Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

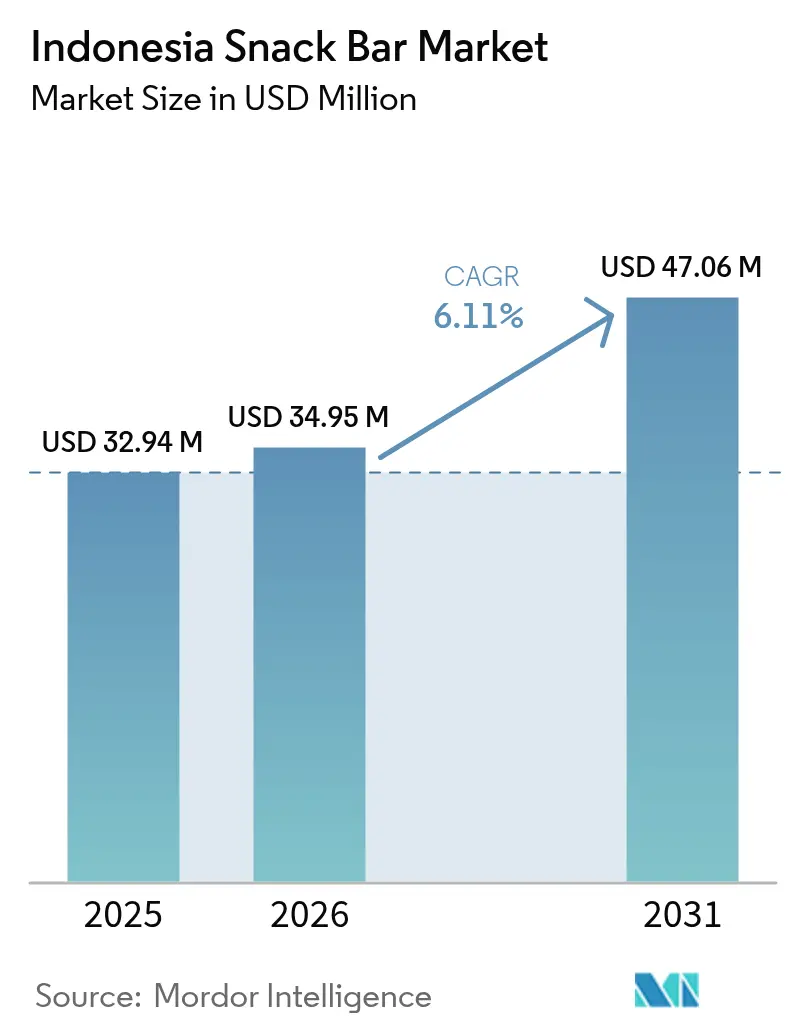

| Base Year Market Size (2025) | USD 32.94 Million |

| Market Size (2026) | USD 34.95 Million |

| Market Size (2031) | USD 47.06 Million |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia Snack Bar Market Analysis by Mordor Intelligence

The Indonesian snack bars market size is expected to grow from USD 32.94 million in 2025 to USD 34.95 million in 2026 and is forecast to reach USD 47.06 million by 2031 at 6.11% CAGR over 2026-2031. This robust growth is buoyed by a surge in the nation's healthy food consumption in 2024, an expanding middle class with increased purchasing power, and regulatory mandates for transparent labeling on nutrient-rich snacks. Factors such as rising urbanization, a bolstered e-commerce framework, and manufacturers' investments in local flavor innovations are driving deeper penetration of snack bars in both traditional and modern retail outlets. For example, the World Bank reported that in 2024, 59.2% of Indonesia's population resided in urban locales[1]Source: World Bank, "DataBank", www.databank.worldbank.org. Furthermore, as competitive dynamics intensify, major players like PepsiCo, Mars Wrigley, and Nestlé are amplifying local production, while regional entities such as Indofood and Mamame are capitalizing on cultural nuances to secure shelf space in minimarkets and convenience stores.

Key Report Takeaways

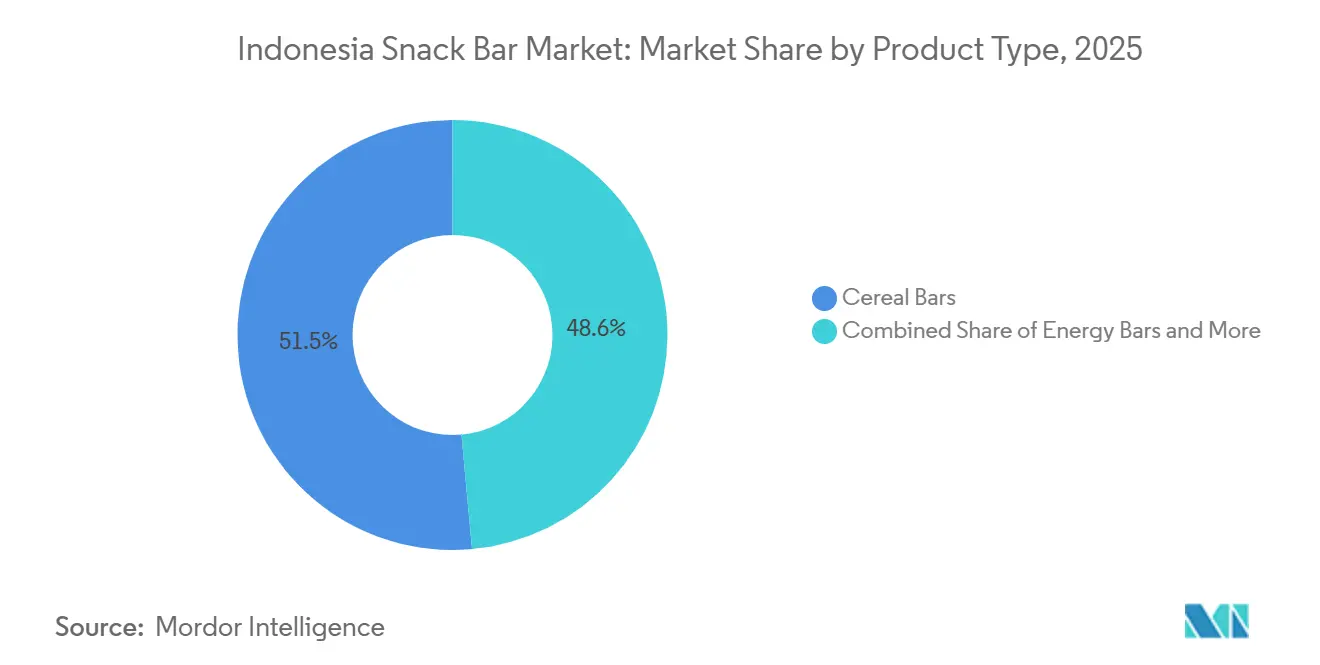

- By product type, cereal bars led with 51.45% Indonesian snack bars market share in 2025, while energy bars are projected to expand at a 7.67% CAGR through 2031.

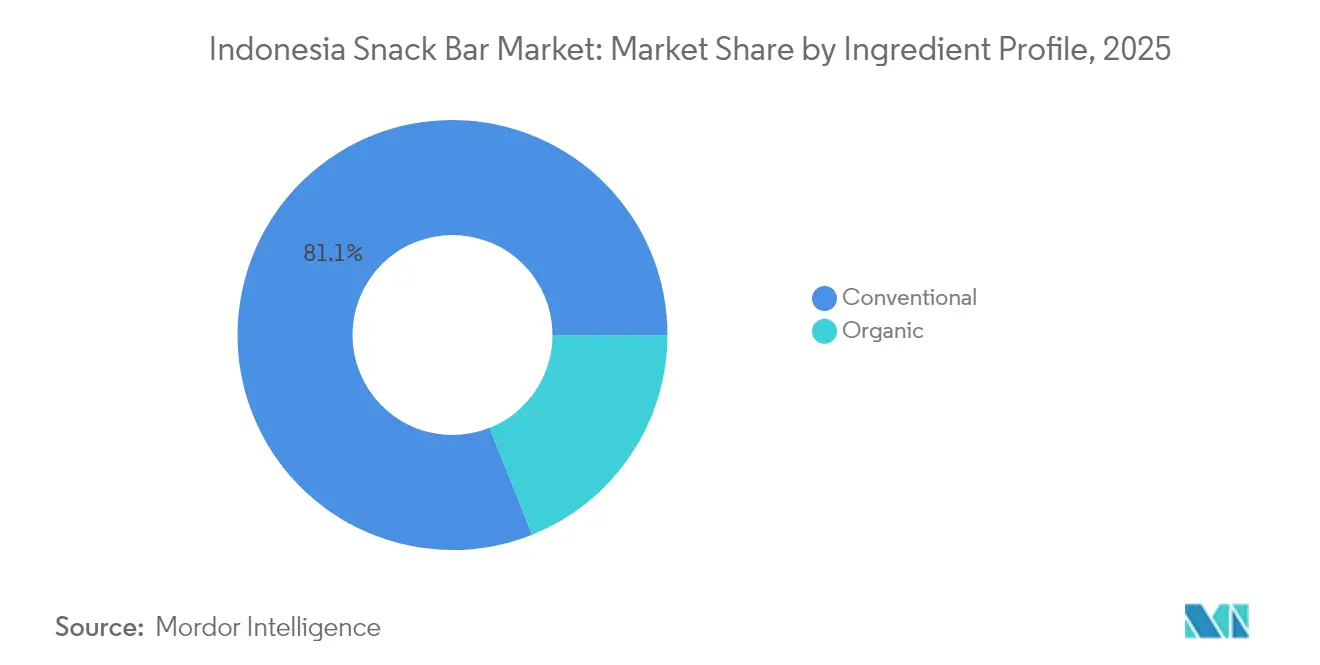

- By ingredient profile, conventional formulations held 81.05% of the Indonesian snack bars market size in 2025, whereas organic variants record the highest projected CAGR at 8.01% between 2026-2031.

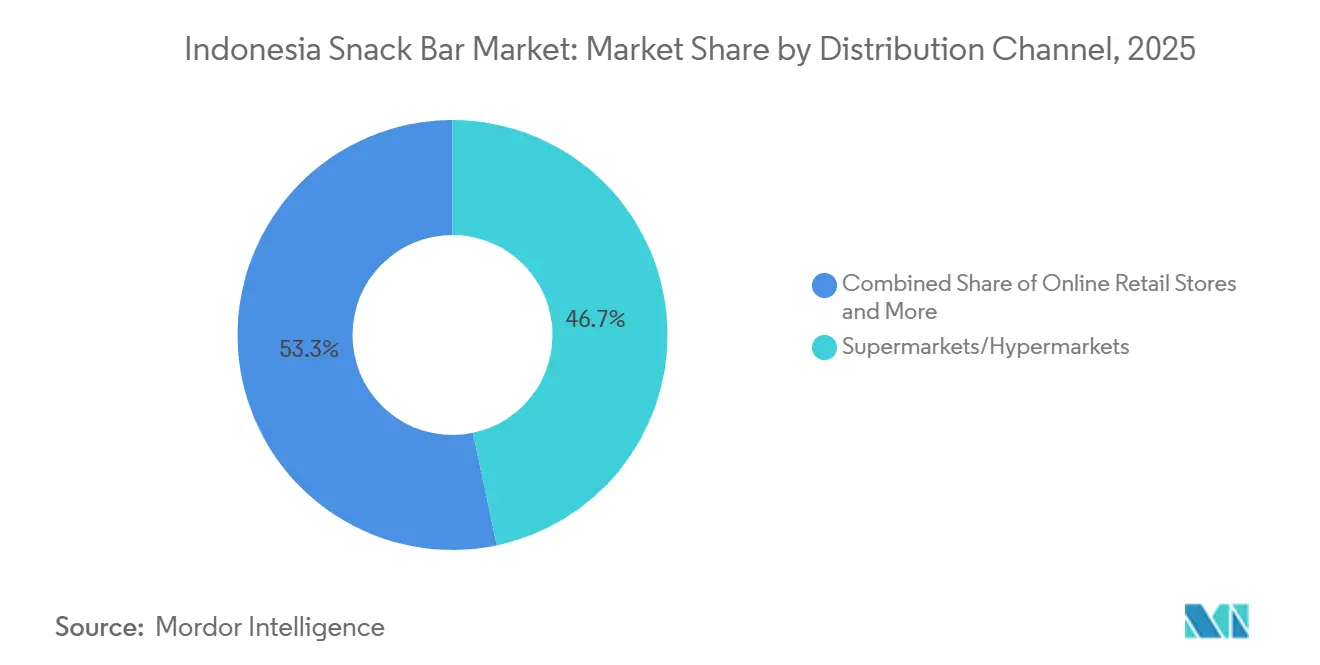

- By distribution channel, supermarkets and hypermarkets commanded 46.70% share of the Indonesian snack bars market size in 2025, and online retail platforms are advancing at a 8.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Snack Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Health and Wellness Awareness | +1.8% | National, with stronger penetration in Java and urban centers | Medium term (2-4 years) |

| Product Innovation Including Local Flavors | +1.2% | National, with regional flavor preferences in Sumatra, Java, and Sulawesi | Short term (≤ 2 years) |

| Expansion of Retail Infrastructure | +0.9% | National, with accelerated growth in tier 2-3 cities | Long term (≥ 4 years) |

| Sustainability and Ethical Sourcing Trends | +0.7% | Global influence, strongest in Jakarta and major urban areas | Medium term (2-4 years) |

| Government Initiatives Promoting Healthy Lifestyles | +0.6% | National, coordinated through provincial health departments | Long term (≥ 4 years) |

| Cultural Adaptation and Taste Preferences | +0.4% | Regional, varying by cultural zones across archipelago | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Health and Wellness Awareness

Indonesian consumers are increasingly prioritizing health, often opting to spend more on nutritious foods. For example, the Global Organic Trade Guide reported that in 2023, Indonesia's health and wellness product consumption reached approximately USD 12.99 billion. This trend isn't just a fleeting wellness fad; it's a significant shift in dietary priorities, largely driven by rising rates of non-communicable diseases, notably obesity. Generation Z is at the forefront of this change, actively integrating healthy foods into their diets and establishing a robust market for protein-rich, low-sugar snack bars. Today's Indonesian consumers are not just calorie counters; they meticulously examine labels, prioritizing freshness and natural ingredients. This heightened awareness of nutritional quality is reshaping purchasing behaviors, signaling a promising growth trajectory for the healthy food market, especially for snack bars emphasizing functional nutrition.

Product Innovation Including Local Flavors

In Indonesia, snack bar innovation marries traditional ingredients with modern nutritional insights. A prime example is the tempeh-based snack bar, which taps into Indonesia's rich fermentation legacy while boasting a high protein content. Research highlights the benefits of integrating local ingredients, such as white saffron (Curcuma mangga Val.), into snack bars. These formulations not only boost antioxidant activity but also resonate with consumers, especially when paired with Carboxymethyl Cellulose. Looking ahead to 2025, food trends are spotlighting anti-inflammatory components, tropical fruits like mango and pineapple, and dates as natural sweeteners, all of which present lucrative opportunities for snack bar formulations. Companies are realizing that true localization goes beyond just flavor tweaks. It's about aligning with Indonesian preferences in texture and portion sizes, especially since urban adolescents often view snacking as a meal substitute. This drive for innovation is fueling research and development investments in the sector, underscoring the need for companies to deeply understand the diverse regional taste profiles across Indonesia's rich cultural tapestry.

Expansion of Retail Infrastructure

Indonesia's retail landscape is undergoing a transformation, with convenience stores rapidly expanding their footprint and reshaping the accessibility of snack bars. Data from the USDA Foreign Agricultural Service highlights that in 2023, Indonesia boasted 46,118 convenience stores, collectively raking in retail sales of approximately USD 17.5 billion[2]Source: USDA Foreign Agricultural Service, "Indonesia Retail Foods Annual - 2024", apps.fas.usda.gov. This surge in convenience stores, such as Indomaret and Alfamart, especially in rural locales, presents a golden opportunity for snack bar manufacturers, tapping into the rising demand for health-centric products. Furthermore, the Palapa Ring Project, a significant digital infrastructure initiative, is broadening broadband access throughout the archipelago. This advancement paves the way for omnichannel retail strategies, seamlessly blending physical and digital shopping experiences. While traditional markets have long been the cornerstone of food sales, their dominance is waning. Modern retail formats are stepping in, offering the consistent product availability and quality assurance that today's health-conscious consumers prioritize, as noted by the U.S. Department of Agriculture. Notably, this infrastructure boom is most pronounced in tier 2 and 3 cities, where emerging brands are carving out their niche by harnessing local identities and pioneering distribution methods that sidestep conventional gatekeepers.

Sustainability and Ethical Sourcing Trends

In Indonesia's food sector, sustainability initiatives are gaining traction as companies increasingly recognize the direct link between environmental stewardship, long-term ingredient security, and consumer trust. Mondelēz International has pledged to source 100% of its cocoa and palm oil sustainably by 2025, underscoring how global giants are reshaping their supply chains to align with Indonesia's sustainability goals. In Indonesia, where many consumers are willing to pay a premium for sustainably produced foods, there's a clear market differentiation opportunity for snack bars that can showcase ethical sourcing. Responding to this trend, local firms are weaving renewable energy and local raw materials into their operations. A prime example is PepsiCo's newly designed Cikarang factory, which underscores a commitment to environmental responsibility. Beyond just environmental concerns, the sustainability movement in Indonesia also emphasizes social responsibility. Companies are challenged to navigate the nation's intricate agricultural supply chains, ensuring fair compensation for smallholder farmers who cultivate essential ingredients like palm oil, coconut, and tropical fruits. This landscape presents snack bar manufacturers with a unique opportunity: forging direct ties with Indonesian agricultural cooperatives. Such relationships could lead to cost reductions and bolster sustainability credentials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Cultural Loyalty to Traditional Snacks | -1.1% | National, strongest in rural areas and outer islands | Long term (≥ 4 years) |

| Ingredient Sourcing Constraints | -0.8% | National, with supply chain vulnerabilities in remote regions | Medium term (2-4 years) |

| Sustainability Cost Burden | -0.6% | Global influence, affecting import-dependent manufacturers | Short term (≤ 2 years) |

| Regulatory Scrutiny on Health Claims | -0.4% | National, enforced through the BPOM compliance framework | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Cultural Loyalty to Traditional Snacks

In regions outside Java and Bali, where traditional foods hold deep cultural significance and are often more affordable, there's a strong loyalty to these age-old snacks. This loyalty poses a significant hurdle for the adoption of modern snack bars. Research indicates that in provinces beyond Java and Bali, traditional snacks, ranging from those made with cereals, vegetables, and legumes to other savory varieties, are consumed more frequently. Here, socio-economic factors intertwine with a commitment to cultural preservation, leading to a resistance against Western-style nutrition bars. Data from the USDA Foreign Agricultural Service highlights that in 2023, Indonesia's savory snack consumption hit a retail sales value of approximately USD 2.2 billion[3]Source: USDA Foreign Agricultural Service, "Indonesia retail foods 2023", apps.fas.usda.gov. Price sensitivity further complicates the challenge: traditional snacks are often priced significantly lower than their imported or premium health bar counterparts, making them the go-to choice for Indonesia's budget-conscious consumers. Yet, this loyalty isn't set in stone. Studies indicate that when traditional culinary products are modernized, featuring innovative packaging, authentic flavors, enhanced convenience, and extended shelf life, they can find acceptance in the market. For snack bar manufacturers, the pivotal insight is clear: instead of trying to dismantle cultural loyalty, they can harness it. By infusing traditional Indonesian ingredients and flavors into modern nutritional formats, they can cater to local taste preferences while offering contemporary health benefits.

Ingredient Sourcing Constraints

Indonesia's intricate ingredient sourcing landscape poses challenges that influence both the production costs of snack bars and the reliability of their supply chains. The nation's agricultural sector grapples with infrastructure constraints and climate-related vulnerabilities, impacting the steady supply of essential ingredients, such as nuts, fruits, and grains, vital for snack bar production. Furthermore, surging prices of agricultural commodities strain profit margins, given that raw materials account for a substantial share of production costs in Indonesia's food and beverage sector. These sourcing challenges are intensified by Indonesia's unique archipelagic geography, where transportation hurdles and logistical intricacies can lead to supply bottlenecks. Manufacturers, in turn, face difficulties in ensuring consistent ingredient quality and availability. Compounding these challenges is the rising demand for organic and sustainably sourced ingredients. This trend places added strain on already stretched supply chains, as the pursuit of organic certification and traceability introduces further complexity and costs to procurement processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cereal Bars Lead Through Familiar Nutrition

In 2025, cereal bars held 51.45% of Indonesia's snack bars market, reflecting cereals' role as a primary carbohydrate source. Blending oats, rice crisps, and local grains like sorghum ensures affordability and acceptance, strengthening the segment. School-lunch initiatives promoting whole-grain snacks drive repeat purchases among younger demographics. Energy bars, growing at a 7.67% CAGR through 2031, benefit from Indonesia's fitness boom, supported by urban gyms and running clubs. Brands avoid regulatory issues by offering caffeine-free energy boosts from date paste and MCT-rich coconut. Protein bars, with 15g+ protein claims, target office professionals seeking convenient meal replacements. Niche bars, including gluten-free, ketogenic, and diabetic-friendly options, gain credibility through clinical trials with Indonesian academic partners.

Stricter health regulations push companies to validate claims like “muscle recovery” or “immune support.” Brands investing in local randomized studies stand out, turning science into effective marketing for early adopters. Cross-promotions with sports-drink brands, gym café discounts, and marathon sponsorships create omnichannel synergies. Clearer regulations curb gray-market imports, channeling demand toward compliant domestic products.

By Ingredient Profile: Conventional Dominance Tempered by Fast-Rising Organics

In Indonesia's snack bar market, conventional recipes featuring regular oats, glucose syrup, and dairy derivatives dominate with an 81.05% share. Their cost competitiveness and ingredient availability play a pivotal role. Given the economic pragmatism of lower-income groups, these conventional recipes are poised to maintain their lead through 2031. Meanwhile, the organic segment, driven by eco-label allure and rising disposable incomes in cities like Jakarta, Surabaya, and Bandung, is set to expand at an annual rate of 8.01%. Organic vendors emphasize offerings like pesticide-free rice crisps and fair-trade coconut sugar, appealing to premium-focused millennials and parents. To bolster visibility and trust, retailers have introduced branded "organic zones" in supermarkets.

Challenges arise from a limited domestic organic acreage and the associated certification fees. Some players are adopting a hybrid approach, incorporating organic fruits into conventional bases, allowing for mid-tier pricing that broadens their market reach without compromising on green credentials. To combat counterfeit-label concerns, digital tracing methods, such as QR codes indicating farm origins, are being employed to enhance authenticity. With BPOM fine-tuning organic labeling regulations, early adopters are reaping the benefits of first-mover advantage, solidifying their presence in consumer memory.

By Distribution Channel: Supermarkets Anchor Volume, E-Commerce Fuels Incremental Value

In 2025, supermarkets and hypermarkets captured 46.70% of Indonesia's snack bars market, establishing themselves as the go-to purchase points in urban areas. Category management teams strategically position snack bars at eye-level, right next to breakfast cereals, boosting cross-selling and increasing overall basket sizes. Additionally, loyalty programs and in-store sampling make these bars a staple in regular grocery runs. Convenience chains like Indomaret and Alfamart, with their extended hours and close proximity to residential areas, cater to spontaneous snacking desires. Online retail, witnessing a 8.74% annual growth, goes beyond mere sales. They educate consumers with detailed nutrition filters, live-stream demonstrations, and influencer reviews, effectively persuading first-time buyers. Even as online grocery shopping habits solidified post-pandemic, services like click-and-collect bridge the gap between digital and physical shopping. Direct-to-consumer platforms not only offer bundled subscriptions for consistent revenue but also provide brands with deep insights into consumer behavior. Brands from secondary cities leverage TikTok's social-commerce features, sidestepping traditional distributors, and directly engaging with island communities often overlooked by modern retail. While niche, specialty health stores spotlight high-margin functional bars and act as incubators for new innovations.

Geography Analysis

Java, bolstered by rising GDP per capita and a dense retail network, leads Indonesia's snack bars market. Jakarta, with its bustling work culture, accounts for about one-third of the national volume, driving demand for on-the-go nutrition. Meanwhile, urban areas in Kalimantan, Sulawesi, and Sumatra are witnessing mid-single-digit growth, thanks to expanding infrastructure and local government initiatives promoting balanced diets in school feeding programs. Tier-2 cities like Semarang and Makassar present untapped opportunities, especially where modern retail developments align with a burgeoning middle-class demographic.

Indonesia's archipelagic nature poses logistical challenges; smaller islands rely on sporadic shipments, leading to inflated prices and limited product access. While e-commerce offers some relief, shortcomings in cold-chain logistics hinder the distribution of chocolate-coated bars in humid areas. Cikarang, an industrial hub in West Java and the site of PepsiCo's latest plant, serves as a strategic point, reducing transit times to the densely populated western and central markets. In contrast, Papua and Maluku stand as untouched territories where traditional snacks still reign supreme. However, with the backing of NGOs, fortified bars are making inroads, aiming to address malnutrition issues.

Thanks to the Palapa Ring initiative, digital connectivity is set to boost eastern provinces by 2027, facilitating better inventory management and consumer engagement. Brands are collaborating with logistics startups to establish micro-fulfillment centers, streamlining last-mile deliveries, reducing spoilage, and enhancing product freshness. Regional marketing strategies must consider local spice preferences, while chili-mango flavored bars thrive in Sulawesi, they falter in Aceh, where a sweeter taste is favored. Additionally, using local languages like Bahasa and regional dialects for labeling fosters better compliance and builds consumer trust.

Competitive Landscape

In Indonesia's snack bar industry, a blend of international giants and local specialists is reshaping the landscape. Indofood, leveraging its vast distributor network and co-branding with its popular instant noodles, ensures its products dominate the shelves. After a multi-year absence, PepsiCo's USD 200 million facility in Cikarang is back, introducing flexible production lines for granola and protein bars sweetened with local palm sugar. Meanwhile, Mondélez is innovating, expanding its Oreo wafer-stick line into hybrid bar formats and strategically pairing them with beverages to boost sales.

Disruptors like Mamame are carving out a niche, targeting allergen-free markets. By infusing tempeh into their bars, they're appealing to both vegan and Muslim consumers seeking Halal-certified protein. Start-ups are harnessing social commerce, using platforms like WhatsApp for interactive recipes and loyalty coupons, fostering community engagement and feedback for product development. Sustainability is becoming a pivotal differentiator; modern retailers, keen on meeting corporate ESG targets, are influenced by RSPO palm oil sourcing and recyclable wrappers in their procurement decisions.

Collaborations are on the rise; Nestlé partners with Indonesian dairy cooperatives, securing a consistent whey-protein supply and reducing import dependency. Mars Wrigley introduces portion-controlled lines, aligning with government initiatives to combat obesity. Retailers like Hypermart are expanding private labels, tightening price competition but also boosting category visibility, pushing branded players to innovate at a faster pace.

Indonesia Snack Bar Industry Leaders

-

Otsuka Pharmaceutical Co., Ltd.

-

Mondelez International

-

Nestlé S.A.

-

General Mills, Inc.

-

PT Kalbe Farma Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Mondelez International launched innovative versions of snack bars combining global and local flavors like tempeh, tropical fruits, and spices tailored to Indonesian tastes. These novel adaptations aimed to capture local consumer preferences and leverage popular traditional ingredients in convenient snack formats, launched in retail channels in 2024.

- August 2024: Fitbar introduced additional organic and tropical fruit-based snack bars to build on its initial healthier snack bar line. These variants broadened product offerings with more options carrying health and wellness positioning in retail sectors.

- September 2023: Mayora Indah, a major Indonesian FMCG player, partnered with an international food innovation company to develop plant-based snack bars. This product launch focused on vegan and sustainable snack options, aligning with rising consumer interest in plant-based diets and eco-friendly products.

- August 2023: Fitbar, an Indonesian brand under Kalbe Farma, launched a new line of health-focused snack bars made with locally sourced, organic ingredients such as coconut and tropical fruits. These bars targeted clean-label, nutritious snack options aimed at health-conscious consumers in Indonesia.

Indonesia Snack Bar Market Report Scope

Snack bars offer the market players lucrative opportunities for growth in terms of functional ingredients, reduced sugar, savory spins, and plant proteins.

Indonesia snack bar Market is segmented by type and distribution channel. Based on type, the market is segmented into cereal bars, energy bars, and other snack bars. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, specialty stores, online stores, and others.

The report offers market size and forecasts for the Indonesia Snack Bar Market in value (USD million) for all the above segments.

By Product Type

| Cereal Bars |

| Energy Bars |

| Protein Bars |

| Other Bars |

By Ingredient Profile

| Conventional |

| Organic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty/Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Cereal Bars |

| Energy Bars | |

| Protein Bars | |

| Other Bars | |

| By Ingredient Profile | Conventional |

| Organic | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty/Health Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the current size of the Indonesian snack bars market?

It is valued at USD 34.95 million in 2026.

How fast will the market grow through 2031?

The market is projected to register a 6.11% CAGR to reach USD 47.06 million by 2031.

Which product type leads in sales?

Cereal bars command 51.45% share of total 2025 sales.

Which distribution channel is expanding the quickest?

Online retail platforms are set to grow at a 8.74% CAGR between 2026-2031.

Why are organic snack bars gaining traction?

72% of shoppers say they will pay more for sustainably sourced foods, driving 8.01% annual growth in organic formulations.

What regulation affects snack bar labeling in Indonesia?

BPOM Regulation No. 10/2024 mandates full ingredient, allergen, and nutrition labeling for all processed snacks from January 2025 onward.

Page last updated on: