Ethylene Propylene Diene Monomer (EPDM) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

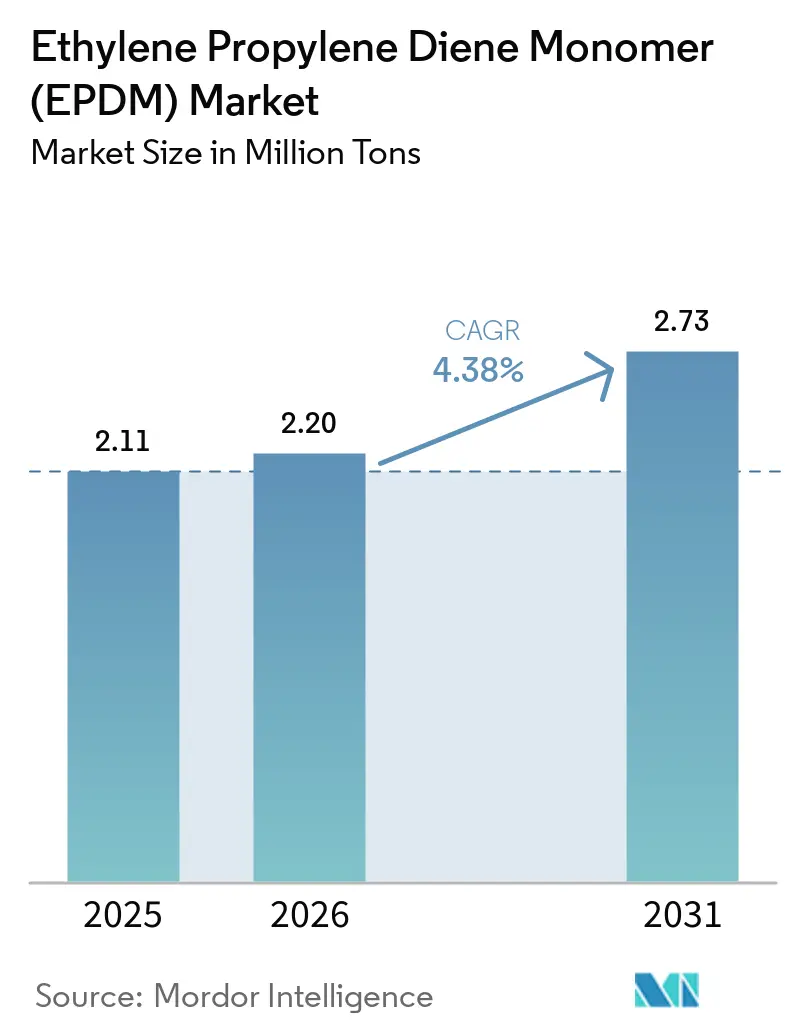

| Market Volume (2026) | 2.20 Million tons |

| Market Volume (2031) | 2.73 Million tons |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethylene Propylene Diene Monomer (EPDM) Market Analysis by Mordor Intelligence

The Ethylene Propylene Diene Monomer Market size was valued at 2.11 million tons in 2025 and is estimated to grow from 2.20 million tons in 2026 to reach 2.73 million tons by 2031, at a CAGR of 4.38% during the forecast period (2026-2031). As demand shifts from internal-combustion vehicle weather-strips to electric-vehicle thermal-management seals, peroxide-cured grades, which maintain a compression-set recovery below a certain threshold after extended exposure at high temperatures, are outpacing thermoplastic alternatives. By 2025, the Asia-Pacific region is set to command a significant share of the Ethylene Propylene Diene Monomer market, driven by China's ramp-up in new-energy vehicle (NEV) production and Southeast Asia's 5G backhaul fiber-optic expansions. Slurry polymerization routes, which consume less energy than their solution counterparts, are witnessing the fastest growth due to their integration of metallocene catalysts, eliminating the need for expensive solvent-recovery units. Competitive pressures are mounting as bio-attributed grades bolster Scope 3 carbon-reduction claims. Simultaneously, producers in the Middle East leverage integrated ethylene-propylene feedstocks, allowing them to reduce spot prices.

Key Report Takeaways

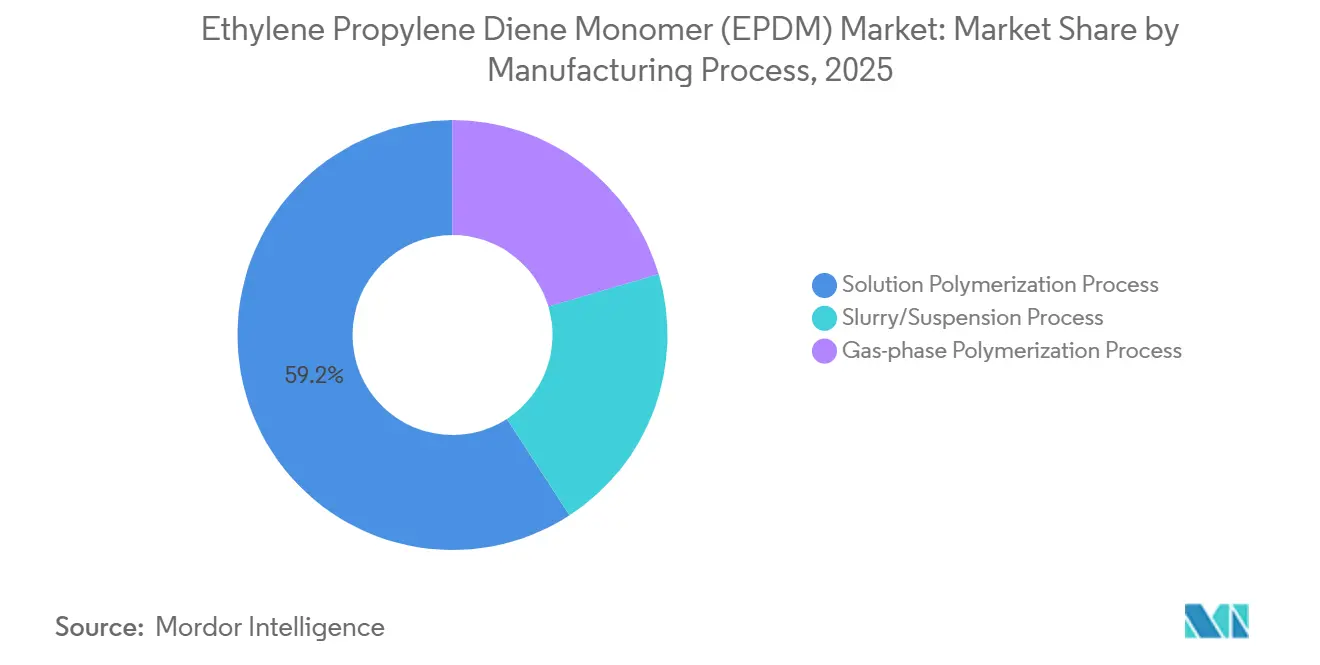

- By the manufacturing process, solution polymerization captured 59.16% of the Ethylene propylene diene monomer market size in 2025, and slurry/suspension polymerization is forecast to expand at a 4.83% CAGR through 2031, the fastest among routes.

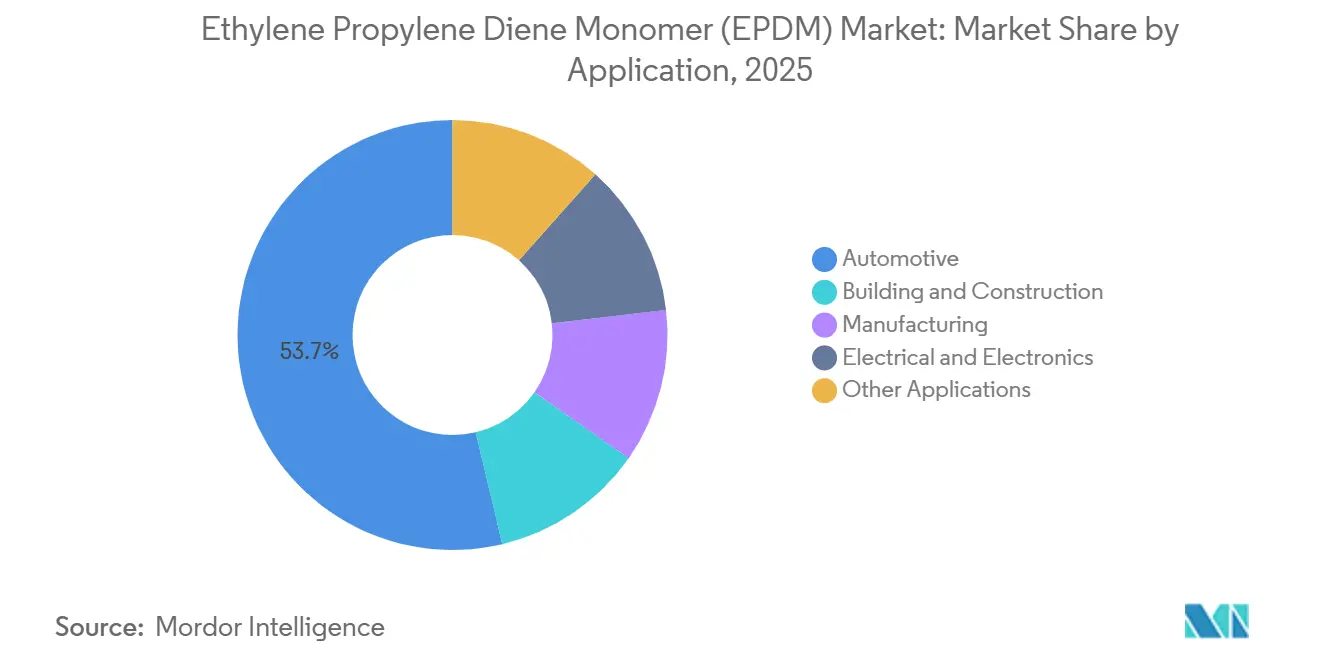

- By application, automotive captured 53.72% of the Ethylene propylene diene monomer market size in 2025 and is advancing at a 4.62% CAGR through 2031.

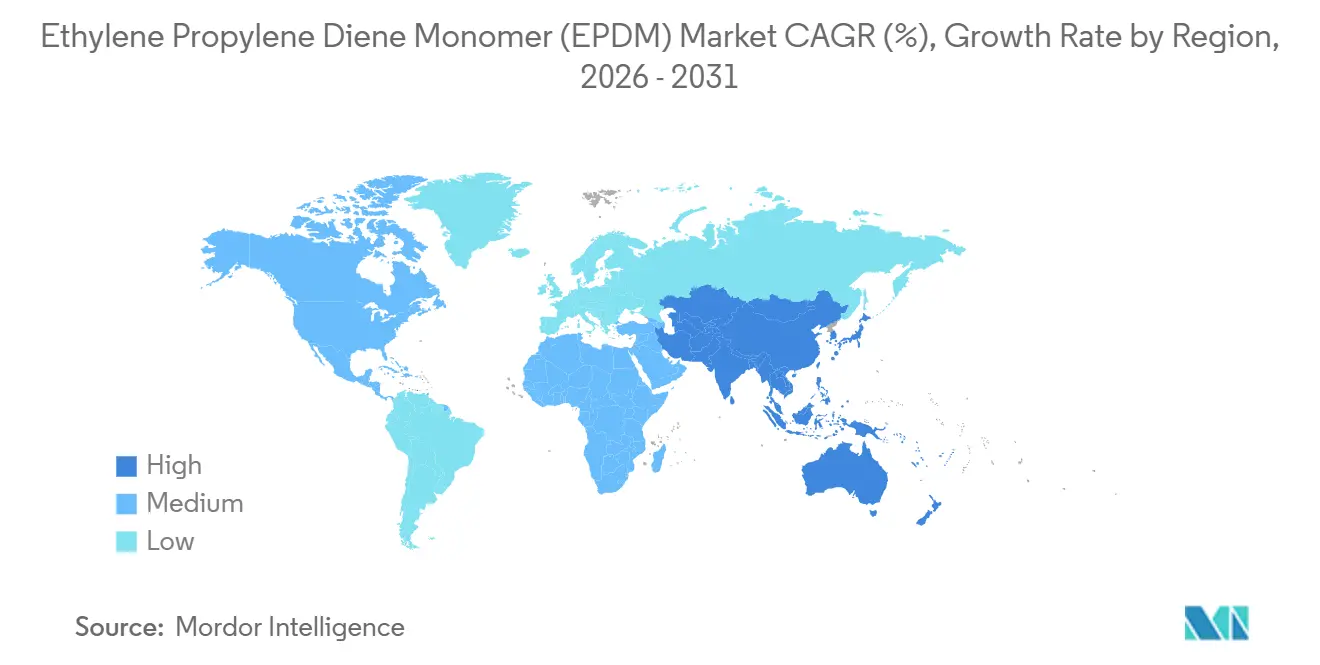

- By region, Asia-Pacific commanded 56.15% of the Ethylene propylene diene monomer market share in 2025 and is projected to grow at a 4.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ethylene Propylene Diene Monomer (EPDM) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated EV production boosting seals and gaskets demand | +1.2% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Mandatory 5G roll-outs requiring weather-resistant cables | +0.7% | APAC core, spill-over to MEA and Latin America | Short term (≤ 2 years) |

| Rapid expansion of precision-drip irrigation tubing | +0.5% | India, Middle East, North Africa, Mediterranean Europe | Long term (≥ 4 years) |

| Hydrogen fuel-cell infrastructure needs high-temperature elastomers | +0.4% | Japan, South Korea, Germany, California | Long term (≥ 4 years) |

| OEM shift to peroxide-cured EPDM for low-VOC interior parts | +0.9% | Europe, North America, premium segments in China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated EV Production Boosting Seals and Gaskets Demand

Electric-vehicle battery packs require EPDM, which maintains a compression-set recovery under specific thermal conditions, a benchmark thermoplastic elastomer can't achieve. As the industry shifts from R134a to the high-pressure R744 refrigerant in EV cooling systems, EPDM's non-polar backbone offers an advantage, resisting plasticization even at a high system pressure. In 2024, China produced a significant number of new energy vehicles (NEVs), with each car consuming a notable amount of EPDM. Tier-1 suppliers are opting for IP67-rated EPDM gaskets in battery-disconnect units, as the higher raw-material cost of silicone makes it an uneconomic substitute. This alignment of thermal, chemical, and mechanical needs is leading to a consolidation of supply, favoring integrated producers adept in polymerization, compounding, and in-house testing.

Mandatory 5G Roll-Outs Requiring Weather-Resistant Cables

Global 5G deployments require EPDM-jacketed power and fiber cables. These cables must endure tropical UV and salt-fog conditions for extended periods without cracking[1]ASTM International, “D1149 Ozone Resistance,” astm.org. Under BharatNet III, India mandates EPDM or LSZH-EPDM compounds for village fiber links by 2025. This initiative is set to generate significant incremental demand. EPDM, with a dielectric constant in the range of 2.3 to 2.5 at 1 GHz, experiences less signal loss than silicone. This advantage facilitates denser small-cell layouts, subsequently reducing site-acquisition costs. Notably, each small-cell node introduces multiple outdoor terminations. This surge amplifies the demand for EPDM connector boots by eight to twelve times compared to 4G macro towers. As telecom projects consolidate their purchases into narrow delivery windows, Asian compounders are operating at high capacity utilization.

Rapid Expansion of Precision-Drip Irrigation Tubing

Regions facing water stress are increasingly adopting drip irrigation, witnessing significant annual growth. EPDM seals, known for their durability, can endure fertilizers, pesticides, and chlorinated water for a considerable span of years. By 2025, India's PMKSY subsidy program has successfully covered millions of hectares, leading to a substantial demand for EPDM in inline drippers, valves, and connectors. In desert environments, EPDM's service life is significantly longer than polyethylene when exposed to UV and chemicals. This longevity translates to reduced lifetime system costs, especially when factoring in a long-term payback on water savings. Installers in the Middle East favor EPDM for its resistance to biofilm formation, even at high field temperatures, a feat where PVC seals quickly embrittle. Meanwhile, producers are maintaining stable spot resin prices, ensuring that drip-system economics remain appealing to farmers.

Hydrogen Fuel-Cell Infrastructure Needs High-Temperature Elastomers

Proton-exchange membrane fuel-cell stations, operating at 70 MPa and temperatures between 120–150 °F, necessitate the use of peroxide-cured EPDM gaskets, which are resistant to hydrogen permeation cracking. Both Japan's and South Korea's hydrogen roadmaps project the establishment of numerous refilling stations by 2030. Each station is expected to utilize high-temperature seals, leading to significant annual EPDM demand. Germany's H2 Mobility network adheres to specifications outlined in DIN EN 17124, mirroring the demands of Japan and South Korea. This alignment offers European producers a lucrative opportunity, as peroxide-cured grades command a price premium over their sulfur-cured counterparts. In North America, California's Clean Transportation Program is making a significant move, designating funding for hydrogen refueling hubs in 2026. This investment underscores the region's growing specialty demand. Furthermore, integrated producers, equipped with compound validation labs, are locking in long-term supply contracts. This is crucial, as fuel-cell stack OEMs mandate durability data before granting platform approval.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from thermoplastic polyolefin (TPO) elastomers | -0.8% | North America, Europe (automotive exterior parts) | Short term (≤ 2 years) |

| Carbon-intensity scrutiny of petro-based polymers | -0.5% | Europe (CBAM), California (SB 253), China (dual-control policy) | Medium term (2-4 years) |

| Impending micro-plastics limits on EPDM crumb applications | -0.5% | Europe (REACH Entry 78), North America (state-level bans), APAC (emerging regulations) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Thermoplastic Polyolefin (TPO) Elastomers

Automotive exterior parts are increasingly adopting TPO due to its advantages, such as enabling in-mold painting and reducing paint-line cycle time[2]Society of Plastics Engineers, “TPO Processing Advantages,” 4spe.org. Unlike EPDM crumb, which incurs recycling costs due to devulcanization, TPOs can be reground without this process. Since 2024, North American OEMs have boosted TPO content in light trucks, leading to a displacement of EPDM annually. The end-of-life fees imposed by EU and California EPR rules further accelerate this shift. However, EPDM maintains a significant share in cold-climate sealing. This is because TPOs become brittle at low temperatures, whereas EPDM remains flexible in much colder conditions. In response, producers are turning to thermoplastic vulcanizates, which combine the elasticity of EPDM with the recyclability of polypropylene carriers.

Carbon-Intensity Scrutiny of Petro-Based Polymers

Conventional EPDM emits a significant amount of CO₂e per kg, surpassing the OEM Scope 3 limit. Starting in 2026, the EU's Carbon Border Adjustment Mechanism will levy a charge on imported EPDM without decarbonization certificates. Dow’s NORDEL REN, introduced in 2024, achieves a substantial reduction in carbon footprint using a bio-feedstock mass-balance approach. However, it comes at a premium, limiting its uptake to high-end electric vehicle brands in Europe and China. California’s SB 253 mandates Scope 3 emissions disclosure for companies with revenues exceeding a certain threshold, starting in 2026, intensifying scrutiny on construction supply chains. With bio-naphtha production significantly lower than fossil sources, bio-attributed EPDM is projected to remain capped at a small percentage of the global volume until 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Manufacturing Process: Slurry Routes Gain on Cost Efficiency

Solution polymerization process delivered 59.16% of global output in 2025. However, the slurry/suspension process, operating at 40–60 °C and eliminating the need for solvent recovery, emerged as the fastest-growing route at a 4.83% CAGR through 2031, achieving notable growth and reducing energy consumption. Utilizing metallocene catalysts in slurry reactors enhanced ethylene distribution while curtailing the costly consumption of ENB. The cost advantage was evident: greenfield slurry plants incurred lower expenses per annual ton compared to solution units. This price disparity drove capacity expansions in India and Southeast Asia. While solution routes continued to lead in peroxide-curable and ultra-high-molecular-weight grades, slurry producers began post-reactor grafting of maleic anhydride to bridge gaps in applications where adhesion was critical.

Regional trends highlighted this evolution. Kumho Polychem’s Yeosu unit, with a significant capacity, employed ultra-low-temperature slurry polymerization, achieving a notable reduction in refrigeration costs. Meanwhile, ARLANXEO’s Changzhou line, which had expanded in 2022, capitalized on shipping cost-advantaged slurry grades to cater to China’s growing construction and cable sectors. Investors adopted a dual capital strategy: amplifying slurry production for volume while maintaining solution lines for their high-margin specialties. This strategic balance redefined capital allocations among suppliers in the Ethylene propylene diene monomer market.

By Application: Automotive Dominance Masks Segment Bifurcation

Automotive captured 53.72% of the Ethylene propylene diene monomer market size in 2025 and is advancing at a 4.62% CAGR through 2031. While the demand for EV sealing in battery enclosures and coolant hoses has been growing annually, traditional ICE mounts and radiator hoses have been experiencing a decline. This divergence indicates a rising market share for high-margin peroxide-cured grades of Ethylene propylene diene monomer, even as the demand for the more common sulfur-cured variants remains stagnant. The building and construction sector, in second place, has benefited from EU efficiency mandates. Reflective EPDM roofing membranes, which can extend service life and reduce cooling energy consumption, have been driving growth. Meanwhile, the electrical and electronics sector has been expanding, fueled by the demand for halogen-free flame retardancy in 5G cable jacketing and data-center power cords.

Industrial rubber goods have been growing, influenced by capital expenditure cycles in mining and chemicals. In contrast, sectors like precision-drip irrigation, synthetic turf, and consumer appliances have collectively experienced growth, driven by regulatory restrictions on PVC and phthalates. Regional preferences are distinct: the Asia-Pacific region's Ethylene propylene diene monomer market has been skewed towards automotive and electronics; North America has shown a preference for construction retrofits; and Europe, after tightening VOC limits in 2025, has leaned towards specialty peroxide-cured interiors.

Geography Analysis

Asia-Pacific led the Ethylene propylene diene monomer market with 56.15% of global volume in 2025 and will grow at 4.63% CAGR to 2031 as China’s NEV output, India’s drip-irrigation push, and Southeast-Asian 5G fiber spurs compound demand. Mitsui's Ichihara facility, with a significant capacity, is setting its sights on premium metallocene grades. Meanwhile, after signing an MOU in 2024 with SK Geocentric, Kumho Polychem has been steering its Yeosu plant towards producing ISCC PLUS bio-attributed rubber. Coastal provinces in China are paying a premium for peroxide-cure specifications, which meet the standards for European exports, leading to a differentiated pricing landscape domestically.

North America captured a notable market share in 2025. While automotive plateaus have limited volume growth, Dow's Plaquemine facility has resumed operations, producing bio-attributed NORDEL REN for exports. Concurrently, Lion Elastomers has been enhancing its operations by adding finishing lines for water-based emulsions. Mexican compounders have been witnessing significant growth, fueled by the near-shoring of U.S. EV assembly and a rising specialty demand, especially under California's SB 253 carbon-reporting mandates.

Europe, holding a considerable share in 2025, has been experiencing the slowest growth rate, primarily due to high energy costs squeezing margins. In response to market dynamics, LANXESS has modernized its Geleen facility to emphasize peroxide-cure and bio-attributed production, following the closure of its Marl line. To counteract the sluggish EU auto production, Versalis has been strategically exporting its Ferrara slurry grades to North Africa and the Middle East.

South America, along with the Middle East and Africa, constituted a smaller portion of the global volume. ExxonMobil's KEMYA joint venture has been capitalizing on low-cost feedstocks, pricing its products below Asia's spot rates, thereby exerting pressure on regional margins. Brazil has been witnessing a rebound, thanks to infrastructure spending, while players in the Gulf have been channeling investments into downstream compounding hubs, aiming to capture greater value rather than merely exporting commodity bale rubber.

Competitive Landscape

The ethylene propylene diene monomer (EPDM) market is moderately consolidated. Middle-Eastern producers exploit integrated ethylene-propylene streams to undercut global prices, forcing North-American and European units to idle or pivot toward specialties such as peroxide-curable roof membranes and water-based EPDM emulsions. Disruptive compounders launch maleic-anhydride-grafted EPDM compatible with polyamide and metal substrates, widening use in lightweighting assemblies where mechanical fasteners are deleted. Metallocene EPDM from Chinese plants threatens Western technology rents as local producers replicate narrow-composition-distribution profiles that once warranted double-digit price premiums. White-space growth lies in hydrogen sealings and bio-TPV blends that satisfy circular-economy mandates. Lion Elastomers and Emulco commercialize water-borne emulsions, positioning EPDM for low-VOC coatings, while Dow and Kumho certify bio-attributed lines that help automakers meet Scope 3 targets under EU CBAM and California SB 253.

Ethylene Propylene Diene Monomer (EPDM) Industry Leaders

ARLANXEO

Exxon Mobil Corporation

SK geocentric Co., Ltd.

Dow

Kumho P&B Chemicals (Kumho Polychem)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Trelleborg Sealing Solutions introduced new EPDM rubber grades designed to reduce the product's carbon footprint by up to 55%. These ethylene propylene diene monomer (EPDM) rubber grades are available in 70 Shore A and 80 Shore A variants.

- August 2025: ARLANXEO launched ISCC PLUS-certified Keltan Eco-B and Eco-BC grades in India, offering bio-based EPDM alternatives with identical performance to conventional rubbers.

Global Ethylene Propylene Diene Monomer (EPDM) Market Report Scope

Ethylene Propylene Diene Monomer (EPDM) is a copolymer, and its elastomers exhibit properties like heat, ozone/weathering, and aging resistance. It is used in the automotive industry, roofing, and waterproofing for various applications.

The ethylene propylene diene monomer (EPDM) market is segmented by manufacturing process, application, and geography. By manufacturing process, the market is segmented into solution polymerization process, slurry/suspension process, and gas-phase polymerization process. By application, the market is segmented into the automotive, building and construction, manufacturing, electrical and electronics, and other applications. The report also covers the market size and forecasts for the ethylene propylene diene monomer (EPDM) in 27 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (Tons).

| Solution Polymerization Process |

| Slurry/Suspension Process |

| Gas-phase Polymerization Process |

| Automotive |

| Building and Construction |

| Manufacturing |

| Electrical and Electronics |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Spain | |

| Turkey | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Manufacturing Process | Solution Polymerization Process | |

| Slurry/Suspension Process | ||

| Gas-phase Polymerization Process | ||

| By Application | Automotive | |

| Building and Construction | ||

| Manufacturing | ||

| Electrical and Electronics | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Which production route is gaining share within global EPDM output?

Slurry/suspension polymerization is the fastest-growing route at a 4.83% CAGR in 2025 because it lowers energy use and capital intensity compared with solution processes.

What is driving EPDM adoption in telecom infrastructure?

5G roll-outs require UV- and ozone-resistant cable jackets; EPDM meets IEC 60502 weathering tests and has a favorable dielectric constant that minimizes signal loss.

How does TPO competition affect EPDM demand?

TPOs displace EPDM in exterior auto parts where recyclability and in-mold painting cut assembly costs, reducing EPDM use in North America.

What is the current global demand for the EPDM market and its expected growth by 2031?

The Ethylene Propylene Diene Monomer Market size was valued at 2.11 million tons in 2025 and is estimated to grow from 2.20 million tons in 2026 to reach 2.73 million tons by 2031, at a CAGR of 4.38% during the forecast period (2026-2031).

Page last updated on: