China Data Center Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 12.95 Billion |

| Market Size (2026) | USD 15.36 Billion |

| Market Size (2031) | USD 36.68 Billion |

| Growth Rate (2026 - 2031) | 19.02% CAGR |

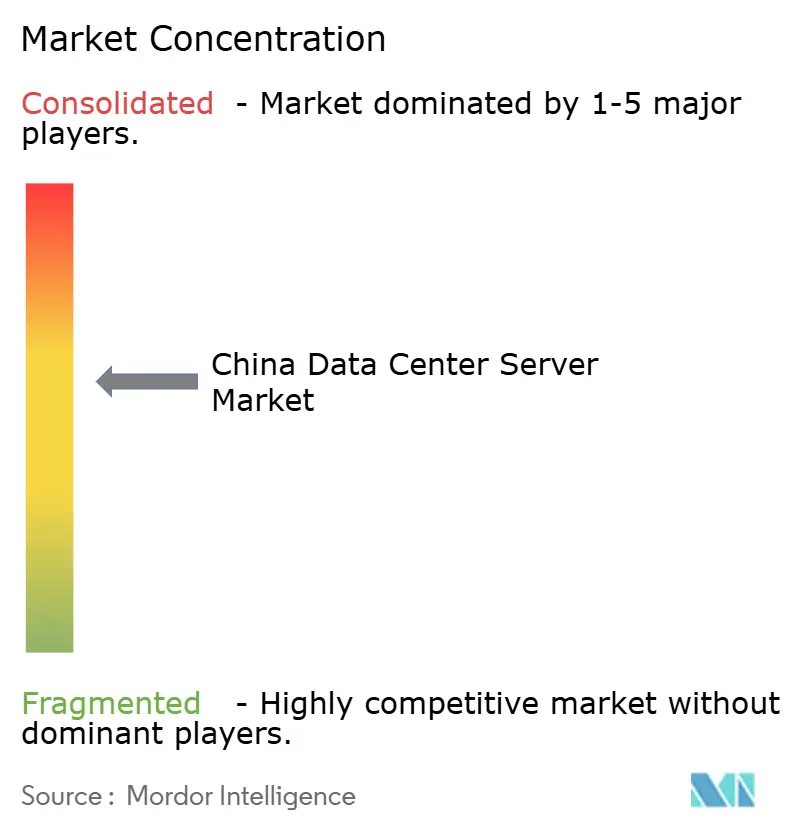

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Data Center Server Market Analysis by Mordor Intelligence

The China data center server market size was valued at USD 12.95 billion in 2025 and is estimated to grow from USD 15.36 billion in 2026 to reach USD 36.68 billion by 2031, at a CAGR of 19.02% during the forecast period (2026-2031). Beijing’s push for sovereign computing, the mounting demand for generative AI, and the fast-spreading adoption of edge analytics are reshaping procurement criteria away from legacy x86 refreshes toward GPU-dense, liquid-cooled systems. Hyperscalers are accelerating direct campus builds to gain control of thermal design, while colocation operators invest in Tier 3 expansions to capture enterprise workloads migrating out of aging server rooms. Simultaneously, western provinces entice batch-processing applications with lower power tariffs and abundant renewable energy, freeing scarce Tier 1 capacity for latency-sensitive AI training. Supply-chain headwinds, chiefly advanced packaging constraints and export restrictions on top-end GPUs, continue to temper near-term shipment velocity but are also stimulating indigenous processor adoption and the development of creative cooling architectures.

Key Report Takeaways

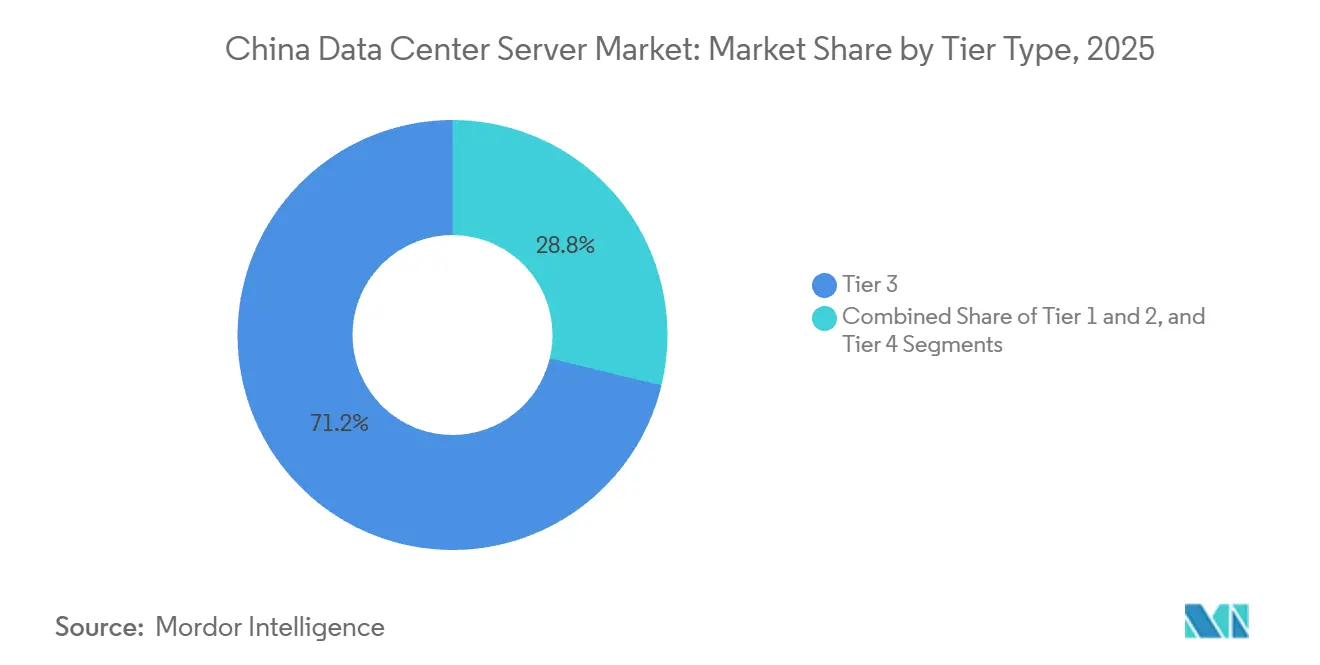

- By tier type, tier 3 installations dominated with a 71.24% share in 2025, whereas tier 4 facilities are expanding at a 20.31% CAGR through 2031.

- By data-center type, colocation deployments led with 56.87% of market share in 2025, while hyperscaler-owned sites are advancing at a 20.65% CAGR.

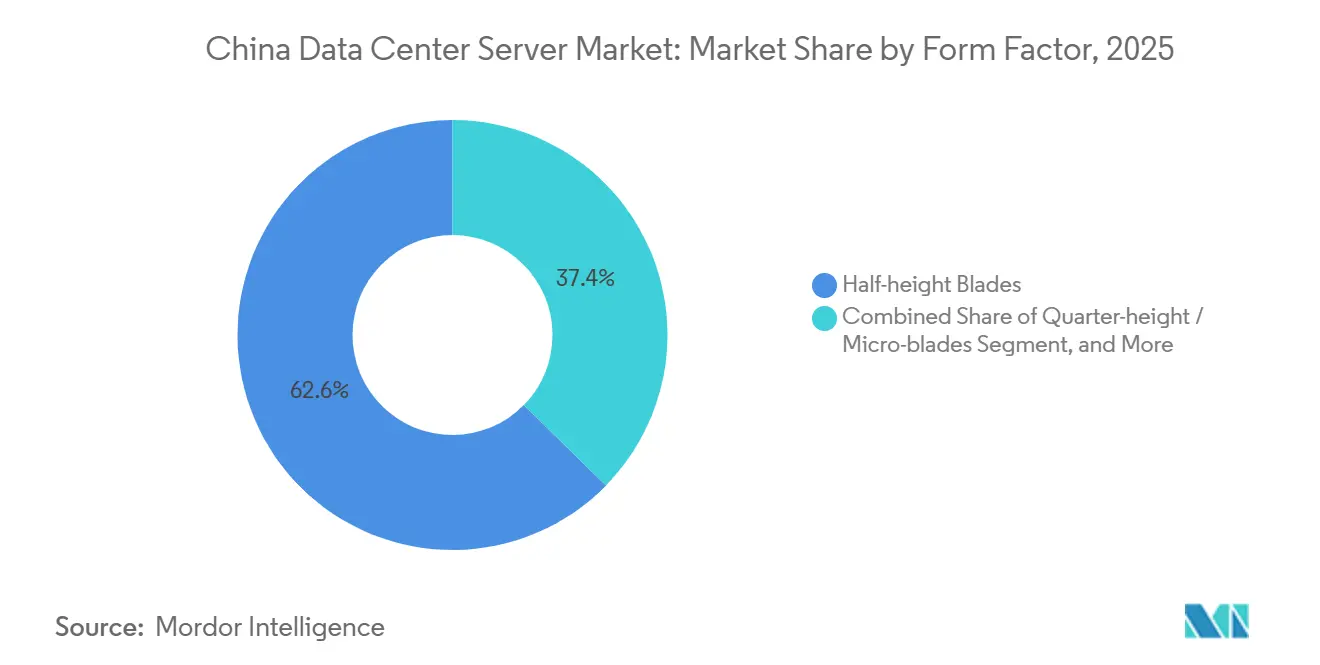

- By form factor, half-height blade servers captured 62.65% of market share in 2025; quarter-height micro-blades register the fastest growth at a 20.73% CAGR.

- By application, AI and machine-learning workloads accounted for 36.76% of market share in 2025, yet virtualization and private cloud workloads are rising at a 20.82% CAGR.

- By data-center size, hyperscale campuses held 40.54% of market share in 2025 and are on track for a 20.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide data center server market outlook captures this forward trajectory.

China Data Center Server Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI and GPU-Accelerated Workload Demand | +4.2% | National, concentrated in Beijing, Shanghai, Shenzhen, Hangzhou | Short term (≤ 2 years) |

| Rising Enterprise Cloud Adoption and Public Cloud IaaS Spending | +3.8% | National, led by eastern provinces and Pearl River Delta | Medium term (2-4 years) |

| Rapid 5G Roll-Out Catalyzing Edge Data Center Expansion | +3.5% | National, early gains in Guangdong, Jiangsu, Zhejiang | Medium term (2-4 years) |

| Government Digital-Infrastructure Incentives and Subsidies | +2.9% | National, prioritizing western regions under East-Data-West-Computing | Long term (≥ 4 years) |

| Commercialization of Underwater Data Centers for Sustainable Cooling | +1.8% | Coastal provinces: Shanghai, Hainan, Guangdong | Long term (≥ 4 years) |

| Factory-Integrated Cabinet Delivery Shortening Deployment Lead Times | +1.6% | National, with ODM hubs in Shenzhen, Suzhou | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in AI and GPU-Accelerated Workload Demand

Large language models such as Alibaba’s Tongyi Qianwen and Baidu’s ERNIE require clusters of eight-way GPU nodes linked by 400 GbE or InfiniBand fabrics, pushing typical rack densities above 70 kW. Operators purchased roughly 1 million Nvidia H20 GPUs in 2025, pairing them with custom cold-plate loops to maximize throughput despite lower peak flops. Huawei’s Ascend 910B, fabricated at SMIC, is winning share among state-owned enterprises prioritizing supply-chain sovereignty over raw benchmark records. The Ministry of Industry and Information Technology reported a 45% jump in intelligent-computing power installations in early 2025, triple the growth of general-purpose servers. These dynamics lift average selling prices, accelerate adoption of NVMe storage, and magnify the overall momentum of the China data center server market.

Rising Enterprise Cloud Adoption and Public Cloud IaaS Spending

CAICT estimated that 38% of enterprise workloads ran on public or hybrid clouds by end-2025, up from 29% in 2023.[1]Alibaba Cloud, “Tongyi Qianwen Technical White Paper,” ALIBABACLOUD.COM Tencent Cloud pledged USD 10 billion through 2030 for new campuses in Tianjin, Chongqing, and Qingyuan, heightening bulk demand for high-density chassis. Alibaba Cloud’s fifth-generation ECS instances, powered by ARM-based Yitian 710 chips, trimmed per-VM cost by 20% relative to x86 predecessors.[2]China Academy of Information and Communications Technology, “Cloud Computing Development White Paper 2025,” CAICT.AC.CN With Baidu operating more than 500,000 servers and planning 100,000 more in 2026, vendor success hinges on securing hyperscale design wins. This concentration further solidifies purchasing power and shapes customization trends across the China data center server market.

Rapid 5G Roll-Out Catalyzing Edge Data Center Expansion

The three national telecom carriers had installed 3.6 million 5G base stations by 2025, all requiring proximate edge compute for latency-critical workloads. CAICT projects 50,000 MEC sites by 2027, each with 2–10 RU of servers. Huawei’s ruggedized FusionServer E series and Inspur’s NF5180M6-Edge illustrate designs that tolerate −5 °C to 45 °C ambient ranges, run on 300 W envelopes, and enable remote O&M via 5G backhaul. Regulatory targets of PUE < 1.3 at the edge accelerate adoption of direct-to-chip liquid loops even in micro-server formats. Collectively, edge build-outs extend the geographic and workload footprint of the China data center server market.

Government Digital-Infrastructure Incentives and Subsidies

Under the East-Data-West-Computing program, Beijing allocated CNY 50 billion (USD 7 billion) in 2025 to spur hyperscale construction in Inner Mongolia, Gansu, Guizhou, and Ningxia. Electricity tariffs in these zones fall to CNY 0.28 /kWh versus CNY 0.65 in Shanghai, shaving TCO by up to 30%. China Telecom’s 100-MW Hohhot build exemplifies latency-tolerant batch processing shifting inland, freeing Tier 1 racks for revenue-dense AI clusters. Policies mandate 50% renewable power by 2027, driving server buyers toward energy-efficient liquid-cooled architectures. Incentives therefore widen regional capacity while lifting premium server demand along the coast, reinforcing growth drivers for the China data center server market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CapEx and Power-Land Scarcity in Tier 1 Hubs | -2.7% | Beijing, Shanghai, Shenzhen, Guangzhou | Short term (≤ 2 years) |

| Export Controls Limiting Access to Cutting-Edge GPUs and CPUs | -2.3% | National, acute in AI research institutions and hyperscalers | Medium term (2-4 years) |

| Advanced Packaging Capacity Bottlenecks for AI Server Components | -1.9% | National, supply-chain dependencies on Taiwan and South Korea | Medium term (2-4 years) |

| Water-Use Restrictions Challenging Liquid-Cooling Scale-Up | -1.4% | Beijing, Shanghai, Tianjin, Hebei province | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CapEx and Power-Land Scarcity in Tier 1 Hubs

Land in Beijing’s Yizhuang and Shanghai’s Lingang averaged CNY 15 million (USD 2.1 million) per acre in 2025, while municipal power caps hold new allocations to 50 MW per project.[3]China Real Estate Information Corporation, “Land Price Index Report Q4 2025,” CRIC.COM Shenzhen bans builds with PUE above 1.25, effectively mandating liquid cooling and adding 20% to upfront spend. Operators retrofit telecom exchanges or source capacity in Chengdu and Wuhan where land costs one-third as much, then reserve Tier 1 racks for GPU-dense clusters. The bifurcated strategy increases logistical complexity and slows urban expansion, curbing near-term velocity for the China data center server market.

Export Controls Limiting Access to Cutting-Edge GPUs and CPUs

U.S. rules bar shipment of Nvidia H100, A100, and AMD MI300 GPUs, forcing Chinese buyers to rely on down-binned H20 parts that extend AI training cycles 40-60%. Huawei’s Ascend 910B delivers 26 TFLOPS FP16, yet porting CUDA-optimized frameworks to CANN prolongs software integration. Meanwhile, CoWoS packaging queues lengthened to eight months in 2025, inflating server prices by 25% and stretching lead times past two quarters. Such constraints temper deployment schedules and complicate capacity planning across the China data center server market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Emphasis On Fault Tolerance Lifts Premium Segment

Tier 3 facilities held 71.24% of 2025 installations, underscoring their balance of cost and 99.982% uptime, while Tier 4 capacity is rising at a 20.31% CAGR as finance and public-cloud operators safeguard AI training runs from interruption. In 2025, China Construction Bank reported 12 Tier 4 sites that hosted distributed-ledger settlement workloads without unscheduled outages. Insurance carriers and hospitals follow suit to comply with 99.995% availability mandates. Vendors cater with blade platforms featuring dual-path fabrics and hot-swap everything, elevating ASPs but minimizing downtime penalties.

Price-sensitive SMEs continue to favor Tier 3 colocation racks that cost roughly 30% less than Tier 4 cabinets, fueling resilient refresh for single-supply air-cooled servers. Prefabricated Tier 3 pods, deliverable in six months, suit the rapid iteration culture of Chinese software firms. Consequently, the China data center server market sustains a dual-track mix, where high-margin Tier 4 nodes grow fastest yet Tier 3 still anchors shipment volume.

By Data Center Size: Hyperscale Dominates Capacity And Innovation

Hyperscale campuses with more than 10,000 servers commanded 40.54% of installed units in 2025 and are progressing at a 20.14% CAGR as Alibaba Cloud, Tencent Cloud, and Baidu Cloud add greenfield sites inland. Alibaba operated seven such campuses in 2025 and announced two more in Chengdu and Wuhan, each designed for 80,000 liquid-cooled racks. Volume buys secure up to 30% list-price discounts and enable co-design of custom silicon.

Large (1,000-10,000 servers) and medium (100-1,000) facilities remain vital for regional ISPs, provincial governments, and industrial hubs that crave local control but lack hyperscale budgets. Small on-premise rooms are retiring as cloud-first mandates take hold, redirecting replacement demand into shared facilities. The resulting scale polarization concentrates bargaining power and defines roadmaps for the China data center server market.

By Data Center Type: Colocation Leads, Hyperscalers Gain Share

Colocation operators enjoyed 56.87% deployment share in 2025, hosting regulated workloads that require customer hardware ownership yet professional facilities management. GDS Holdings added 120 MW of Tier 1 city capacity in late-2025, illustrating persistent urban demand. At the same time, hyperscalers are pressing a 20.65% CAGR by internalizing batches to fine-tune cooling and networking at lower TCO.

Enterprise server rooms continue to shrink, giving way to edge PoPs or cloud services that better meet PUE and staffing constraints. Colocation firms differentiate with liquid-cooling-as-a-service and compliance audits, boosting stickiness even as hyperscalers scoop strategic land. These cross-currents shape procurement cycles and vendor ranking within the China data center server market.

By Form Factor: Blades Remain Mainstream As Micro-Blades Accelerate

Half-height blades filled 62.65% of shipments in 2025, leveraging shared chassis resources to enhance density. A 10U enclosure holding 16 blades provides 32 CPU sockets, translating into operational savings on cabling and airflow. Liquid-cooling-ready variants enable 15 kW per blade, keeping pace with GPU requirements. Quarter-height micro-blades, however, are expanding at a 20.73% CAGR as 5G MEC sites need compact, low-power nodes.

Huawei’s CH121 V5 and Inspur’s NF5180M6-Edge typify micro-servers that fit telecom racks and tolerate high ambient temperatures. As operators shift inference workloads to the edge, the China data center server market size for micro-blades is expected to multiply, while full-height GPU blades remain staples for centralized AI training clusters.

By Application And Workload: AI Leads While Virtualization Rebounds

AI, ML, and data-analytics tasks occupied 36.76% of server cycles in 2025, fueled by multimodal model training and fraud-detection engines. Alibaba’s Tongyi Qianwen required a USD 300 million, 10,000-GPU cluster, spotlighting the capital intensity of frontier AI. Nevertheless, virtualization and private cloud workloads are rising at a 20.82% CAGR as enterprises refactor monoliths into containerized microservices to satisfy digital-transformation targets.

High-performance computing and storage workloads migrate to inland hyperscale sites where power is cheaper. Edge servers, equipped with T4 or MLU220 accelerators, proliferate in mobile-gaming and autonomous-vehicle telemetry. The resulting workload mosaic expands total addressable demand, ensuring the China data center server market share of AI remains high even as traditional IT refresh accelerates.

Geography Analysis

Eastern seaboard provinces such as Beijing, Shanghai, Guangdong, and Zhejiang hosted 55% of installed capacity in 2025, leveraging dense fiber, high spending power, and proximity to multinational headquarters. Beijing’s Yizhuang zone interconnects directly with ChinaNet backbones, supporting latency-sensitive fintech and gaming apps. Shanghai’s Lingang cluster specializes in Tier 4 builds for high-frequency trading, sustaining rack rates that justify sub-1.1 PUE investments. Guangdong’s linkage to Hong Kong attracts cross-border SaaS, with colocation vacancy under 8% despite steady supply growth.

Under the East-Data-West-Computing program, Inner Mongolia, Gansu, Guizhou, and Ningxia are absorbing batch-processing and archival workloads. Inner Mongolia offers CNY 0.25 /kWh wind power, 60% below Shanghai levels, prompting China Mobile and China Unicom to commission 100-MW campuses. Guizhou’s cool climate enables free-air cooling ten months a year, further improving TCO. Western deployments typically emphasize storage-dense x86 nodes, while coastal sites reserve racks for GPU-rich AI clusters, illustrating a bifurcated hardware mix within the China data center server market.

Tier 2 cities like Chengdu, Wuhan, Xi’an, and Hangzhou emerge as equilibrium locations, offering land 50% cheaper than Tier 1 yet fiber latency under 10 ms to coastal IXPs. Alibaba’s planned hyperscale builds in Chengdu and Wuhan exemplify the trend. These cities also benefit from university talent pools and provincial incentives, driving localized edge deployments that expand the geographic footprint of the China data center server industry.

The data center server market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Africa, North America, and Americas. This is complemented by country-specific insights for Malaysia, Philippines, South Africa, Canada, United States, and Israel, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The market indicates moderate concentration, with players such as Huawei, Inspur, Lenovo, Dell Technologies, New H3C, and others. Huawei leverages Kunpeng CPUs and Ascend GPUs to sell vertically integrated FusionServers insulated from export shocks, winning government and SOE deals. Inspur and Lenovo deploy rapid-customization factories capable of delivering tailored racks in four weeks, catering to hyperscalers that refresh thousands of nodes per order. Dell Technologies and Hewlett Packard Enterprise remain preferred by multinationals for global support continuity but face 20-25% pricing gaps versus domestic peers.

Original design manufacturers such as Foxconn accelerate share gains by shipping turnkey, liquid-ready cabinet pods that compress on-site installation from weeks to days. Cooling specialists like CoolIT Systems partner with server brands to retrofit installed fleets, prolonging asset life cycles. Indigenous chipmakers Phytium, Hygon, Cambricon collaborate with OEMs on reference boards to meet cybersecurity localization rules, creating alternate technology stacks that diversify the China data center server market.

Huawei filed over 1,200 thermal-management patents between 2023 and 2025, potentially extracting royalties or deterring fast followers. Pricing battles persist, yet service attach rates liquid-coolant maintenance, firmware updates, AI-platform consulting now drive profitability more than bare-metal margin. The evolving landscape ultimately advantages suppliers capable of integrating silicon, firmware, rack mechanics, and field services into cohesive offers.

China Data Center Server Industry Leaders

Huawei Technologies Co., Ltd.

Lenovo Group Limited

New H3C Technologies Co., Ltd.

Super Micro Computer, Inc.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Alibaba Cloud committed USD 5 billion to hyperscale campuses in Chengdu and Wuhan, each designed for 80,000 liquid-cooled racks.

- December 2025: Huawei launched FusionServer Pro 2488H V7, integrating eight Ascend 910C accelerators with 12 kW direct-to-chip cooling.

- November 2025: GDS Holdings acquired three Tier 1 city facilities for USD 800 million, adding 120 MW of capacity.

- October 2025: Inspur and China Mobile agreed to deploy 50,000 NF5180M6-Edge servers across the carrier’s MEC network.

China Data Center Server Market Report Scope

A data center server is basically a high-capacity computer without peripherals like monitors and keyboards. It is a hardware unit installed inside a rack, having a central processing unit (CPU), storage, and other electrical and networking equipment, making them powerful computers that deliver applications, services, and data to end-user devices.

The China Data Center Server Market Report is Segmented by Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, Hyperscalers/CSPs, and Enterprise and Edge), Form Factor (Half-height Blades, Full-height Blades, and Quarter-height/Micro-blades), Application/Workload (Virtualization and Private Cloud, HPC, AI/ML and Data Analytics, Storage-centric, and Edge/IoT Gateways). The Market Forecasts are Provided in Terms of Value (USD).

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Small Data Center |

| Medium Data Center |

| Large Data Center |

| Hyperscale Data Center |

| Colocation Data Center |

| Hyperscalers Data Center/CSPs |

| Enterprise and Edge Data Center |

| Half-height Blades |

| Full-height Blades |

| Quarter-height / Micro-blades |

| Virtualisation and Private Cloud |

| High-Performance Computing (HPC) |

| Artificial Intelligence/Machine Learning and Data Analytics |

| Storage-centric |

| Edge / IoT Gateways |

| By Tier Type | Tier 1 and 2 |

| Tier 3 | |

| Tier 4 | |

| By Data Center Size | Small Data Center |

| Medium Data Center | |

| Large Data Center | |

| Hyperscale Data Center | |

| By Data Center Type | Colocation Data Center |

| Hyperscalers Data Center/CSPs | |

| Enterprise and Edge Data Center | |

| By Form Factor | Half-height Blades |

| Full-height Blades | |

| Quarter-height / Micro-blades | |

| By Application / Workload | Virtualisation and Private Cloud |

| High-Performance Computing (HPC) | |

| Artificial Intelligence/Machine Learning and Data Analytics | |

| Storage-centric | |

| Edge / IoT Gateways |

Key Questions Answered in the Report

What is the current value of the China data center server market?

The market was valued at USD 15.36 billion in 2026 and is forecast to reach USD 36.68 billion by 2031.

How fast is spending on servers in China growing?

Revenue is projected to rise at a 19.02% CAGR between 2026 and 2031, led by AI-optimized, liquid-cooled platforms.

Which server form factor is most popular among Chinese operators?

Half-height blade servers dominate shipments with a 62.65% share in 2025, though micro-blades are the fastest-growing choice for edge sites.

Why are hyperscale data centers expanding inland?

Western provinces offer cheaper land, lower power tariffs, and renewable-energy incentives, helping operators shift latency-tolerant workloads while freeing Tier 1 space for GPU clusters.

How are U.S. export controls affecting Chinese server procurement?

Restrictions on top-end GPUs extend AI training times and force operators to adopt domestically produced accelerators, lengthening deployment cycles and raising server costs.

What cooling technologies are gaining traction in China’s data centers?

Direct-to-chip liquid loops, immersion baths, and pilot underwater modules are all being adopted to meet aggressive PUE targets and municipal water quotas.

Page last updated on: