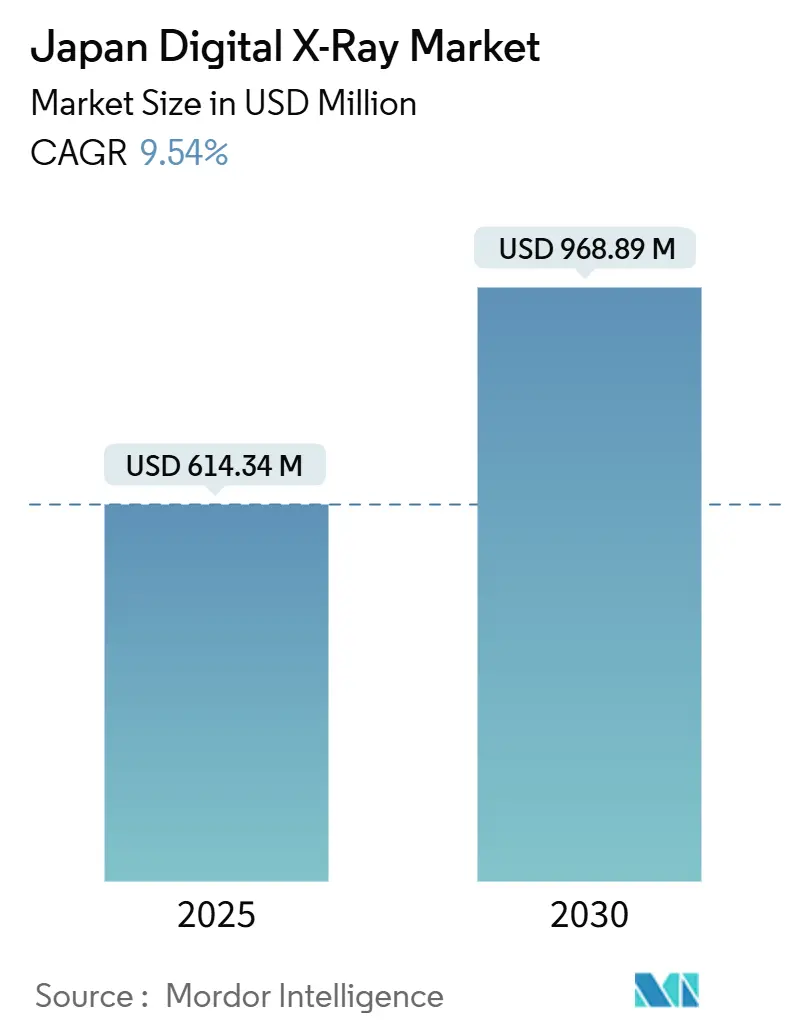

| Market Size (2025) | USD 614.34 Million |

| Market Size (2030) | USD 968.89 Million |

| Growth Rate (2025 - 2030) | 9.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Digital X-Ray Market Analysis by Mordor Intelligence

Japan digital X-ray market size stands at USD 614.34 million in 2025 and is projected to reach USD 968.89 million by 2030, registering a 9.54% CAGR. An unprecedented increase in the 65+ population, favorable reimbursement incentives, and rapid adoption of AI-enabled detectors are combining to lift Japan digital X-ray market growth across hospital, clinic, and mobile care settings. Fixed rooms remain the workhorse in high-volume urban hospitals, yet fast-growing hand-held systems and mobile vans are unlocking new opportunities in rural prefectures. CMOS panels are eroding amorphous silicon dominance as facilities look for lower dose, energy-efficient alternatives that fit carbon-neutral targets. Competitive dynamics favor vertically integrated Japanese manufacturers able to navigate supply-chain constraints in CsI scintillators and semiconductors while aligning with PMDA fast-track approval rules.

Key Report Takeaways

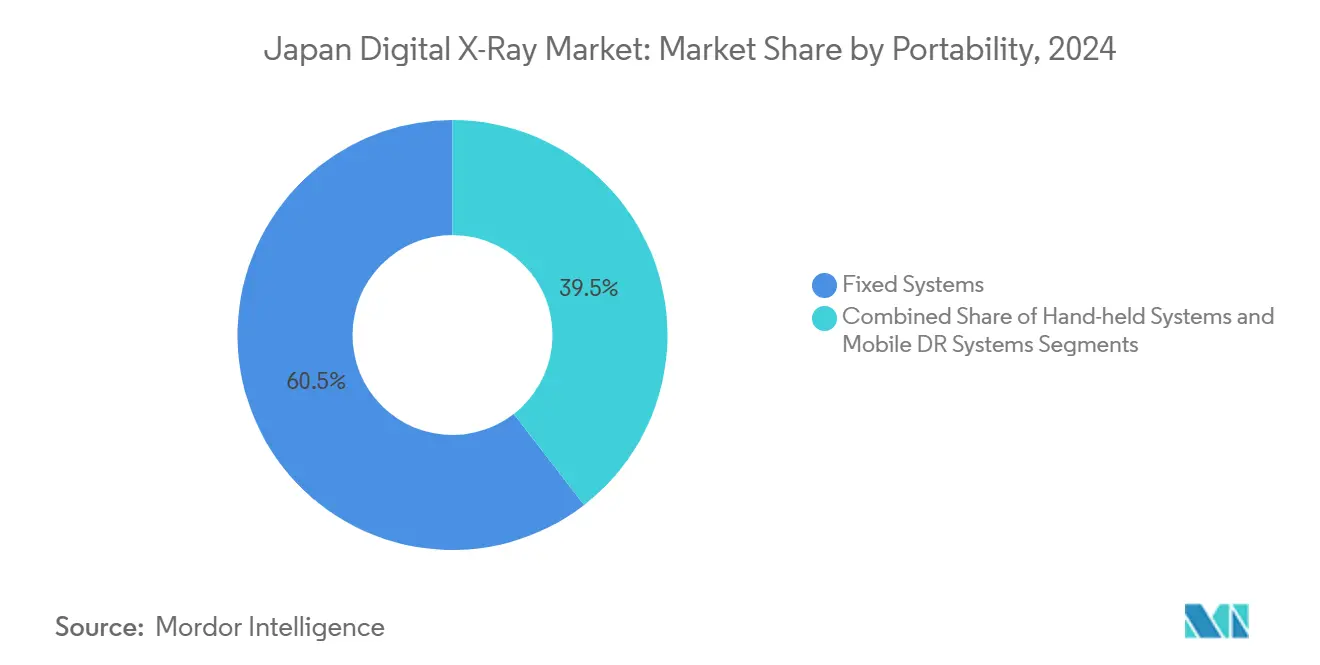

- By portability, fixed systems captured 60.55% of Japan digital X-ray market share in 2024, while hand-held systems are advancing at a 12.25% CAGR through 2030.

- By detector type, amorphous silicon panels held 45.53% of the Japan digital X-ray market size in 2024; CMOS detectors are forecast to expand at an 11.85% CAGR to 2030.

- By application, orthopedic imaging led with 28.63% revenue share in 2024, whereas dental imaging is predicted to grow at a 10.87% CAGR to 2030.

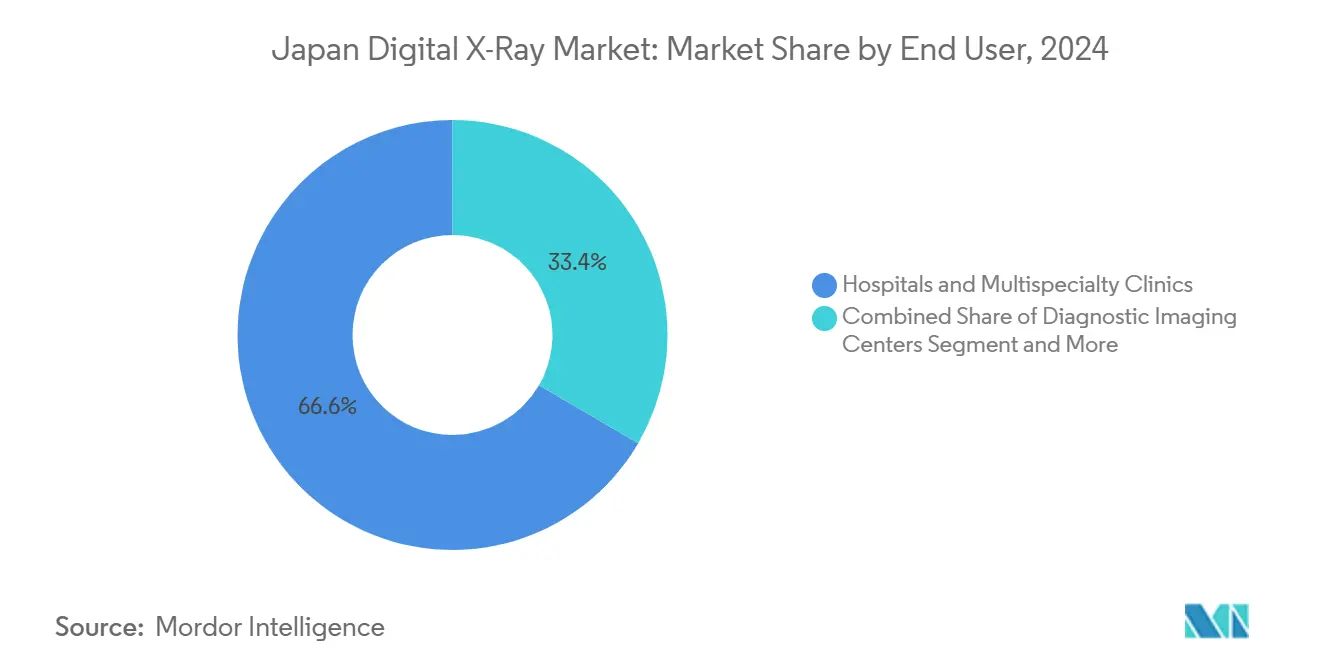

- By end user, hospitals and multispecialty clinics accounted for 66.63% share of the Japan digital X-ray market size in 2024, and mobile screening units are on course for an 11.07% CAGR through 2030.

Japan Digital X-Ray Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly aging population boosting imaging volumes | +2.1% | National, rural concentration | Long term (≥4 years) |

| Reimbursement incentives accelerating shift from CR to DR | +1.8% | National, early metropolitan uptake | Medium term (2-4 years) |

| AI-enabled workflow & dose-reduction innovations | +1.5% | Urban centers expanding to regions | Medium term (2-4 years) |

| Prefecture hospital-merger programs driving fleet renewal | +1.2% | Consolidating prefectures | Short term (≤2 years) |

| PMDA fast-track for AI imaging devices | +0.9% | National, academic medical centers | Short term (≤2 years) |

| Carbon-neutral hospital mandates favoring energy-efficient DR | +0.7% | Government hospitals nationwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapidly Aging Population Boosting Imaging Volumes

Japan’s 65+ cohort grew to 36 million in 2023 and is projected to reach 40 million by 2040, a shift that is lifting imaging utilization by 3.2-fold relative to younger cohorts. Orthopedic and chest examinations dominate the incremental demand, and the surge is especially acute in prefectures with half the specialist density seen in Tokyo. Rural clinics therefore depend heavily on Japan digital X-ray market solutions that deliver immediate images and minimal retakes. Without proportional staff growth, administrators are prioritizing automation, dose optimization, and PACS integration to maintain throughput. Collectively, these demographic pressures add 2.1 percentage points to the forecast CAGR for the Japan digital X-ray market.

Reimbursement Incentives Accelerating Shift from CR to DR

The FY 2024 medical fee revision introduced an 8-point “Medical DX promotion” add-on worth about JPY 80 per X-ray, subsidizing facilities that adopt EMR, e-prescribing, and digital imaging. The scheme rewards DR adoption while implicitly penalizing legacy CR, triggering accelerated replacement decisions ahead of March 2025 electronic prescription and September 2025 EMR compliance deadlines. Remote prefectures benefit from subsidies covering up to 60% of equipment costs. Facilities choosing AI-ready detectors can justify higher capital outlays by documenting shorter exam times and diagnostic gains. These incentives are expected to contribute 1.8 percentage points to the CAGR of the Japan digital X-ray market.

AI-Enabled Workflow & Dose-Reduction Innovations

PMDA’s 2024 Software as Medical Device guideline cut AI tool clearance to 12-18 months, setting the stage for rapid commercialization of positioning algorithms and dose-reduction software[1]Pharmaceuticals and Medical Devices Agency, “Software as Medical Device Guidelines 2024,” PMDA.GO.JP. Canon’s automatic positioning trims patient setup time by 40%, while Fujifilm’s adaptive exposure algorithms maintain image quality at lower doses. Technologists in rural sites running multiple modalities simultaneously gain particular value from such automation. The innovations align with the government’s goal to halve administrative burden by 2030 and add 1.5 percentage points to the Japan digital X-ray market CAGR.

Prefecture Hospital-Merger Programs Driving Fleet Renewal

Regional planning toward 2040 is consolidating secondary and tertiary facilities, allowing merged systems to negotiate standardized fleet contracts. Replacement of CR units with DR suites is a centerpiece of these plans, often sweetened by prefecture-level subsidies. Vendors providing bundled training and service contracts gain a competitive edge. The procurement cycles associated with mergers are front-loaded, making this a short-term accelerator that adds 1.2 percentage points to market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & lifecycle cost of DR systems | −1.4% | National, rural hospitals hardest hit | Medium term (2-4 years) |

| Urban saturation of installed base | −1.1% | Tokyo, Osaka, Nagoya metros | Long term (≥4 years) |

| Radiographer skills gap outside metros | −0.8% | Rural and regional areas | Long term (≥4 years) |

| Supply-chain risk for CsI scintillators | −0.6% | National, manufacturing hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Capital & Lifecycle Cost of DR Systems

Initial DR room investments of JPY 15-50 million versus JPY 3-8 million for CR create sticker shock, especially for prefectural clinics. Lifetime service contracts, software licenses, and periodic detector upgrades add an extra 40-60% to ownership cost[2]Japan Medical Imaging and Radiological Systems Industries Association, “Industry Vision 2030 Report,” JIRA-NET.OR.JP. Smaller facilities with low daily volumes find it hard to recoup the outlay despite reimbursement add-ons, shaving 1.4 percentage points off the Japan digital X-ray market CAGR.

Urban Saturation of Installed Base

Tokyo, Osaka, and Nagoya boast near-universal DR penetration, pushing purchase cycles into replacement mode only. Replacement intervals have stabilized at 8-10 years, slowing unit growth and trimming 1.1 percentage points from national CAGR. Vendors must now differentiate through AI, workflow speed, and energy metrics rather than simple digitization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Portability: Mobile Solutions Drive Rural Access

Japan digital X-ray market size for portability segments shows fixed rooms retaining 60.55% revenue share in 2024, yet hand-held and cart-based units are forecast to grow 12.25% annually through 2030. Rural consolidation drives mobile van deployments that cover several satellite clinics in weekly rotations, maximizing detector utilization. Urban trauma centers continue to rely on ceiling-mounted rooms optimized for throughput, showcasing a dual-track demand structure.

Hand-held devices weighing under 4 kg let a single technologist serve emergency, ward, and ICU scans without moving patients, a priority under infection-control protocols. Mobile DR carts meet the middle-ground need for semi-fixed positioning in community hospitals lacking radiography suites. Vendors are bundling AI auto-standing and preview displays to cut exposure repeats, vital in settings with limited staff. Consequently, mobile solutions are central to narrowing rural imaging disparities inside the Japan digital X-ray market.

By Detector Panel Type: CMOS Technology Disrupts Silicon Dominance

Amorphous silicon retained 45.53% share of Japan digital X-ray market size in 2024, but CMOS panels are growing 11.85% annually, fueled by energy savings and faster readouts. Hospitals chasing carbon-neutral scores are reprioritizing procurement toward CMOS based on 30-40% lower power consumption and integrated AI chips that accelerate in-room analytics.

Domestic semiconductor policy now offers tax credits for detectors sourced from Japanese fabs, making CMOS an even stronger option. Flexible IGZO panels are entering pediatric use cases where conformability reduces patient repositioning. While silicon dominates by installed base, CMOS momentum signals a tipping point that will reshape detector purchasing in the Japan digital X-ray market by mid-decade.

By Application: Dental Imaging Capitalizes on Demographic Trends

Orthopedic scans controlled 28.63% of Japan digital X-ray market share in 2024, yet dental imaging’s 10.87% CAGR positions it as the break-out segment[3]Japan Dental Association, “Dental Health Statistics 2024,” JDA.OR.JP. Growth is linked to implant volume among seniors and a national preventive oral health campaign that subsidizes peri-implantitis screening. Digital intraoral sensors and panoramic units together form a steady replacement revenue stream for vendors.

Orthopedic demand remains robust, fueled by osteoarthritis and fracture management in the aging population. However, AI-guided bone-age estimation and fracture detection are opening new value pools. Chest imaging holds sizable volume in annual health checks mandated by employers, while cardiovascular applications gain support from AI calcium scoring algorithms. In every application, dose-reduction and workflow acceleration shape the product roadmap in the Japan digital X-ray market.

By End User: Mobile Units Address Access Disparities

Hospitals and multispecialty clinics generated 66.63% of Japan digital X-ray market size in 2024, but mobile screening vans are expanding at an 11.07% CAGR. Prefecture health departments deploy truck-mounted DR for tuberculosis, lung cancer, and bone density programs, reaching remote islands and mountainous towns with limited fixed infrastructure.

Diagnostic imaging centers in suburban belts are filling overflow from tertiary hospitals, often emphasizing value-added AI reconstruction services. Occupational health providers use portable units to comply with mandatory worker checkups, while university laboratories test prototype detectors under PMDA fast-track schemes. Together, the diversified end-user mix grants vendors resilience against cyclical hospital spending patterns in the Japan digital X-ray market.

Geography Analysis

Japan digital X-ray market displays stark regional contrasts despite a unified reimbursement framework. Tokyo, Osaka, and Kanagawa hospitals have nearly 100% DR penetration and prioritize AI upgrades over base hardware replacements. Conversely, prefectures such as Shimane, Kochi, and Akita operate fewer than 0.4 radiographers per 1,000 residents, making mobile fleets essential for coverage.

Northern regions—Hokkaido and Tohoku—are early adopters of truck-mounted X-ray fitted with AI positioning tools, leveraging ruggedized CMOS panels that survive sub-zero logistics. Central Honshu benefits from proximity to detector manufacturing hubs, reducing service lead times and influencing purchase decisions. Kyushu hospitals, located near semiconductor fabs, experiment with locally produced CMOS prototypes under economic security initiatives.

Government consolidation plans foster cross-prefecture procurement alliances, allowing shared service contracts that lower lifecycle costs. This cohesion accelerates DR adoption in areas where standalone facilities once lacked financial capacity. Consequently, geography-driven variation is narrowing, yet it still shapes the competitive playbook for the Japan digital X-ray market.

Competitive Landscape

The Japan digital X-ray market is moderately concentrated, with the top five vendors—Canon, Fujifilm, Siemens Healthineers AG, Koninklijke Philips NV, and GE Healthcare—collectively holding significant share. Domestic players employ extensive service networks and familiarity with reimbursement coding to lock in long-term accounts. International firms—Siemens Healthineers and Philips—compete on AI workflow and energy efficiency, aligning with carbon-neutral mandates to penetrate mature urban sites.

Vertically integrated manufacturers gain insulation from CsI shortages and semiconductor lead-time swings, a strategic advantage under Japan’s Economic Security Promotion Law. GE Healthcare’s full acquisition of Nihon Medi-Physics bolsters local radio-isotope supply and signals commitment to deeper localization. Konica Minolta’s procurement joint venture with FUJIFILM BI underscores cost-sharing moves among Japanese incumbents.

Competitive levers center on AI dose control, detector robustness, and integrated cloud PACS. Vendors that bundle hardware with subscription analytics are converting capital sales into annuity revenues, locking customers through data ecosystems. Supply-chain resilience and regulatory agility now rank alongside image quality in buyer evaluations, reshaping the strategic landscape of the Japan digital X-ray market.

Japan Digital X-Ray Industry Leaders

Fujifilm Holdings Corporation

GE Healthcare

Koninklijke Philips NV

Siemens Healthineers AG

Canon Medical Systems Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: FUJIFILM unveiled a portable X-ray unit employing AI-based patient positioning for remote and home care settings.

- March 2025: Canon Medical Systems launched Radrex i5 / Flex Edition, a manual general X-ray room designed for cost-sensitive domestic hospitals.

Japan Digital X-Ray Market Report Scope

As per the scope of this report, digital X-ray or digital radiography is a form of X-ray imaging where digital X-ray sensors are used instead of traditional photographic films. This has the added advantage of time efficiency and the ability to transfer images digitally and enhance them for better visibility. This method bypasses the chemical processing of photographic films. Digital X-ray imaging has high demand, as it requires less radiation exposure compared to traditional X-rays. Japan's digital X-ray market is segmented by application, technology, portability and end user. By application market is segmented into orthopedic, cancer, dental, cardiovascular, and other applications. By technology market is segmented into computed radiography and direct radiography. By portability the market is segmented into fixed systems and portable systems. By end-user market is segmented into hospitals, diagnostic centers, and other end-users. The report offers the value (in USD) for all the above segments.

By Portability

| Fixed Systems |

| Mobile DR Systems |

| Hand-held Systems |

By Detector Panel Type

| Amorphous Silicon |

| CMOS |

| IGZO / Flexible Panels |

By Application

| Orthopedic |

| Chest Imaging |

| Cardiovascular |

| Dental |

| Other Applications |

By End User

| Hospitals & Multispecialty Clinics |

| Diagnostic Imaging Centers |

| Mobile Screening Units |

| Other End Users |

| By Portability | Fixed Systems |

| Mobile DR Systems | |

| Hand-held Systems | |

| By Detector Panel Type | Amorphous Silicon |

| CMOS | |

| IGZO / Flexible Panels | |

| By Application | Orthopedic |

| Chest Imaging | |

| Cardiovascular | |

| Dental | |

| Other Applications | |

| By End User | Hospitals & Multispecialty Clinics |

| Diagnostic Imaging Centers | |

| Mobile Screening Units | |

| Other End Users |

Key Questions Answered in the Report

How large is the Japan digital X-ray market in 2025?

The market stands at USD 614.34 million in 2025 and is on track to approach USD 968.89 million by 2030.

What CAGR is projected for Japan digital X-ray through 2030?

A CAGR of 9.54% is forecast for the 2025-2030 period.

Which detector technology is gaining fastest in Japan?

CMOS panels are growing at 11.85% annually due to energy savings and built-in AI processing.

Why are mobile screening units expanding rapidly?

Government rural health programs and hospital consolidation are driving 11.07% CAGR for mobile vans that offer flexible, low-cost coverage.

Who are the leading companies in Japan digital X-ray?

Canon, Fujifilm, Shimadzu, Konica Minolta, and GE Healthcare together control roughly 68% of national revenue.

What policy changes are influencing X-ray adoption?

The FY 2024 medical fee revision with its Medical DX add-on and PMDA fast-track approvals are accelerating replacement of legacy CR systems.

Page last updated on: