Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

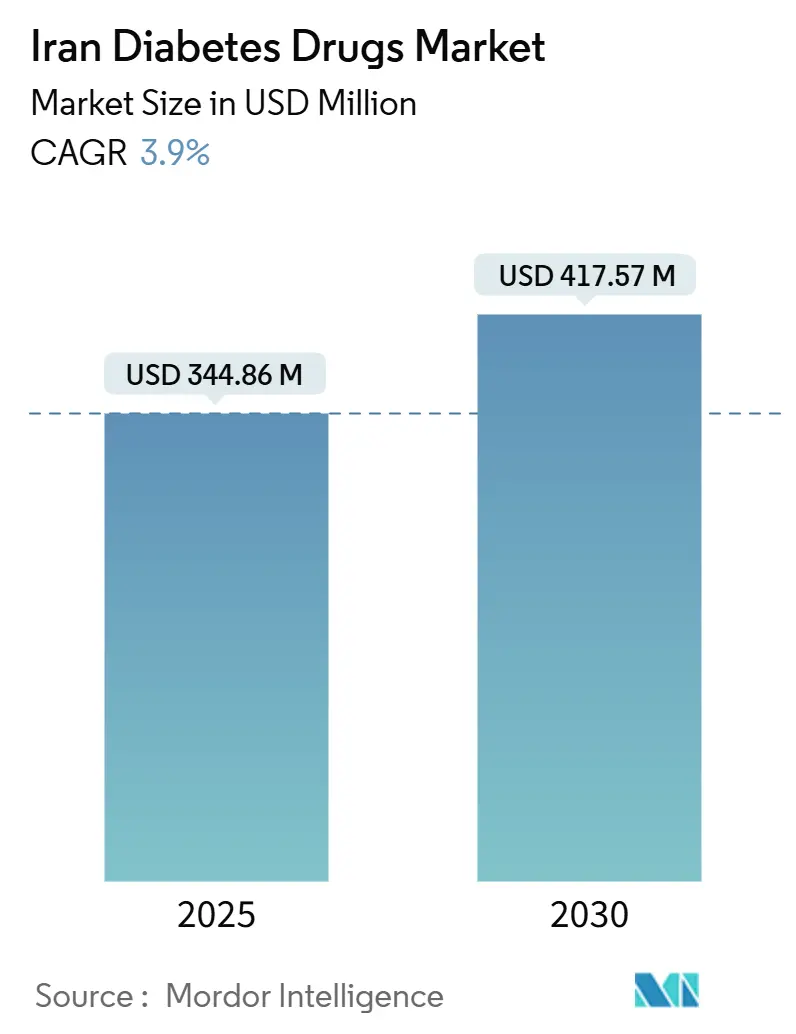

| Market Size (2025) | USD 344.86 Million |

| Market Size (2030) | USD 417.57 Million |

| Growth Rate (2025 - 2030) | 3.90% CAGR |

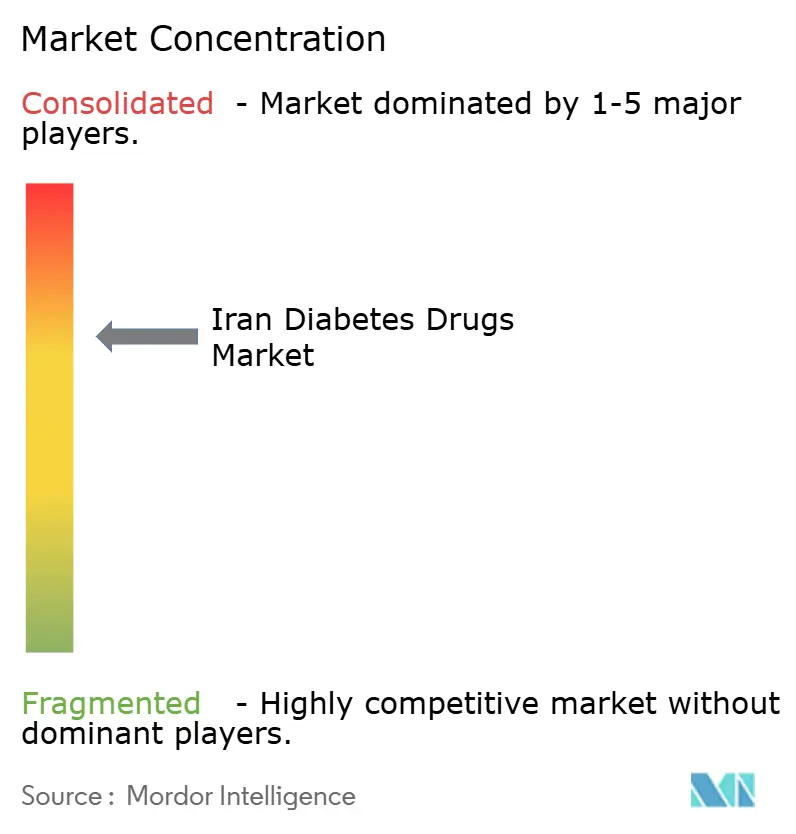

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iran Diabetes Drugs Market Analysis by Mordor Intelligence

The Iran Diabetes Drugs Market size is estimated at USD 344.86 million in 2025, and is expected to reach USD 417.57 million by 2030, at a CAGR of 3.9% during the forecast period (2025-2030).

According to the World Health Organization's 2022 report, the prevalence of diabetes in Iran stands at 10.3%, with rates of 9.6% for men and 11.1% for women. In Yazd province, the prevalence of diabetes is notably higher at 16.3%. This disease results from a combination of genetic and environmental factors.

The rapid and significant lifestyle changes observed in many countries have led to an increase in obesity and other risk factors for non-communicable diseases. Common risk factors for diabetes include being overweight, obesity, low physical activity, high fat consumption, low fiber diet, race, family history, age, low birth weight, smoking, and high blood pressure.

Diabetes mellitus poses a significant healthcare challenge in Yazd province due to its prevalence, costs, and impact on individuals' lives, although it can be managed and prevented. Lifestyle-related factors play a crucial role in the early development of type 2 diabetes. Identifying these risk factors, understanding their individual contributions, and implementing interventions based on them are essential steps in diabetes management and prevention of complications.

Overall, the rise in the use of diabetes medications in iran is a positive development that reflects the growing awareness and understanding of diabetes as a chronic disease that requires ongoing management and treatment. With continued advancements in diabetes drug treatments and increased access to healthcare services, the diabetic population in iran can look forward to better outcomes and improved quality of life in the years to come.

Iran Diabetes Drugs Market Trends and Insights

Oral-Anti Diabetes Drugs Segment is Having the Highest Market Share in the Current Year.

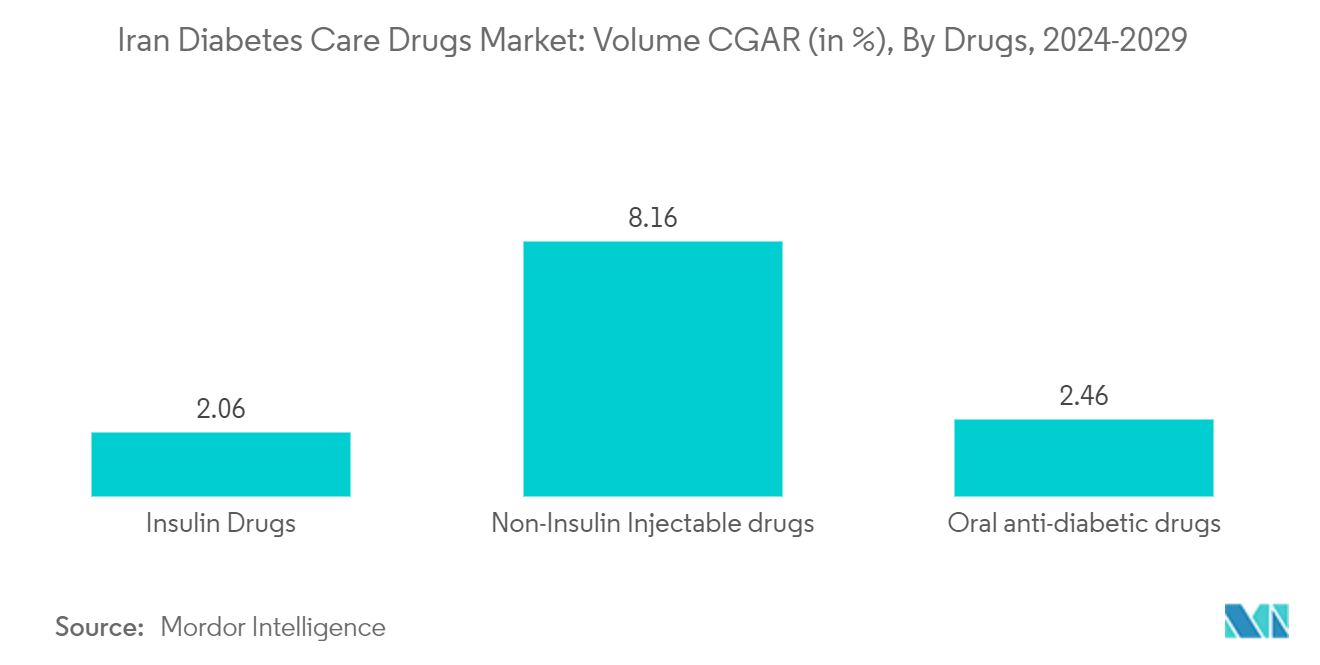

The Oral-Anti Diabetes Drugs segment is expected to increase with a CAGR of over 3.8% during the forecast period, mainly due to the demand from the diabetes population, which was more than 5.7 million by the end of the current year.

People living with Diabetes in Iran confront financial difficulties. Pharmacies do not sell enough insulin to people with diabetes; instead, insulin is sold on the open market at a higher price. Sometimes a diabetic child's parent is unable to locate insulin. Insulin costs 20-30% of a family's monthly income for type 1 diabetic children and adults. This does not include the excessively high cost of test strips and other supplies.

In addition, insurance firms in Iran are lowering financial assistance for diabetes treatments. Because insulin is scarce, Iranian families with diabetes children adapt by limiting the number of carbs in their child's diet. Though food and lifestyle are highly helpful in managing blood glucose levels, they frequently fail and necessitate oral medication therapy. If the second phase of pharmacological therapy fails, multiple oral therapies will be used.

Multiple therapies will be optimized, and in the ultimate stages, it will be shifted to oral-injectable multiple treatments. With broad modifications in hyperglycemia prescription therapy, guidelines for regulating blood glucose levels have evolved. Considering these developments in diabetes care, the trend in glucose-lowering medicines and their efficacy in blood glucose is critical.

One of the most prevalent difficulties in patients is poor drug adherence. Many patients struggle to adhere to therapy suggestions. Adherence to oral hypoglycemic medications (OHAs) ranges from 36% to 93% in controlling type 1 and type 2 diabetes. Sulphonylureas are commonly used to treat type 2 diabetes. Patient compliance is critical to the efficacy of oral diabetes therapy. It became vital to emphasize the recent status of diabetic medication adherence among type 2 diabetes patients in Tehran and the cultural variances within the same Iranian community.

Through the Iran government's encouragement, the usage of Drugs increased over the forecast period.

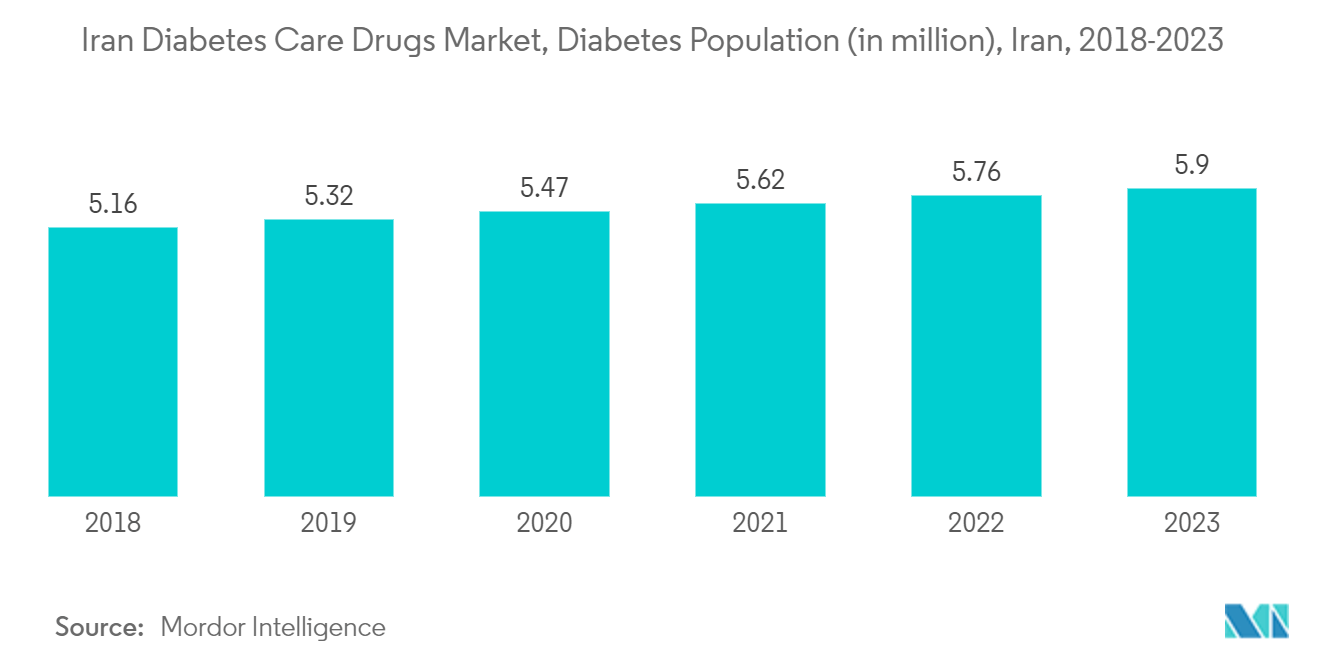

The rising prevalence of diabetes in Iran is boosting the country's diabetes drugs market.

In Iran, diabetes is a leading cause of mortality, blindness, renal failure, heart attack, stroke, and amputation of lower limbs. According to estimates by the National Program for Prevention and Control of Diabetes, diabetes will affect 9.2 million Iranians by 2030. This steady and large rise in diabetes prevalence reflects Iran's high disease burden, particularly when diabetes-related comorbidities are included.

Through serious worldwide attempts to lower the burden of diabetes, Iran's National Program for Prevention and Control of Diabetes (NPPCD) has achieved significant progress in providing effective diabetes prevention for the general population and long-term treatment for diabetic patients.

Despite the NPPCD's ongoing efforts to provide local, regional, and subnational estimates of diabetes, the current state of type-specific status, natural history, comorbidities, quality and accessibility of care, indicators of control, diabetes-related complications, and burden of diabetes among patients with diabetes in Iran remains poorly characterized.

Thus, the above factors are expected to drive the market growth over the forecast period.

Competitive Landscape

The diabetes drugs market is semi-consolidated, with few significant generic players. The insulin drugs and Sglt-2 drugs market are dominated by a few major players, like Novo-Nordisk, Sanofi, AstraZeneca, and Bristol Myers Squibb. The market for oral drugs, like Sulfonylureas and Meglitinides, comprises more generic players. The intensity of competition among the players is high, as each player is striving to develop new drugs and offer them at competitive pricing. Furthermore, players are tapping into new markets to increase their market shares, especially in emerging economies where the demand is very high compared to the supply.

Iran Diabetes Drugs Industry Leaders

Eli Lilly

Boehringer Ingelheim

Astrazeneca

Sanofi

NovoNordisk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Ozempic injection and Rybelsus tablets have been authorized for reducing blood sugar levels in adults diagnosed with type 2 diabetes mellitus, in conjunction with a proper diet and regular exercise. Furthermore, Ozempic has also received approval for its ability to decrease the risk of heart attack, stroke, or mortality in adults with type 2 diabetes mellitus and a pre-existing heart condition.

- August 2022: Tirzepatide: A weight-loss drug, is now available in UAE to treat Type 2 diabetes. Mounjaro, also known as Tirzepatide, is a US Food and Drug Administration-approved injectable prescription medication used to improve blood sugar, or glucose, through weight loss.

Iran Diabetes Drugs Market Report Scope

Diabetes or diabetes mellitus describes a group of metabolic disorders characterized by a high blood sugar level in a person. With diabetes, the body either does not produce enough insulin or the body's cells do not respond properly to insulin, or both. Iran Diabetes care drugs segment the market into Insulin, Oral Anti-Diabetic Drugs, Non-Insulin Injectable Drugs, and Combination Drugs. The report offers the value (in USD) and Volume (in unit) for the above segments.

Oral Anti-diabetic drugs

| Biguanides | Metformin |

| Alpha-Glucosidase Inhibitors | Alpha-Glucosidase Inhibitors |

| Dopamine D2 receptor agonist | Bromocriptin |

| SGLT-2 inhibitors | Invokana (Canagliflozin) |

| Jardiance (Empagliflozin) | |

| Farxiga/Forxiga (Dapagliflozin) | |

| Suglat (Ipragliflozin) | |

| DPP-4 inhibitors | Onglyza (Saxagliptin) |

| Tradjenta (Linagliptin) | |

| Vipidia/Nesina(Alogliptin) | |

| Galvus (Vildagliptin) | |

| Sulfonylureas | Sulfonylureas |

| Meglitinides | Meglitinides |

Insulins

| Basal or Long Acting Insulins | Lantus (Insulin Glargine) |

| Levemir (Insulin Detemir) | |

| Toujeo (Insulin Glargine) | |

| Tresiba (Insulin Degludec) | |

| Basaglar (Insulin Glargine) | |

| Bolus or Fast Acting Insulins | NovoRapid/Novolog (Insulin Aspart) |

| Humalog (Insulin Lispro) | |

| Apidra (Insulin Glulisine) | |

| Traditional Human Insulins | Novolin/Actrapid/Insulatard |

| Humulin | |

| Insuman | |

| Biosimilar Insulins | Insulin Glargine Biosimilars |

| Human Insulin Biosimilars |

Combination drugs

| Insulin combinations | NovoMix (Biphasic Insulin Aspart) |

| Ryzodeg (Insulin Degludec and Insulin Aspart) | |

| Xultophy (Insulin Degludec and Liraglutide) | |

| Oral Combinations | Janumet (Sitagliptin and Metformin) |

Non-Insulin Injectable drugs

| GLP-1 receptor agonists | Victoza (Liraglutide) |

| Byetta (Exenatide) | |

| Bydureon (Exenatide) | |

| Trulicity (Dulaglutide) | |

| Lyxumia (Lixisenatide) | |

| Amylin Analogue | Symlin (Pramlintide) |

| Oral Anti-diabetic drugs | Biguanides | Metformin |

| Alpha-Glucosidase Inhibitors | Alpha-Glucosidase Inhibitors | |

| Dopamine D2 receptor agonist | Bromocriptin | |

| SGLT-2 inhibitors | Invokana (Canagliflozin) | |

| Jardiance (Empagliflozin) | ||

| Farxiga/Forxiga (Dapagliflozin) | ||

| Suglat (Ipragliflozin) | ||

| DPP-4 inhibitors | Onglyza (Saxagliptin) | |

| Tradjenta (Linagliptin) | ||

| Vipidia/Nesina(Alogliptin) | ||

| Galvus (Vildagliptin) | ||

| Sulfonylureas | Sulfonylureas | |

| Meglitinides | Meglitinides | |

| Insulins | Basal or Long Acting Insulins | Lantus (Insulin Glargine) |

| Levemir (Insulin Detemir) | ||

| Toujeo (Insulin Glargine) | ||

| Tresiba (Insulin Degludec) | ||

| Basaglar (Insulin Glargine) | ||

| Bolus or Fast Acting Insulins | NovoRapid/Novolog (Insulin Aspart) | |

| Humalog (Insulin Lispro) | ||

| Apidra (Insulin Glulisine) | ||

| Traditional Human Insulins | Novolin/Actrapid/Insulatard | |

| Humulin | ||

| Insuman | ||

| Biosimilar Insulins | Insulin Glargine Biosimilars | |

| Human Insulin Biosimilars | ||

| Combination drugs | Insulin combinations | NovoMix (Biphasic Insulin Aspart) |

| Ryzodeg (Insulin Degludec and Insulin Aspart) | ||

| Xultophy (Insulin Degludec and Liraglutide) | ||

| Oral Combinations | Janumet (Sitagliptin and Metformin) | |

| Non-Insulin Injectable drugs | GLP-1 receptor agonists | Victoza (Liraglutide) |

| Byetta (Exenatide) | ||

| Bydureon (Exenatide) | ||

| Trulicity (Dulaglutide) | ||

| Lyxumia (Lixisenatide) | ||

| Amylin Analogue | Symlin (Pramlintide) | |

Key Questions Answered in the Report

How big is the Iran Diabetes Drugs Market?

The Iran Diabetes Drugs Market size is expected to reach USD 344.86 million in 2025 and grow at a CAGR of 3.9% to reach USD 417.57 million by 2030.

What is the current Iran Diabetes Drugs Market size?

In 2025, the Iran Diabetes Drugs Market size is expected to reach USD 344.86 million.

Who are the key players in Iran Diabetes Drugs Market?

Eli Lilly, Boehringer Ingelheim, Astrazeneca, Sanofi and NovoNordisk are the major companies operating in the Iran Diabetes Drugs Market.

What years does this Iran Diabetes Drugs Market cover, and what was the market size in 2024?

In 2024, the Iran Diabetes Drugs Market size was estimated at USD 331.41 million. The report covers the Iran Diabetes Drugs Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Iran Diabetes Drugs Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: