Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

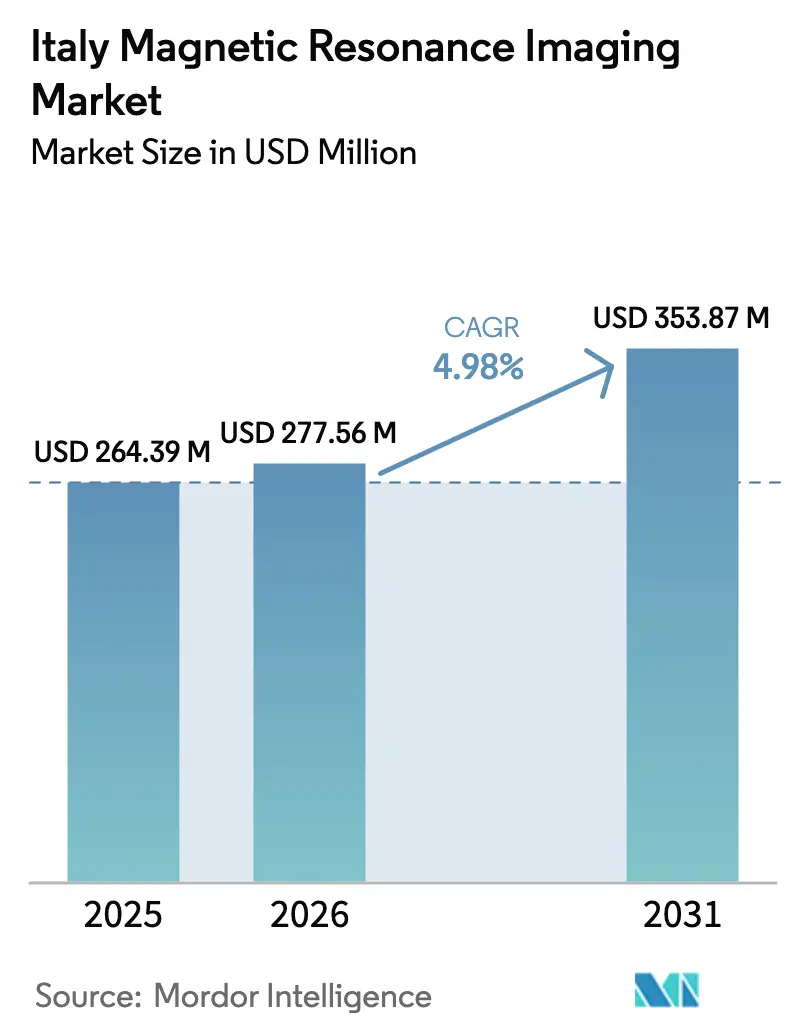

| Base Year Market Size (2025) | USD 264.39 Million |

| Market Size (2026) | USD 277.56 Million |

| Market Size (2031) | USD 353.87 Million |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Magnetic Resonance Imaging Market Analysis by Mordor Intelligence

Italy MRI market size in 2026 is estimated at USD 277.56 million, growing from 2025 value of USD 264.39 million with 2031 projections showing USD 353.87 million, growing at 4.98% CAGR over 2026-2031. Growth rests on three pillars: the National Recovery and Resilience Plan, the country’s rapidly aging demographic profile, and continuous technology upgrades that shorten scan times and broaden clinical indications. Rising incidence of cancer and neurodegenerative disorders keeps demand for high-resolution, non-ionizing imaging on an upward curve, while value-based procurement models encourage hospitals to replace helium-intensive equipment with energy-efficient platforms. Portable scanners widen geographic access in underserved regions, and AI-enabled workflow tools increase patient throughput, partially offsetting MRI workforce shortages.

Key Report Takeaways

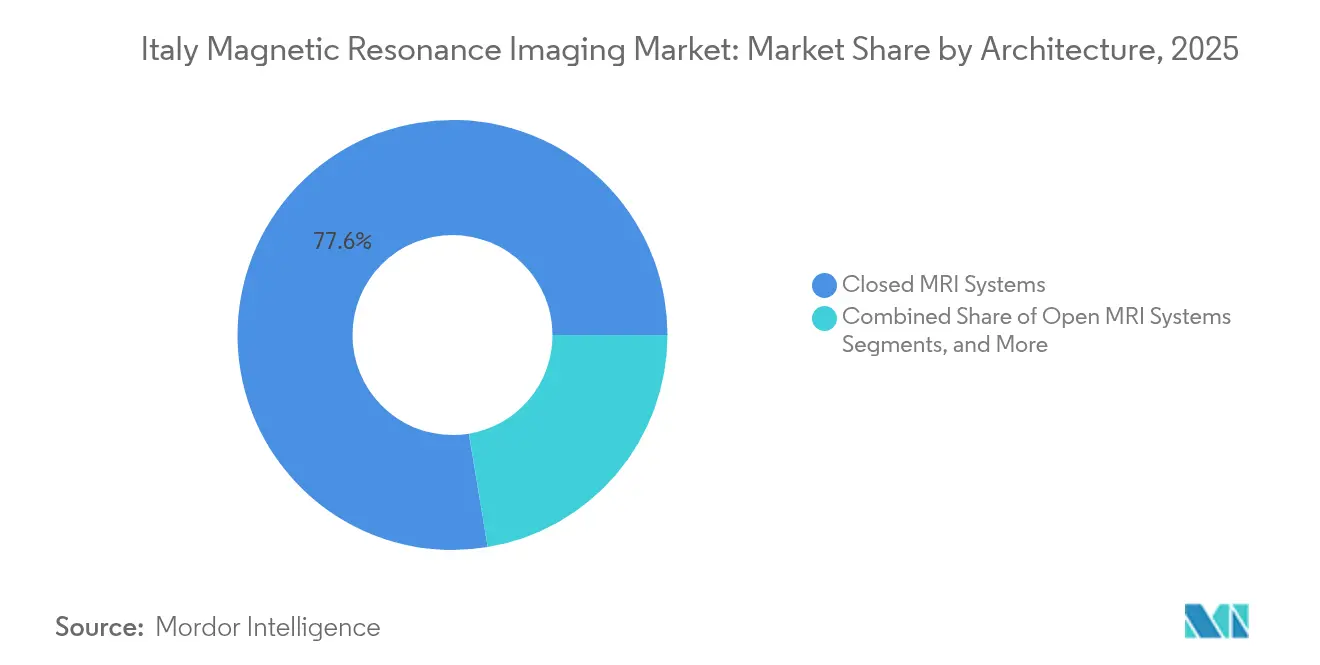

- By architecture, closed MRI systems led with 77.62% of Italy MRI market share in 2025; portable MRI systems are forecast to rise at a 5.32% CAGR through 2031.

- By field strength, mid-field (0.5–1.5 T) units controlled 47.65% of Italy MRI market size in 2025, whereas ultra-high field (>3 T) units are expected to expand at a 5.58% CAGR to 2031.

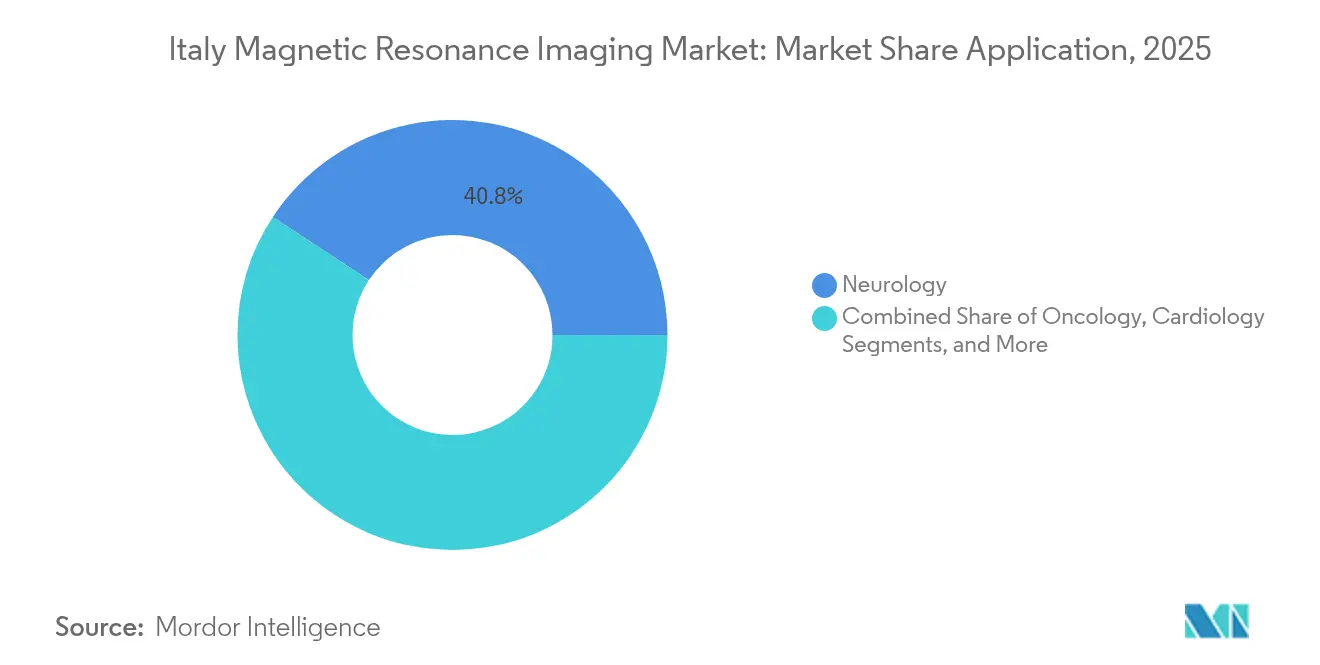

- By application, neurology captured 40.75% Italy MRI market share in 2025; oncology is on track for the fastest 5.93% CAGR through 2031.

- By end user, hospitals commanded 66.80% of the Italy MRI market size in 2025; diagnostic imaging centers are projected to grow at a 5.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Magnetic Resonance Imaging Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising chronic-disease imaging demand | +1.2% | National, concentrated in Northern regions | Medium term (2-4 years) |

| National Recovery & Resilience (PNRR) cap-ex for MRI upgrades | +1.8% | National, with priority to underserved Southern regions | Short term (≤ 2 years) |

| Technological breakthroughs in MRI | +0.9% | National, early adoption in major urban centers | Long term (≥ 4 years) |

| Steady growth in healthcare spending and modernization | +0.7% | National, regional variations in implementation | Medium term (2-4 years) |

| Expanding clinical indications for MRI | +0.8% | National, specialty centers leading adoption | Medium term (2-4 years) |

| Shift toward patient-centric, non-ionizing diagnostic alternatives | +0.6% | National, driven by patient awareness campaigns | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Recovery & Resilience (PNRR) Cap-ex for MRI Upgrades

Italy’s EUR 194.4 billion PNRR channels unprecedented funds toward hospital equipment modernization, opening a short procurement window that favors immediate replacement of aging scanners [1]Italia Domani, “Piano Nazionale di Ripresa e Resilienza,” Presidency of the Council of Ministers, italia-domani.gov.it. Revised community‐hospital targets, cut from 1,350 to 936 because of construction-cost inflation, still translate into hundreds of new MRI installations. The complementary Piano Transizione 5.0 adds EUR 12.7 billion in tax credits for facilities that cut energy consumption by at least 3%, effectively subsidizing zero-boil-off magnets. Together, these measures accelerate purchasing decisions, especially in Southern regions that historically lagged in imaging capacity.

Rising Chronic-Disease Imaging Demand

Population aging to 24% above 65 years fuels MRI use across neurology, oncology, and cardiology. Alzheimer’s prevalence already tops 413,715 patients and drives neuroimaging protocols that add to scanner workloads. Annual cancer incidence reached 390,700 cases in 2022 and is poised for a further 15% increase by 2025, intensifying demand for precise staging and follow-up imaging. AI-based reconstruction tools cut scan time by as much as 30%, enabling higher daily volumes without compromising image quality.

Technological Breakthroughs in MRI

Innovation centers on helium-free magnets, zero-click planning, and ultra-high field research platforms. Siemens Healthineers introduced a virtually helium-free 1.5 T system that eases siting constraints and slashes lifecycle costs [2]Siemens Healthineers, “Virtually Helium-Free MRI: The Future of Sustainable Imaging,” siemens-healthineers.com. Philips and NVIDIA are co-developing foundational AI models that automate pathology detection to further improve turnaround times. At the University of Pisa, 7 T imaging demonstrated 84% vascular-parameter detection compared with digital subtraction angiography, underscoring the clinical potential of ultra-high field technology.

Expanding Clinical Indications for MRI

Whole-body protocols now guide metastatic prostate cancer management with higher sensitivity than conventional imaging and no contrast agent. AI-enhanced cardiac scans predict arrhythmia risk and fine-tune ablation strategies. MRI-compatible robotic tools enable real-time neurosurgical navigation, evidenced by early adoption at Ospedale San Raffaele in Milan.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment & lifecycle costs | -1.4% | National, acute in South | Short term (≤ 2 years) |

| Slow, fragmented reimbursement approvals | -0.8% | National, regional variations | Medium term (2-4 years) |

| Shortage of MRI-trained personnel | -1.1% | National, severe in peripheral areas | Long term (≥ 4 years) |

| Volatile helium & energy prices | -0.7% | National, affecting legacy systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Equipment & Lifecycle Costs

New scanners range between USD 1 million and USD 3 million, while service contracts consume 8–12% of purchase price annually [3]DirectMed Imaging, “Total Cost of MRI Ownership,” directmedparts.com. Helium refill prices have soared 250% over ten years, pushing annual outlays to USD 28,000–36,000 for older magnets. Energy audits in Italian radiology departments show MRI units account for 24% of daily departmental electricity at 214.6 kWh, eroding hospital budgets.

Shortage of MRI-Trained Technologists & Radiologists

More than 11,000 physicians quit the National Health Service from 2019–2022, leaving radiology departments understaffed. Technologist vacancies rose to 18.1% in 2024, nearly triple 2021 levels, prolonging patient wait times. Recruitment challenges are most acute in peripheral regions that offer fewer career development opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Portable Innovation Challenges Traditional Dominance

Closed scanners kept 77.62% of Italy MRI market share in 2025, favored for image quality, multichannel coils, and high diagnostic confidence in oncology and neurology. The Italy MRI market size for portable units is modest today yet rising quickly; portable platforms are forecast to record a 5.32% CAGR between 2026-2031. Adoption is fastest in emergency departments and rural clinics where space and helium logistics restrict classic cylindrical designs. Manufacturers are integrating AI reconstruction to uplift image quality, shrinking the performance gap versus closed systems.

Portable scanners support Italy’s goal of equitable access, particularly in Calabria and Sicily, where patient travel distances exceed national averages. Esaote’s Magnifico Open and O-scan systems use permanent magnets and low acoustic noise to enhance user comfort. Hospitals also deploy mobile trailers to manage surges in oncology referrals. Market consolidation could intensify as global vendors acquire niche portable innovators to broaden their portfolio.

By Field Strength: Ultra-High Field Gains Momentum Despite Mid-Field Dominance

Mid-field (0.5–1.5 T) platforms commanded 47.65% of Italy MRI market size in 2025 and remain the workhorse for routine brain, spine, and joint imaging. The Italy MRI market share advantage stems from clinical versatility and relatively low operating costs. Nonetheless, ultra-high field (>3 T) systems are projected to grow at 5.58% CAGR, propelled by advanced neuro-oncology protocols and research funding flows to Lombardy and Tuscany.

At 7 T, clinicians achieve superior contrast-to-noise and microvascular visualization, helping detect cortical microbleeds and subtle hippocampal sclerosis. Cost remains the primary barrier, yet PNRR incentives could tip the business case for select academic centers. Mid-field scanners are not static; vendors are adding AI-driven sequences that mimic high-field resolution, keeping these systems relevant for community hospitals.

By Application: Oncology Acceleration Challenges Neurology Leadership

Neurology retained 40.75% Italy MRI market share in 2025, fueled by Alzheimer's surveillance and cerebrovascular assessments. Oncology is forecast to be the fastest-growing segment at a 5.93% CAGR through 2031, supported by the adoption of whole-body MRI in routine metastatic workups for prostate and breast cancer. Cardiac and musculoskeletal indications contribute steady volumes, aided by AI algorithms that cut acquisition times and automate reporting.

The Italy MRI industry sees oncology demand broaden beyond tertiary centers; private clinics now advertise total-body oncology scans bundled with AI triage reports. Synthetic MRI techniques that remove the need for gadolinium contrast attained 93% sensitivity in early malignancy detection. Health authorities encourage modality appropriateness, supporting MRI use in oncology pathways when clinically indicated.

By End User: Diagnostic Centers Capitalize on Outpatient Shift

Hospitals maintained a sturdy 66.80% revenue foothold in 2025, reflecting 24/7 emergency needs and multidisciplinary case management. Still, independent imaging centers will log the fastest 5.49% CAGR, buoyed by outpatient procedure migration policy and payer incentives for day-case diagnostics. Service differentiation revolves around same-day reporting, patient-friendly scheduling apps, and transparent pricing.

Outpatient penetration already reaches 48% of advanced imaging volumes nationally and is higher in metropolitan Milan and Rome. Hospitals are responding by spinning off imaging departments into revenue-sharing joint ventures to retain market share. Research institutes focus on experimental protocols and early-phase device trials, acting as key opinion leaders for the broader Italy MRI market.

Geography Analysis

Lombardy, Veneto, and Emilia-Romagna anchor the advanced tier of Italy MRI market development, benefiting from robust regional GDP and dense hospital networks. These regions capture the lion’s share of ultra-high field installations and act as launchpads for AI pilots with multinational vendors. Rome and Tuscany form the middle tier, balancing high research output with moderate funding constraints; flagship centers such as Ospedale San Raffaele routinely publish in peer-reviewed journals and host multinational clinical trials.

In contrast, Sicily, Calabria, and Campania still record lower scanner density per capita. The 2024 differentiated autonomy law may widen this North-South gap by delegating greater budget control to already well-funded regions. PNRR allocation criteria, however, assign higher weight to socioeconomic disadvantage, potentially channeling capital to Southern provinces for the first time in decades. Early evidence comes from Sardinia’s Aou Sassari, which introduced contrast-enhanced mammography with 3,000 patient accesses in six months, signaling readiness to adopt sophisticated imaging.

Mobile multi-screening units in Tuscany’s Valle del Serchio cut patient travel emissions by 97% and demonstrate how IT-enabled outreach can offset geographic disparities. Regional universities coordinate teleradiology pools that allow Northern subspecialists to read Southern studies overnight, mitigating personnel shortages. Over the forecast horizon, equitable Italy MRI market growth hinges on aligning equipment purchases with parallel investments in workforce and digital infrastructure.

Competitive Landscape

Market concentration remains moderate. Siemens Healthineers, GE HealthCare, and Philips collectively dominate premium bids through integrated hardware-software ecosystems and long-term managed-service contracts. Domestic champion Esaote leverages intimate local relationships and tailored service bundles to hold share in extremity and open systems. Bracco supplies contrast agents and is branching into AI analytics to diversify revenue streams.

Strategic initiatives increasingly center on value-based imaging. Siemens Healthineers’ EUR 55 million agreement with University Hospital Nantes—involving virtually helium-free scanners and outcome-linked pricing—sets a template likely to be replicated with Italian health authorities. Philips’ partnership with NVIDIA builds proprietary foundation models that promise zero-click protocols and automated triage, differentiating its offering beyond magnet strength.

Emerging disruptors include United Imaging, whose installation at Cobellis Clinic signals competitive pricing pressure in mid-field systems, and several AI software start-ups targeting scan planning and post-processing. Supply-chain resilience, particularly helium sourcing, has become a new battleground; vendors advertising negligible helium burn rates gain an edge as energy costs rise. Over the forecast period, competitive intensity will likely pivot from hardware performance toward ecosystem partnerships, workflow guarantees, and sustainability metrics.

Italy Magnetic Resonance Imaging Industry Leaders

GE Healthcare

Fujifilm Holdings Corporation

Koninklijke Philips NV

Siemens Healthcare AG

Canon Medical Systems Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Siemens Healthineers co-leads the EUR 26.9 million UMBRELLA project to boost AI-driven stroke care across Europe, with multiple Italian hospitals participating.

- May 2024: United Imaging installs a full-suite MRI solution at Cobellis Clinic, expanding its Italian footprint through a turnkey service contract.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italian magnetic resonance imaging market as all newly manufactured, human-diagnostic MRI scanners, fixed or mobile, low to ultra-high field, that are installed inside hospitals, imaging centers, and research institutes across Italy. Systems imported as ready units and those locally assembled from OEM kits are counted once they enter active clinical service.

Scope exclusion: veterinary scanners, refurbished units, aftermarket service contracts, and standalone coils or contrast agents are not counted.

Segmentation Overview

- By Architecture

- Closed MRI Systems

- Open MRI Systems

- By Field Strength

- Low Field (<0.5 T)

- Mid Field (0.5-1.5 T)

- High Field (1.5-3 T)

- Very-/Ultra-High (>3 T)

- By Application

- Neurology

- Oncology

- Cardiology

- Gastroenterology

- Musculoskeletal

- Other Applications

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Research Institutes

Detailed Research Methodology and Data Validation

Primary Research

Analysts held structured calls with Italian radiologists, biomedical engineers, and procurement officers from the North, Center, and South. Their inputs clarified typical scanner lifespans, field-strength mix shifts after PNRR funding, and average selling prices for 1.5 T versus 3 T models, allowing us to fine-tune assumptions pulled from desk work.

Desk Research

We began by mapping the installed base and annual import flow of MRI systems using open datasets such as OECD health equipment statistics, ISTAT trade codes, and Italian Ministry of Health procurement bulletins. Trade association digests from AIIC and EU MedTech, peer-reviewed papers on scan utilization, and company 10-K filings added pricing and replacement-cycle clues. Select paid databases, notably D&B Hoovers and Dow Jones Factiva, supplied revenue splits for leading suppliers. Many other public and subscription sources were also reviewed for cross-checks.

Market-Sizing & Forecasting

A top-down model rebuilt annual demand from procedure volumes, scan-to-scanner ratios, and average uptime, which are then validated through selective bottom-up supplier roll-ups and channel checks. Key variables include chronic-disease prevalence, capital-expenditure cycles under the National Recovery Plan, euro-dollar movements, tender lead times, and the share of high-field systems in total installs. We forecast with multivariate regression anchored to these drivers and confirmed directionally by expert consensus; gaps in bottom-up counts are bridged with midpoint estimates from import value trends.

Data Validation & Update Cycle

Outputs pass a three-level review where anomalies against external benchmarks trigger re-contacts. Reports refresh once a year, and an interim update is released whenever large tenders or currency swings materially shift the baseline.

Why Our Italy Magnetic Resonance Imaging Baseline Commands Confidence

Published numbers often differ because firms pick unique scopes, price assumptions, and refresh cadences. Our disciplined variable set and annual recalibration keep the baseline steady yet responsive.

Key gap drivers arise when others drop mobile units, fold service revenue into hardware totals, or freeze exchange rates at historic levels, which can compress or inflate market value relative to our 2025 base case.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 264.4 m (2025) | Mordor Intelligence | - |

| USD 175.4 m (2024) | Regional Consultancy A | Omits open and mobile scanners |

| USD 235.5 m (2024) | Trade Journal B | Uses 2020 euro parity and list prices |

| USD 1.2 bn (2024) | Industry Data Publisher C | Adds service and contrast media revenue |

The comparison shows how scope breadth and price treatment swing totals. By centering on equipment revenue only, validating variables with on-ground voices, and updating each year, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can track and replicate.

Key Questions Answered in the Report

How big is the Italy Magnetic Resonance Imaging Market?

The Italy Magnetic Resonance Imaging Market size is expected to reach USD 277.56 million in 2026 and grow at a CAGR of 4.98% to reach USD 353.87 million by 2031.

Which architecture segment is growing fastest?

Portable MRI systems, aided by zero-helium designs, are set for a 5.32% CAGR through 2031.

Who are the key players in Italy Magnetic Resonance Imaging Market?

GE Healthcare, Fujifilm Holdings Corporation, Koninklijke Philips NV, Siemens Healthcare AG and Canon Medical Systems Corporation are the major companies operating in the Italy Magnetic Resonance Imaging Market.

What main challenge limits market growth?

High acquisition costs, personnel shortages, and helium price volatility are key hurdles that could shave up to 1.4 percentage points off CAGR forecasts.

Page last updated on: