Ion Exchange Resin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

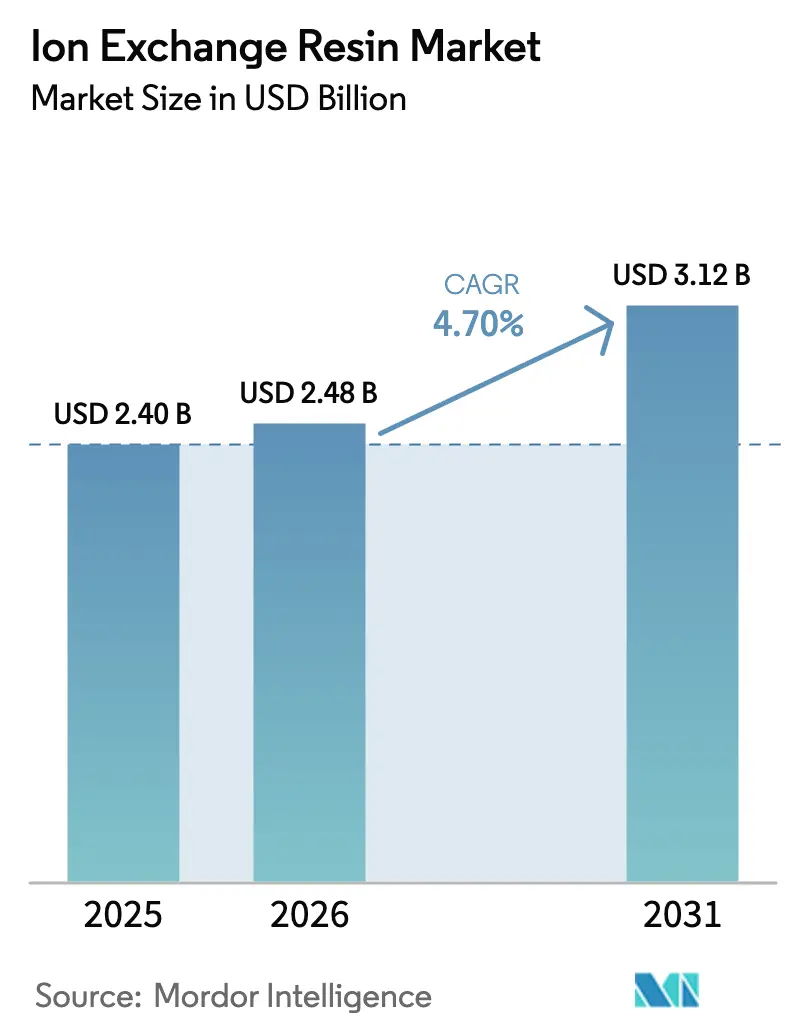

| Market Size (2026) | USD 2.48 Billion |

| Market Size (2031) | USD 3.12 Billion |

| Growth Rate (2026 - 2031) | 4.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ion Exchange Resin Market Analysis by Mordor Intelligence

The Ion Exchange Resin Market size was valued at USD 2.40 billion in 2025 and is estimated to grow from USD 2.48 billion in 2026 to reach USD 3.12 billion by 2031, at a CAGR of 4.70% during the forecast period (2026-2031). Regulatory tightening around PFAS, semiconductor-grade ultrapure-water demand, and direct-lithium-extraction projects are reallocating capital from commodity softening beads toward highly engineered chemistries. Specialty grades command premium pricing that offsets raw-material inflation, while mixed-bed systems for zero-liquid-discharge desalination and PEM electrolyzers are unlocking incremental value pools. Competitive intensity remains moderate: five multinational suppliers still control roughly 40% of installed capacity, yet Asian challengers are eroding price leadership in commodity segments through lower capital costs and faster scale-up.

Key Report Takeaways

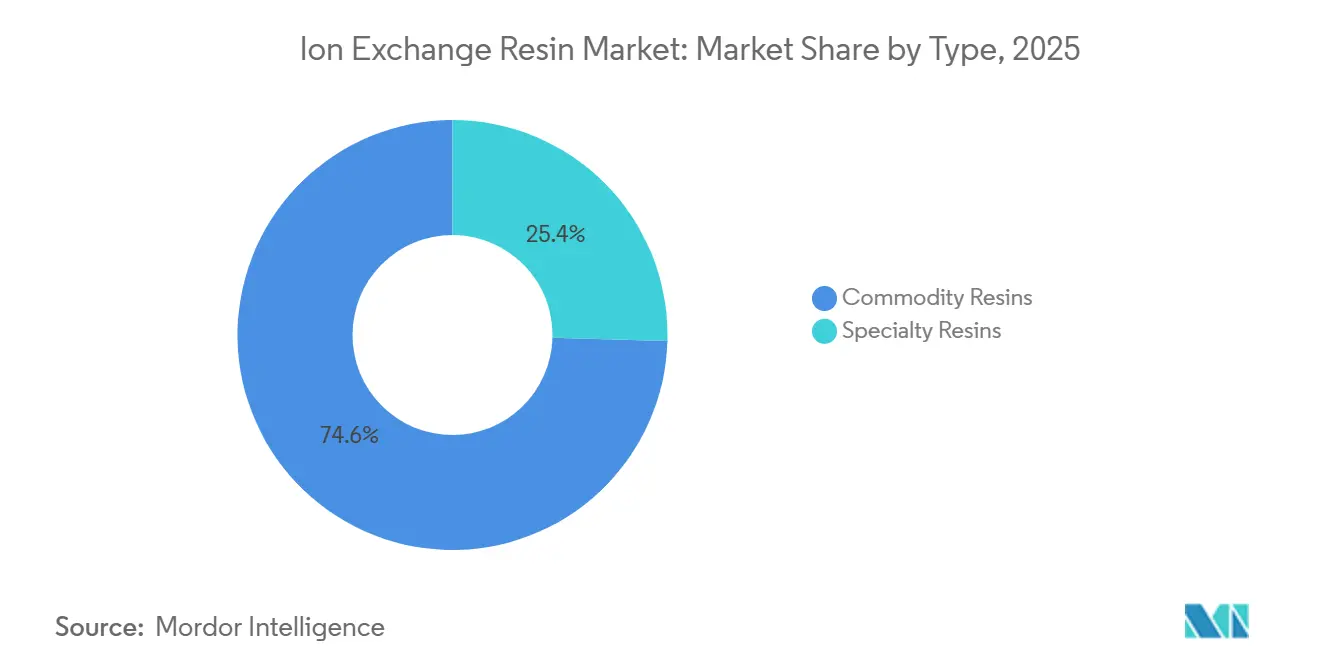

- By type, commodity resins held a 74.35% ion exchange resin market share in 2025, whereas specialty grades are advancing at a 5.23% CAGR through 2031.

- By application function, softening and demineralization captured 58.42% of 2025 revenue, while ultrapure water removal is expanding at a 6.09% CAGR through 2031.

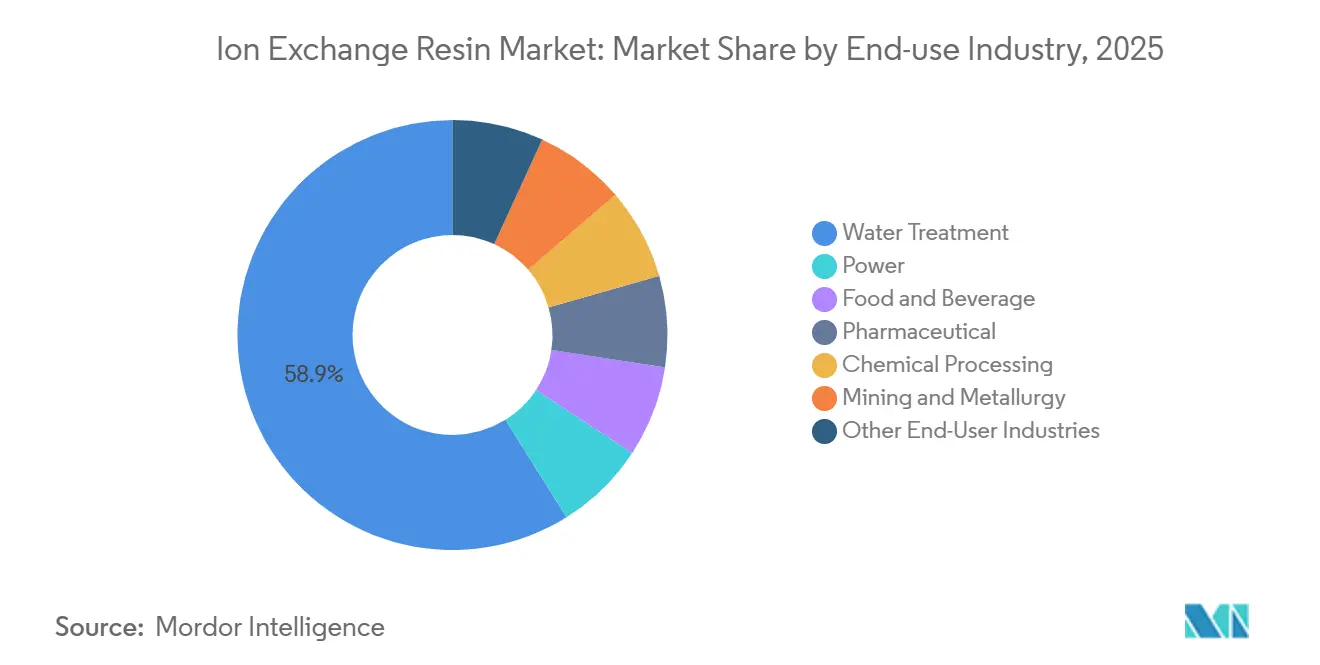

- By end-use industry, water treatment led with 52.43% of 2025 revenue; the Semiconductor and Electronics segment is forecast to grow 6.97% annually to 2031.

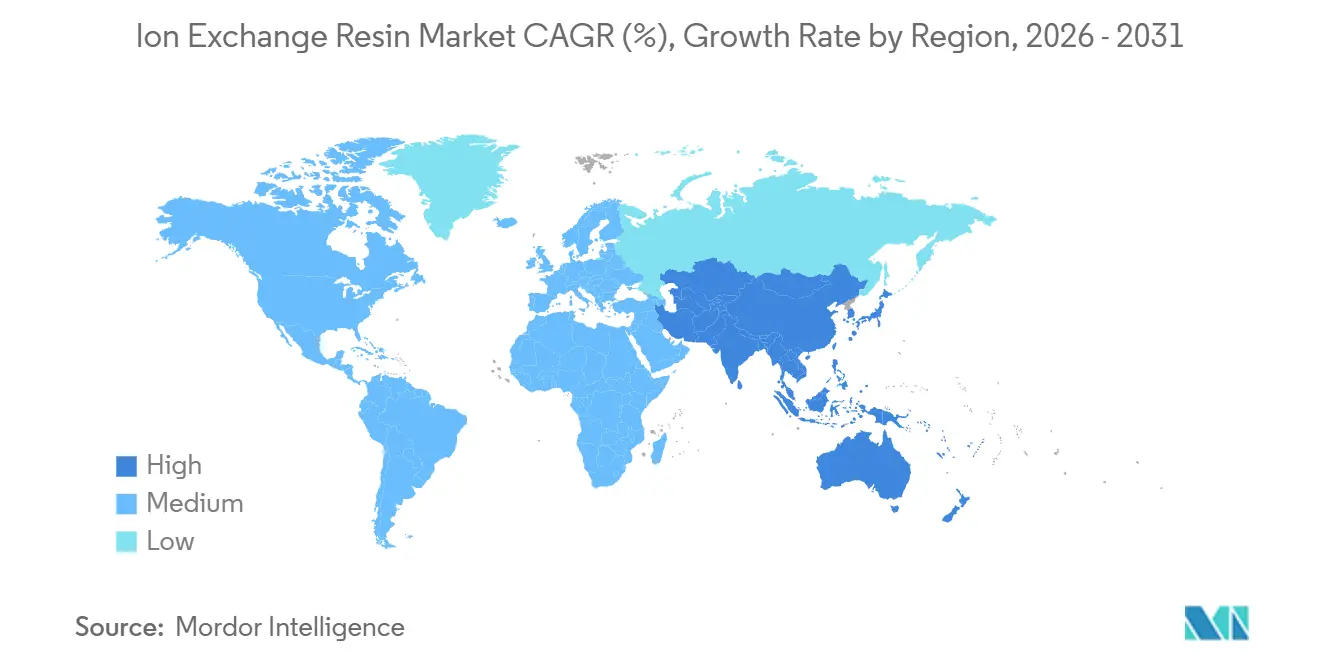

- By geography, Asia-Pacific commanded 34.59% of the 2025 value and is set to compound at 5.54% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ion Exchange Resin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor-Grade Ultrapure Water Demand in Asia-Pacific | +1.2% | Asia-Pacific core (China, South Korea, Taiwan), spillover to Japan | Medium term (2-4 years) |

| PFAS and Heavy-Metal Discharge Limits Boosting Chelating Resins in North America | +1.0% | North America, EU secondary | Short term (≤ 2 years) |

| Desalination and ZLD Megaprojects in the Middle East Raising Mixed-Bed Uptake | +0.8% | Middle East (Saudi Arabia, UAE), North Africa | Medium term (2-4 years) |

| Hydrogen-Electrolyzer Incentives Lifting PFSA Ion-Exchange Membranes in Europe | +0.6% | Europe (Germany, Netherlands, Spain), North America secondary | Long term (≥ 4 years) |

| Sugar-Decolorization Boom Driving Food-Grade Resins in South America | +0.5% | South America (Brazil, Argentina) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Semiconductor-Grade Ultrapure Water Demand in Asia-Pacific

Fabricating sub-3 nm logic chips requires water with total organic carbon below 1 ppb and resistivity above 18.2 MΩ·cm, a specification met only by nuclear-grade mixed-bed resins. Mitsubishi Chemical disclosed a 15% Diaion capacity expansion in April 2026, aimed at Taiwanese and South Korean foundries now ramping 2 nm production. SEMI standards mandate ion-exchange polishers as the final barrier before photolithography tools, displacing stand-alone membrane loops. China installed more than 200 ultrapure-water systems in 2025, each consuming 10-15 m³ of mixed-bed resin per gigawatt of fab capacity, creating supply-chain risk whenever typhoons delay styrene shipments across East Asia.

PFAS and Heavy-Metal Discharge Limits Boosting Chelating Resins in North America

The U.S. EPA finalized maximum contaminant levels of 4 ppt for PFOA and 10 ppt for PFOS in April 2024, with compliance required by 2029[1]U.S. Environmental Protection Agency, “Final PFAS National Primary Drinking Water Regulation,” epa.gov . Type II strong-base anion resins emerged as the best available technology for simultaneous removal of legacy and short-chain PFAS. Utilities in Michigan, New Jersey, and California awarded contracts exceeding USD 300 million in 2025 to retrofit granular-bed systems, even though spent-resin disposal remains unresolved. Parallel Clean Water Act updates tightened lead, cadmium, and chromium limits, accelerating uptake of iminodiacetic- and aminophosphonic-functional resins. Specialty grades now sell at 40–60% price premiums over commodity softening beads.

Desalination and ZLD Megaprojects in the Middle East Raising Mixed-Bed Uptake

Saudi Arabia’s NEOM and the UAE’s Taweelah expansion specify zero-liquid-discharge lines that combine RO, mixed-bed ion exchange, and brine crystallization. Mixed-bed units push TDS below 0.1 mg/L, enabling 98% water recovery and compliance with strict discharge bans. A 2025 Nature Water study pegged ZLD cost at USD 2.50–4.00 per m³ but noted that avoiding brine-disposal penalties offsets the premium within 5–7 years in arid regions. Resin life in Gulf seawater averages 3–4 years because high silica and organics accelerate fouling, creating repeat-purchase revenue for suppliers.

Hydrogen-Electrolyzer Incentives Lifting PFSA Membranes in Europe

Proton-exchange-membrane electrolyzers use perfluorosulfonic acid films—ion-exchange membranes that shuttle protons while blocking gas crossover. Germany installed 1.2 GW of PEM capacity in 2025, consuming about 180,000 m² of Nafion-equivalent membrane. The EU’s Horizon Europe program is funding non-PFAS alternatives, yet incumbent PFSA chemistry still delivers more than 0.1 S/cm proton conductivity at 80 °C. Membrane costs account for 12–15% of the electrolyzer stack, so any durability breakthrough in hydrocarbon ionomers could reshape the cost curve after 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Styrene and Acrylic Monomer Prices | -0.7% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Bio-Based Adsorbents Undercutting Resin Economics | -0.4% | North America, EU pilot markets | Medium term (2-4 years) |

| European Union Landfill and Incineration Restrictions on Spent Resins | -0.3% | EU-27, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Styrene and Acrylic Monomer Prices

Styrene-divinylbenzene copolymers constitute more than 80% of global output, yet styrene traded between USD 1,150 and USD 1,450 t⁻¹ in Asia during 2024-2025, lifting finished-resin costs 6–8%. Acrylic resins used in pharma and food lines face similar volatility after European acrylic-acid prices rose 22% year-on-year in H1 2025. Smaller producers in India and China, reliant on spot feedstock, saw margins compress to 7–9%, forcing consolidation and occasional plant shutdowns.

European Union Landfill and Incineration Restrictions on Spent Resins

Amended EU Waste Framework Directive classifies spent resin with heavy metals as hazardous, pushing disposal costs to EUR 800–1,500 t⁻¹ and introducing extended producer responsibility[2]European Union, “Waste Framework Directive 2008/98/EC,” eur-lex.europa.eu . LANXESS and Purolite have built take-back programs across Germany, France, and the Netherlands, but smaller firms lack scale, increasing market entry barriers and nudging some end users toward membrane alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Specialty Grades Gain on Compliance and Purity Mandates

Commodity resins delivered 74.35% of 2025 revenue, anchored by boiler-feed softening systems priced at USD 8–12 L⁻¹. However, specialty resins are projected to grow 5.33% annually, eclipsing commodity expansion by 63 bps. Lithium-selective resins launched by Sunresin and LANXESS in 2024-2025 provide Mg:Li selectivity above 100:1, enabling direct extraction from Argentine and Chilean brines. Food-grade variants that meet NSF/ANSI 61 carry USD 3–5 L⁻¹ additional cost yet prevent off-flavor recalls in beverage lines.

Macroporous beads with permanent porosity now dominate sugar-decolorization and antibiotic purification because they resist osmotic shock, extending service life. Continued migration toward compliance-driven chemistries will narrow commodity revenue share by 2031.

By Application Function: PFAS Mitigation Reshapes Demand Mix

Softening and demineralization contributed 58.42% of 2025 turnover, yet demand is plateauing as membrane alternatives gain traction in residential appliances. Driven by the rapid expansion of semiconductor fabs, sterile pharmaceutical manufacturing, and high-precision electronics assembly, the market for ion-exchange resins used in ultrapure water (UPW) production is projected to grow at a rate of approximately 6.09% through 2031. Heavy-metal removal and PFAS mitigation will expand at a moderate rate through 2031, driven by U.S. EPA and EU discharge limits. Anion beds can concentrate PFAS 10,000–50,000×, transferring liability to waste handlers and creating a secondary treatment market. Catalysis and chromatographic separations remain high-margin niches, fetching USD 60–100 L⁻¹ for thiourea-functionalized gold-recovery resins.

By End-use Industry: Semiconductor and Electronics Segment Leads Growth

Water treatment kept 52.43% of end-use revenue in 2025, underpinned by municipal, industrial boiler, and wastewater circuits. Driven by chip-fabrication node miniaturization and stringent ultrapure-water polishing requirements, the semiconductor and electronics sector is set to grow at a brisk pace, achieving a 6.97% CAGR through 2031, underscoring the industry's heightened demand for sub-ppb ionic contamination control. The pharmaceutical industry benefits from USP (1231) requirements that specify conductivity below 1.3 µS cm⁻¹. Single-use chromatography resins priced at USD 8,000–15,000 L⁻¹ are replacing stainless columns, cutting cleaning validation and cross-contamination risk. Power generation’s transition away from steam-cycle coal plants tempers resin demand, limiting growth through 2031. Mining and metallurgy garner incremental traction via lithium and rare-earth extraction, whereas food-and-beverage volumes move in tandem with sugar pricing cycles.

Geography Analysis

Asia-Pacific held 34.59% of 2025 revenue and should log a 5.54% CAGR through 2031, paced by semiconductor fabs and lithium-brine projects. China added more than 200 ultrapure-water systems in 2025, each deploying 10–15 m³ of mixed-bed resin per gigawatt of capacity. India’s pharmaceutical boom and revised Schedule M water codes are catalyzing mixed-bed upgrades, while ASEAN markets such as Vietnam and Malaysia are attracting greenfield electronics investments. Volatile styrene feedstock—26% price swing peak-to-trough in 2024-2025—compresses margins for producers without vertical integration.

In North America, EPA PFAS rules mean 6–10% of U.S. public water systems will require anion-exchange retrofits by 2029. Canada’s oil-sands projects rely on ion exchange to polish produced water, but capex cuts in Alberta curb incremental demand. Mexico’s near-shoring inflow is pushing electronics-coating lines that require ultrapure water, expanding the ion exchange resin market across the USMCA corridor.

Europe trails in growth as landfill restrictions raise lifecycle costs, yet the bloc retains a technology edge. EU hydrogen targets of 40 GW electrolyzer capacity by 2030 imply cumulative PFSA membrane demand of 6–8 million m², though AEM pilots could partially cannibalize PFSA volumes. South America concentrates in Brazil and Argentina, where sugar refining and mining projects drive food-grade and chelating resin adoption. The Middle East and Africa drive demand as desalination and zero-liquid-discharge mandates rolled out across Saudi Arabia, the UAE, and Qatar.

Value Chain Analysis

The value chain starts with petrochemical feedstocks, primarily styrene and divinylbenzene for styrene-DVB matrices, plus acrylic monomers for niche grades. It then moves through catalysts and functionalizing reagents, followed by polymerization, bead sizing, and chemical functionalization, such as sulfonation for cation resins and amination routes for anion resins. Finished resins are supplied to OEMs and system integrators, including municipal and industrial water-treatment skids, semiconductor UPW tool chains, and industrial wastewater packages, before reaching end users such as utilities, fabs, refineries, and process industries. Within the report scope, revenues are tied to new resin sales rather than operating contracts or disposal services.

Value-add and bottlenecks concentrate in high-purity specialty production steps, including clean manufacturing, tight ionic contamination control, and consistent bead morphology for mixed-bed and semiconductor UPW applications. Capacity actions by established producers and product introductions in higher-value niches point to where qualification barriers and margins are strongest. For example, Mitsubishi Chemical is expanding semiconductor UPW-focused ion exchange resin production at its Kyushu-Fukuoka plant, with operations commencing in April 2026, while DuPont launching AmberChrom TQ1 in May 2025 for biopharmaceutical purification highlights how specialty segments differ from commodity softening beads.

Competitive Landscape

The ion exchange resin industry exhibits moderate concentration, with LANXESS, DuPont, Mitsubishi Chemical, Ecolab, and Samyang Corporation collectively holding an estimated 55% of global capacity. Chinese challengers such as Sunresin and Suqing Group expand specialty output at capital costs 40–50% lower than Western peers, eroding commodity margins. DuPont filed 14 patents in 2024-2025 for PFAS-free membranes targeting electrolyzer applications. LANXESS partnered with Veolia in January 2026 to supply Lewatit chelating beads for a Saudi Aramco ZLD facility, illustrating a pivot toward lifecycle-service contracts. ResinTech and Eichrom carve out analytical niches, selling ultra-pure beads at USD 200 L⁻¹. Bio-based adsorbents and electrodeionization units pose long-run substitution threats, but current durability gaps confine them to pilots.

Ion Exchange Resin Industry Leaders

DuPont

LANXESS

Mitsubishi Chemical Group Corporation

Ecolab

Samyang Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Unmet need is concentrated where ion exchange resins solve problems that membranes or conventional sorbents struggle to address at the required purity and selectivity. This includes semiconductor-grade ultrapure water polishing, industrial PFAS removal (including short-chain species), nuclear-grade primary-loop cleanup, and selective hydrometallurgy streams. Recent proof points align with that shift, with Mitsubishi Chemical bringing additional ion exchange resin capacity online in April 2026 for semiconductor UPW demand and LANXESS reporting industrial-use performance for Lewatit MDS TP 108 in PFAS-contaminated wastewater in May 2026. Together, these updates reinforce the move away from commodity softening beads toward engineered grades that require qualification and support premium pricing.

White space also persists in lifecycle and performance-linked offerings aimed at reducing end-user risk without changing the report sizing boundary. These include higher selectivity PFAS anion resins that address ultrashort-chain breakthrough, resin designs that maintain kinetics under fouling-prone ZLD and desalination pretreatment conditions, and nuclear-grade localization initiatives that tighten supply assurance. The July 2026 in-reactor validation of a domestically produced nuclear-grade ion exchange resin in the primary loop at Hainan Nuclear Power indicates how qualification pathways are opening for new suppliers in critical applications. At the same time, continued feedstock volatility, including styrene and acrylic monomers, keeps attention on formulation efficiency and regional manufacturing footprints.

Recent Industry Developments

- July 2026: Samyang Corporation reported supplying TRILITE UPRM300U and TRILITE UPRM400U high-value resins for semiconductor ultrapure water systems to South Korean manufacturers. The update highlights accelerating qualification and localization of UPW media for advanced fabs, supporting a specialty mix rather than reliance on commodity softening grades.

- October 2025: IEI inaugurated a new resin manufacturing facility in Roha, Maharashtra, as part of its expansion strategy. The greenfield plant is designed for a total capacity of 42,600 m3 per annum and began operations with an initial phase capacity of 3,696 m3, strengthening regional supply availability for India-focused water and industrial demand.

- October 2024: Mitsubishi Chemical Group Corporation increased production capacity of ion exchange resins used in ultrapure water production for semiconductor manufacturing processes at its Kyushu-Fukuoka Plant in Japan. The move tightened supply for high-purity mixed-bed and UPW grades and reflected a capex shift toward semiconductor-linked resin chemistries.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is counted as revenues from sales of new synthetic ion exchange resins used to purify, separate, or decontaminate liquid streams across municipal and industrial use cases, with cation, anion, and mixed-bed resins treated as the media.

Scope exclusions: This sizing excludes off-site regeneration services, on-site operating contracts, chromatography resins for bioprocessing, and spent-resin disposal or resale revenues.

Segmentation Overview

- By Type

- Commodity Resins

- Specialty Resins

- By Application Function

- Softening and Demineralization

- Ultrapure Water Production

- Heavy-Metal Removal and PFAS Mitigation

- Catalysis and Separation (Non-Water)

- Sugar Decolorization and Food and Beverage Purification

- Precious-Metal Recovery and Hydrometallurgy

- By End-use Industry

- Water Treatment

- Power

- Food and Beverage

- Pharmaceutical

- Chemical Processing

- Mining and Metallurgy

- Other End-User Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with public numbers that help us map demand signals and realistic supply capacity before resin consumption assumptions are built. Common inputs include government water and wastewater statistics such as US EPA releases, Eurostat water data, and India CPCB references, followed by trade and production indicators from sources such as UN Comtrade, national customs summaries, and industrial production series.

To keep the resin context grounded, we also review standards and technical literature such as ASTM and peer-reviewed journals on demineralization, condensate polishing, and contaminant removal performance. This helps when translating end-use activity into resin consumption logic for cation, anion, and mixed-bed systems. Company annual reports, investor presentations, and press coverage are then used to cross-check capacity additions, price movement commentary, and application mix. In a few places, paid subscriptions for company financials and patent databases are used to fill gaps around product ownership, positioning, and technology direction. These desk sources are illustrative only, and many other public references are also consulted for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk sources cannot fully explain, especially application-level volume splits, price bands by resin chemistry, and the pace of replacement versus new installations. We speak with stakeholders across the chain, including resin producers, distributors, EPC and water-treatment solution providers, and large end users across power, municipal water, chemicals, food processing, and electronics grade water, and then align these views across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 19% | APAC: 50% |

| Mid tier: 44% | Functional/Unit leaders: 23% | EMEA: 30% |

| Smaller Players: 20% | Managers: 58% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where water treatment and industrial processing activity is translated into a resin demand pool using penetration and replacement logic, then the totals are distributed by region and key end uses. After the demand pool is formed, we check it against supply-side signals using selective bottom-up approximations such as a sampled roll-up of producer sales, channel feedback on shipment momentum, and simple ASP times volume checks for the major resin families.

A few inputs that matter in this market are tracked consistently, including installed and new water treatment capacity additions, regeneration and replacement cycles (which change consumption even when plants are not expanding), shifts toward ultrapure water requirements in electronics and power, and contaminant-driven upgrades such as PFAS related treatment where applicable. We also watch feedstock and energy-linked cost pressure, since it can move realized prices, and we validate regional import and export patterns to avoid counting the same resin volume twice.

Forecasts are produced using scenario analysis supported by a light multivariate regression where demand is linked to a small set of drivers such as municipal water capex, industrial output proxies, and energy and power capacity trends. Where bottom-up information is incomplete for smaller geographies, gaps are handled by using calibrated per-capita or per-output intensity factors reviewed with interview feedback, then normalized so regional totals still match the broader demand pool logic.

Data Validation & Update Cycle

Validation is done by comparing outputs against independent signals such as regional trade flows, published plant addition pipelines, and changes in end-use activity that should show up in resin demand within a reasonable lag. If a region shows a jump that these checks do not support, assumptions on replacement rate, price progression, and application mix are revisited and then rechecked through follow-up expert outreach.

Before sign-off, the model is reviewed in multiple steps so calculations, unit conversions, and year-to-year movements are consistent and explainable. The report is refreshed annually, and interim updates are made when a material event occurs such as a major capacity start-up, regulation-driven demand change, or unusual price movement. Right before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Ion Exchange Resin Market Sizing Compared With Other Published Estimates

Published market sizes for ion exchange resin can look different even when the topic label sounds the same, since the counted revenue lines are not always consistent and year choices do not line up. The variation also comes from how firms handle price trends, whether they treat replacement demand separately, and how often the model is refreshed.

In this study, the spread is mainly explained by what gets included beyond new resin sales, since some estimates bundle regeneration and operating contracts, or they mix in bioprocessing chromatography resins that follow a different demand cycle and pricing logic. Another driver is the base year selection, because a 2025 value will not match a 2026 value even under the same growth rate, and the gap widens when currency conversion timing and price escalation assumptions are handled differently.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.48 B (2026) | |

| Global Consultancy A | USD 2.96 B (2025) | Uses a different base year and appears to apply a faster growth path, and the scope notes shown do not call out exclusions for regeneration-linked services or adjacent resin categories, which can raise the counted revenue. |

| Industry Publisher B | USD 2.04 B (2025) | Leans toward a narrower 2025 value that can result from conservative pricing and replacement assumptions, and the available scope description does not clarify whether specialty applications with higher ASPs are fully counted. |

The comparison shows that year alignment and clear inclusion rules are the two biggest reasons for the spread, followed by how ASP movement is modeled across end uses. By keeping the number tied to new resin sales and explicitly excluding regeneration services and chromatography resins, the total is kept closer to the repeatable demand pool and price checks used by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the ion exchange resin market?

The ion exchange resin market size is USD 2.48 billion in 2026 and is on course for USD 3.12 billion by 2031.

Which region leads demand growth for ion-exchange resins?

Asia-Pacific leads, capturing 34.59% of 2025 revenue and posting a forecast 5.54% CAGR through 2031.

Which application is expanding fastest?

Ultrapure Water Production is growing 6.09% annually, outpacing all other functions.

Why are specialty resins gaining share?

Regulatory mandates in semiconductors, pharma, and PFAS remediation favor high-purity, selective chemistries that command premium pricing.

Page last updated on: