Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2022 - 2024 |

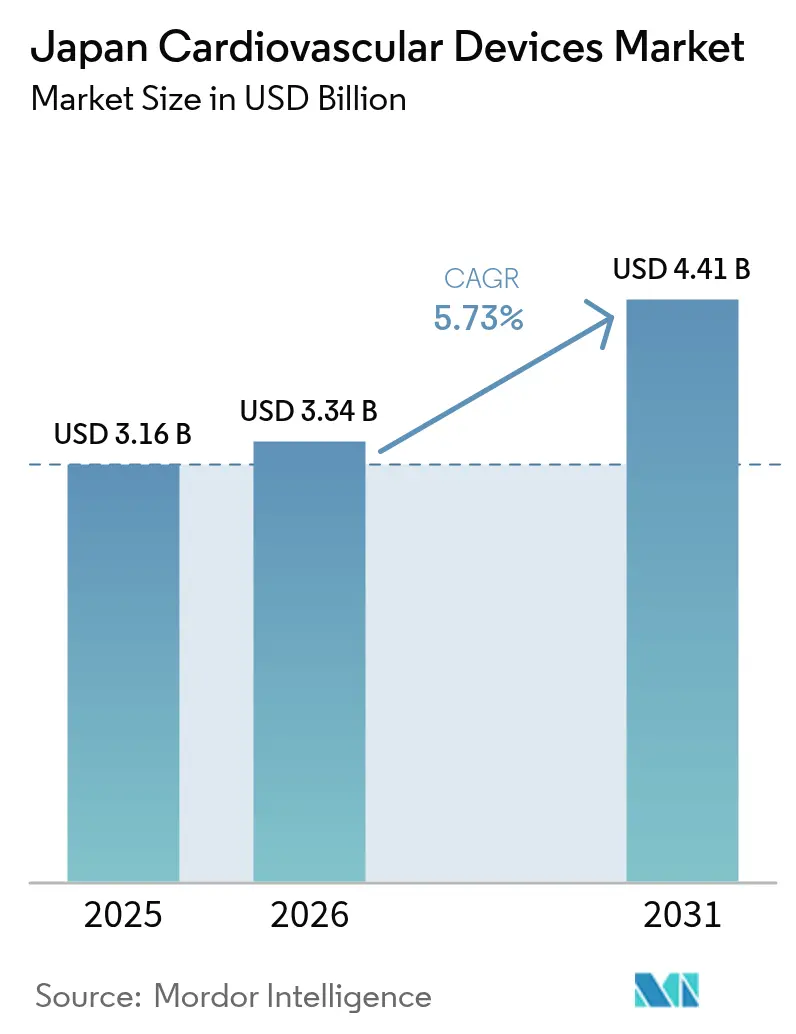

| Base Year Market Size (2025) | USD 3.16 Billion |

| Market Size (2026) | USD 3.34 Billion |

| Market Size (2031) | USD 4.41 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Cardiovascular Devices Market Analysis by Mordor Intelligence

The Japan cardiovascular devices market size was valued at USD 3.16 billion in 2025 and estimated to grow from USD 3.34 billion in 2026 to reach USD 4.41 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031). This expansion is powered by an aging population, nationwide reimbursement reforms that favor minimally invasive interventions, and rapid uptake of remote diagnostic technologies. Competition has intensified as international innovators use accelerated approval pathways such as SAKIGAKE to gain traction, while domestic companies leverage deep distribution networks. Price‐cutting cycles under the National Health Insurance (NHI) apply continuous pressure on margins, forcing manufacturers to differentiate through smarter materials, AI integration, and miniaturization. Simultaneously, a shortage of electrophysiology specialists caps growth for complex arrhythmia therapies, but it also accelerates investment in automated mapping systems and simplified workflows. Overall, the Japan cardiovascular devices market continues to grow even as the national population shrinks because the pace of age-linked cardiovascular disease outstrips demographic decline [meti.go.jp].

Key Report Takeaways

- By device type, therapeutic & surgical devices held 75.72% of the Japan cardiovascular devices market share in 2025.

- Diagnostic & monitoring devices are projected to post the fastest 6.72% CAGR from 2026 to 2031.

- By application, coronary artery disease led with 42.12% revenue share of the Japan cardiovascular devices market size in 2025. Structural & congenital heart defects are forecast to expand at a 6.89% CAGR between 2026 and 2031.

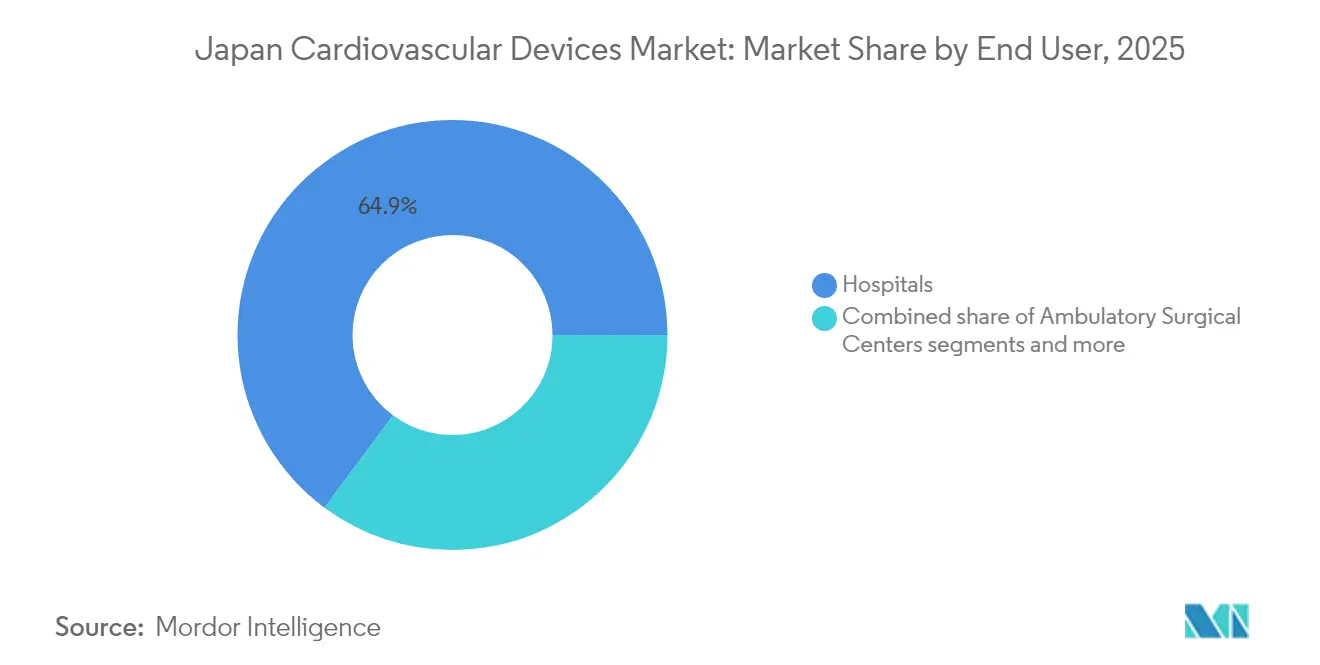

- By end user, hospitals & cardiac centers commanded 64.85% share in 2025, while ambulatory surgical centers are advancing at a 6.48% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing Population Intensifies Cardiac Disease Burden in Japan | +2.1% | National, with higher impact in rural prefectures | Long term (≥ 4 years) |

| Nationwide Implementation of Advanced Reimbursement Codes for TAVI and PCI | +1.4% | National, with concentration in urban centers | Medium term (2-4 years) |

| High Penetration of Screening Programs using ECG & Holter in Community Clinics | +1.2% | National, with early adoption in Tokyo, Osaka, Kyoto | Medium term (2-4 years) |

| Government Grants Supporting Domestic R&D in Catheter-based Therapies | +0.7% | National, with focus on industrial clusters | Long term (≥ 4 years) |

| Surge in Private Cath Lab Infrastructure across Secondary Cities | +0.6% | Regional, concentrated in tier-2 cities | Medium term (2-4 years) |

| Preference for Minimally Invasive Valve Repairs among Elderly Cohorts | +0.9% | National, with higher adoption in major cardiac centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing population intensifies cardiac disease burden

Nearly 29.1% of Japanese citizens are now above 65 years, the highest proportion globally. That demographic trend correlates with rising prevalence of atrial fibrillation, heart failure, and aortic stenosis, boosting long-term demand for stents, valves, pacemakers, and diagnostic monitors. Sudden cardiac death already claims more than 80,000 Japanese lives each year[1]Source: Ikeda T. et al., “2025 Japanese Heart Rhythm Society / Japanese Circulation Society Consensus Statement on the Appropriate Use of Ambulatory and Wearable Electrocardiographs,” jstage.jst.go.jp . Cohort data involving 3.5 million working-age adults shows a 96% jump in adverse cardiovascular outcomes among individuals with significant ECG abnormalities. Those statistics strengthen government resolve to fund preventive screening programs and device-based therapies nationwide.

Nationwide reimbursement codes for TAVI & PCI

Since 2021 Japan’s Ministry of Health, Labour and Welfare (MHLW) has consistently upgraded reimbursement schedules for transcatheter aortic valve implantation (TAVI) and percutaneous coronary intervention (PCI). Cost-effectiveness models indicate TAVI is economically dominant for intermediate-risk patients and cost-effective for low-risk cohorts, with incremental ratios well below the ¥5 million per quality-adjusted life-year benchmark. The broadened codes enlarge the eligible patient pool and incentivize hospitals to invest in imaging, fractional-flow reserve systems, and next-gen stent platforms.

High penetration of ECG screening in community clinics

Mandatory annual ECG exams for every employee aged 35+ translate into roughly 40 million recordings each year. Updated 2025 guidance from the Japanese Heart Rhythm Society encourages the clinical use of wearable ECG devices, fueling demand for cloud-linked monitors that push data to AI algorithms for triage and early detection [jstage.jst.go.jp]. Widespread screening drives earlier referral for ablation, pacemaker implantation, or drug therapy, indirectly lifting sales of therapeutic hardware.

Preference for minimally invasive valve repairs

Japan Circulation Society guidelines now recommend TAVI for patients ≥ 80 years, citing lower in-hospital mortality versus surgical valve replacement [jacc.org]. Device makers have responded by tailoring delivery systems to smaller Asian anatomies and by launching leadless pacemakers and subcutaneous defibrillators suitable for frail elderly patients. Rapid uptake in high-volume centers makes structural heart devices one of the fastest rising revenue pools within the Japan cardiovascular devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking Overall Procedure Volumes due to COVID-Related Deferrals | -1.0% | National, with greater impact in urban centers | Short term (≤ 2 years) |

| Stringent Post-Market Surveillance by PMDA Raising Compliance Costs | -0.9% | National, affecting all device categories | Medium term (2-4 years) |

| Price Revision Policies under NHI Driving Down Device ASPs | -1.3% | National, with greater impact in high-volume centers | Medium term (2-4 years) |

| Talent Shortage in Electrophysiology Subspecialty Limits Ablation Adoption | -0.8% | National, with acute impact in rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price revision policies under NHI reduce device ASPs

Japan’s biennial NHI price review slashed balloon catheter reimbursement from JPY 300,000 to JPY 32,000 and drug-eluting stents from JPY 421,000 to JPY 136,000 between 2022 and 2024. The Central Social Insurance Medical Council forecasts an additional 4% cut in 2025 after detecting a 6% divergence between invoice prices and real-world purchasing costs. Continuous price erosion forces manufacturers to launch value-added upgrades just to maintain revenue trajectories.

Talent shortage in electrophysiology subspecialty

Japan has roughly 40% fewer electrophysiologists per capita than the United States. That scarcity limits adoption of advanced ablation catheters and 3D mapping platforms beyond major universities. The University of Tokyo Hospital has expanded fellowships, but the multiyear training cycle means the gap will persist through 2030. Vendors are countering with automated navigation software and single-shot pulsed-field ablation devices that shorten procedures and lower operator skill thresholds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Therapeutic dominance meets diagnostic innovation

Therapeutic & surgical devices generated 75.72% of 2025 revenue. Coronary stents, rhythm-management implants, and heart valves lead the pack, even though biennial price cuts challenge legacy platforms. Emerging trends include drug-coated balloons for complex lesions and polymer-free stents aimed at speeding endothelial healing.

Diagnostic & monitoring devices presently account for 24.28% of value but will outpace therapeutics with a 6.72% CAGR. Remote cardiac monitors, AI-enhanced ECG analyzers, and home-based hemodynamic sensors headline growth. The 2025 relaxation of direct-to-consumer advertising rules has already boosted retail sales of wearable ECG patches. Community clinics connect those devices to cloud platforms, allowing cardiologists in urban centers to interpret rural patient data in real time.

By Application: Structural heart momentum outpaces traditional coronary focus

Coronary artery disease remains the largest application, claiming 42.12% of Japan cardiovascular devices market share in 2025. High PCI volumes and rising diabetes prevalence preserve demand for drug-eluting stents and optical coherence tomography (OCT) imaging.

Structural & congenital heart defect therapies are expanding fastest with a 6.89% CAGR. Widespread adoption of TAVI, mitral repair clips, and emerging tricuspid technologies is reshaping procedural mix. Domestic firms such as Japan Lifeline are partnering with foreign valve innovators to customize devices for Japanese anatomies.

Heart failure & cardiomyopathy solutions—ventricular assist devices, implantable loop recorders, and pressure-sensing shunts—occupy a growing niche as guideline updates emphasize early device therapy. Arrhythmia and conduction disorders grow steadily yet below potential owing to the electrophysiology talent gap, while peripheral vascular disease gets uplift from nationwide smoking-cessation campaigns that highlight limb-ischemia screening.

By End User: Ambulatory settings challenge hospital dominance

Hospitals & cardiac centers held 64.85% revenue in 2025, backed by full-service catheter labs and hybrid operating rooms. Yet tightening reimbursement and push for shorter stays steer selected procedures to specialized outpatient sites. The Japan cardiovascular devices market size in hospitals is projected to advance at 4.72% CAGR, slower than the overall market.

Ambulatory surgical centers are set to produce the quickest 6.48% CAGR, fueled by streamlined PCI suites and same-day TAVI initiatives. They attract urban patients seeking convenience and lower copayments. Cardiology/EP clinics thrive on device follow-ups and ablation aftercare, while home-care & remote monitoring programs, though small, expand rapidly as insurers reimburse telemetric heart failure management.

Geography Analysis

Urban mega-regions—Tokyo, Osaka-Kansai, and Nagoya-Chukyo—concentrate most high-complexity cardiovascular procedures because they house tier-one academic hospitals and experienced operators. These areas capture more than half of Japan cardiovascular devices market revenue. By contrast, rural Tohoku and Shikoku prefectures struggle with specialist shortages; hence remote monitoring devices see disproportionate demand there. National policy targets closing the gap through the “Vision for the Medical Device Industry 2024,” which funds decentralized clinical trials and subsidizes tele-cardiology rollouts.

Regional health-tech clusters are emerging: Kyushu focuses on catheter R&D, while Hokuriku promotes biomaterial patches made from regional biotech know-how. The upcoming Japan Health 2025 expo in Osaka will showcase these localized innovations to global investors. Demand trajectories vary by disease burden: Okinawa, despite its younger demographic, spends heavily on rhythm management because of genetically linked Brugada syndrome, whereas Hokkaido’s older populace drives valve repair volumes.

Japan’s universal coverage ensures that even remote prefectures have baseline access to PCI and pacemaker implants. However, procedural waiting times remain longer outside metropolitan areas, amplifying the importance of early detection programs. The national e-Health rollout aims to link every rural clinic to cloud ECG analytics by 2027, further integrating regional demand into a single, data-driven Japan cardiovascular devices market.

Regulatory Landscape

Japan regulates cardiovascular devices, including drug-device combination products, under the Pharmaceuticals and Medical Devices Act (PMD Act), with scientific review led by the Pharmaceuticals and Medical Devices Agency (PMDA) and marketing authorization granted by the Ministry of Health, Labour and Welfare (MHLW). For combination products, Japan uses a primary mode of action approach and generally expects a single filing pathway aligned to the primary regulated component, which can create parallel evidence expectations for the non-primary constituent (for example, a device element embedded in a drug-led submission).

Regulatory requirements also emphasize structured pre-submission engagement and post-market obligations. PMDA communications in 2025, including multiple Early Consideration publications, and the May 2026 update to provisional guidance covering software as a medical device (SaMD) and integrity expectations underscore the need for clinical evidence planning, cybersecurity and data integrity controls for connected monitors, and readiness for intensive post-market surveillance for cardiovascular implants and high-risk interventions.

Value Chain Analysis

The Japan cardiovascular devices value chain starts with specialized raw materials and components (medical-grade polymers, metals, batteries, sensors, coatings, and catheter sub-assemblies), then moves into device design, verification/validation, and manufacturing under a quality management system aligned with Japan QMS requirements (Ordinance No. 169, aligned with ISO 13485). For drug-device combinations, development and manufacturing coordination extends to drug constituent controls, stability, and packaging configuration, adding complexity when the primary regulatory category differs from the secondary constituent.

Commercialization is shaped by Japan’s Marketing Authorization Holder (MAH) structure: a domestic MAH bears legal responsibility for quality and vigilance (GQP and GVP compliance). As a result, foreign manufacturers often work with a local partner or designated MAH for importation, release, and post-market duties. Distribution typically runs through established domestic networks into hospitals and cardiac centers, with growing reach into ambulatory surgical centers and clinic-led diagnostics. Key bottlenecks include limited supplier options for specialized components, low-volume procurement challenges for niche cardiovascular parts, and the regulatory burden involved in changing materials or components, which can slow qualification of alternate suppliers and raise the risk of supply disruption.

Competitive Landscape

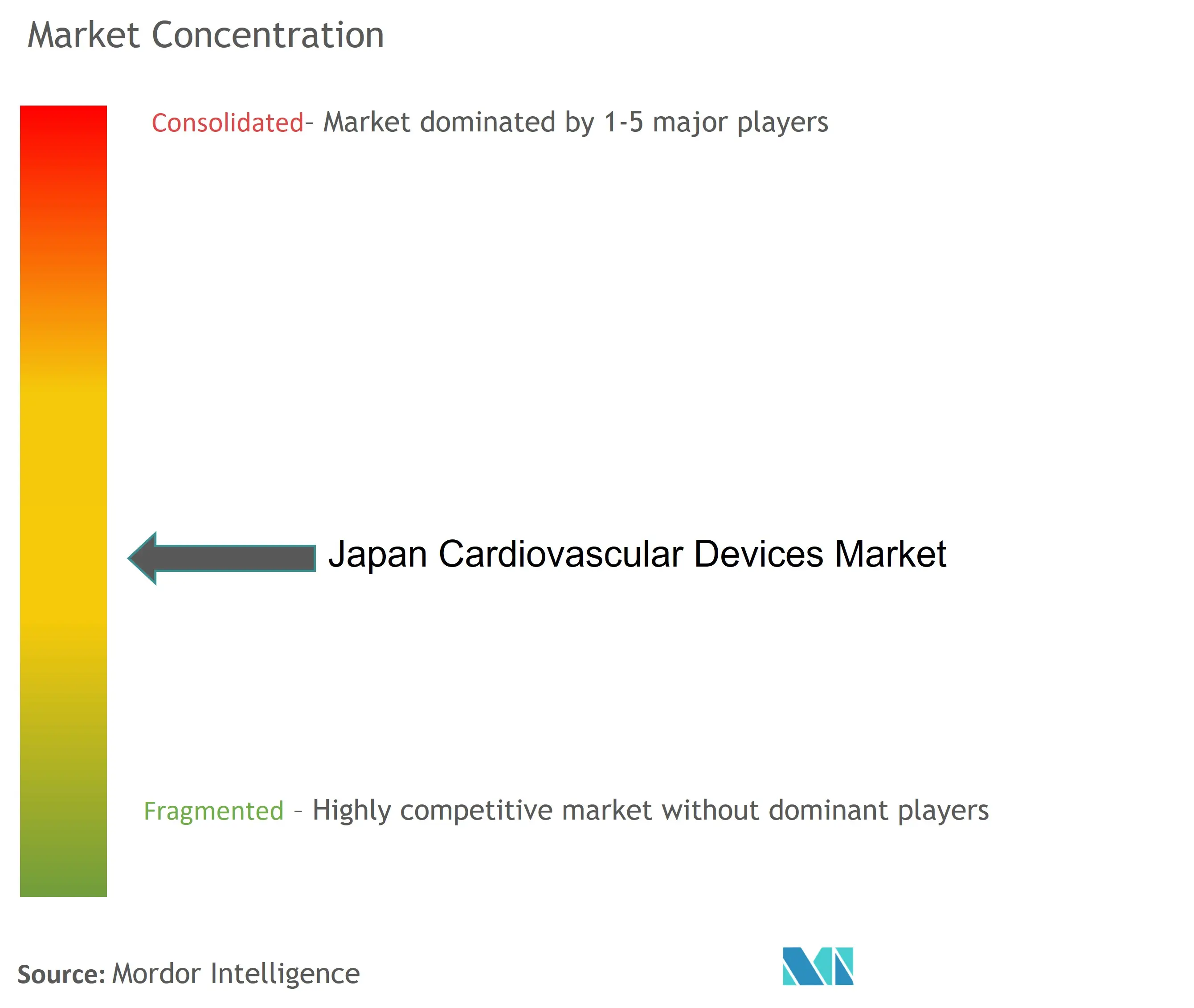

Global heavyweights—Medtronic, Abbott, Boston Scientific, and Johnson & Johnson— while domestic champions such as Terumo, Asahi Intecc, Fukuda Denshi, and Japan Lifeline bring combined share to nearly more than half of market revenue. That configuration marks a moderately concentrated environment. Recent moves illustrate the dual imperative of technology leadership and local presence: GE HealthCare purchased the remaining 50% of Nihon Medi-Physics to deepen diagnostic imaging reach, and Kaneka bought Endostream Medical to acquire catheter IP optimized for structural heart disease.

Price-erosion pressure prompts tier-two suppliers to bundle service packages—predictive analytics, training, and inventory management—to protect margins. Artificial intelligence becomes a differentiator: Nihon Kohden’s AI ECG platform targets detection of silent atrial fibrillation in seniors, while Omron integrates hypertensive DTx into BP monitors for home use [nature.com]. Talent scarcity in electrophysiology also influences strategic direction: vendors are racing to develop pulsed-field ablation catheters that minimize learning curves and radiation exposure.

White-space opportunities include patient-specific grafts produced via 3-D printing, biodegradable vascular patches such as Teijin’s PMDA-cleared platform, and compact ventricular assist devices tailored for low-BMI Asian patients. The Japan cardiovascular devices industry continues to witness alliances that marry overseas R&D with Japanese distribution acumen, exemplified by Boston Scientific’s bid for laser lithotripsy specialist Bolt Medical aimed at calcified lesion management in the elderly

Japan Cardiovascular Devices Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Cardinal Health Inc

Edwards Lifesciences

Medtronic PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Remote diagnostics and software-enabled cardiovascular care represent a clear whitespace as Japan expands screening and connected monitoring across community clinics and home settings. Mandatory annual ECG exams for employees aged 35+ generate roughly 40 million recordings each year, and 2025 Japanese Heart Rhythm Society guidance encouraging wearable ECG use supports broader adoption of cloud-connected monitoring workflows. PMDA’s use of registries for post-marketing surveillance also favors vendors that can pair devices with real-world evidence generation, which supports more iterative upgrades in monitors, implants, and catheter-based therapies.

Structural heart and complex coronary interventions remain opportunity areas where reimbursement and technology upgrades intersect, while cost containment continues to pressure legacy portfolios under NHI price revision cycles. Programs that strengthen domestic innovation capacity also expand the addressable partner base, including AMED initiatives that fund medical device creation and startup support to translate catheter, biomaterials, and digital health R&D into commercial candidates. At the same time, regulatory modernization steps, including ongoing PMDA guidance updates around SaMD integrity expectations, increase demand for compliant cybersecurity, data governance, and interoperable platforms across hospitals, cardiac centers, and decentralized care models.

Recent Industry Developments

- May 2026: PMDA released updated provisional guidance addressing software as a medical device (SaMD) and integrity-related expectations. The update elevates compliance requirements for connected cardiac monitoring and diagnostic software, reinforcing investment priorities in cybersecurity, data governance, and post-market performance tracking.

- March 2025: Medtronic launched the Aurora EV-ICD in Japan following local regulatory clearance. The approval broadened competitive options in defibrillation by adding an extravascular approach, supporting differentiation in rhythm management portfolios.

- January 2025: Boston Scientific agreed to acquire Bolt Medical to expand its position in calcium-management technologies for complex coronary disease. The deal indicated continued strategic focus on differentiated interventional tools amid NHI price revisions that compress pricing for mature device categories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Japan cardiovascular devices market is defined as the revenues generated from devices used to diagnose, monitor, and treat heart and vascular conditions across care settings inside Japan, reported in USD.

Scope exclusions: It does not include cardiovascular drugs, general hospital infrastructure, or non-device service revenues such as procedure fees and physician payments.

Segmentation Overview

- By Device Type

- Diagnostics Devices

- ECG Systems

- Remote Cardiac Monitor

- Cardiac MRI

- Cardiac CT

- Echocardiography / Ultrasound

- Fractional Flow Reserve (FFR) Systems

- Therapeutic & Surgical Devices

- Coronary Stents

- Drug-Eluting Stents

- Bare-Metal Stents

- Bioresorbable Stents

- Catheters

- PTCA Balloon Catheters

- IVUS/OCT Catheters

- Cardiac Rhythm Management

- Pacemakers

- Implantable Cardioverter Defibrillators

- Cardiac Resynchronization Therapy Devices

- Heart Valves

- TAVR/TAVI

- Mechanical Valves

- Tissue/Bioprosthetic Valves

- Ventricular Assist Devices

- Artificial Hearts

- Grafts & Patches

- Other Cardiovascular Surgical Devices

- Coronary Stents

- Diagnostics Devices

- By Application

- Coronary Artery Disease

- Arrhythmia & Conduction Disorders

- Heart Failure & Cardiomyopathy

- Structural & Congenital Heart Defects

- Peripheral Vascular Disease

- By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand environment in Japan and to anchor assumptions needed before modeling starts. We relied on public sources such as Japan Ministry of Health, Labour and Welfare releases (including reimbursement and price revision signals), PMDA updates on approvals and safety actions, and statistics from OECD and the World Health Organization on population aging and disease burden.

To keep sizing grounded, we also reviewed import and trade signals from Japan Customs, relevant peer reviewed clinical literature on procedure trends, and disclosures such as company annual reports and investor presentations where Japan exposure is discussed. In a few places, paid subscriptions for company financials and patent databases were used to cross-check product focus and launch timing. These sources are illustrative, and many other public documents and datasets were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys with a mix of device suppliers, distributors, hospital procurement and cath lab stakeholders, and clinician level users who see procedure mix changes in real time. Since this is a Japan-only market, inputs were checked for differences in reimbursement driven adoption, hospital versus ambulatory settings, and the pace at which newer technologies replace older systems.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 19% | |

| Mid tier: 44% | Functional/Unit leaders: 26% | |

| Smaller Players: 19% | Managers: 55% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where procedure and patient pathways are translated into device demand pools, then converted into value using Japan-specific pricing and utilization patterns. When the model is mature, we corroborate results using selective bottom-up approximations such as sampled average selling price times implied volumes for key device groups, then perform channel checks to make sure totals are realistic.

Inputs used in the model include indicators such as coronary intervention activity, rhythm management implant volumes, adoption of remote cardiac monitoring, the share of minimally invasive structural procedures, and reimbursement pricing updates under the national schedule. Because price erosion and mix shifts matter in Japan, we treat average price movement as an explicit driver rather than a single flat uplift.

For forecasting, scenario analysis is run around procedure recovery, technology uptake, and reimbursement pressure, then aligned to what interviewees describe as a reasonable base case. Where bottom-up coverage is incomplete for smaller device categories, gaps are handled through ratio based allocation from closely tracked device groups, and those ratios are re-tested during validation.

Data Validation & Update Cycle

Outputs are validated by comparing modeled totals with independent signals such as procedure trend direction, regulatory approval cadence, and pricing revision expectations, and then checking for unusual jumps across device groups. If a variance is too large to explain with the available signals, assumptions are revisited and respondents may be re-contacted to confirm whether the change is real or timing-related.

Before sign-off, the work is reviewed in multiple steps so that unit logic, currency treatment, and growth drivers remain consistent with the market narrative. Reports are refreshed annually, and interim updates are made when material events occur, such as major reimbursement changes or meaningful shifts in procedure volumes. Right before delivery, a final pass is done so clients receive the latest updated view.

Mordor Intelligence's Japan Cardiovascular Devices Market Size Compared With Other Published Estimates

Published market sizes for Japan cardiovascular devices can look far apart, even when they claim to measure the same space, because category borders and the year used for comparison are not always aligned. The table below summarizes the spread and shows where scope, pricing treatment, and update timing can change the final value.

The biggest gaps usually come from what is counted as a cardiovascular device versus an adjacent hospital product, and whether an estimate emphasizes therapeutic and surgical devices or stays narrow in diagnostics and monitoring. Currency conversion timing, the handling of reimbursement driven price erosion, and the choice of base year versus forecast start year can also move the number up or down in a visible way.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.34 B (2026) | |

| Global Consultancy A | USD 12.40 B (2026) | Uses a broader device universe that can fold in wider peripheral vascular and cardiac surgery related instrument categories, which expands the counted revenue pool beyond the tighter cardiovascular device definition used in many healthcare device trackers. |

| Industry Publisher B | USD 0.04 B (2021) | Appears to concentrate on a narrow diagnostic and monitoring subset and uses an older base year, which makes the reported value much smaller and not directly comparable to a full cardiovascular device market coverage. |

The table shows that most of the spread is explained by scope width and the year chosen for the headline number. In Mordor Intelligence's model, the Japan total is built by counting both therapeutic and surgical device revenues along with diagnostic and monitoring devices, while keeping out non-device clinical services and unrelated hospital spend. With those boundaries explicit, the sizing steps stay traceable to procedure activity, price movement, and adoption indicators that can be re-checked each refresh cycle.

Key Questions Answered in the Report

What is the current size of the Japan cardiovascular devices market?

The market is valued at USD 3.34 billion in 2026, with projections indicating it will climb to USD 4.41 billion by 2031.

Which device segment is growing fastest in Japan?

Diagnostic & monitoring devices are expanding at a 6.72% CAGR (2026-2031), driven by wearable ECG adoption and AI-based analytics.

How does Japan’s aging population affect market growth?

With 29.1% of citizens over 65, age-linked cardiac conditions drive sustained demand for stents, valves, and rhythm management implants.

Why are reimbursement reforms important for device makers?

Enhanced codes for TAVI and PCI boost procedure volumes and justify investment in premium technologies despite NHI price cuts.

Page last updated on: