Italy Barbeque Grill Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

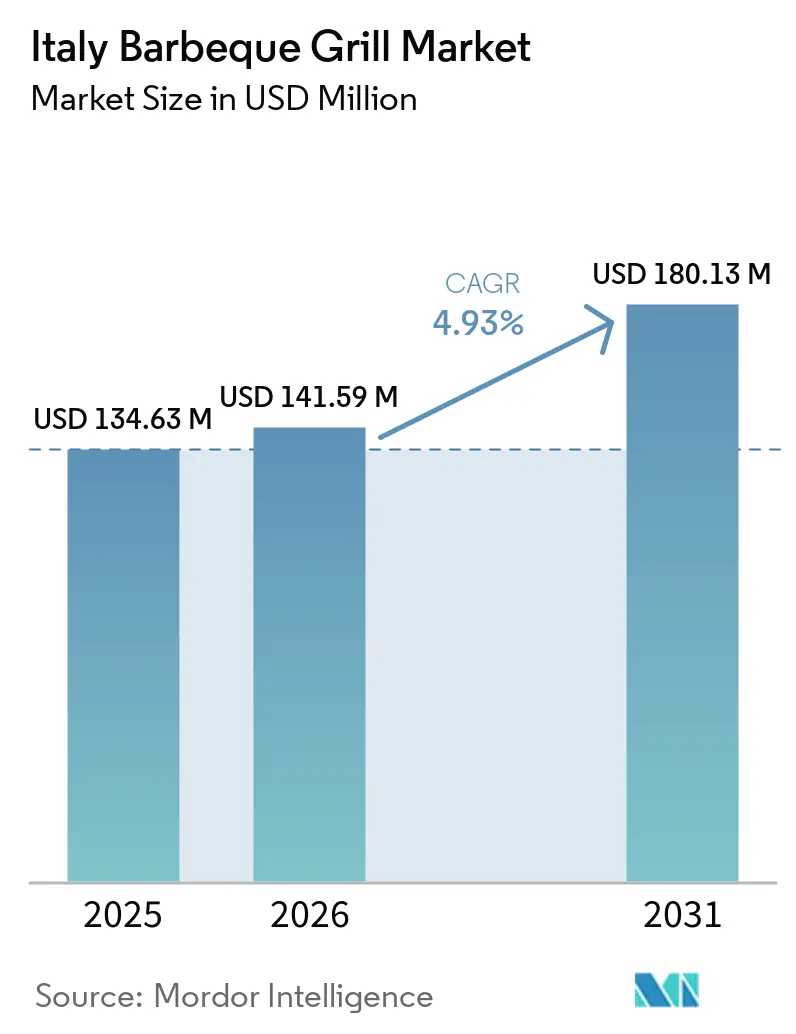

| Base Year Market Size (2025) | USD 134.63 Million |

| Market Size (2026) | USD 141.59 Million |

| Market Size (2031) | USD 180.13 Million |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Barbeque Grill Market Analysis by Mordor Intelligence

The Italy barbeque grill market size is expected to grow from USD 134.63 million in 2025 to USD 141.59 million in 2026 and is forecast to reach USD 180.13 million by 2031, at a CAGR of 4.93% over 2026-2031. A controlled pace of growth reflects steady household demand, a visible uptick in hospitality investment tied to record visitor nights, and a regulatory tilt in favor of gas and pellet systems over charcoal. Gas grills held the largest share of the market. In contrast, pellet platforms are set to experience the fastest growth. This uptick is primarily due to a rising number of consumers opting for traceable wood fuels to ensure compliance with the European Union's Deforestation Regulation due diligence requirements. Seasonal wildfire rules that restrict open flames in select regions further reinforce the shift toward cleaner-burning options during peak summer months. Smart and connected products will grow from a smaller base as manufacturers extend app-guided cooking, remote monitoring, and probe integration across price bands and fuel types. Distribution remains retail-heavy, but direct-to-consumer and e-commerce models are gaining reach through brand-controlled storefronts, accessory bundles, and software-enabled add-ons that increase lifetime value.

Key Report Takeaways

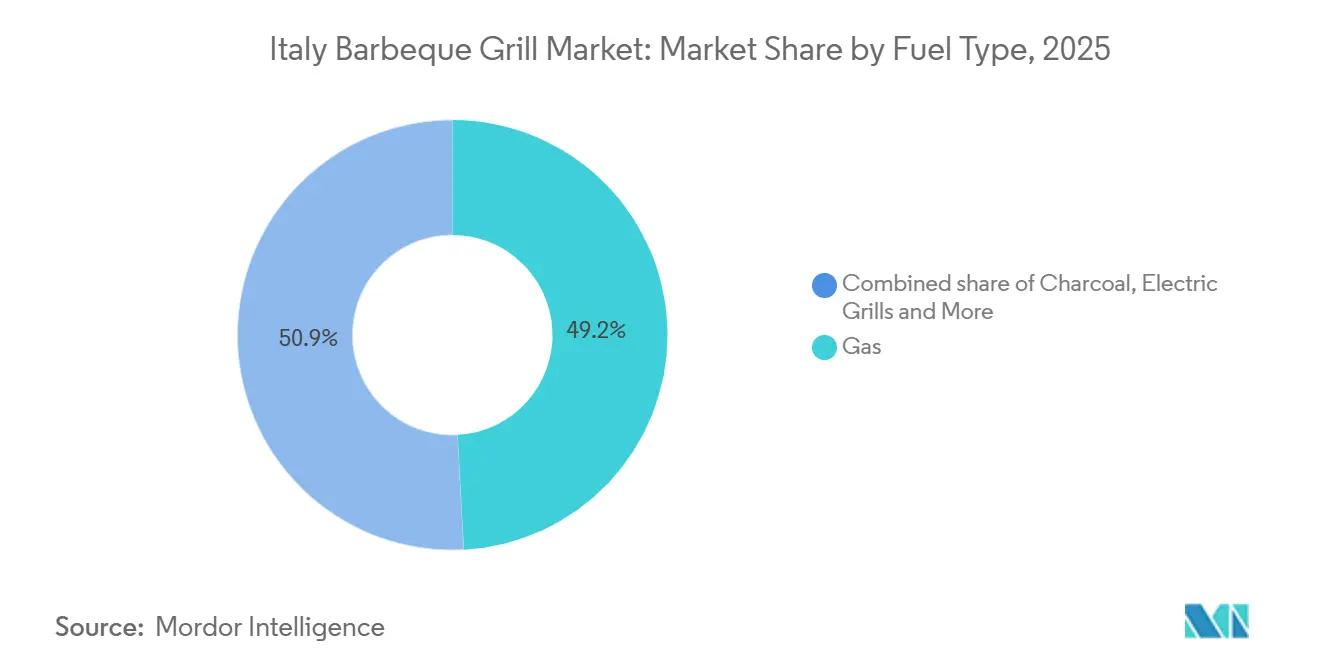

- By fuel type, gas led with 49.15% share in 2025 in the Italy barbeque grill market, while pellet grills are projected to post the highest growth at 5.93% CAGR through 2031.

- By product design, freestanding grills accounted for 58.72% in 2025 in the Italy barbeque grill market, and portable and table-top models are forecast to grow at 5.46% CAGR by 2031.

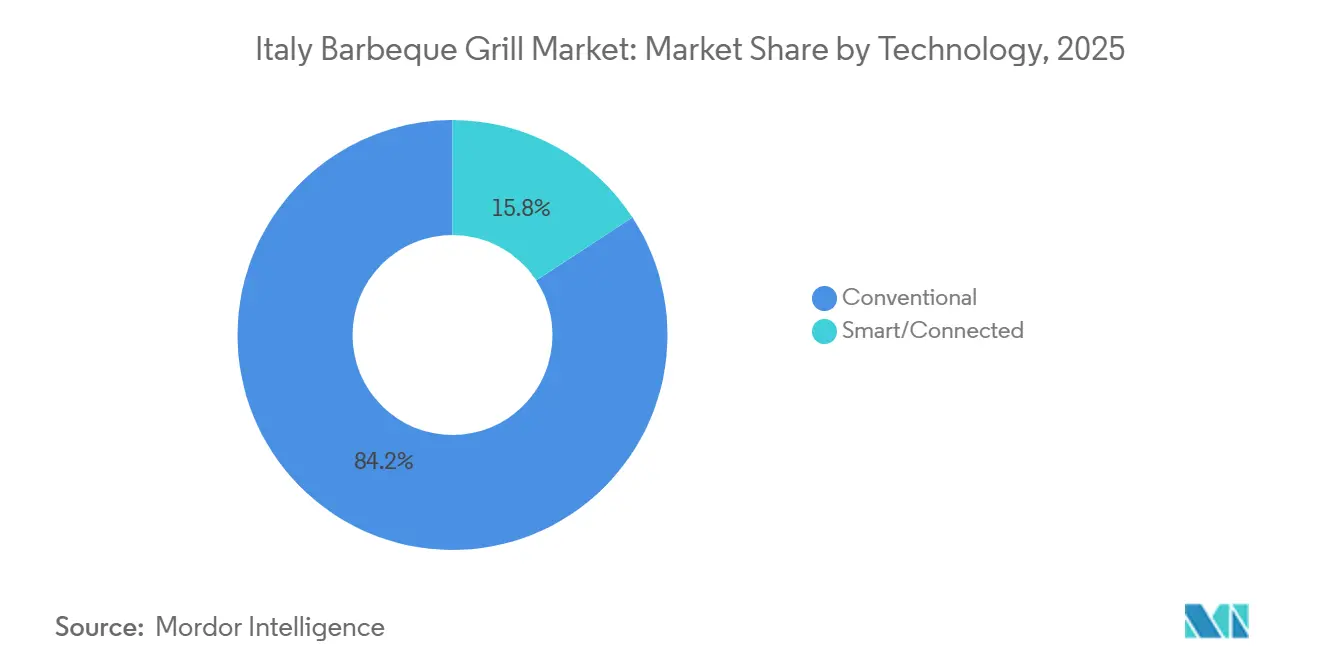

- By technology, conventional grills represented 84.21% in 2025 in the Italy barbeque grill market, while smart and connected grills are expected to register a 6.07% CAGR through 2031.

- By end-user, residential held 67.53% in 2025 in the Italy barbeque grill market, and the commercial segment is set to grow at 5.09% CAGR through 2031.

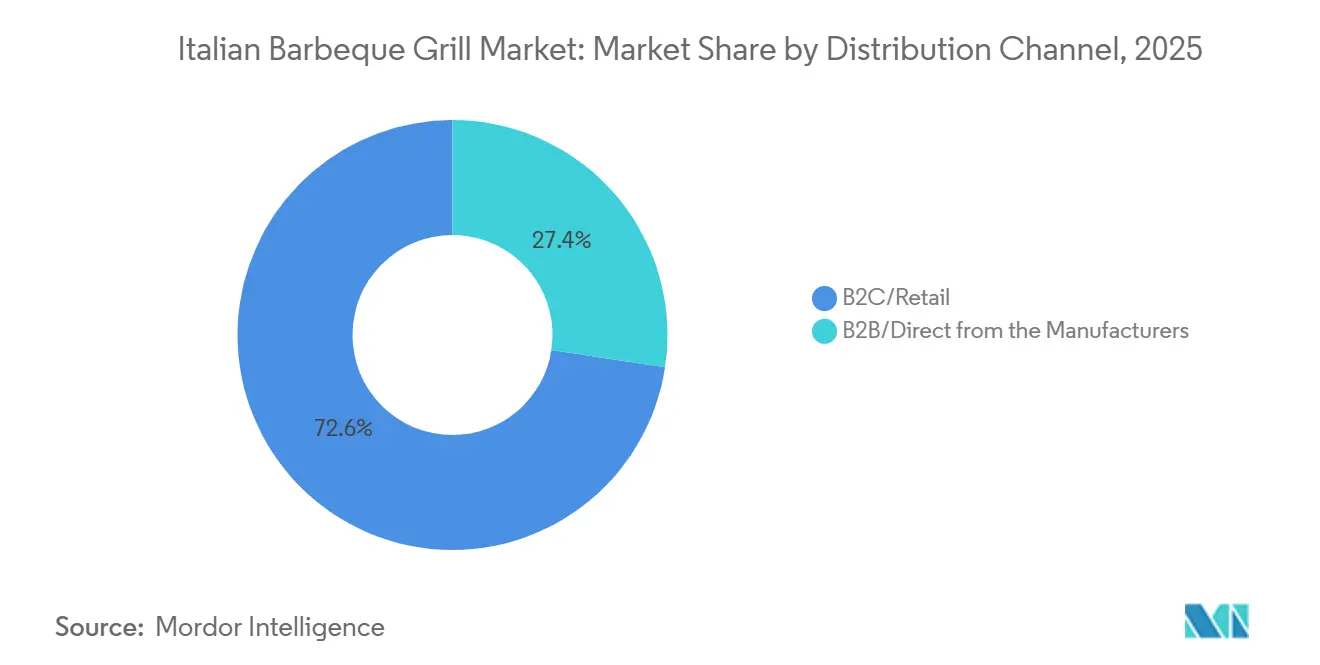

- By distribution channel, B2C retail captured 72.61% in 2025 in the Italy barbeque grill market, and online platforms are projected to grow at 5.55% CAGR by 2031.

- By geography, Northern Italy led with 27.54% in 2025 in the Italy barbeque grill market, while Central Italy is forecast to grow fastest at 6.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Barbeque Grill Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outdoor living investments and garden upgrades (Bonus Verde incentive) | +1.2% | National, concentrated in Northern and Central urban areas | Medium term (2-4 years) |

| Tourism recovery and record visitor nights are sustaining commercial demand | +1.5% | National, with early gains in Southern Italy, the islands, and the central cities of art | Short term (≤ 2 years) |

| Expansion of DIY and specialty retail, plus online channels for grills | +0.9% | National, urban centers with higher e-commerce penetration | Medium term (2-4 years) |

| Harmonized European Union Gas Appliances Regulation enabling safer, faster access | +0.7% | European Union-wide, Italy as compliant market | Long term (≥ 4 years) |

| EUDR due diligence pressure on charcoal nudging shift to gas, electric, and pellet | +0.8% | European Union-wide, with spillover to Italy’s charcoal-heavy regions | Medium term (2-4 years) |

| Premium outdoor kitchens are catalyzing demand for built-in and high-end grills | +1.0% | National, with a concentration in Northern Italy and coastal resort areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tourism Recovery Sustains Commercial Outdoor Cooking Infrastructure

Italy recorded 476.9 million overnight stays in 2025, up 2.3% year over year, while international visitor nights rose 4.3%, supporting capital spending by hotels, agriturismi, and outdoor dining venues that differentiate with upgraded grill stations and outdoor kitchens [1]Eurostat, “Another Record Year for EU Tourism in 2025,” Eurostat, ec.europa.eu. The Italy barbeque grill market benefits from strong flows to resort corridors and heritage cities, where operators refresh terraces and garden dining areas to meet guest expectations for al fresco experiences. Commercial operators are aligning fleet choices to uptime and throughput needs, with large-format gas grills favored for fuel logistics and ease of maintenance in peak seasons. Cross-regional travel within Italy channels demand toward rental properties and hospitality venues that standardize on fuel types allowed under local fire-risk rules, further shaping product mix and inventory planning. This demand pulse translates into the fastest expansion in the commercial end-user segment through 2031 as operators pursue consistent, regulation-compliant cooking options.

DIY Retail and E-Commerce Expansion Lower Purchase Barriers

The Italy barbeque grill market continues to rely on B2C retail for discovery and conversion, with specialty stores and home centers anchoring 2025 sales, while online channels add reach, speed, and range to the accessory and replacement parts business. As brands expand direct-to-consumer storefronts, early access to connected modules and software-enabled accessories supports premium attachment rates and improves sell-through of higher-margin SKUs. E-commerce also compresses launch cycles for incremental innovations such as smart controllers, probe kits, and grill-to-app integrations, which are easier to merchandise digitally with content and guided setup. Physical stores retain an edge for tactile validation of ignition systems, build quality, and cooking area, which remains decisive for first-time buyers who plan multi-year use. Together, omnichannel strategies reduce friction for first purchases and accelerate repeat purchases of add-ons that extend unit lifecycles.

EUDR Compliance Costs Accelerate Fuel Substitution Toward Traceable Alternatives

Under the European Union Deforestation Regulation, charcoal falls within regulated categories and will require plot-level geolocation and deforestation-free due diligence from large operators by December 30, 2026, raising documentation, monitoring, and audit costs across the supply chain. The Italy barbeque grill market is already seeing buyer preferences shift toward fuels that are simpler to certify under EUDR, which supports the outlook for pellet grills and helps stabilize gas adoption for peak-season reliability. Retailers are rebalancing assortments in favor of traceable wood pellets and compliant packaging, prioritizing suppliers that can furnish documentation while maintaining service levels. Pellet brands with certified forestry inputs can align marketing and compliance narratives, while charcoal importers restructure logistics to meet reporting and verification obligations. Post-deadline enforcement includes material penalties, reinforcing long-run incentives to de-risk assortments with fuels that meet traceability thresholds.

Premium Outdoor Kitchens Elevate Built-In Grill Demand

The Italy barbeque grill market is moving upmarket in affluent districts, where owners invest in cohesive outdoor kitchens that pair built-in grills with modular storage, refrigeration, and ventilation for year-round use. Premium lines that offer robust materials and accessory ecosystems support professional-grade cooking performance in coastal and high-value residential settings. Modular planchas and griddle stations have extended the use case beyond classic grilling, drawing interest from households that entertain frequently and seek flexible multi-zone setups. Brand portfolios that cover gas, pellet, and charcoal across freestanding and built-in formats help buyers match aesthetics and fuel stability with local codes and usage cycles. Over the forecast period, outdoor kitchen adoption tracks renovation and new-build timelines, reinforcing sustained demand for integrated solutions at the premium end.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal wildfire, open-flame restrictions limiting charcoal use periods | -0.6% | Regional, concentrated in Tuscany, Veneto, and wildfire-prone zones | Short to medium term (≤ 3 years) |

| Elevated household electricity costs affect the operating cost of the electric grill | -0.4% | National, with higher sensitivity in low-consumption households | Short term (≤ 2 years) |

| Charcoal supply compliance costs under EUDR tightening availability and prices | -0.5% | European Union-wide, Italy as importer of charcoal | Medium term (2-4 years) |

| Limited natural-gas conversion options for EMEA models are constraining installs | -0.3% | Regional, concentrated in Southern Italy and rural areas without piped gas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Wildfire Restrictions Fragment Charcoal Grill Usage Windows

Seasonal fire-risk rules in regions such as Tuscany impose open-flame limits during high-risk months, which compresses the practical window for charcoal users and nudges households toward gas or pellet options with more consistent availability [2]CIA Toscana, “Rischio Incendi, Abbruciamenti Vietati in Toscana,” CIA Toscana, cia.it. Local ordinances often allow braziers and barbecues only in private homes or designated areas during bans, creating uncertainty for owners who rely on public or shared outdoor spaces. Charcoal’s peak-season constraints reduce return-on-use for buyers who cook most during summer and prefer spontaneous outdoor gatherings. For retailers and brands, the rules require more precise inventory cycles and responsive merchandising that highlight compliant alternatives during alert periods. These dynamics have a modest but persistent dampening effect on charcoal volumes within the Italy barbeque grill market.

Charcoal Supply Chain Compliance Costs Constrict Availability

As the EUDR deadline for large operators approaches, charcoal suppliers face added costs to demonstrate geolocation, risk assessment, and deforestation-free status, which tightens assortments and supports price discipline for compliant stock. Retailers respond by favoring suppliers with clearer documentation and scalable due diligence processes, which reduces volatility in shelf planning and aligns with post-deadline enforcement. For consumers, reduced charcoal variety and firmer pricing shift the value equation toward gas and pellet systems that promise operational certainty in peak months. Over time, value chains with integrated forestry or verifiable pellet sourcing can compete more effectively for premium placement and consumer trust. These changes reinforce the medium-term rebalancing of fuel choices in the Italy barbeque grill market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Pellet Grills Gain as EUDR Reshapes Charcoal Economics

Gas grills commanded 49.15% of the Italy barbeque grill market share in 2025 as buyers prioritized easy ignition, precise control, and flexible LPG or natural gas connections. Pellet platforms are projected to expand at 5.93% CAGR through 2031, drawing momentum from their compatibility with certified forestry inputs and simpler EUDR compliance narratives than those facing charcoal import chains. Clearer documentation and reliable restocking cycles underpin steady peak-season performance for gas and pellet users who cannot risk disruptions during summer holidays [3]BM Certification, “EUDR Due Diligence and Compliance Guidance,” BM Certification, bmcertification.com. The Italy barbeque grill market will continue to feature a loyal charcoal base, yet its relative weight softens where seasonal fire-risk limits and due diligence obligations intersect. Electric grills retain a small but stable role in settings that restrict open flames, aided by cleaner operation and compact footprints for urban dwellers.

Pellet innovation improves usability without losing wood-fired appeal, closing the convenience gap with gas while guarding on flavor and smoke control [4]Traeger, Inc., “Traeger Grills Celebrates 40 Years with the Woodridge Series,” PR Newswire, prnewswire.com. Feature sets such as integrated controllers, guided cook programs, and pellet sensors now deliver consistent results for time-constrained home cooks who value repeatability. Gas segments focus on burner performance, heat distribution, and durable finishes that withstand outdoor exposure across Italy’s varied climates. Hybrid and niche fuels remain enthusiast-driven, with coverage in specialty retail and limited impact on mainstream volumes. The net effect is a steady reweighting toward fuels that ensure legal clarity, supply chain visibility, and dependable summer throughput in the Italy barbeque grill market.

By Product Design: Portable Grills Rise as Urban Density Intensifies

Freestanding models accounted for 58.72% of 2025 demand as their mobility, size, variety, and easy setup met the needs of homes that shift use between primary residences and holiday properties. Portable and table-top grills are projected to grow at 5.46% CAGR through 2031, aligning with tighter urban living and the need for smoke-managed solutions that respect condominium policies and shared spaces. Buyers seeking premium outdoor kitchens still rely on built-in formats that integrate with broader entertaining areas and permanent gas supplies where available. In-store consultation remains important for footprint planning, safety clearances, and accessory fit, which supports specialty retailers that offer design guidance and installation services. The balance of formats reflects Italy’s housing mix and outdoor leisure habits, both of which support variety within the Italy barbeque grill market.

Modular systems and planchas support cooking versatility beyond traditional grates, encouraging buyers to assemble stations that match recipes and group sizes through seasons. Premium builders and homeowners value material quality and a coherent look across cabinetry, countertops, and appliances that hold up under salt air and sun exposure. Portable grills gain when shared outdoor areas or code constraints reduce the feasibility of larger installations, keeping entry-level and mid-tier choices active. Retailers leverage display zones and live demos to compare ignition systems, heat zones, and workflow, which influence unit selection in a crowded aisle. These shifts point to a broadening base of configurations within the Italy barbeque grill market that serve both compact city balconies and expansive coastal villas.

By Technology: Smart Connectivity Commands Premium but Conventional Grills Dominate Volume

Conventional grills represented 84.21% of sales in 2025, favored by buyers who want mechanical simplicity and proven reliability at accessible price points. Smart and connected formats are forecast to post a 6.07% CAGR to 2031 as connectivity spreads across fuel types and price tiers, adding remote monitoring, guided cooking, and multi-probe integration. The Italy barbeque grill industry is adopting these capabilities to reduce cook-time errors, support consistent doneness across proteins, and compress the learning curve for new grillers. Brands position smart features to elevate weeknight reliability and weekend entertaining, which helps justify premiums and sustains upgrade interest. Over time, component cost declines for sensors and modules will enable broader adoption without eroding the value of premium SKUs.

Feature-rich lines now cover charcoal, gas, and pellet ecosystems, which allows households to standardize on one app and probes across fuel types. Accessory ecosystems matter as much as the core grill, with probe accuracy, controller stability, and firmware support shaping perceived value. Traditional buyers still prefer manual control and lower total cost of ownership, so that conventional grills will remain the volume anchor of the Italy barbeque grill market. Retailers lean on live displays and content to demystify features, which helps reluctant adopters bridge from conventional to connected setups. This blend of manual and smart formats keeps the technology curve gradual and broad-based.

By End-User: Commercial Segment Accelerates Amid Tourism Recovery

Residential users held 67.53% of demand in 2025, supported by household cooking traditions and incremental upgrades to outdoor spaces. The commercial segment is projected to grow at 5.09% CAGR through 2031 as hotels, agriturismi, and restaurants invest in outdoor kitchens and grill stations to enhance guest experiences during peak travel months. Rising overnight stays lift refresh cycles that prioritize uptime and consistent throughput for group dining, which often favors multi-burner gas grills and durable finishes. Operators increasingly align fuel choices with local regulations to avoid service interruptions during seasonal fire alerts. This steers procurement toward the most dependable options under variable local rules across the Italy barbeque grill market.

Households continue to drive replacement and accessory purchases, often adding side burners, griddles, and rotisserie kits that extend menus through the year. Premium buyers consider built-in configurations that pair with storage and refrigeration for cohesive entertaining spaces. Commercial buyers focus on serviceability, parts availability, and compliant installation, which shapes brand selection. Expansion in events and outdoor dining formats supports a broader fleet mix across venues that want to serve breakfast, lunch, and dinner outdoors in high season. These use cases contribute to steady diversification in the Italy barbeque grill market.

By Distribution Channel: Online Growth Complements Specialty Retail’s Tactile Advantage

B2C retail captured 72.61% of 2025 sales, anchored by specialty showrooms and home centers, where in-person evaluation and consultant support remain decisive. Online channels are projected to grow at 5.55% CAGR through 2031 as brands launch direct storefronts, streamline logistics, and broaden accessory availability. Brand-controlled digital launches for smart attachments and controllers are improving speed-to-market and increasing attach rates for connected ecosystems. Retailers leverage in-store events and live fire demos to educate buyers on configuration options and fuel tradeoffs. These patterns keep the Italy barbeque grill market omnichannel, with digital paths supporting discovery and replenishment while stores manage complex first purchases.

E-commerce is particularly effective for replacement parts, consumables, and accessories that extend unit life and functions. Specialty retailers continue to add value with delivery, assembly, and compliance guidance that smooths the last mile to the first cook. Direct-to-consumer campaigns for exclusive accessories and app-enabled features encourage repeat engagement and software-based differentiation. For institutional buyers, B2B sourcing remains important for multi-site standardization, but it is a smaller share relative to the retail-driven base. Together, these routes keep choice wide and access straightforward across the Italy barbeque grill market.

Geography Analysis

Northern Italy held 27.54% in 2025, the highest regional share of the Italy barbeque grill market, supported by higher household incomes, an established outdoor living culture, and broader access to piped gas for permanent installations. The region’s resorts and heritage destinations also benefit from rising overnight stays, sustaining commercial investment in outdoor dining and terrace cooking. Central Italy is forecast to grow fastest at a 6.34% CAGR as tourism density in art and culture hubs supports hospitality upgrades and rooftop or courtyard installations. Southern Italy and the Islands are experiencing stronger tourism momentum, which lifts portable and built-in demand in resort corridors that modernize for international standards. These regional patterns collectively shape inventory planning, fuel mix, and installation services within the Italy barbeque grill market.

Regional regulatory differences affect fuel choices and formats. In wildfire-prone zones, seasonal restrictions steer demand toward gas and pellet rigs that maintain service continuity during peak months. Tourist-driven markets concentrate on uptime and guest experience, with format choices reflecting terrace size, airflow, and code compliance in dense urban settings. Coastal resorts privilege corrosion resistance, service networks, and extended warranties that fit outdoor exposure profiles. Higher-income districts support premium built-in installations that integrate grills with storage and refrigeration into cohesive layouts. This supports a diverse product mix across the Italy barbeque grill market.

Cross-regional flows influence assortment and support models. Northern households with vacation properties in Southern regions carry preferences for gas and pellet setups that scale from city terraces to coastal villas. Hospitality operators in Central hubs cater to international visitors by upgrading to multi-zone stations that handle varied menus from breakfast through late-night service. Retailers stock accessories and fuel types with attention to local fire-risk calendars and tourism seasonality. Together, these factors reinforce the granular, region-specific mix within the Italy barbeque grill market.

Competitive Landscape

The Italy barbeque grill market shows moderate concentration, with the top five brands accounting for about 60% of 2025 sales, which provides room for regional specialists and private label entries to compete on features and price points. Incumbents are expanding smart ecosystems across fuel types, adding app-guided features and multi-probe monitoring that lift average selling prices and consumer confidence. Strategic moves include more direct launches of accessories and controllers online, which accelerate attach rates and compress go-to-market timelines. Over the forecast period, connected features and compliance-ready fuel assortments will be central to premium positioning and shelf strategy. These themes help define the next phase of competition in the Italy barbeque grill market.

Operational restructuring and channel shifts are reshaping the competitive field. Cost optimization programs and distributor-led models in Europe indicate a pivot toward profitability, with ripple effects on promotional intensity and retail partnerships. This creates opportunities for mid-tier challengers to add share with balanced feature sets and robust after-sales support. Private labels from large DIY groups compete on value, bundle accessories, and have strong in-store visibility, while specialist brands win on materials, serviceability, and premium finishes. Brands that align EUDR-compliant pellet or charcoal assortments with their grill portfolios can reduce retailer risk and secure better placement post-2026. This mix sustains a competitive but disciplined market.

Product innovation centers on connectivity, fuel flexibility, and expanded cooking surfaces. Flagship launches demonstrate how app integrations, probe ecosystems, and proprietary controllers are becoming standard at accessible price points. Grill makers are also stepping into griddle and plancha formats to widen use cases for breakfast and high-heat searing, which strengthens engagement and accessory sales. As firmware updates, app support, and sensor quality improve, connected buyers expect multi-year software enhancements that protect their investment. The net result is a multi-channel, multi-fuel contest where premium differentiation relies on experience, reliability, and compliant fuel ecosystems across the Italy barbeque grill market.

Italy Barbeque Grill Industry Leaders

Weber

Campingaz

Sochef

Napoleon

Char-Broil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Current Backyard, a W.C. Bradley Company brand, launched a Wi-Fi-enabled dual-zone smart electric grill with app-guided recipes and precise heating controls targeting balcony users facing open-flame restrictions.

- January 2026: Weber-Stephen Products LLC unveiled its 2026 smart grilling portfolio, expanding connectivity across all major fuel types to create the backyard’s first seamless, smart ecosystem. The lineup includes the Performer Smart Charcoal Grill with Wi-Fi-enabled LCD controller, a Kettle Smart Ring attachment available exclusively on weber.com, and updated SPIRIT Smart Gas Grills, alongside a Smart Wireless Probe Plus with Booster and Smart Hub Display that integrates with the WEBER CONNECT App.

- April 2025: Traeger introduced the FLATROCK 2 ZONE griddle, expanding beyond pellet grills into flat-surface cooking with a dual-zone design for high-heat searing and low-heat holding.

- January 2025: Traeger Grills celebrated 40 years with the Woodridge Pellet Grill Series, adding WiFIRE connectivity, accessory integration, and features aimed at mid-tier price points to compete with gas on convenience.

Italy Barbeque Grill Market Report Scope

A barbeque grill is an outdoor cooking appliance with a metal grate over a heat source, such as charcoal, gas, or wood. Users cook food directly on the grate, usually meat or vegetables. These grills come in various sizes and designs, from portable ones for picnics to larger, stationary models for backyard gatherings. Grilling cooks the food and imparts a distinctive smoky flavor, making it a popular choice for outdoor cooking, especially at social gatherings and events.

The Italy Barbeque Grill Market Report is Segmented by Fuel Type (Gas, Charcoal, Electric, Pellet, Hybrid/Alternative, Infrared), Product Design (Built-In, Freestanding, Portable/Table-top, Disposable/Single-use), Technology (Conventional, Smart/Connected), End-User (Residential, Commercial), Distribution Channel (B2B/Direct, B2C/Retail – Specialty, Home Centers & DIY, Mass Merchandisers, Online, Other), and Geography (Northern Italy, Central Italy, Southern Italy & Islands). Market Forecasts are Provided in Terms of Value (USD).

| Gas Grills |

| Charcoal Grills |

| Electric Grills |

| Pellet Grills |

| Hybrid/Alternative Fuel |

| Infrared |

| Built-In |

| Freestanding |

| Portable / Table-top |

| Disposable / Single-use |

| Conventional |

| Smart/Connected |

| Residential |

| Commercial |

| B2B/Direct from the Manufacturers | |

| B2C/Retail – Specialty Stores | Home Centers & DIY Stores |

| Mass Merchandisers | |

| Online | |

| Other Distribution Channels |

| Northern Italy |

| Central Italy |

| Southern Italy & Islands |

| By Fuel Type | Gas Grills | |

| Charcoal Grills | ||

| Electric Grills | ||

| Pellet Grills | ||

| Hybrid/Alternative Fuel | ||

| Infrared | ||

| By Product Design | Built-In | |

| Freestanding | ||

| Portable / Table-top | ||

| Disposable / Single-use | ||

| By Technology | Conventional | |

| Smart/Connected | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2B/Direct from the Manufacturers | |

| B2C/Retail – Specialty Stores | Home Centers & DIY Stores | |

| Mass Merchandisers | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | Northern Italy | |

| Central Italy | ||

| Southern Italy & Islands | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Italy barbeque grill market?

The Italy barbeque grill market size is expected to grow from USD 134.63 million in 2025 to USD 141.59 million in 2026 and is forecast to reach USD 180.13 million by 2031, at a CAGR of 4.93% over 2026-2031.

Which fuel types are leading and growing fastest in Italy?

Gas led with 49.15% share in 2025, while pellet grills are set to grow fastest at a 5.93% CAGR through 2031, supported by EUDR-aligned traceability advantages.

How do regulations influence grill choices across Italy?

Seasonal wildfire restrictions limit charcoal usage in high-risk months, and EUDR due diligence raises costs for non-traceable charcoal, which pushes demand toward gas and pellet options.

Which regions show the strongest positions and growth?

Northern Italy led with 27.54% in 2025, while Central Italy is projected to expand fastest at 6.34% CAGR to 2031, aided by tourism density and hospitality investments.

What distribution channels matter most to buyers in Italy?

B2C retail accounted for 72.61% in 2025, while online channels are projected to grow at 5.55% CAGR through 2031 as brands scale direct storefronts and accessory ecosystems.

How is technology changing the competitive landscape?

Conventional grills dominate volumes at 84.21% in 2025, but smart and connected grills will post a 6.07% CAGR to 2031 as app-guided cooking and multi-probe monitoring extend across fuel types.

Page last updated on: