Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

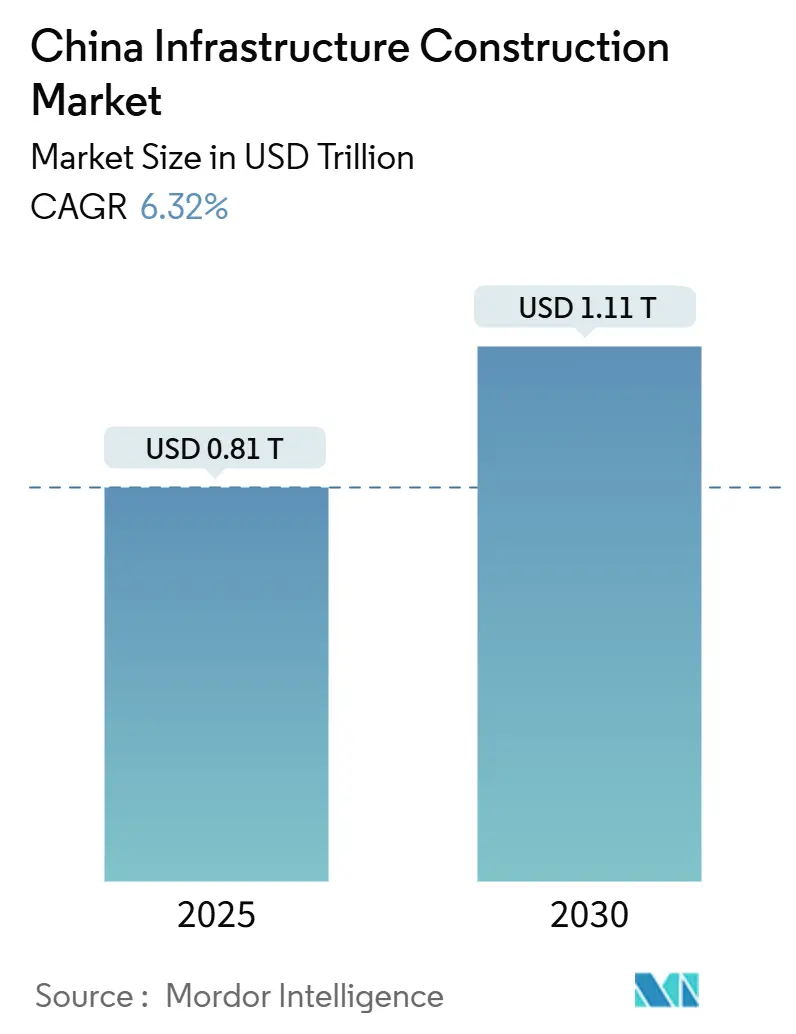

| Market Size (2025) | USD 0.81 Trillion |

| Market Size (2030) | USD 1.11 Trillion |

| Growth Rate (2025 - 2030) | 6.32% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Infrastructure Construction Market Analysis by Mordor Intelligence

The China Infrastructure Construction Market size is estimated at USD 0.81 trillion in 2025, and is expected to reach USD 1.11 trillion by 2030, at a CAGR of 6.32% during the forecast period (2025-2030). This momentum stems from Beijing’s pivot away from property-driven growth toward infrastructure-led modernization, the integration of digital capabilities such as 5G and artificial intelligence into hard assets, and aggressive regional connectivity goals. Transportation projects, especially high-speed rail, anchor demand, while fiscal support through special-purpose bonds and ultra-long treasury bonds keeps project pipelines active. Public-private partnerships boost capital efficiency, and renewable-energy micro-grids broaden the project map into western provinces. Supply-chain diversification efforts, advances in Building Information Modeling, and stringent carbon-neutrality targets are reshaping material choices and construction methods[1]National Development and Reform Commission, “14th Five-Year Plan—New Infrastructure Guidelines,” gov.cn. .

Key Report Takeaways

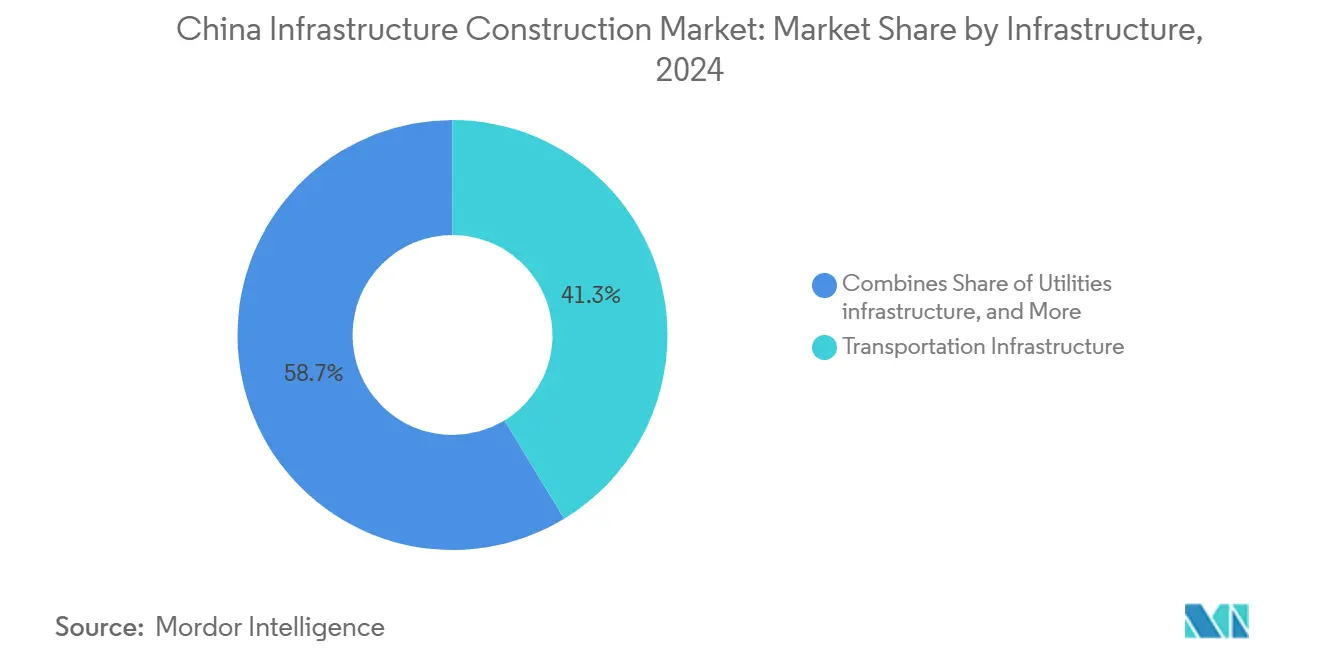

- By infrastructure, Transportation infrastructure led with 41.3% of China's infrastructure construction market share in 2024.

- By construction type, Renovation projects are advancing at a 7.70% CAGR through 2030, the fastest among construction types.

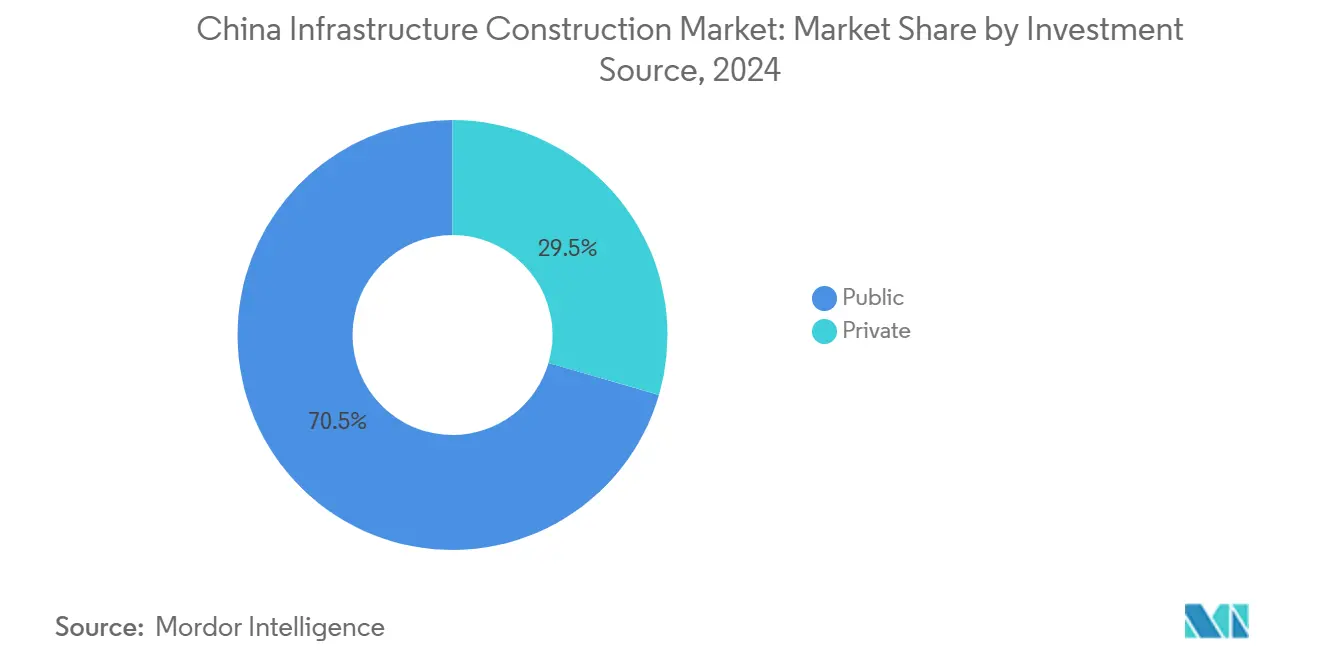

- By investment source, Private investment is accelerating at an 8.50% CAGR, outpacing the sector average while holding 29.46% of current spending.

- By geography, Shanghai accounted for 50.65% of the 2024 spend, and the rest-of-China cluster is growing at a 7.56% CAGR to 2030.

China Infrastructure Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 14th Five-Year Plan focus on new infrastructure | +1.8% | Beijing-Tianjin-Hebei, Yangtze River Delta, Greater Bay Area | Long term (≥ 4 years) |

| Rapid urbanization and smart-city rollout | +1.5% | Shanghai, Shenzhen, Hangzhou, Chongqing | Medium term (2-4 years) |

| Expansion of high-speed rail corridors | +1.2% | National corridors, Yangtze River Belt, Pearl River Delta | Long term (≥ 4 years) |

| Rural micro-grids for renewable power | +0.9% | Xinjiang, Inner Mongolia, Gansu, central provinces | Medium term (2-4 years) |

| Edge-computing and data-center build-outs | +0.7% | Eastern data hubs, western compute zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government’s 14th Five-Year Plan Focus on New Infrastructure

The 14th Five-Year Plan compels every major project to pair physical works with digital functions such as sensor platforms, 5G, and cloud connectivity, translating a USD 972 billion bond program in 2024 into immediate construction demand. Net-zero design rules are now mandatory, pushing contractors toward low-carbon materials and smart-site management. Central ministries coordinate approvals, and local governments must report digital-readiness indicators before funding is released. This framework raises technical entry barriers yet rewards firms with integrated engineering and software capabilities. Long-run visibility on funding secures order books for state-owned and private builders alike, supporting market growth.

Rapid Urbanization Fueling Smart-City Initiatives

China’s urbanization rate is nearing 70%, and more than 400 municipalities are installing smart traffic, energy, and public-safety grids. The People-Centered New Urbanization plan links migrant-housing targets with digital-infrastructure quotas, ensuring construction work in both social and technology segments. Shenzhen’s 2024 Smart City Expo award highlighted a 40% logistics efficiency gain after widespread sensor deployment. National standards issued by the Ministry of Housing promote interoperable systems, lowering maintenance costs. Consequently, demand grows for contractors that can deliver fiber, power, and civic-space upgrades in a single package.

Expansion of High-Speed Rail Network and Inter-City Connectivity

China aims to extend its high-speed network to 60,000 kilometers by 2030, requiring about 3,800 kilometers of new track each year. Projects such as the USD 74 billion Shanghai-Chongqing-Chengdu line link multiple megacities, creating cascading station, road, and logistics investments. Rail fixed-asset outlays exceeded USD 111.3 billion in 2024 and will remain above USD 80 billion through 2025 according to China Railway plans. These multi-phase builds secure long-duration contracts for civil works, signaling systems, and transit-oriented developments. Suppliers of high-performance concrete, track slabs, and tunnel-boring equipment benefit from sustained volume orders.

Decentralized Renewable Micro-Grids Enabling Rural Upgrades

An 8 GW solar installation in Ordos, Inner Mongolia, illustrates the size of rural micro-grid opportunities with its USD 11 billion capital spend and extensive land preparation work. Ultra-high-voltage lines such as the 2,370-kilometer Gansu-Zhejiang DC project, costed at USD 4.82 billion, require specialized tower foundations and long-haul logistics. Rural grids spur ancillary roads, storage depots, and maintenance facilities, inviting local contractors and labor. Grid resilience goals also trigger substation retrofits and smart-meter rollouts, expanding renovation workloads in nearby towns. These projects distribute economic benefits beyond coastal provinces while supporting national carbon-reduction commitments.

Restraints Impact Analysis*

| Restraints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Local-government debt sustainability | -1.4% | Nationwide, acute in central and western tier-2/3 cities | Medium term (2-4 years) |

| Supply-chain disruptions and material-cost volatility | -0.8% | Nationwide, with eastern manufacturing hubs driving costs | Short term (≤ 2 years) |

| Stricter ESG scrutiny on coal projects | -0.6% | Shanxi, Inner Mongolia, Xinjiang; heavy-industry belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Local Government Debt-Sustainability Concerns

Local Government Financing Vehicles must service USD 651 billion of bonds in 2024, squeezing cash for new contracts. Debt-swap measures lower coupon costs but cover only part of total liabilities, compelling Beijing to freeze some projects in over-leveraged provinces. Tsinghua University scholars propose a USD 4.2 trillion sovereign-bond program, yet implementation remains unclear and delays procurement cycles. Construction firms face elongated payment terms and higher contingent‐liquidity buffers. Credit-rating downgrades for several LGFVs further tighten bank-financing windows.

Supply-Chain Disruptions and Material-Cost Volatility

Steel prices fell more than 20% in 2024 amid oversupply, prompting output cuts and threatening timely deliveries; copper shortages loom because current global mine plans meet only 80% of 2030 demand, while China accounts for three-quarters of new smelter capacity. Builders are adopting sliding-scale pricing clauses and diversifying supplier bases to preserve margins. Equipment OEMs now source critical components such as power semiconductors from multiple provinces to mitigate lockdown risks. Project schedules incorporate greater buffer days to absorb logistics delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure: Transportation Sustains Headline Growth

Transportation infrastructure held 41.3% of China infrastructure construction market share in 2024 as rail and urban-transit builds dominated tenders. The sector enjoys predictable funding through the Eight Vertical and Eight Horizontal corridor plan, which mobilized USD 111.3 billion of rail spending in 2024 alone. Projects such as the 47,000-kilometer high-speed network drive ancillary depot, signaling, and station developments, enlarging order books for civil and systems integrators. For contractors, standardized track-bed designs shorten lead times and cut material waste, improving unit margins. Downstream, city governments package real-estate rights around new hubs to co-finance infrastructure outlays, sustaining long-term commercial viability.

Transportation is also the fastest-growing infrastructure vertical, logging an 8.12% CAGR through 2030 thanks to synchronized provincial investments and cross-border Belt and Road extensions. Mega-projects like the USD 74 billion Shanghai-Chongqing-Chengdu line showcase multi-tunnel engineering, while Chongqing East Station’s 1.22 million-square-meter footprint illustrates the scale of integrated transport complexes. Advanced slab-track designs and predictive-maintenance software further lift lifecycle ROI, attracting private capital under availability-payment PPP models. As transit-oriented developments unlock land value, local authorities redeploy gains into new extensions, perpetuating the upgrade cycle.

By Construction Type: Renovation Accelerates Under Fiscal Discipline

New construction dominated with 77.5% of 2024 outlays, confirming that greenfield megaprojects still anchor the China infrastructure construction market. Subway lines, expressways, and data-center campuses often commissioned in clusters require large-scale earthworks and heavy equipment, favoring state-owned entities with strong credit support. Technology mandates under the new infrastructure banner ensure that every fresh build integrates IoT interfaces, raising demand for digital twin modeling and 3D-printed components. Nationwide rollout of project-management platforms improves oversight and compresses delivery risk premiums.

Renovation, however, is the fastest-growing segment at 7.70% CAGR, driven by a USD 551 billion underground-pipeline renewal program and 60,000 urban-upgrade projects launched in 2024. Cities receive federal grants up to USD 167 million apiece, easing budget constraints on complex retrofits. Renovation contracts feature higher margin potential because technical requirements such as integrating smart meters or reinforcing heritage structures limit bidder pools. Energy-efficient façades, LED relighting, and sensorized HVAC upgrades align with carbon targets, attracting ESG-focused investors. Successful refurbishments, like Guangzhou’s Yongqing Square, demonstrate retail-traffic rebounds and rising lease rates post-completion, reinforcing the commercial logic for asset-life extension[2]Ministry of Finance, “Urban Underground Pipeline Renewal Funding Notice,” mof.gov.cn..

By Investment Source: Private Capital Gains Traction

Public funding retained 70.54% of total spend in 2024, underscoring the state’s anchor role in strategic assets such as high-speed rail and ultra-high-voltage grids. Policy banks and special-purpose bonds offer sub-3% coupons, granting state builders cost advantages. Oversight by the National Development and Reform Commission ensures alignment with climate and security goals. Yet fiscal ceilings cap provincial borrowing, prompting ministries to refine procurement rules that encourage co-financing and risk sharing.

Private investment is expanding at an 8.50% CAGR, reflecting reforms that let up to 50% of special bonds serve as project equity and that broaden PPP eligibility to digital infrastructure. New fair-competition review rules level bidding by prohibiting hidden SOE preferences, and dynamic risk-allocation models tested on western-region highways enhance bankability. International projects further sharpen domestic firms’ structuring skills; Chinese consortia use revenue-share PPPs on Kenya’s Standard Gauge Railway and Zambia’s Lusaka-Ndola road, applying lessons at home. As rating agencies applaud predictable cash-flow frameworks, insurance giants and pension funds allocate more to long-duration infrastructure assets.

Geography Analysis

Shanghai commanded 50.65% of national outlays in 2024, propelled by the East Railway Station mega-hub and a dense pipeline of AI-oriented data-center builds. The city’s Foundation Model Innovation Center has attracted 400 AI firms since 2023, catalyzing specialized facility demand ranging from liquid-cooling plants to high-voltage substations. Within the Greater Shanghai Metropolitan Area, integrated planning aligns transit and utility corridors, letting contractors bundle road, rail, and telecom ducts into single mobilizations. Continual land-value capture near hubs funds station-area public-realm upgrades, keeping the local order book full despite cyclical property slowdowns.

Beyond the financial capital, the Yangtze River Delta injected USD 19.4 billion into rail projects during 2024, marking an eighth consecutive year above USD 11 billion. Coordinated approvals across Jiangsu and Zhejiang compress tender times, and prefabrication yards along the delta enable just-in-time segment delivery. Regional supply-chain strength in steel and electronics reduces procurement risk for complex transit systems. Concurrently, the Beijing-Tianjin-Hebei cluster advances the USD 119.25 billion Xiong’an build-out, drawing 200 SOE branch offices that guarantee a continuous flow of social-infrastructure contracts[3]Jiangsu Provincial People’s Government, “2024 GDP and R&D Expenditure Release,” jiangsu.gov.cn..

Western and northeastern provinces are pacing the growth story, with the rest-of-China group expanding at 7.56% CAGR through 2030. Renewable-energy megaprojects like the Inner Mongolia 8 GW solar farm and the 4,197-kilometer Tarim Basin transmission loop shift heavy-construction crews inland. Ultra-high-voltage corridors spawn service-road, warehouse, and crew-camp builds, sustaining local SMEs. Government incentives that offset higher logistics costs, combined with subsidized land, lure prefabrication plants to these regions, further lowering project life-cycle emissions.

Competitive Landscape

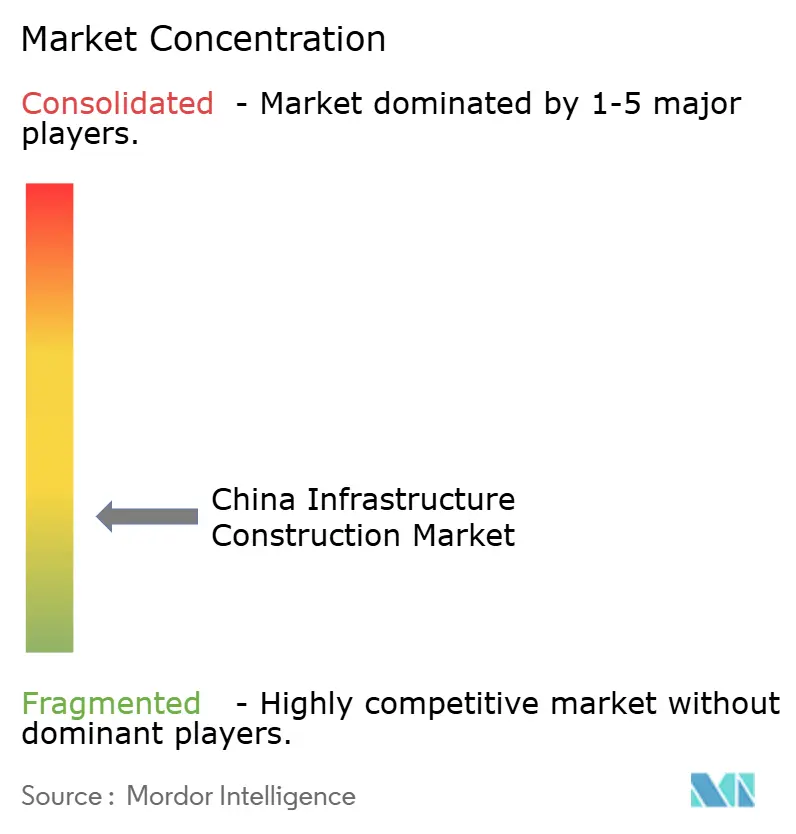

China’s infrastructure arena remains moderately fragmented around state-owned giants, with China State Construction Engineering Corporation generating more than USD 300 billion revenue in 2024, outstripping global peers. China Railway Group and China Railway Construction Corporation add heavyweight capacity in heavy civil works, especially tunneling and bridge engineering. The State-owned Assets Supervision and Administration Commission orchestrates macro-capacity planning, yet subsidiaries compete openly for packages, fostering price discipline and process innovation.

Digitalization is the emerging battleground. Market leaders deploy Building Information Modeling, AI-enabled scheduling, and drone-based site inspections to shave days off critical paths and minimize rework. Pilot projects show labor-productivity gains of 12% and accident reductions of 15% when augmented-reality safety checks are used. Smaller private players carve niches in smart-city systems integration, offering cyber-physical solutions that combine civil, electrical, and software elements. Cross-border wins, such as the USD 2.1 billion King Salman Knowledge Complex in Saudi Arabia, underscore Chinese firms’ competitiveness in international design-build-finance contracts.

Cost pressures, ESG mandates, and new professional-registration rules for supervisors effective May 2024 are likely to accelerate further consolidation, as under-capitalized firms struggle to meet compliance thresholds. Tier-1 contractors with captive financing arms and R&D capabilities can absorb material volatility and pivot to green-tech solutions more readily. Niche specialists will survive by aligning with large SOE joint-ventures that need agile partners for digital subsystems, securing a place in an otherwise managed-competition landscape.

China Infrastructure Construction Industry Leaders

China State Construction Engineering Corp. (CSCEC)

China Railway Group Limited (CREC)

China Railway Construction Corp. (CRCC)

China Communications Construction Co. (CCCC)

China electric power construction co. LTD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: China commenced construction of the world's largest hydropower station in Tibet with CNY 1.2 trillion (USD 167 billion) investment, featuring 300 billion kWh annual output capacity and expected to create 100,000-200,000 jobs while generating CNY 20 billion annual fiscal revenue for the region.

- May 2025: China’s finance ministry is setting aside fresh money to help cities upgrade older neighborhoods. Up to 20 municipalities can claim subsidies of USD 112–168 million each, with the exact amount tied to their regional status. In 2024, more than 60,000 renewal projects got underway nationwide, drawing a combined USD 406 billion in investment.

- April 2025: Xiong'an New Area investments exceeded CNY 860 billion (USD 119.25 billion) by February 2025, with over 200 subsidiaries from state-owned enterprises establishing operations and population growing to 1.36 million residents.

- March 2025: China Civil Engineering Construction Corporation (CCECC) secured a USD 1.4 billion investment contract for Africa's Tazara railway line under a 30-year concession agreement, highlighting China's ongoing commitment to infrastructure development beyond its borders.

China Infrastructure Construction Market Report Scope

Infrastructure is the backbone of domestic and international commerce and industrial and agricultural production. It is the fundamental organizational and physical framework necessary to operate a firm successfully. Basic infrastructure in an organization or a nation comprises communication and transportation, sewage, water, a health and education system, safe drinking water, and a monetary system. The report offers a complete background analysis of the infrastructure sector in China, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends.

The China Infrastructure Construction Market Report is Segmented by Infrastructure (Transportation Infrastructure, Utilities Infrastructure, and More), by Construction Type (New Construction and Renovation), by Investment Source (Public and Private), and by Geography (Jiangsu, Guangdong, Zhejiang, Beijing, Shanghai and the Rest of China). The Market Forecasts are Provided in Terms of Value (USD).

By Infrastructure

| Transportation Infrastructure |

| Utilities Infrastructure |

| Social Infrastructure |

| Extraction Infrastructure |

By Construction Type

| New Construction |

| Renovation |

By Investment Source

| Public |

| Private |

By Geography

| Jiangsu |

| Guangdong |

| Zhejiang |

| Beijing |

| Shanghai |

| Rest Of China |

| By Infrastructure | Transportation Infrastructure |

| Utilities Infrastructure | |

| Social Infrastructure | |

| Extraction Infrastructure | |

| By Construction Type | New Construction |

| Renovation | |

| By Investment Source | Public |

| Private | |

| By Geography | Jiangsu |

| Guangdong | |

| Zhejiang | |

| Beijing | |

| Shanghai | |

| Rest Of China |

Key Questions Answered in the Report

What is the value of the China infrastructure construction market in 2025?

The China infrastructure construction market size reached USD 815.47 billion in 2025 and is forecast to hit USD 1,107.85 trillion by 2030.

Which infrastructure segment currently contributes the most spending?

Transportation holds 41.3% of 2024 spending thanks to rapid high-speed rail and urban-transit expansion.

Which construction type is growing fastest?

Renovation projects are advancing at 7.70% CAGR through 2030, reflecting extensive urban-renewal schemes.

How fast is private investment expanding?

Private capital is rising at an 8.50% CAGR as PPP reforms and bond-equity flexibility attract non-state funds.

Which geography leads project value today?

Shanghai leads with just over half of 2024 outlays, boosted by mega transport hubs and AI data-center clusters.

What risk could slow future project approvals?

Rising local-government debt, now at USD 651 billion in bond repayments for 2024, may delay new tender releases.

Page last updated on: