Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

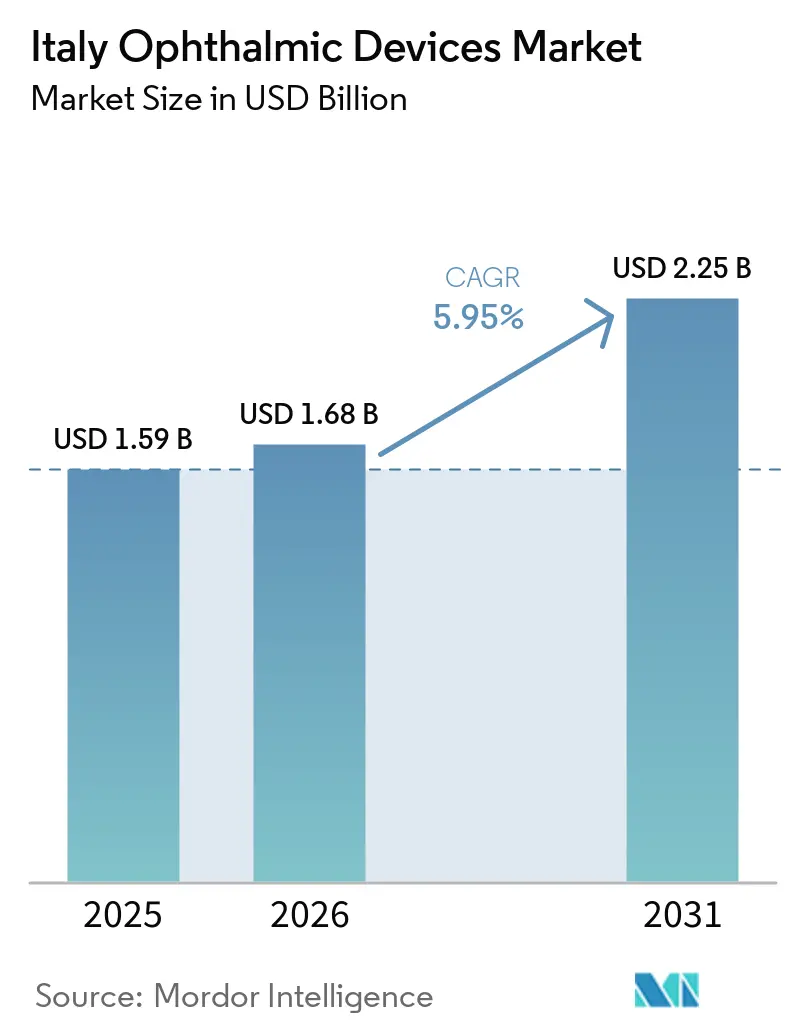

| Base Year Market Size (2025) | USD 1.59 Billion |

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 2.25 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Ophthalmic Devices Market Analysis by Mordor Intelligence

The Italy ophthalmic devices market size is expected to grow from USD 1.59 billion in 2025 to USD 1.68 billion in 2026 and is forecast to reach USD 2.25 billion by 2031 at 5.95% CAGR over 2026-2031. This trajectory is powered by a rapidly aging population, a southern European diabetes cluster, and Milan’s unique ability to merge medical need with fashion-forward eyewear demand. Hospitals dominate complex surgery volumes, yet ambulatory surgery centers (ASCs) are scaling quickly as Piano Nazionale di Ripresa e Resilienza (PNRR) grants modernize outpatient infrastructure. At the same time, corporate optical chains deepen market consolidation while EU-MDR rules slow the speed of new product launches, indirectly protecting incumbents with seasoned compliance functions. These dynamics collectively shape the competitive rhythm of the Italy ophthalmic devices market.

Key Report Takeaways

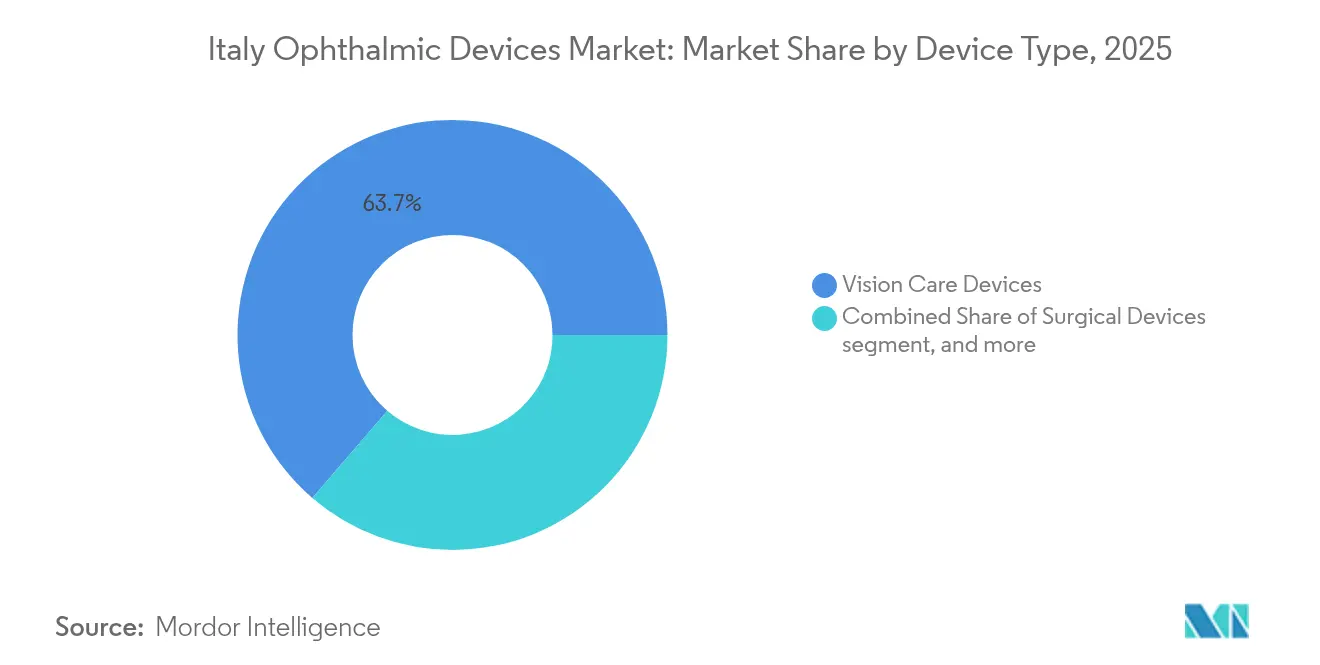

- By device type, vision care devices held 63.70% of the Italy ophthalmic devices market share in 2025, whereas diagnostic & monitoring devices are projected to post an 8.02% CAGR through 2031.

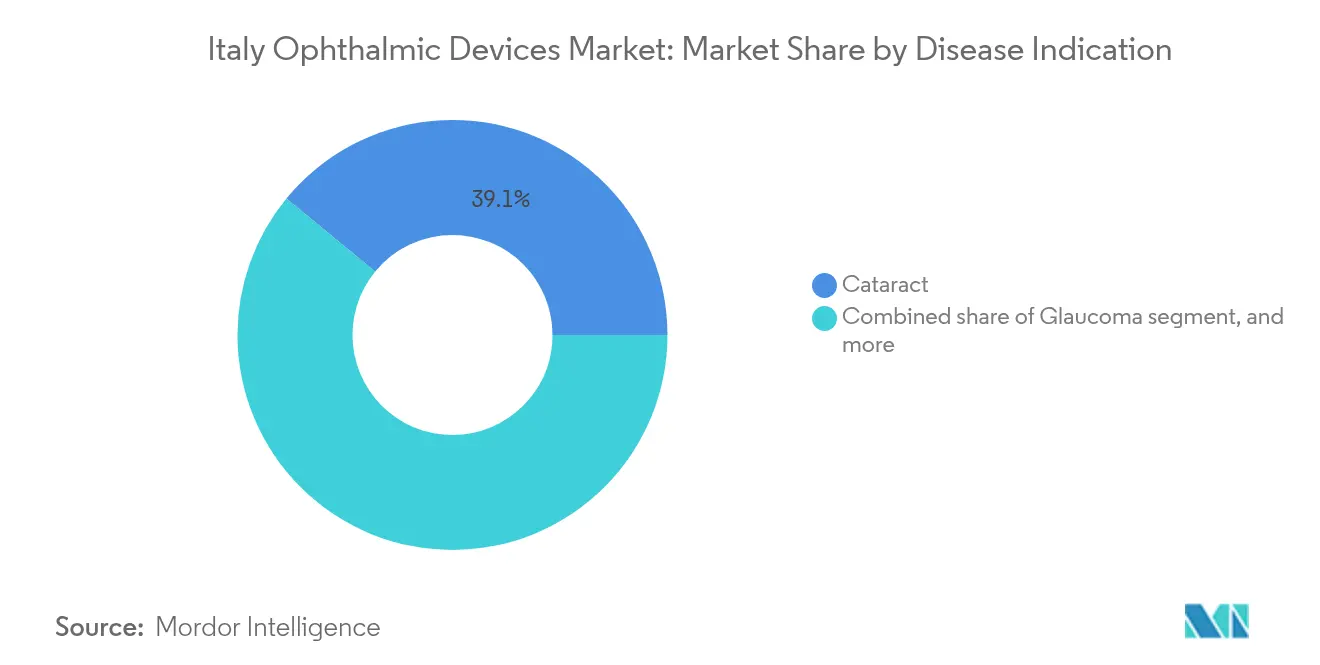

- By disease indication, cataract solutions accounted for 39.05% of the Italy ophthalmic devices market size in 2025 while diabetic retinopathy devices are poised to expand at 7.21% CAGR over 2026-2031.

- By end user, hospitals captured 44.60% of the Italy ophthalmic devices market share in 2025, and ASCs are advancing at a 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Ophthalmic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetic retinopathy & AMD | +2.0% | Northern regions (Lombardy, Veneto, Emilia-Romagna) | Medium term (2-4 years) |

| High per-capita eyewear spending driven by Milan fashion cluster | +1.7% | Nationwide (peak in Lombardy) | Long term (≥4 years) |

| Rapid public-hospital adoption of femtosecond & excimer lasers | +1.5% | Nationwide | Short term (≤2 years) |

| Government PNRR funding for ASC upgrades | +1.2% | Southern & central regions | Medium term (2-4 years) |

| Expansion of corporate optical retail chains | +1.0% | Major urban centers | Long term (≥4 years) |

| Domestic IOL contract-manufacturing base lowering procurement costs | +0.8% | Industrial hubs in Northern & Central Italy | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetic Retinopathy & AMD In Northern Italy

Northern provinces now report diabetic retinopathy (DR) rates as high as 39% among adults with diabetes, a burden that elevates demand for spectral-domain OCT scanners, ultra-wide-field fundus cameras, and tele-ophthalmology kits. Screening uptake hovers below 50%, creating latitude for community-based programs that route retinal images to tertiary centers for rapid reads. Direct DR treatment costs lie between EUR 4,050 and 5,799 per patient, an outlay that convinces payers to reimburse technologies that catch pathology sooner rather than later. In response, vendors bundle artificial-intelligence triage algorithms with hardware to shorten interpretation times and unlock incremental revenue in the Italy ophthalmic devices market.

High Per-Capita Eyewear Spending Driven by Fashion Industry Clustering in Milan

Milan’s global fashion pull reframes glasses as lifestyle accessories, allowing “Made in Italy” labels to command premium price points even during macroeconomic volatility. Exports still totaled EUR 5.236 billion in 2024 despite a fractional 0.6% dip from the prior year, underscoring the resilience of high-end frames[1]ANFAO, “Italian Eyewear Export Performance 2024,” anfaonet.it. Younger professionals favor recycled acetate and bio-based polymers, driving a sustainability narrative that enhances margins. Omnichannel corporate chains amplify brand storytelling with digitally enabled fittings, strengthening their grip on the Italy ophthalmic devices market.

Rapid Public-Hospital Adoption of Femtosecond & Excimer Laser Platforms

Public hospitals increasingly install femtosecond and excimer systems to boost throughput and improve refractive precision. Transepithelial PRK, supported by platforms such as Schwind Amaris, now enjoys guideline recognition by the European Society of Cataract and Refractive Surgeons (ESCRS) for its post-operative comfort and speed of recovery[2]European Society of Cataract and Refractive Surgeons, “2024 Clinical Practice Guidelines,” escrs.org. Hospitals leverage bundled service contracts to guarantee uptime, a strategy that cements platform loyalty and fuels replacement cycles inside the Italy ophthalmic devices market.

Government PNRR Funding for ASC Upgrades

Roughly EUR 20 billion in PNRR health allocations flow toward ASC expansion, most notably in Calabria, Apulia, and Sicily. Grants fund laminar airflow theaters, high-definition microscopes, and cloud-linked diagnostic suites, facilitating same-day bilateral cataract procedures and easing surgical backlogs. Modernized ASCs offer ophthalmologists autonomy, shorter turnover times, and predictable scheduling, conditions that accelerate their 7.38% CAGR within the Italy ophthalmic devices market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy EU-MDR conformity approval cycles | –1.6% | Nationwide | Short term (≤2 years) |

| Price caps imposed by SSN tenders | –1.3% | Nationwide | Long term (≥4 years) |

| Shortage of ophthalmologists in Southern regions | –1.1% | Southern regions | Medium term (2-4 years) |

| Rising post-operative endophthalmitis litigation risk | –0.9% | Nationwide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Lengthy EU-MDR Conformity Approval Cycles Delaying Product Launches

The 2021 EU-MDR regime increases data requirements, post-market surveillance steps, and unique device identification mandates. Smaller domestic innovators now face certification delays up to 18 months, pushing commercialization milestones and elevating costs[3]Lucia Contardi, “EU-MDR Challenges for Italian Manufacturers,” Regulatory Affairs Journal, raam.it. Limited notified-body capacity prioritizes certificate renewals over new submissions, giving multinational incumbents a timing advantage and slowing innovation flow into the Italy ophthalmic devices market.

Price Caps Imposed By Servizio Sanitario Nazionale (SSN) Tenders

Centralized SSN tenders fix ceiling prices for implants, disposables, and diagnostics, compressing margins on high-precision products. Hospitals supply 45.2% of overall volume, so tender success remains critical even when profits are slim. Manufacturers balance compliance by offering dual-tier portfolios: value lines for public bids and premium variants for private clinics, safeguarding profitability across the Italy ophthalmic devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Fashion Drives Vision Care Dominance

Vision care devices secured 63.70% of the Italy ophthalmic devices market in 2025, propelled by domestic design strength and high per-capita eyewear replacement cycles. Premium acetate frames now retail near EUR 250 and frequently integrate smart coatings for blue-light absorption, reflecting consumer readiness to invest in performance and aesthetics. Contact lenses ride a hygiene-focused tailwind, with daily disposables outpacing monthlies as urban professionals choose convenience over price. Meanwhile diagnostic & monitoring devices represent the fastest-growing slice, expanding at an 8.02% CAGR as hospitals upgrade to spectral-domain OCT units that interface with AI triage software. The Attention-Based DenseNet model recently validated for OCT segmentation with 0.9792 accuracy adds clinical momentum for imaging investments. These dynamics cement multi-year demand certainty for suppliers in the Italy ophthalmic devices market.

Second-generation point-of-care tonometers, handheld fundus cameras, and cloud-linked slit lamps further widen the technological scope of the Italy ophthalmic devices market. Vendors increasingly bundle analytics dashboards that integrate Electronic Health Record (EHR) data, allowing clinicians to track disease progression and streamline referrals. Portfolio depth thus becomes a differentiator as hospitals seek single-source partners to simplify procurement compliance.

By Disease Indication: Diabetic Retinopathy Drives Growth

Cataract devices commanded 39.05% of the Italy ophthalmic devices market share in 2025, supported by roughly 380,000 surgical cases across public and private theaters. Growing patient preference for multifocal and toric intraocular lenses raises procedure value, especially in private clinics where out-of-pocket payment is common. Northern surgeons now report femtosecond laser usage in 38% of cataract cases, citing superior wound construction and astigmatism control.

Diabetic retinopathy devices grow at 7.21% CAGR and stand at the forefront of innovation within the Italy ophthalmic devices market. Tele-ophthalmology pilots supply pharmacies and primary-care offices with portable cameras, routing images to cloud services for AI-assisted grading. The estimated treatment cost burden nudges payers to reimburse early detection, driving adoption in both urban and rural settings. Academic centers in Verona and Bologna trial retinal function biomarkers to refine DR staging, hinting at future device demand beyond traditional imaging.

By End User: ASCs Gain Momentum Through PNRR Funding

Hospitals held 44.60% of the Italy ophthalmic devices market size in 2025 due to their role in handling complex vitreoretinal, pediatric, and oncology cases. Quality benchmarking through the National Outcome Assessment Program (PNE) nudges administrators to invest in high-resolution devices that document success metrics. Clusters around Milan, Padua, and Rome lead technology refresh cycles and often function as early adopters in multicenter trials.

ASCs, forecast to grow 7.12% CAGR, represent the agility arm of the Italy ophthalmic devices market. The Ardian acquisition of Vista Vision illustrates private-equity appetite for high-volume specialty networks. Refurbished centers leverage modular theaters and optimized patient flow, achieving same-day throughput that appeals to surgeons seeking predictable schedules and patients seeking fast recovery. Device suppliers respond with flexible leasing plans and service contracts tailored to outpatient economics, positioning themselves for recurring income streams.

Geography Analysis

Northern Italy generates the lion’s share of revenue within the Italy ophthalmic devices market. Lombardy alone houses about 25% of the nation’s ophthalmologists, fostering early adoption of AI-ready OCT units and femtosecond lasers. Milan and Turin’s industrial ecosystems streamline distribution logistics for frames, lenses, and surgical disposables, reducing lead times and supporting aggressive promotional calendars. Veneto’s university-hospital clusters partner with startups on machine-learning algorithms that mine perimetry and imaging datasets, underscoring a research-to-clinic feedback loop that accelerates innovation.

Central regions such as Lazio and Tuscany post steady device uptake anchored by mixed public-private delivery models. Rome’s medical-tourism inflow lifts premium intraocular-lens volumes, while Florence leverages its craftsmanship heritage to market luxury eyewear lines to both locals and tourists. Public-private partnerships roll out mobile screening vans to peri-urban communities, filling care gaps and improving diabetic retinopathy detection rates. Vendors active in this corridor pivot marketing narratives toward preventive care and lifestyle alignment to resonate with middle-income households.

Southern Italy lags in penetration but offers pronounced upside for the Italy ophthalmic devices market as PNRR assignments refurbish ASCs in Calabria, Apulia, and Sicily. Shorter travel distances for routine cataract surgery reduce no-show rates and improve access, cataract surgery device makers that deliver turnkey operating-room setups with surgeon training programs gain footing in these price-sensitive, high-potential zones. Local medical schools now integrate tele-ophthalmology rotations, ensuring a future workforce familiar with remote diagnostic workflows.

Competitive Landscape

The Italy ophthalmic devices market sits in a moderate-concentration band, as the top five suppliers together capture about 60% of revenue yet niches remain for specialized entrants. EssilorLuxottica dominates the vision-care segment through 17,500 global retail sites and a vertically integrated supply chain. Its 2024 licensing agreement with Diesel injects fresh fashion capital into eyewear assortments, reinforcing front-of-store brand visibility. Alcon leads surgical equipment with iterative software enhancements on the Centurion phaco platform, while Johnson & Johnson Vision scales dual-focus lenses under the TECNIS Synergy banner.

Carl Zeiss Meditec cements diagnostic leadership via the CIRRUS OCT line, and Topcon continues to support community screening programs with portable fundus cameras. Thirty-six AI-driven image-analysis devices now carry EU clearance, the majority focused on diabetic retinopathy screening. Researchers, however, call for deeper peer-review pipelines to confirm real-world performance across Italy’s ethnically diverse population.

White-space growth opportunities cluster around cloud-native analytics platforms, home-monitoring devices for age-related macular degeneration, and sustainable frame materials aligned with EU circular-economy goals. Start-ups addressing these niches often partner with academic hospitals for clinical validation and tap venture funds keen on digital-health portfolios within the Italy ophthalmic devices market.

Italy Ophthalmic Devices Industry Leaders

Alcon Inc

Carl Zeiss Meditec AG

Johnson & Johnson Vision

Bausch + Lomb Corp.

EssilorLuxottica S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: iCare confirmed its MAIA microperimeter is in final preparation, with a commercial launch scheduled for Q1 2025.

- December 2024: EssilorLuxottica announced a definitive agreement to acquire Espansione Group, a maker of non-invasive devices for dry-eye and retinal-disease care.

Italy Ophthalmic Devices Market Report Scope

As per the scope of the report, ophthalmology is a branch of medical sciences that deals with the structure, function, and various diseases related to the eye. Ophthalmic devices are medical equipment for diagnosis, surgical, and vision correction purposes.

The Italian ophthalmic devices market is segmented by devices (surgical devices, diagnostic and monitoring devices, and vision correction devices). The report offers the value (in USD million) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | |

| Autorefractors & Keratometers | |

| Corneal Topography Systems | |

| Ultrasound Imaging Systems | |

| Perimeters & Tonometers | |

| Other Diagnostic & Monitoring Devices | |

| Surgical Devices | Cataract Surgical Devices |

| Vitreoretinal Surgical Devices | |

| Refreactive Surgical Devices | |

| Glaucoma Surgical Devices | |

| Other Surgical Devices | |

| Vision Care Devices | Spectacles Frames & Lenses |

| Contact Lenses |

By Disease Indication

| Cataract |

| Glaucoma |

| Diabetic Retinopathy |

| Other Disease Indications |

By End-user

| Hospitals |

| Specialty Ophthalmic Clinics |

| Ambulatory Surgery Centers (ASCs) |

| Other End-users |

| By Device Type | Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | ||

| Autorefractors & Keratometers | ||

| Corneal Topography Systems | ||

| Ultrasound Imaging Systems | ||

| Perimeters & Tonometers | ||

| Other Diagnostic & Monitoring Devices | ||

| Surgical Devices | Cataract Surgical Devices | |

| Vitreoretinal Surgical Devices | ||

| Refreactive Surgical Devices | ||

| Glaucoma Surgical Devices | ||

| Other Surgical Devices | ||

| Vision Care Devices | Spectacles Frames & Lenses | |

| Contact Lenses | ||

| By Disease Indication | Cataract | |

| Glaucoma | ||

| Diabetic Retinopathy | ||

| Other Disease Indications | ||

| By End-user | Hospitals | |

| Specialty Ophthalmic Clinics | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Other End-users | ||

Key Questions Answered in the Report

What is the current size of the Italy ophthalmic devices market?

The Italy ophthalmic devices market size is USD 1.68 billion in 2026.

How fast is the market expected to grow?

It is forecast to expand at a 5.95% CAGR, reaching USD 2.25 billion by 2031.

Which device category leads the market today?

Vision care devices lead with 63.70% share, driven by Milan’s fashion-centric eyewear culture.

Which disease indication segment is growing fastest?

Devices addressing diabetic retinopathy register the fastest CAGR at 7.21% due to rising diabetes prevalence and expanded screening.

Why are ambulatory surgery centers important to future growth?

PNRR funding accelerates ASC expansion, enabling more outpatient cataract and refractive surgeries and supporting a 7.12% CAGR in this end-user segment.

How do EU-MDR rules affect Italian manufacturers?

Stricter conformity assessments delay new product launches, favoring large incumbents with established regulatory infrastructure.

Page last updated on: