Intraoperative Neuromonitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

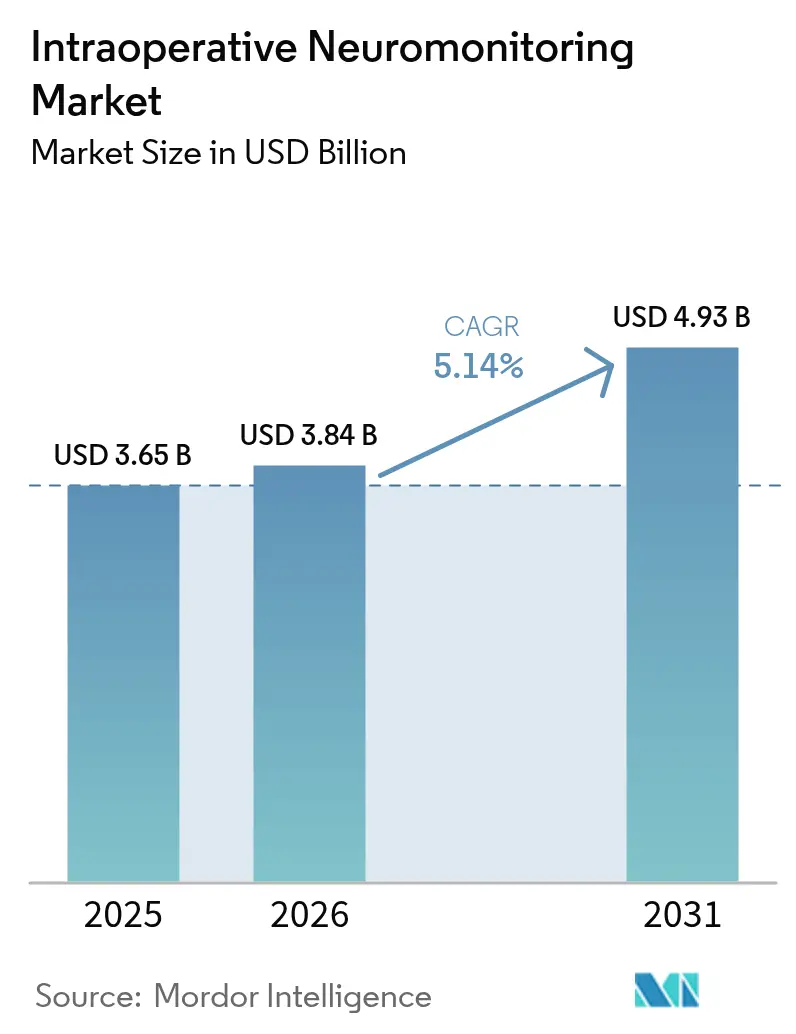

| Market Size (2026) | USD 3.84 Billion |

| Market Size (2031) | USD 4.93 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

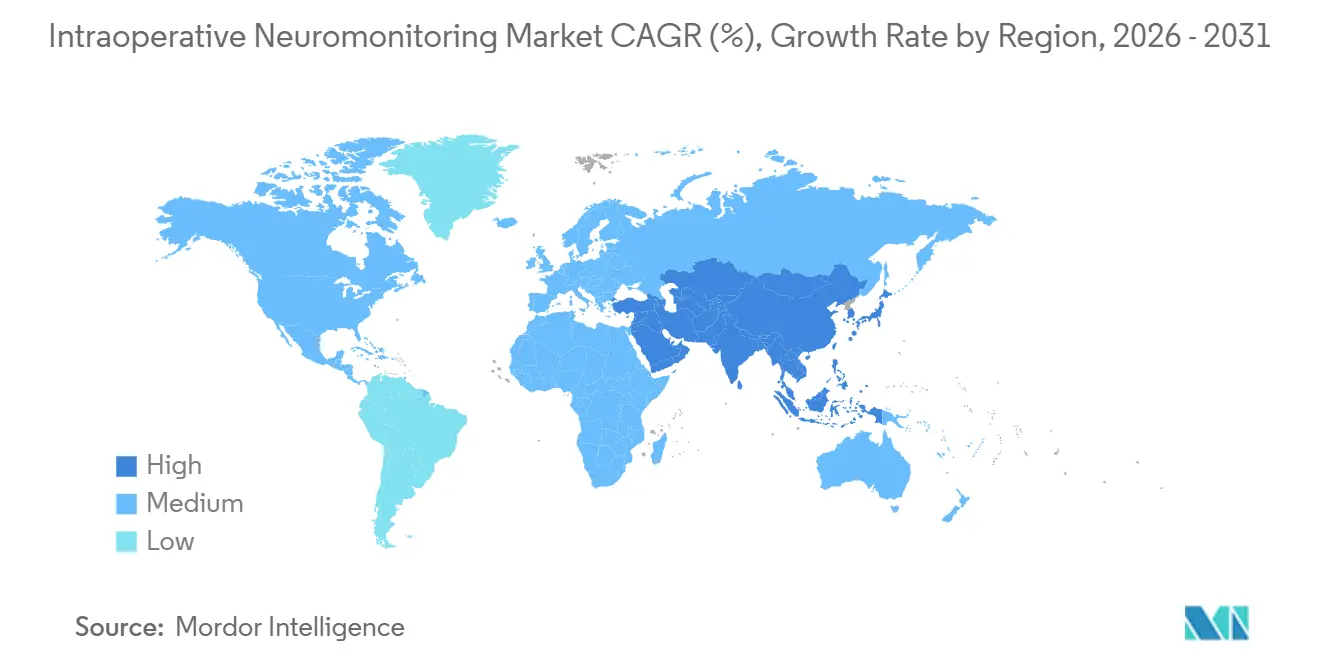

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intraoperative Neuromonitoring Market Analysis by Mordor Intelligence

The Intraoperative Neuromonitoring Market size is expected to grow from USD 3.65 billion in 2025 to USD 3.84 billion in 2026 and is forecast to reach USD 4.93 billion by 2031 at 5.14% CAGR over 2026-2031.

Rising surgical volumes, tighter risk-mitigation mandates from hospitals and insurers, and the rapid build-out of third-party monitoring networks are repositioning real-time neural surveillance as a routine component of operating-room workflows rather than an elective add-on. Portable, cloud-connected systems are enabling ambulatory surgical centers to handle complex spine and ENT cases while meeting same-day discharge targets. Consumable demand is climbing as single-use electrodes replace reusable probes in infection-control-conscious theaters, and outsourcing is democratizing access for community hospitals that lack certified neurophysiologists. Competitive intensity is moderate: capital-equipment leaders leverage installed bases, yet service specialists are winning multi-year contracts by bundling staffing, liability insurance, and remote oversight.

Key Report Takeaways

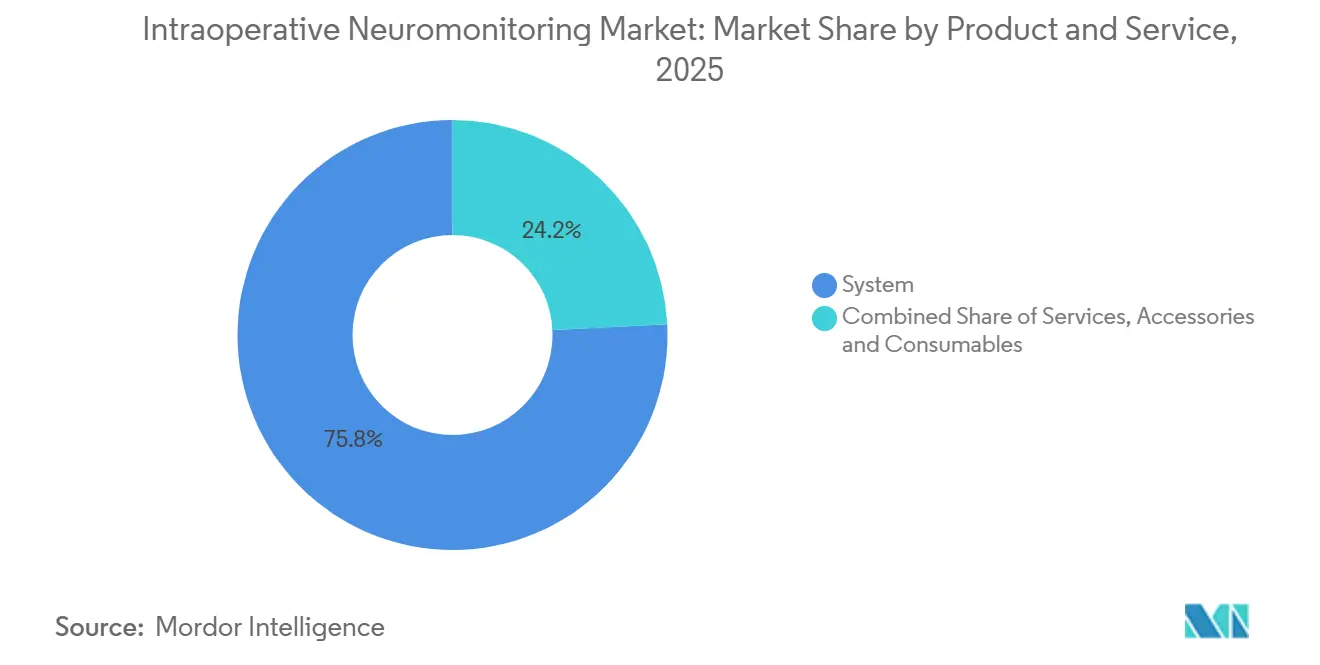

- By product & services, the system held 75.8% of the intraoperative neuromonitoring market share in 2025, while accessories & consumables are projected to rise at a 6.08% CAGR to 2031.

- By source type, insourced monitoring accounted for 59.4% of the intraoperative neuromonitoring market size in 2025, yet outsourced providers are set to expand at a 7.25% CAGR through 2031.

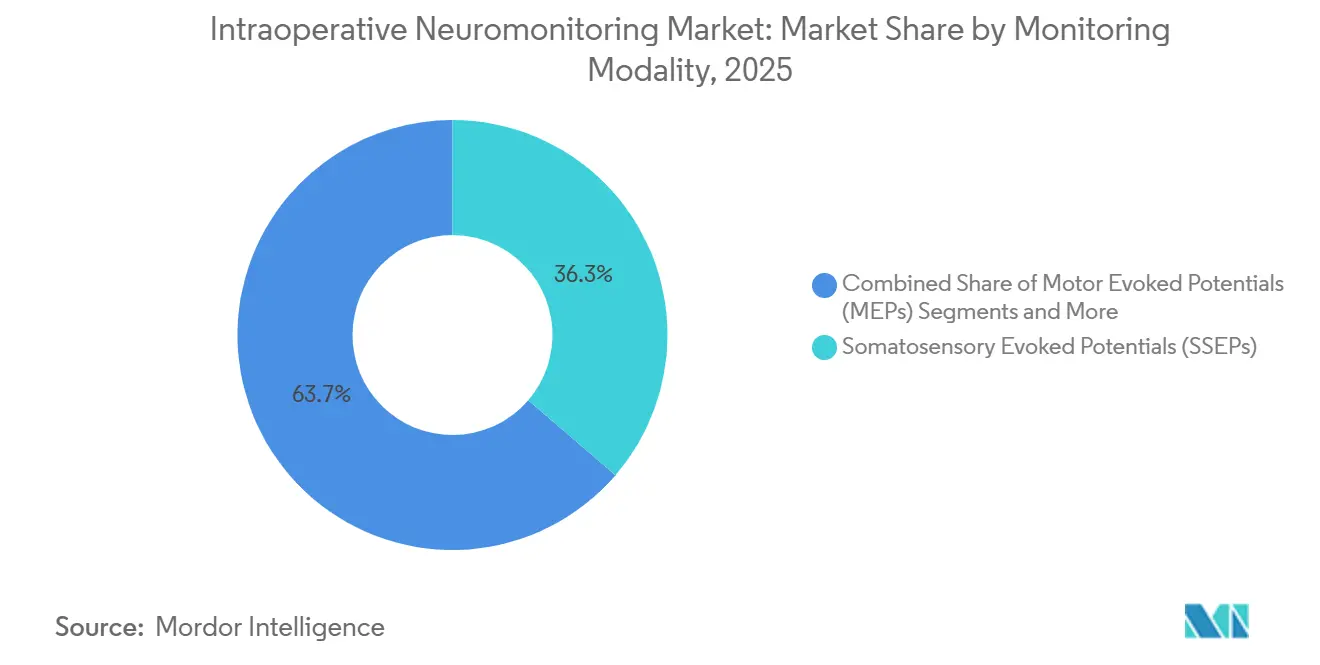

- By monitoring modality, somatosensory evoked potentials led with 36.3% revenue share in 2025; auditory and motor evoked potentials (MEPs) are poised for the fastest 6.43% CAGR to 2031.

- By surgical application, neurosurgery captured 37.22% of the intraoperative neuromonitoring market share in 2025, while spinal surgery is on course for a 6.57% CAGR to 2031.

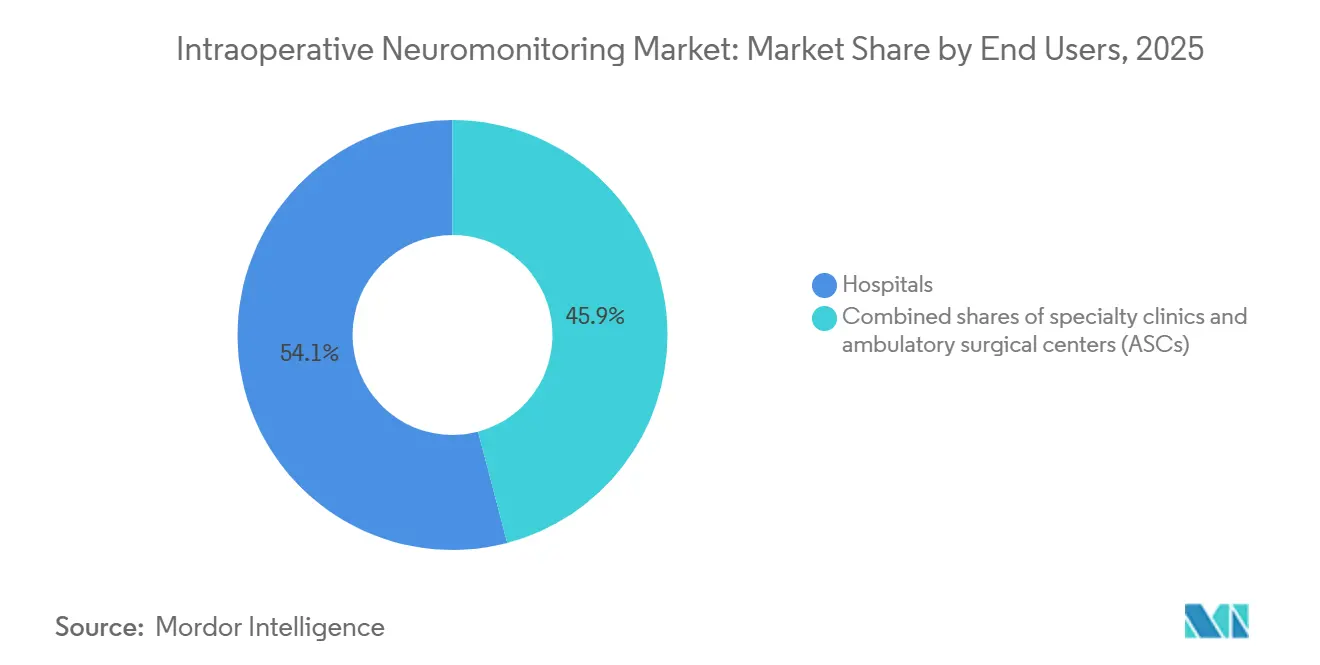

- By end-user, hospitals contributed 75.81% of the intraoperative neuromonitoring market size in 2025, even as ambulatory surgical centers advance at a 7.67% CAGR through 2031.

- By geography, North America led with 43.4% contribution in 2025, and Asia-Pacific is forecast to grow the quickest at an 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intraoperative Neuromonitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising chronic-disease burden & surgical volumes | +0.9% | Global, North America & Europe | Medium term (2-4 years) |

| Mandatory risk-mitigation policies by hospitals & insurers | +0.7% | North America & Western Europe | Short term (≤ 2 years) |

| Expansion of third-party IONM service networks | +0.6% | North America core; spill-over to APAC & MEA | Medium term (2-4 years) |

| Outpatient/ASC shift driving portable & remote IONM | +0.5% | North America & select APAC markets | Medium term (2-4 years) |

| Convergence with robotic, AR & navigation platforms | +0.8% | Global, led by North America & Europe | Long term (≥ 4 years) |

| AI-driven real-time quantitative neuro-mapping | +0.7% | North America, Europe & advanced APAC centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic-Disease Burden & Surgical Volumes

Complex spine, vascular, and neurosurgical case volumes are climbing by roughly 4-5% each year as populations age and diabetes prevalence increases, exposing more patients to iatrogenic nerve-injury risk [1]International Diabetes Federation, “IDF Diabetes Atlas 2021,” idf.org. Surgeons now view multimodal monitoring as a core safety measure rather than an optional safeguard. The intraoperative neuromonitoring market consequently benefits whenever payers broaden coverage, as seen in CMS’s 2024 decision to reimburse monitoring during select cardiovascular procedures. Hospital credentialing committees have responded by embedding monitoring into perioperative checklists, effectively transforming discretionary spend into a fixed operating cost. The pattern holds across North America and Western Europe, where malpractice-premium discounts reward documented monitoring use. As procedure counts rise, consumable turnover accelerates, compounding revenue growth for electrode manufacturers.

Mandatory Risk-Mitigation Policies by Hospitals & Insurers

Liability carriers increasingly tie malpractice premiums to documented use of neuromonitoring in high-risk specialties. A 2025 American Association of Neurological Surgeons survey showed that 62% of neurosurgeons receive lower premiums when hospitals record routine multimodal monitoring [2]American Association of Neurological Surgeons, “Professional Liability Survey 2025,” aans.org. Joint Commission National Patient Safety Goals issued in 2024 encourage real-time neural surveillance for surgeries with nerve-injury rates above 1%, reinforcing institutional compliance requirements. These intertwined financial and accreditation pressures speed technology adoption more than clinical evidence alone. Facilities unable to meet internal monitoring targets often outsource, fueling service-provider growth.

Expansion of Third-Party IONM Service Networks

Community hospitals and ambulatory surgical centers lacking on-staff neurophysiologists rely on vendors that bundle equipment, technologists, and remote oversight. Assure Holdings reported 18% revenue growth in fiscal 2025 on the back of exclusive multi-year hospital contracts. Service providers scale efficiently because one board-certified specialist can supervise several cases simultaneously via secure cloud platforms. The model converts a large capital outlay into a manageable case-based fee, expanding access to the intraoperative neuromonitoring market in price-sensitive regions. Continued network build-out in North America, plus early entry into Asia-Pacific, is expected to lift global CAGR.

Outpatient/ASC Shift Driving Portable & Remote IONM

Between 2022 and 2025, the majority of elective lumbar decompressions migrated from hospitals to ambulatory settings, according to the Ambulatory Surgery Center Association. Portable, tablet-based systems such as Cadwell’s CASCADE enable fast turnover and same-day discharge, aligning with payer incentives for lower-cost sites of service. Remote oversight further trims staffing burdens, allowing technologists to cover multiple rooms. These dynamics increase procedure counts addressable by the intraoperative neuromonitoring market while spreading technology into suburban and rural catchment areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & service cost of IONM systems | -0.6% | Global, acute in emerging APAC & MEA markets | Short term (≤ 2 years) |

| Shortage of certified neurophysiologists | -0.5% | North America & Europe | Medium term (2-4 years) |

| Fragmented reimbursement in emerging economies | -0.4% | APAC, MEA & South America | Long term (≥ 4 years) |

| Value-for-money scrutiny limiting routine-use guidelines | -0.3% | Europe & select North American payers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Service Cost of IONM Systems

Comprehensive suites list between USD 80,000 and USD 150,000, numbers that strain community-hospital budgets, while per-case outsourced fees can exceed USD 1,500 [3]Cadwell Industries, “Product Catalog 2025,” cadwell.com. In India, only 22% of tertiary centers had access to multimodal monitoring in 2024. Consumable costs further inhibit uptake, with single-use electrode sets priced at USD 15–25. Although leasing and subscription schemes defer cash outlays, they require predictable surgical volumes that many facilities cannot guarantee, subtracting 0.6 percentage points from forecast CAGR.

Shortage of Certified Neurophysiologists

ABRET certified fewer than 400 new intraoperative neurophysiologists in 2025, far short of U.S. hospital demand. The majority of practitioners cluster near academic centers. Scarcity inflates salaries and signing bonuses, pushing some hospitals toward outsourcing despite internal-staffing preferences. State licensing boards cap the number of simultaneous cases a remote specialist may supervise, limiting scalability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Services: Consumables Gain as Infection-Control Tightens

Systems generated 75.8% of 2025 revenue, underscoring the capital-intensive nature of integrated multimodal consoles that underpin the intraoperative neuromonitoring market size for hospital buyers. Consumables, however, are rising at a 6.08% CAGR through 2031 as single-use needle electrodes become standard under 2024 CDC guidelines advocating disposables to prevent prion transmission.

Cadwell’s USD 18 electrode set undercut incumbent prices by 25%, catalyzing uptake among cost-sensitive ASCs. Vendors now bundle replenishment kits, software updates, and remote support into subscription packages, shifting revenue toward predictable recurring flows and locking customers into proprietary consumable ecosystems.

Wireless hubs and tablet-based interfaces shrink footprints in crowded theaters. Inomed’s Bluetooth electrode arrays eliminate cable clutter, a user-centric feature that appeals to multi-modality cases. Medtronic’s subscription model pairs its base station with monthly shipments of sterilized electrodes and cloud analytics, embedding consumables in operating budgets. As disposable volumes climb, the intraoperative neuromonitoring market share of consumables is set to widen, particularly in ASC networks that favor low-inventory, infection-controlled workflows.

By Source Type: Outsourcing Unlocks Access for Mid-Tier Facilities

Insourced programs held 59.4% of 2025 revenue, concentrated in academic centers that leverage internal neurophysiologist teams to train residents and conduct research. Outsourced monitoring is expanding at a 7.25% CAGR, bridging gaps for community hospitals performing fewer than 200 monitored cases annually. A Journal of Healthcare Management study found outsourced programs cut per-case costs by 18% versus insourced alternatives at low-volume facilities. Assure Holdings’ acquisition spree in 2025 extended coverage to 400 hospitals across 14 states, exemplifying consolidation trends that raise the intraoperative neuromonitoring market size accessible to mid-tier institutions.

Remote-supervision technology allows a single board-certified neurophysiologist to oversee four concurrent surgeries, relieving workforce constraints. Nevertheless, large spine centers still justify dedicated in-house teams where annual volumes exceed 600 procedures, preserving an insourced stronghold. Moving forward, payer pressure to trim capital budgets and the maturation of vendor networks will keep outsourcing growth ahead of insourcing, gradually shifting intraoperative neuromonitoring market share toward variable-cost service models.

By Monitoring Modality: Auditory & Visual EPs Rise with ENT Volume

Somatosensory evoked potentials delivered 36.3% of modality revenue in 2025, a reflection of their entrenched role in spinal-cord surveillance during deformity correction and fusion. Motor EPs and EMG complement SSEPs by tracking corticospinal and peripheral pathways in real time. Auditory and visual EPs are accelerating at a 6.43% CAGR as thyroid, parathyroid, and skull-base surgeries adopt continuous cranial-nerve monitoring to curb postoperative vocal-cord paralysis. Checkpoint Surgical’s C2 Xplore system anchors this growth, with more than 300 ENT practices adopting the platform since 2024.

Electroencephalography finds niche application in carotid endarterectomy and aortic arch repair, guided by the American Heart Association 2025 recommendations. Multimodal consoles that synchronize up to five signal streams improve workflow efficiency, positioning integrated platforms to dominate future intraoperative neuromonitoring market share. As ENT volumes climb and guidelines expand, auditory and visual EP penetration will continue to outpace legacy modalities.

By Surgical Application: Spinal Procedures Outpace Neurosurgery

Neurosurgery captured 37.22% of revenue in 2025 owing to its dependence on cortical mapping and deep-brain stimulation. Yet spinal procedures are set to grow faster, at 6.57% CAGR, driven by the surge in minimally invasive fusions and decompressions for an aging population. The intraoperative neuromonitoring market size for spine applications benefits from payer-approved site-of-service migration to ASCs, widening the addressable base. ENT and thyroid surgery is expanding quickly as surgeons seek to mitigate litigation tied to recurrent laryngeal nerve injury, while vascular indications gain momentum under new AHA guidance.

Although orthopedic joint replacements represent a smaller slice, surgeons increasingly deploy nerve-proximity alerts to prevent postoperative foot-drop and quadriceps weakness. Vascular centers use EEG and SSEP monitoring to detect cerebral ischemia during complex repairs. Collectively these trends diversify demand, anchoring growth even as neurosurgical volumes mature.

By End-User: ASCs Leverage Portable Platforms for Growth

Ambulatory surgical centers (ASCs) are growing at 7.67% a year through 2031 as insurers steer many elective spine, orthopedic, and ENT cases to lower-cost outpatient settings. Between 2023 and 2025, 68% of single-level lumbar fusions and 54% of cervical decompressions moved out of hospitals, a shift made possible by better anesthesia, refined pain protocols, and lightweight neuromonitoring systems that roll straight into an operating room. ASCs prefer compact, wireless units such as Cadwell’s CASCADE platform, which pairs a tablet interface with Bluetooth electrodes and has gone into more than 150 centers since its 2024 debut. Outsourced service firms round out the picture by sending certified technologists and remote neurophysiologists on a case-by-case basis, letting ASCs avoid hiring permanent specialists.

Hospitals still held 54.1% of end-user revenue in 2025 because they handle high-acuity neurosurgery, multilevel spine work, and cardiovascular procedures that need full multimodal monitoring and on-site experts. Academic medical centers and large tertiary hospitals justify salaried technologists through heavy case volumes and resident-training needs. Focused spine centers and pain clinics sit between hospitals and ASCs. They run streamlined schedules yet turn to outside providers when a revision fusion or intrathecal pump implant demands deeper monitoring. Hospitals keep the edge for operations that require intensive care support, but the lines are blurring. Regulators now clear outpatient sites for increasingly complex work, and vendors answer with modular systems that scale from single-modality ENT monitoring to full multimodal spine surveillance in one unit.

Geography Analysis

North America generated 43.4% of 2025 revenue, supported by Medicare reimbursement, Joint Commission standards, and the broad reach of outsourced service networks. The United States dominates spending, while Canada limits adoption to academic centers under single-payer budget caps. Mexico remains nascent, although private hospital chains are investing to attract medical tourists.

Europe follows, with Germany, the United Kingdom, and France leading penetration, thanks to national reimbursement for defined spinal and intracranial indications. Germany’s statutory insurers cover neuromonitoring in deformity correction, ensuring consistent usage. The United Kingdom’s 2024 NICE guidance endorsed monitoring for complex spine surgery, likely to lift utilization in NHS trusts under capital-tight constraints. Southern Europe lags as hospitals prioritize imaging and robotic systems ahead of neuromonitoring.

Asia-Pacific is the fastest-growing region at 7.11% CAGR. China’s Healthy China 2030 initiative funds tertiary hospital upgrades that require neuromonitoring capability. India’s private chains, such as Apollo Hospitals, install multimodal suites to attract domestic and international patients. Japan’s aging demographic drives spine-procedure demand, benefiting domestic vendor Nihon Kohden. The Middle East concentrates adoption in Gulf Cooperation Council countries building flagship medical cities, whereas Africa and South America progress more slowly due to fragmented reimbursement and capital shortfalls.

Regulatory Landscape

Intraoperative neuromonitoring (IONM) equipment marketed in the United States typically falls under FDA medical device oversight for neurological diagnostic devices, where many systems and related stimulators/monitors are handled as Class II devices and commonly follow the 510(k) pathway. In May 2026, FDA opened a Federal Register request for comments on potentially expanding exemptions from premarket notification for certain Class II devices, signaling an active review cycle that can affect administrative burden and documentation strategies for established product categories.

In Europe, manufacturers selling IONM systems and accessories operate under the Medical Device Regulation (EU) 2017/745 (MDR), which raises requirements for quality management systems, clinical evaluation, and technical documentation. MDCG guidance (MDCG 2022-4) formalized the transition of notified body surveillance responsibilities for legacy devices by September 2024, tightening ongoing conformity-assessment expectations for companies maintaining installed bases while updating portfolios for MDR compliance. Parallel updates in international standards, including ongoing work to revise ISO 14708-3 for active implantable neurostimulators, also influence cross-border technical files when IONM ecosystems interface with neuromodulation and related neurotechnology.

Competitive Landscape

Top players Medtronic, Natus Medical, Nihon Kohden, Cadwell Industries, and Globus Medical command the majority of the intraoperative neuromonitoring market, leaving room for regional manufacturers and service specialists. Capital-equipment incumbents leverage cross-selling opportunities into electrophysiology and navigation portfolios. Service pure-plays such as Assure Holdings and SpecialtyCare erode hardware moats by bundling technologists, equipment, and liability coverage under multi-year contracts. Globus Medical’s 2023 purchase of NuVasive demonstrates vertical integration, pairing implants with in-house monitoring to deepen surgeon loyalty.

Niche innovators target underserved segments: Checkpoint Surgical focuses on ENT and thyroid applications, while Proprio’s AI-guided 3-D imaging integrates with monitoring for spine accuracy. AI software vendors partner with hardware manufacturers to embed analytics that streamline interpretation, creating recurring revenue streams from algorithm licenses. Geographic expansion through distributor agreements, such as NCC Medical’s 2025 South Korea rollout, further fragments competitive dynamics. Given that the top five hold half the market, concentration remains moderate, allowing new entrants to carve share via portability, AI features, or service-centric business models

Intraoperative Neuromonitoring Industry Leaders

Nihon Kohden Corporation

Medtronic plc

Natus Medical Inc.

Cadwell Industries

Globus Medical

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace centers on operationalizing remote and software-led neuromonitoring across mixed sites of care, including ambulatory surgical centers, while staying aligned with reimbursement and compliance constraints. In the United States, CMS Local Coverage Determinations for neuromonitoring physician services (for example, LCDs L34623 and L35003) emphasize billing for time spent exclusively monitoring a single patient, which increases demand for workflow tooling that clearly documents attention, timestamps, and case ownership across on-site and remote teams. On the supplier side, the FDA Quality Management System Regulation (QMSR) update that became effective in February 2026 raises the bar for harmonized quality processes, creating an opening for vendors that can deliver validated software updates, cybersecurity-controlled connectivity, and traceable consumable programs within a compliant lifecycle framework.

Technology opportunity also concentrates on reducing false alarms and standardizing interpretation, two issues that affect surgeon trust and the economics of routine use. Clinical literature in 2026 highlighted machine learning approaches that combine MEP and SSEP data for outcome prediction and earlier alerting during spine procedures, and practice-level discussion of transabdominal MEP strategies has focused on cutting false alarms in lumbar surgery. These proof points support product roadmaps that bundle quantitative signal analytics into consoles and service platforms, and they also strengthen the business case for outsourcing networks that can spread scarce expert oversight across facilities while keeping protocol consistency.

Recent Industry Developments

- January 2026: Natus introduced the latest version of Natus Elite EMG software with Augmented Visual Electromyograph (AVEMG) functionality to quantify signals in real time. The release supports software-driven differentiation in IONM workflows where interpretation speed and consistency influence adoption across hospitals and ambulatory settings. It also supports service providers and multi-site customers seeking standardized analytics across distributed monitoring teams.

- December 2025: Natus received FDA 510(k) clearance for an electrographic status epilepticus diagnostic indication within its BrainWatch point-of-care EEG solution. While centered on EEG, the clearance reinforces Natus platform credibility in regulated neurodiagnostic software and device claims that can translate into adjacent neuromonitoring procurement decisions. Hospitals evaluating integrated neurophysiology ecosystems also benefit from clearer regulatory positioning for expanded indications.

- November 2024: Nihon Kohden acquired a 71.4% stake in NeuroAdvanced Corp., the parent of Ad-Tech Medical Instrument Corporation. The deal deepens vertical integration in neurodiagnostics by pairing electrodes and related accessories with established monitoring platforms, supporting bundled offerings across EEG and intraoperative monitoring use cases. It also increases competitive pressure on standalone consumables suppliers as large OEMs broaden end-to-end portfolios.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the intraoperative neuromonitoring market includes the devices, consumables, and related monitoring services used during surgical procedures to track nerve and brain pathway function in real time, with revenues counted at the point of sale or service delivery.

Scope exclusions: standalone diagnostic EEG/EMG tests performed outside the operating room and general anesthesia monitoring that does not include neuromonitoring are not counted.

Segmentation Overview

- By Product & Services

- Systems

- Accessories & Consumables

- Services

- By Source Type

- Insourced Monitoring

- Outsourced Monitoring

- By Monitoring Modality

- Somatosensory Evoked Potentials (SSEPs)

- Motor Evoked Potentials (MEPs)

- Electroencephalography (EEG)

- Electromyography (EMG)

- Auditory & Visual EPs (BAEPs, VEPs)

- By Surgical Application

- Spinal Surgery

- Neurosurgery

- Orthopedic Surgery

- ENT & Thyroid Surgery

- Vascular & Cardiovascular Surgery

- Other Complex Procedures

- By End-User

- Hospitals

- Speciality Clinics

- Ambulatory Surgical Centers (ASCs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the clinical and procedure context, since intraoperative neuromonitoring (IONM) demand is tied to how many complex surgeries are performed and where those cases are concentrated. We review public health statistics and procedure references from sources such as the World Health Organization, the US Centers for Disease Control and Prevention, the US National Institutes of Health (including clinical literature), and national health ministries that publish hospital activity indicators.

Then we cross-check supply-side and pricing logic using sources such as US FDA device databases, patent databases, peer-reviewed journals covering neurophysiology and spine surgery, and trade association publications that discuss standards and practice trends. We also use company filings, investor decks, and reputable press to confirm product mix and regional exposure, supported by paid subscriptions for company financials, news and financials, and patent lookups where it speeds up validation. These desk sources are illustrative and not exhaustive, and other public references were used to collect, verify, and clarify the data.

Primary Interviews and Surveys

Fieldwork is used to sanity check what desk sources cannot show clearly, such as how monitoring is staffed (insourced versus outsourced), how modalities are bundled in real cases, and what typical pricing looks like by procedure complexity. We spoke with a mix of hospital clinical stakeholders, service providers, device channel participants, and industry experts across major regions to tighten assumptions on utilization, attach rates, and service mix before final sign-off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | APAC: 44% |

| Mid tier: 59% | Functional/Unit leaders: 43% | EMEA: 37% |

| Smaller Players: 14% | Managers: 45% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built with a top-down model where procedure volumes and the eligible surgical pool are reconstructed by region, and then filtered through IONM adoption rates and modality usage patterns. Once the demand pool is set, the value is formed by applying typical pricing for monitoring services and equipment use, followed by adjustments for insourced versus outsourced delivery and country-level reimbursement realities.

To keep the model realistic, selective bottom-up approximations are also used, such as supplier revenue direction checks, sampled average selling price assumptions for systems and consumables, and channel discussions on utilization per case. Inputs used in the model include spinal and neurosurgery caseload trends, hospital operating room capacity additions, the share of complex cases where monitoring is clinically preferred, outsourcing penetration, and pricing movement for systems, accessories, and services. When a country has thin visibility, gaps are handled with proxying from similar healthcare systems, then corrected with expert feedback.

Forecasts are run using scenario analysis supported by variable-level expectations gathered from interviews, where procedure growth, outsourcing uptake, and pricing pressure are flexed to form a base case and reasonable bounds. The final forecast path is kept consistent with near-term hospital budgets and longer-term technology adoption pace, rather than assuming step changes without evidence.

Data Validation & Update Cycle

Outputs are validated through repeated checks across independent signals, so sudden jumps in adoption, pricing, or procedure volumes are flagged early and reviewed. Totals are compared against regional surgical activity indicators, product and service mix expectations, and known reimbursement and staffing constraints, and then the drivers are reconciled until variances have a clear explanation.

Before sign-off, the model is reviewed in steps by another analyst, and any large deviations from expected ranges trigger re-checks of inputs and follow-up calls with selected respondents. The report is refreshed annually, and interim updates are added when material events change assumptions, such as reimbursement shifts or major care delivery changes. Right before delivery, a final review pass is done so clients receive the most current view supported by the latest data.

Mordor Intelligence's Intraoperative Neuromonitoring Market Size Measured Against Other Published Estimates

Published estimates for intraoperative neuromonitoring can differ even when the topic label looks identical, because the boundary between systems, consumables, and monitoring services is not handled the same way. Differences also come from how procedure demand is translated into billable cases and how currency timing and inflation are treated in the base year.

By tracking procedure-led demand signals and refreshing pricing and service mix inputs with interviews, Mordor Intelligence keeps the 2025 market value tied to systems plus accessories and consumables plus services, instead of leaning mainly on device shipments or a single dominant product bucket.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.65 B (2025) | |

| Global Consultancy A | USD 3.49 B (2024) | Uses a 2024 base year and places heavier weight on systems revenue, so outsourced monitoring services and recurring consumables are not always fully captured in the total. |

| Industry Publisher B | USD 3.93 B (2024) | Starts from a higher 2024 base and assumes faster service expansion, which can inflate the total when procedure growth and insourcing constraints are not aligned to hospital capacity and staffing reality. |

The spread in values mostly comes down to year selection and how services and recurring consumables are counted alongside equipment. When scope is kept consistent and checked against procedure activity, outsourcing penetration, and realistic pricing movement, the resulting market number stays easier to replicate and explain.

Key Questions Answered in the Report

What CAGR is projected for the intraoperative neuromonitoring market between 2026 and 2031?

A CAGR of 5.14% is forecast for the period 2026-2031, lifting the market to USD 4.93 million by 2031.

Which product category is growing fastest within intraoperative neuromonitoring?

Accessories and consumables are advancing at a 6.08% CAGR as hospitals adopt single-use electrodes to meet infection-control guidelines.

Why are ambulatory surgical centers important to neuromonitoring growth?

ASCs are expanding at a 7.67% CAGR because portable, cloud-enabled systems allow same-day spine and ENT procedures that previously required inpatient care.

How is outsourcing influencing neuromonitoring adoption?

Outsourced service networks provide technologists, equipment, and remote oversight on a per-case basis, enabling community hospitals to use neuromonitoring without large capital investments.

Which region is expected to post the highest growth rate?

Asia-Pacific is forecast to grow at 7.11% CAGR, propelled by government-funded hospital expansion in China and India plus private-sector investment in Japan and South Korea.

Page last updated on: