IO-Link System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

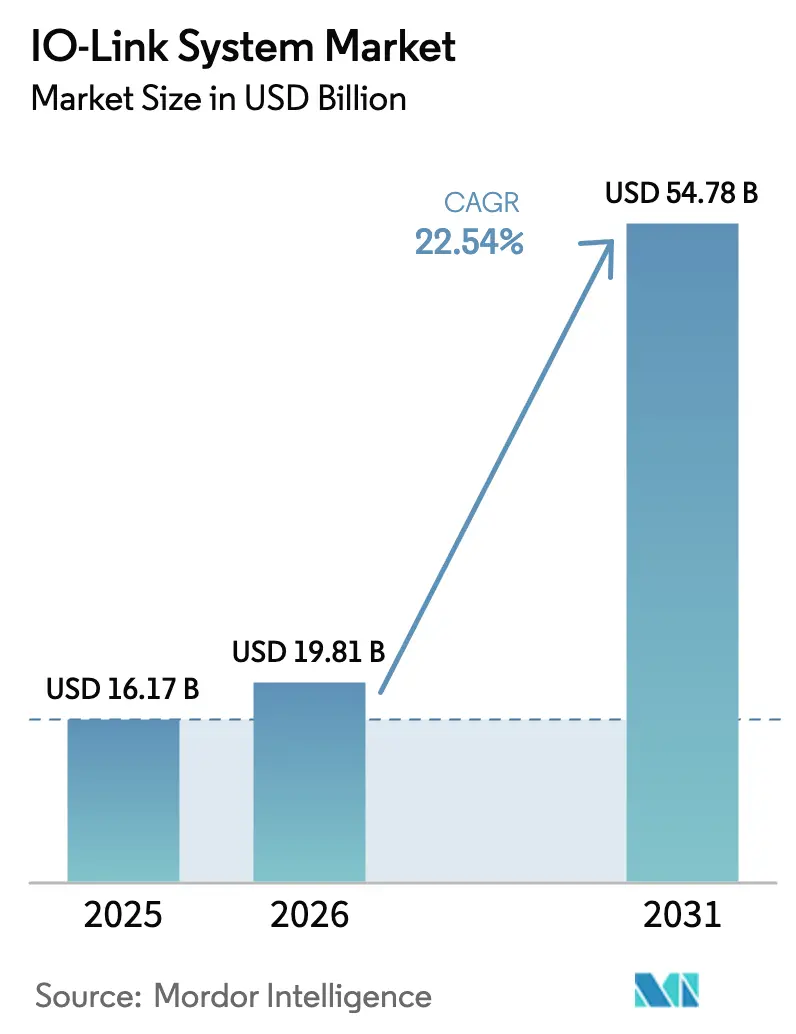

| Market Size (2026) | USD 19.81 Billion |

| Market Size (2031) | USD 54.78 Billion |

| Growth Rate (2026 - 2031) | 22.54% CAGR |

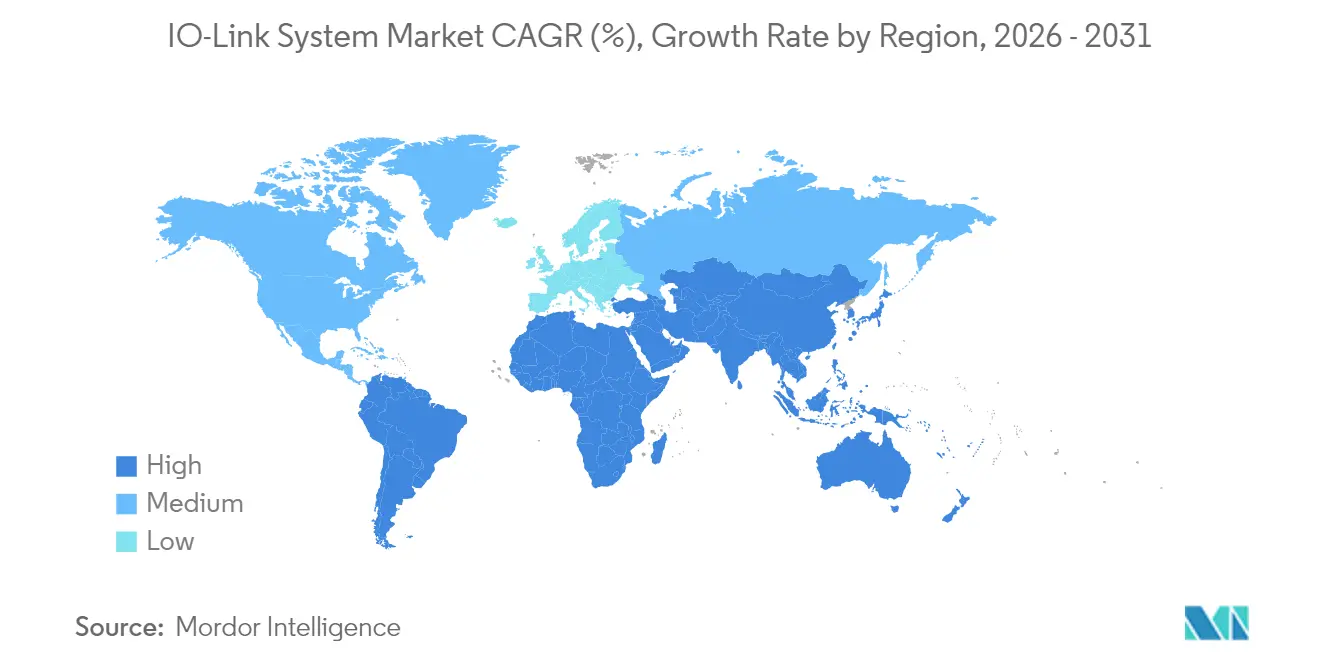

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

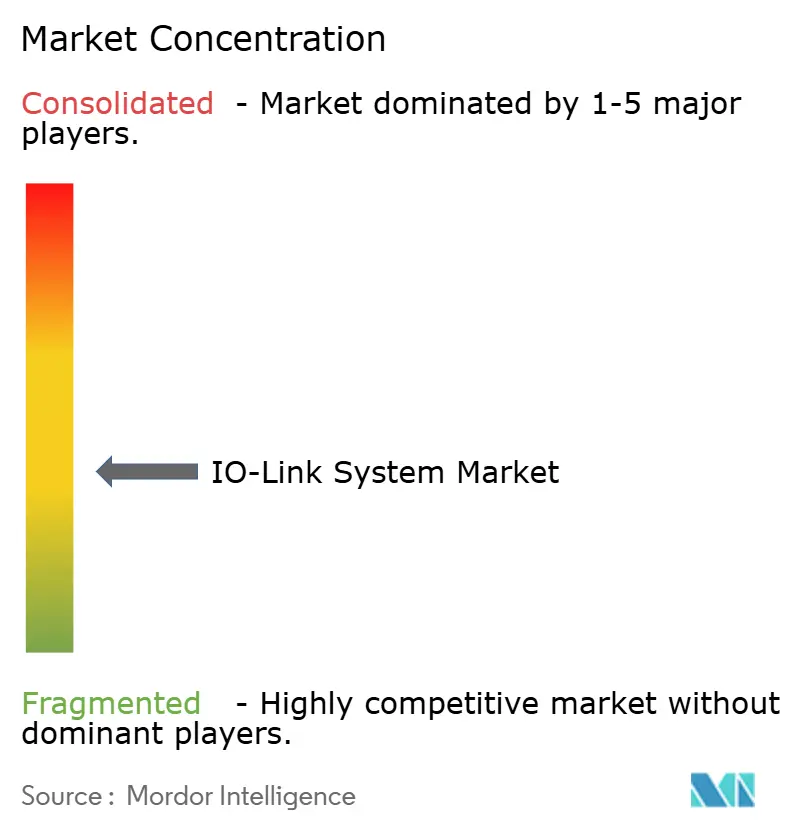

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IO-Link System Market Analysis by Mordor Intelligence

The IO-Link system market size is expected to grow from USD 16.17 billion in 2025 to USD 19.81 billion in 2026 and is forecast to reach USD 54.78 billion by 2031 at 22.54% CAGR over 2026-2031. This trajectory reflects a steady evolution from a point-to-point sensor protocol to a full ecosystem that embeds edge computing and real-time analytics at the field level. Standardization under IEC 61131-9 and the installation of 51.6 million IO-Link nodes worldwide in 2024 have improved interoperability and shortened commissioning cycles.[1]PROFIBUS International, “IO-Link Member's Assembly: Success for Innovation and Growth,” profibus.com Adoption remains strongest where downtime is costly, such as German precision machining, North American automotive retrofits, and Nordic intralogistics facilities. Suppliers are integrating artificial intelligence into gateways that sit closer to machines, lowering latency and cutting cloud traffic volume. Consolidation among automation majors and long-range wireless collaborations indicate that comprehensive solution portfolios, not single products, will shape competitive advantage.

Key Report Takeaways

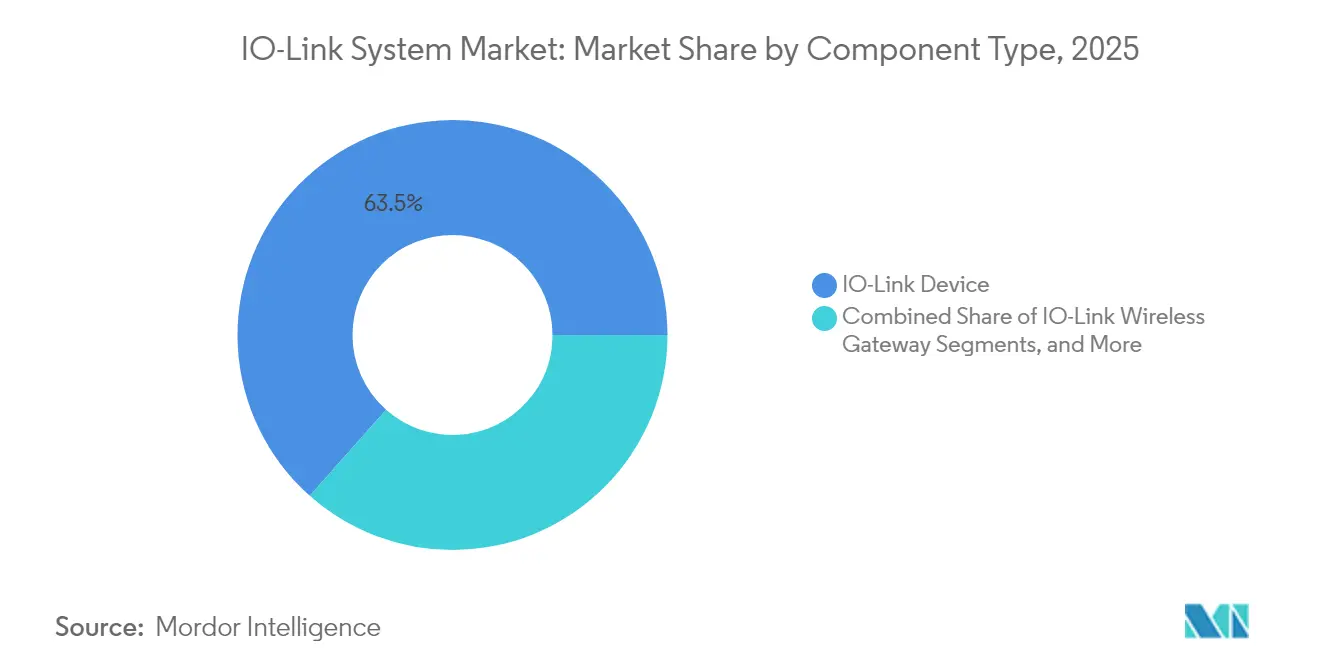

- By component type, IO-Link devices led with 63.45% revenue share in 2025, while the wireless gateway segment is on track for a 31.08% CAGR to 2031.

- By integration architecture, PLC-embedded modules accounted for 47.65% of the IO-Link system market size in 2025, whereas edge or cloud gateways will expand at 29.06% CAGR through 2031.

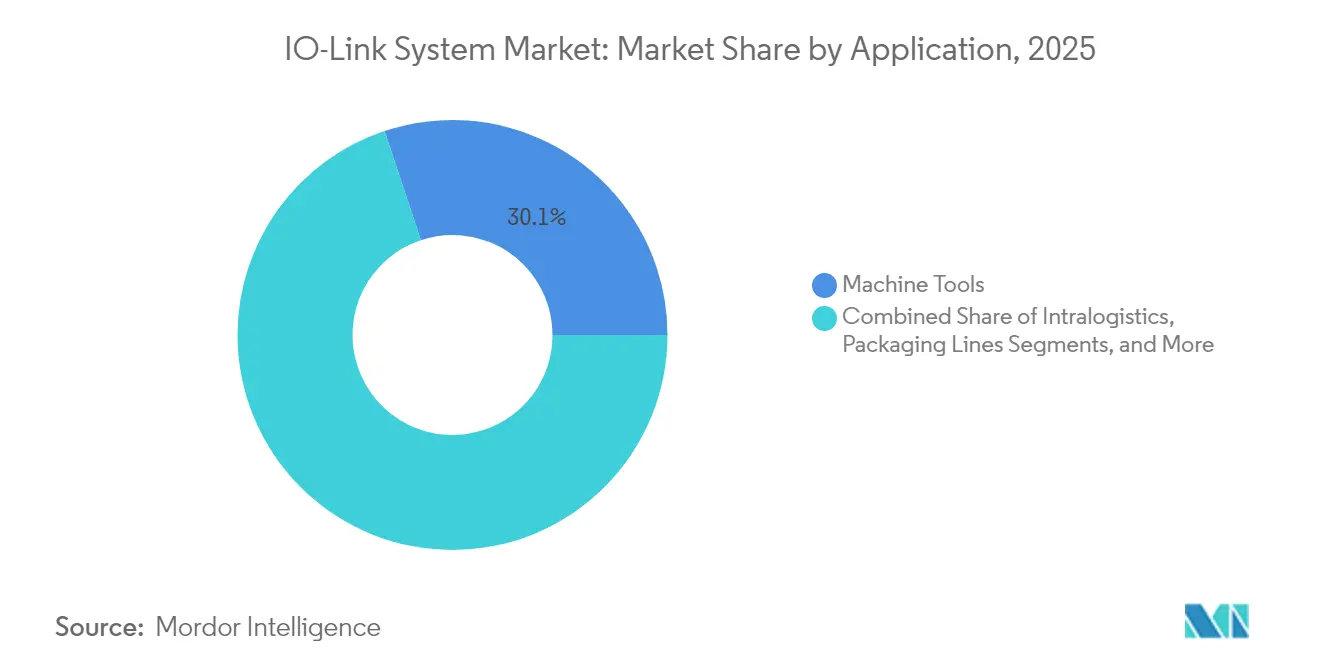

- By application, machine tools captured 30.12% of the IO-Link system market share in 2025, while intralogistics is projected to grow at 26.71% CAGR between 2026 and 2031.

- By end-user industry, discrete manufacturing held 67.85% share in 2025, whereas process manufacturing will post the fastest 27.72% CAGR to 2031.

- By region, Europe led with a 34.12% share in 2025; Asia-Pacific is set to register the highest 25.87% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of IO-Link System Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ramp-up of Industry 4.0 retrofitting projects in North American automotive plants | +5.5% | North America | Medium term (2-4 years) |

| High-speed IO-Link-SPE adoption in German machine-tool hubs | +4.4% | Europe | Medium term (2-4 years) |

| Smart-factory grants accelerating IO-Link uptake in South Korean SMEs | +3.7% | South Korea | Short term (≤ 2 years) |

| Data-rich sensor networks for continuous pharma manufacturing in Ireland | +4.2% | Europe | Medium term (2-4 years) |

| Predictive-maintenance-as-a-service boom in Nordic intralogistics warehouses | +3.0% | Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ramp-up of Industry 4.0 retrofitting projects in North American automotive plants

Automotive producers replaced hard-wired sensors with IO-Link masters that interface directly with existing Wi-Fi, cutting cabinet footprints by 50% and trimming downtime by 30%. Wireless blocks also removed the need for new PLCs in selected stations, enabling payback periods of less than 18 months.

High-speed IO-Link-SPE adoption in German machine-tool hubs

Milling and turning centres now stream vibration, flow, and temperature data ten times faster than classic IO-Link while preserving cost advantages. Starrag reported shorter backup cycles and remote parameter changes that minimized unscheduled stoppages.

Smart-factory grants accelerating IO-Link uptake in South Korean SMEs

Government support that funds half of the implementation costs has broadened access among small manufacturers. Deployments with CoreTigo wireless links reduced CO₂ emissions and aligned with national sustainability targets.

Data-rich sensor networks for continuous pharma manufacturing in Ireland

Pharma plants shifted from batch to continuous processes and achieved 15% cost savings by pairing IO-Link with OPC UA for regulatory traceability.[2]Pepperl+Fuchs SE, “Absolute Encoder With IO-Link Interface for Precise Position Detection in Packaging Machines,” pepperl-fuchs.com Precision encoders ensured 0.1° accuracy at 12,000 RPM on high-speed packaging lines.

Restraints Impact Analysis of IO-Link System Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity certification gaps in US FDA-regulated facilities | −3.5% | North America | Medium term (2-4 years) |

| Price pressure from low-cost Chinese proprietary sensor buses | −2.8% | Global | Short term (≤ 2 years) |

| Space constraints in compact European packaging machines | −1.8% | Europe | Short term (≤ 2 years) |

| Shortage of IO-Link commissioning skills in ASEAN | −2.3% | Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity certification gaps in US FDA-regulated facilities

Pharma and medical device plants incurred 25-40% higher validation costs because no uniform standard exists for IO-Link security. Projects stretched by up to six months as teams created bespoke test protocols.

Price pressure from low-cost Chinese proprietary sensor buses

Alternate buses that cost 30-40% less than IO-Link captured share in price-sensitive applications, pushing established vendors to highlight total-cost savings and develop entry-level lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

IO-Link System Market Segment Analysis

By Component Type:

Wireless gateways redefine industrial connectivityThe IO-Link system market size for component sales remained dominated by devices, yet 63.45% of 2025 revenue derived from smart sensors that now bundle multiple measurements in a single housing. Wireless gateways posted a 31.08% CAGR outlook because they eliminate cable wear on rotating machinery and reduce installation labour. SICK’s model supports 16 nodes with dynamic frequency hopping that sustains data integrity in noisy plants.

Masters evolved toward higher channel densities. Turck released an 8-port IP69K module that also offers 16 configurable digital inputs for harsh food environments. Sensor hubs shrank footprints by 40%, enabling retrofits in confined cabinets. Safety versions that comply with IEC 61139-2 reached Performance Level e through Pilz modules. Phoenix Contact’s contactless couplers transmitted 18 W across a 7 mm air gap and 230.4 kbps data, cutting maintenance on pick-and-place heads.

By Integration Architecture:

Edge computing drives gateway innovationPLC-embedded modules delivered 47.65% of 2025 revenue, yet the IO-Link system market is pivoting toward decentralized intelligence. Edge or cloud gateways are forecast to compound at 29.06% as latency-critical analytics move closer to machines. Hilscher’s sensorEDGE FIELD hosts two container engines and pushes data directly to management software, reducing cloud round-trips.

Stand-alone point-to-point links still serve isolated critical loops. However, multi-protocol masters like IFM’s SolutionBlock now ship with onboard OPC UA, MQTT, and secure HTTPS for enterprise integration. NTP synchronization yields microsecond-level alignment, ensuring that time-stamped events correlate across disparate assets. Such capabilities encourage users to migrate toward modular gateways that can scale analytics workloads without plant-wide controller upgrades.

By Application:

Intralogistics emerges as the growth leaderThe intralogistics segment is projected to grow at a 26.71% CAGR, the highest within the IO-Link system market, owing to warehouse operators targeting IO-Link to enable flexible conveyors, automated storage, and robot shuttles. Wireless nodes collect vibration and temperature readings on constantly moving carriers, feeding predictive-maintenance dashboards that avoid fulfillment delays.

Machine tools remained the largest slice at 30.12% of 2025 revenue. High-speed data streams allow in-process measurement and adaptive control that preserve tight tolerances. Packaging lines shortened changeovers from 90 minutes to 30 minutes when Balluff’s guided format architecture let operators store recipes inside sensor memory. Assembly and test cells leveraged RFID read/write heads with IO-Link to secure traceability and secure password access.

By End-user Industry:

Process manufacturing accelerates adoptionProcess manufacturers are projected to lift spending at a 27.72% CAGR as regulators demand real-time traceability. Endress+Hauser rolled out hygienic IO-Link transmitters for CIP processes that withstand caustic wash-downs. The IO-Link system market size tied to food and beverage is expected to expand steadily as energy-efficient production lines replace legacy analog loops.

Discrete manufacturers still commanded 67.85% of 2025 revenue. Automotive plants installed IO-Link vibration nodes on body-in-white lines to reduce unplanned stoppages. Semiconductor fabs adopted chemical supply sensors with digital outputs that met strict purity requirements. A French bottling plant that runs 30,000 PET units per hour used IO-Link and AS-i to automate data capture and cut capex on field wiring.

Geography Analysis

Europe IO-Link System Market

Europe led the IO-Link system market with a 34.12% slice in 2025. German machining centres adopted IO-Link-SPE to transmit high-frequency vibration data that guides adaptive control, and Phoenix Contact advanced contactless couplers for rotating equipment. Italy and Switzerland followed through precision equipment exports, while the United Kingdom and France applied IO-Link to flexible packaging and automotive stamping.

APAC IO-Link System Market

Asia-Pacific is forecast to record a 25.87% CAGR through 2031 as China upgrades assembly plants and local sensor suppliers join the IO-Link Community. South Korean grants cover half of the project costs for SMEs, prompting network effects across tier-one supply chains. Japanese robotics integrators deploy IO-Link in high-mix lines that require fast tool change. India and several ASEAN economies are adopting the protocol despite commissioning skill shortages, supported by multinational investments that bundle training with equipment.

The Americas and GCC IO-Link System Market

North America maintained strong demand through retrofit programs in automotive assembly, where wireless masters cut downtime and cabinet space. FDA-regulated industries progressed cautiously because of cybersecurity certification gaps, yet suppliers began shipping pre-validated stacks to close compliance hurdles. Canada’s resource sector relied on IP69K hubs for mine and mill automation, while Mexico leveraged IO-Link within new automotive and electronics plants near the border. South America and the Middle East remain nascent, with Brazil and the Gulf Cooperation Council emphasizing diversified manufacturing that could lift regional adoption over the next decade.

Competitive Landscape

More than 485 companies belonged to the IO-Link Community in 2024, yet consolidation advanced as majors purchased niche innovators to build end-to-end portfolios. Market leaders layered edge analytics, wireless, and cybersecurity features into product suites. CoreTigo secured alliances with Emerson to retrofit air treatment units and cut energy use in compressed-air networks. The mioty alliance partnered with the IO-Link Community to enable long-range sensor feeds while keeping the existing toolchain, broadening addressable applications.

Semiconductor vendors entered aggressively. Renesas launched a four-channel master IC that drives 500 mA per port, plus a dual-channel conditioner with an integrated stack, reducing board space for sensor makers. Phoenix Contact expanded the Axioline E remote I/O line with rugged IP69 modules that shorten installation time in wash-down zones. PULS integrated an IO-Link interface into power supplies, enabling remote diagnostics on critical voltage rails.

White-space opportunities revolve around cyber-secure stacks for FDA facilities, cost-adjusted variants to fight low-price Chinese buses, and miniaturized hubs for compact machines. Suppliers that merge several pain-point solutions—wireless, safety, analytics, and security—in a single platform are positioned to capture incremental share as buyers consolidate vendor lists.

IO-Link System Industry Leaders

Balluff GmbH

ifm electronic gmbh

Siemens AG

Pepperl + Fuchs SE

Turck Holding GmbH

- *Disclaimer: Major Players sorted in no particular order

IO-Link System Market Companies Covered in this Report

- Balluff GmbH

- ifm electronic gmbh

- Siemens AG

- Pepperl + Fuchs SE

- Turck Holding GmbH

- SICK AG

- Banner Engineering Corp.

- Omron Corporation

- KEYENCE Corporation

- Beckhoff Automation GmbH

- Weidmüller Interface GmbH

- Baumer Electric AG

- Leuze electronic GmbH

- Phoenix Contact GmbH

- WAGO Kontakttechnik GmbH

- Murrelektronik GmbH

- Bihl + Wiedemann GmbH

- Carlo Gavazzi Holding AG

- Festo SE & Co. KG

- Sensata Technologies Inc.

- Endress + Hauser Group

- Rockwell Automation Inc.

- Bosch Rexroth AG

- Schneider Electric SE

- Eaton Corporation plc

- Contrinex SA

Recent Industry Developments in IO-Link System Market

- May 2025: Phoenix Contact launched contactless IO-Link couplers enabling 18 W power and 230.4 kbps data across a 7 mm air gap.

- May 2025: The mioty alliance and the IO-Link Community signed a cooperation agreement to align data models for long-range sensing.

- May 2025: SICK released an IO-Link wireless gateway that connects 16 sensors with plug-and-play installation.

- February 2025: PULS introduced a power supply featuring an IO-Link interface and onboard display.

IO-Link System Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the IO-Link system market as all revenue generated from new IO-Link masters, devices, hubs, and protocol-certified gateways that enable point-to-point digital communication between sensors or actuators and higher-level controllers under IEC 61131-9. We include associated configuration firmware that is bundled with hardware at first sale, across discrete, process, and hybrid industries worldwide.

Scope exclusion: After-market adapter kits that retrofit non-compliant serial buses into an IO-Link-like signal path are not counted.

Segments Covered in This Report

- By Component Type

- IO-Link Master

- IO-Link Device

- IO-Link Wireless Gateway

- Sensor / Actuator Hub

- By Integration Architecture

- Stand-alone Point-to-Point

- PLC-Embedded Module

- Edge / Cloud Gateway

- By Application

- Machine Tools

- Intralogistics

- Packaging Lines

- Assembly and Test Lines

- By End-user Industry

- Discrete Manufacturing

- Automotive

- Electronics and Semiconductor

- Machinery and Equipment

- Process Manufacturing

- Food and Beverage

- Pharmaceuticals

- Chemicals

- Discrete Manufacturing

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- ASEAN

- India

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- GCC

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed factory-automation engineers, component distributors, and protocol-certification experts across North America, Germany, China, and Brazil. These conversations verified node penetration rates, typical master-to-device ratios, and expected ASP erosion, allowing us to close gaps left by secondary data and align our assumptions with real buying behavior.

Desk Research

We began by mapping the installed base of smart sensors using open datasets from the International Federation of Robotics, UN COMTRADE HS codes for electronic control units, OECD industrial production indices, and sector reports from trade bodies such as VDMA and SEMI. These helped us benchmark how fast factories are adopting point-to-point industrial communication.

Supplementary insight came from company 10-Ks, IPO filings, and engineering journals that publish average selling prices for IO-Link masters and wireless gateways. To enrich financial intelligence, our analysts accessed D&B Hoovers for supplier revenues and Dow Jones Factiva for tender announcements in automotive and food-processing plants. The sources cited here are illustrative; many other public and paid references supported data collection and sense-checking.

Market-Sizing & Forecasting

A top-down and bottom-up blended model was built. Global PLC shipments and sensor export volumes were first reconstructed into an IO-Link-addressable pool, then corroborated with sampled supplier roll-ups and channel checks. Key variables like installed IO-Link nodes, average master ASP, discrete-manufacturing CapEx, industrial robot shipments, and IIoT adoption indices drive the multivariate regression that powers our five-year forecast. Scenario analysis adjusts for currency swings and semiconductor lead-time shocks, while gaps in bottom-up inputs are bridged using regional proxy ratios validated through interviews.

Data Validation & Update Cycle

Outputs pass a two-level analyst review that flags anomalies against external production, trade, and price benchmarks. Models refresh annually; interim updates are triggered when tariff changes, protocol revisions, or megadeals shift the demand curve, ensuring clients always receive the latest vetted view.

How Mordor Intelligence's IO-Link System Market Size Compares to Other Published Estimates

Published estimates often diverge because firms choose dissimilar component scopes, assume varied ASP trajectories, or refresh data at different cadences. We acknowledge these realities upfront.

Differences widen when some studies track only wired nodes, treat wireless as an add-on, or extrapolate from a single region. Mordor Intelligence applies a harmonized scope, quarterly currency re-baselining, and dual-scenario forecasting, which together yield a balanced, decision-ready baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.17 B (2025) | Mordor Intelligence | - |

| USD 15.7 B (2024) | Regional Consultancy A | Device-only scope; Europe-centric sample; biennial updates |

| USD 13.6 B (2023) | Global Consultancy B | Historic import data reliance; single-scenario forecast; static FX rates |

| USD 13.51 B (2023) | Industry Association C | Wired nodes counted exclusively; manufacturing verticals only |

In sum, the consistent scope, live variable tracking, and yearly refresh cadence adopted by Mordor Intelligence deliver a transparent baseline that users can retrace and replicate without specialized tooling, instilling higher confidence in strategic planning.

Key Questions Answered in the Report

What is driving the rapid growth of the IO-Link system market?

Edge computing integration, wireless gateways, and strong government programs in Europe and Asia-Pacific are accelerating deployment, leading to a 22.54% CAGR forecast to 2031.

Which component contributes the most revenue today?

Smart IO-Link devices, including multi-parameter sensors, represented 63.45% of 2025 revenue, reflecting their foundational role in every installation.

How significant is wireless technology to future adoption?

Wireless gateways are projected at a 31.08% CAGR because they remove cabling limits on rotating or mobile equipment and enable easier retrofits in legacy plants.

Why is the pharmaceutical sector adopting IO-Link so quickly?

Continuous manufacturing requires precise, real-time data with full traceability, and IO-Link paired with OPC UA cuts production costs by 15% while meeting regulatory needs.

What challenges could slow market penetration?

Cyber-security certification gaps in FDA-regulated facilities and price competition from low-cost proprietary buses can raise costs or delay decisions, trimming forecast growth by up to 6.3%.

Page last updated on: