Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Indonesia Plastics Report is Segmented by Type (Traditional Plastics, Engineering Plastics, and Bioplastics), Technology (Blow Molding, Extrusion, Injection Molding, and Other Technologies), and Application (Packaging, Electrical and Electronics, Building and Construction, Automotive and Transportation, Furniture and Bedding, and Other Applications). The Market Forecasts are Provided in Terms of Volume (Tons).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

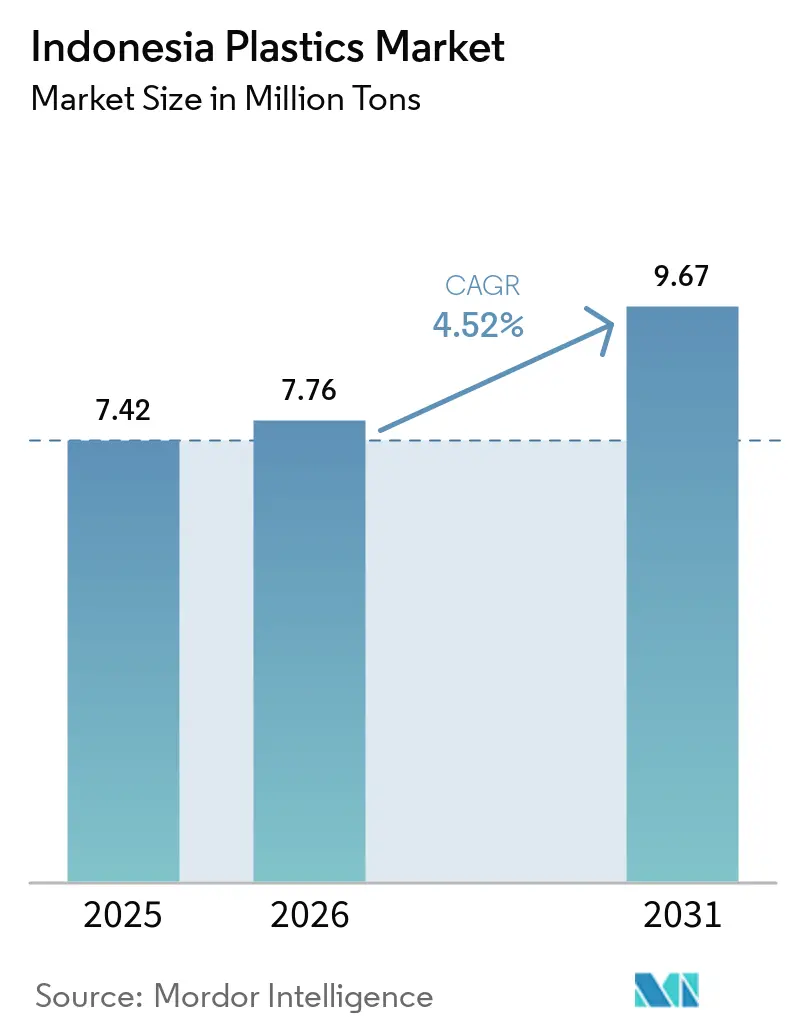

| Market Volume (2026) | 7.76 Million tons |

| Market Volume (2031) | 9.67 Million tons |

| CAGR | 4.52 % |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Indonesia Plastics Market size is expected to grow from 7.42 million tons in 2025 to 7.76 million tons in 2026 and is forecast to reach 9.67 million tons by 2031 at 4.52% CAGR over 2026-2031. The Indonesia plastics market is benefiting from synchronized upstream and downstream investments, tighter self-sufficiency targets for ethylene, and resilient demand from packaging, automotive, and electronics converters. Capacity additions in Cilegon and Tuban are improving feedstock security, while Extended Producer Responsibility rules set for mid-2026 are steering resin specifications toward mono-material solutions that are easier to recycle. E-commerce growth is pushing converter demand for impact-resistant secondary packs, and Indonesia’s dominance in tropical seaweed is opening a premium export niche for compostable biopolymers. Margin pressure from Chinese imports, a rising carbon tax, and logistics bottlenecks temper the outlook, yet integration and specialty-grade pivots are helping leading producers defend profitability.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expansion of downstream petro-complexes Expansion of downstream petro-complexes | +1.8% | Java (Cilegon, Tuban) and spillover to Sumatra | Medium term (2-4 years) | (~) % Impact on CAGR Forecast :+1.8% | Geographic Relevance :Java (Cilegon, Tuban) and spillover to Sumatra | Impact Timeline :Medium term (2-4 years) |

Lightweight auto-parts adoption by OEMs Lightweight auto-parts adoption by OEMs | +0.9% | Greater Jakarta and Karawang automotive belt | Long term (≥ 4 years) | |||

E-commerce logistics boom E-commerce logistics boom | +1.2% | National, early gains in Jakarta, Surabaya, and Bandung | Short term (≤ 2 years) | |||

Mandatory EPR and waste-segregation pilots Mandatory EPR and waste-segregation pilots | +0.7% | Pilot cities Jakarta, Surabaya, and Banyuwangi | Medium term (2-4 years) | |||

Seaweed-based bioplastics clusters Seaweed-based bioplastics clusters | +0.5% | East Java, East Lombok, and South Sulawesi | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Expansion of Downstream Petro-Complexes

The November 2025 start-up of a 1 million ton ethylene cracker and 450,000 ton polyethylene unit in Cilegon eliminates the need for imported ethylene on Java, cuts pipeline logistics, and leverages up to 50% LPG (liquefied petroleum gas) feedstock flexibility that arbitrages naphtha-LPG spreads. A re-scoped CAP-2 project adds chlor-alkali and ethylene dichloride (EDC) output in 2027, shrinking Indonesia’s vinyl import gap, while a planned 720,000 tons polyethylene terephthalate (PET) line set for 2028 lowers beverage-grade reliance on foreign supply. Together, these builds lift projected domestic coverage of overall resin demand to 70% by 2031 and unlock roughly USD 2 billion in annual economic value. Integrated layouts also concentrate skilled labor and shared utilities, reinforcing Java’s status as the nucleus of the Indonesia Plastics market. The combined scale is expected to soften feedstock price volatility, though grid congestion around Merak and Cilegon must still be eased to fully capture logistics savings.

Lightweight Auto-Parts Adoption by OEMs

Automotive assemblers are targeting 10% curb-weight cuts that can translate into 6-8% fuel savings, prompting a steady switch from steel to engineering plastics such as PC-ABS blends for dashboards and polyamide for under-hood parts[1]DuPont Performance Polymers, “Lightweighting benefits in automotive platforms,” Dupont.com. Tier-1 suppliers in Karawang source locally compounded grades, which reduces import lead time and ring-fence original equipment manufacturers (OEMs) from forex swings. ASEAN harmonized standards reward lower CO₂ output, intensifying demand for flame-retardant, high-temperature resins ahead of rising electric-vehicle penetration. Limited domestic capacity for niche polymers like polybutylene terephthalate (PBT) continues to pull in imports from Japan and South Korea, yet joint-venture talks signal momentum toward onshore specialty polymer plants. These moves fortify value capture across the Indonesia Plastics market, even as commodity margins tighten.

E-Commerce Logistics Boom

Online retail growth across 17,000 islands exposes packages to humidity and vibration, raising preference for HDPE (high-density polyethylene) and LLDPE (linear low-density polyethylene) cushioning over paper options. National couriers now specify impact-resistant blow-molded HDPE bottles, canisters, and jerry cans that withstand last-mile handling. Converters have invested in multi-layer extrusion blow molding lines able to incorporate recycled content without sacrificing barrier performance, which meets brand-owner pledges for 25% post-consumer recycled (PCR) integration by 2028. Consumer surveys reveal a shift toward mono-material packs, encouraging designers to drop aluminum foil layers that hinder recyclability, and this plays directly into mid-2026 extended producer responsibility (EPR) compliance needs. The logistics driver, therefore, widens resin off-take while nudging converters up the value chain toward circular design standards.

Mandatory EPR and Waste-Segregation Pilots

Indonesia’s Presidential Regulation on EPR, entering force mid-2026, compels brand owners to finance the collection and recycling of post-consumer packaging. Pilots in Jakarta, Surabaya, and Banyuwangi already lifted collection access for more than half a million residents and recorded over 12,000 tons of recovered plastics, showing that scalable reverse-logistics models are viable. Capital is flowing toward capacity: an r-PET producer secured growth funding in 2025 to process 2.8 billion bottles annually, and a 2026 feasibility study is charting Indonesia’s first integrated polyolefin recycling hub in East Java[2]Borouge, “East Java circular economy feasibility study,” Borouge.com. Resin grades that can be mechanically recycled with minimal quality loss, HDPE, PP, and PET, stand to gain the most, while converters tied to PVDC or multi-material laminates face volume at risk. In the near term, EPR surcharges may raise pack costs, yet long-run compliance is expected to accelerate circular resin uptake across the Indonesia Plastics market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

30% excise on single-use plastic bags 30% excise on single-use plastic bags | -0.6% | National, initial focus on urban centers | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast :-0.6% | Geographic Relevance :National, initial focus on urban centers | Impact Timeline :Short term (≤ 2 years) |

Carbon-pricing scheme Carbon-pricing scheme | -0.8% | Java and Sumatra industrial zones | Medium term (2-4 years) | |||

Rail-infrastructure gaps Rail-infrastructure gaps | -0.4% | National, acute in Sumatra and Kalimantan | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

30% Excise on Single-Use Plastic Bags

Draft excise legislation proposes IDR 30,000 per kg for thin HDPE and LDPE bags, threatening a 5-8% volume hit for film-grade resin suppliers if enacted in 2026. Retailers could pivot to reusable totes or thicker HDPE bags that dodge weight thresholds, softening true environmental gains. Municipal enforcement capacity varies, as past bans in Banjarmasin and Bogor suffered compliance gaps. The uncertainty already stalls new LDPE capacity investments, with converters waiting for final tax brackets before signing long-term offtake deals. Policy clarity is therefore critical for stable growth in the Indonesia Plastics market.

Carbon-Pricing Scheme Raising Energy Costs

A carbon tax of IDR 30,000 per ton CO₂e took effect in 2025 and will likely escalate, adding roughly USD 1.80 per ton of resin for coal-reliant processors. Grid power in Java is more than 60% coal, so crackers face steeper cost creep than gas-based rivals in Malaysia or Vietnam. Large producers are evaluating solar and waste-heat recovery, yet retrofits topping USD 50 million push payback beyond five years. Weak liquidity on the national carbon exchange limits offset options, and absent border adjustments allow imports to undercut local supply. Cost pass-through pressures could erode margins within the Indonesia Plastics market unless more renewable capacity comes onstream.

By Type: Traditional Plastics Anchor Volume, Bioplastics Capture Niches

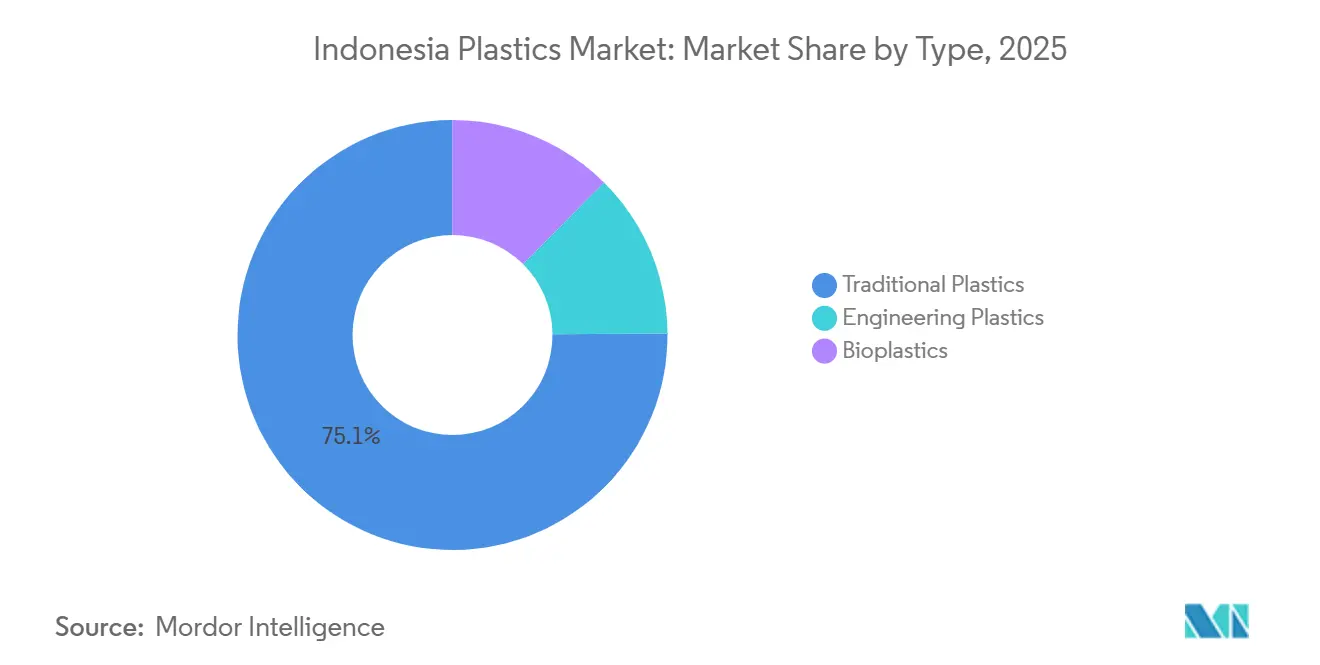

Traditional Plastics secured 75.12% of Indonesia Plastics market share in 2025, with polyethylene and polypropylene making up the bulk of film, bottle, and injection molded items. The Indonesia Plastics market size for these grades rose in tandem with e-commerce packaging and construction pipe demand. Polyethylene benefits from high output at newly commissioned Cilegon lines, and polypropylene growth tracks automotive bumper and raffia sack orders. PVC usage in pipe and cable remains resilient, though some converters experiment with polyolefin substitution to navigate chlorine scrutiny.

Engineering Plastics, though smaller in tonnage, command premium pricing in electronics housings and under-hood auto parts, lifting their revenue footprint. PET is set for a capacity burst once a 720,000-ton plant starts in 2028, improving bottle-grade security and trimming import bills. Bioplastics, led by seaweed resins, hold a thin volume but are expected to grow with the fastest CAGR of 6.12% during the forecast period (2025-2031), mirroring global bans on single-use fossil plastics. The Indonesia Plastics market size for biopolymer grades hinges on cost convergence and potential tax credits that are still on the policy table.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Injection Molding Leads, Blow Molding Gains

Injection Molding owned 47.22% of the 2025 volume, reflecting entrenched use for consumer electronics shells and vehicle interior panels. Its capital-intensive molds reinforce scale economies, favoring established converters across Java. As electric vehicle (EV) adoption widens, molders are investing in high-temperature screw barrels that process flame-retardant polyamides, which should sustain their lead.

Blow Molding is projected to advance at a 5.23% CAGR during the forecast period (2026-2031), fastest among processes, as e-commerce logistics require durable HDPE bottles and IBCs (intermediate bulk containers) that survive multi-modal transit. Multi-layer co-extrusion units unlock oxygen-barrier packaging for juices and pharmaceuticals, nurturing a value-added niche. Extrusion film remains indispensable for LDPE agricultural mulch and consumer sachets, while rotational and thermoforming lines fill out niche demand for tanks and refrigerator liners within the Indonesia Plastics industry.

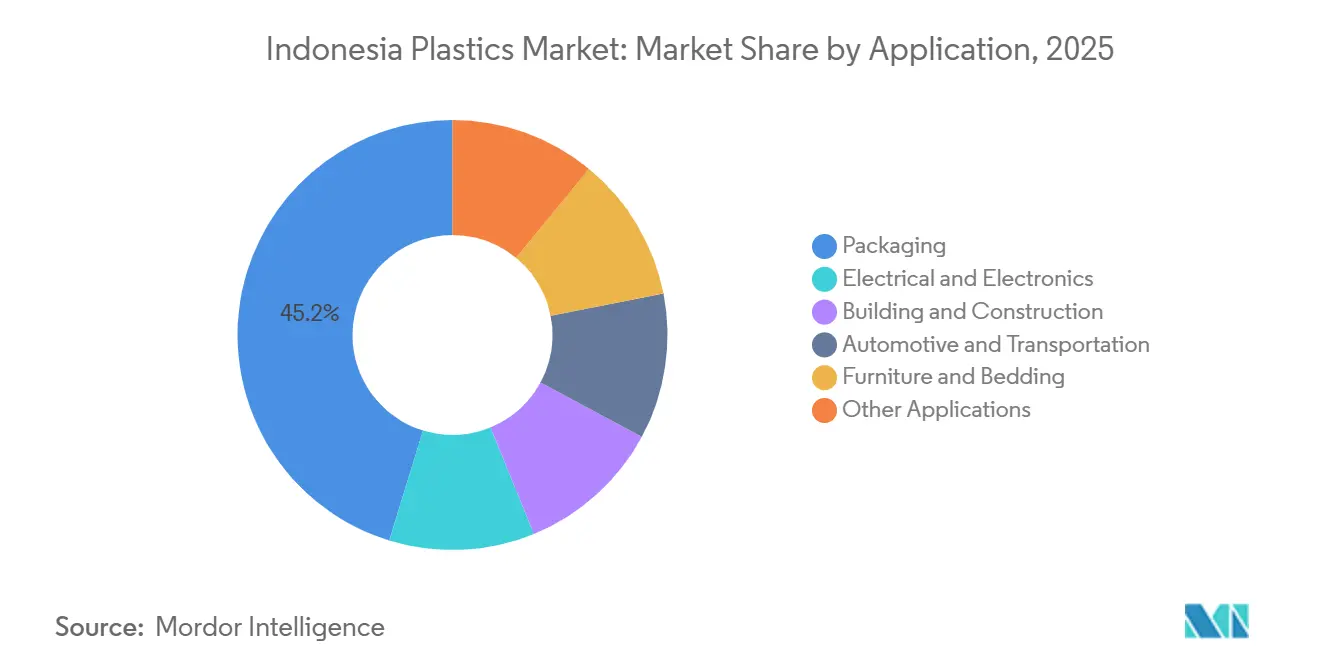

By Application: Packaging Dominates, Automotive and Electronics Climb

Packaging held 45.23% of the Indonesia Plastics market size in 2025, boosted by sachet culture, bottled water, and rapid grocery delivery. Mandatory EPR from 2026 is steering design toward mono-material PE and PP films that are readily recyclable, opening sales for metallocene-based high-clarity grades. Growth in post-consumer recycled content is creating a split market, with premium PCR-certified resins fetching higher margins. However, the packaging is the fastest-growing application in the market with an expected CAGR of 5.35% during the forecast period (2026-2031).

Automotive and Electronics segments trail in tonnage but deliver higher returns through engineering plastics that meet strict mechanical and thermal specs. Under-hood fuel systems, LED lighting, and battery casings are adding polyamide and polycarbonate pulls. Construction consumes PVC pipes and profiles in line with the RPJMN (National Medium-Term Development Plan) housing agenda, though cost inflation from the carbon tax may slow project tendering. Furniture, agriculture, and medical uses round out a balanced demand mix that keeps the Indonesia Plastics market diversified.

Note: Segment shares of all individual segments available upon report purchase

Java absorbs the majority of national resin off-take and now hosts a vertically integrated cluster that runs from naphtha cracking to polymer compounding. Cilegon’s twin crackers pipe ethylene and propylene directly to converters in Greater Jakarta and Karawang, slashing inventory costs and enabling just-in-time deliveries to automotive and electronics OEMs. Congestion on the Merak-Jakarta toll corridor, however, routinely adds hours to truck trips, dampening some of those logistics gains.

Sumatra ranks second for consumption, fueled by palm-oil packaging and pulp-and-paper coatings that rely on LDPE and polypropylene raffia. Limited deep-water port capacity at Dumai and Belawan raises import freight, yet coastal feeder links still challenge Java-origin shipments on cost. East Java is emerging as a circular-economy hotspot, anchored by Surabaya’s port and a proposed polyolefin recycling hub that could serve as a feedstock pool for converters in Gresik and Pasuruan. The region also sits near seaweed farms that supply biopolymer inputs, giving it a strategic edge in green plastics.

Kalimantan and Sulawesi remain underpenetrated, constrained by sparse infrastructure and scattered population clusters. Resin demand here is tied to mining and agro-commodities packaging, with many converters importing finished goods from Java or Malaysia. Inter-island freight premiums of 10-15% persist because dedicated cargo rail or subsidized feeder services are absent. The government’s 2025-2045 roadmap calls for new refinery-cracker capacity in Tuban and Balongan plus rail spurs that could rebalance geography, but funding clarity is pending. Until then, the Indonesia plastics market is expected to stay Java-centric.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

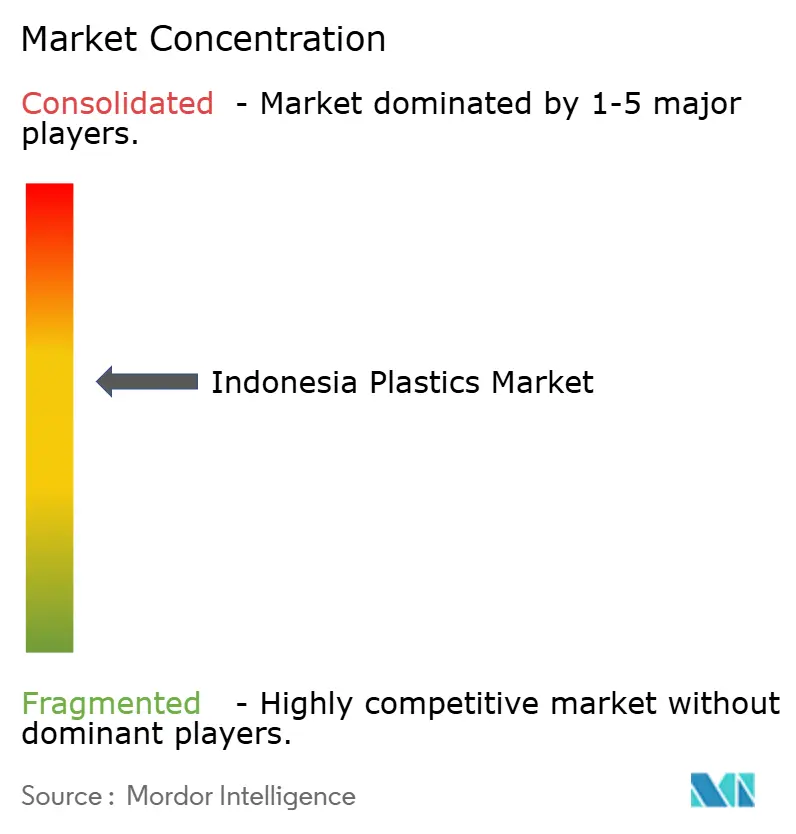

Market Concentration

The Indonesia Plastics market is moderately consolidated. Margin pressure from Chinese exports doubling in 2025 shifts strategic focus toward specialty polymers and circular feedstocks. Chandra Asri’s CAP-2 emphasizes chlor-alkali and EDC to displace vinyl imports, while Barito Pacific channels capex into renewable power to blunt carbon-tax escalation. Recycling is the fastest-moving adjacency: an r-PET leader attracted growth capital in July 2025, and the February 2026 feasibility study for East Java polyolefin recycling underscores investor appetite.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Volume)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

Plastic is an artificial substance produced from polymers, large molecules composed of repeating subunits. These polymers are commonly derived from petrochemicals, although some plastics can be made from natural materials. The distinctive feature of plastics lies in their ability to undergo deformation and take on various forms when exposed to heat or pressure.

The Indonesian plastics market is segmented by type, technology, and application. By type, the market is segmented into traditional plastics, engineering plastics, and bioplastics. By technology, the market is segmented into injection molding, extrusion, blow molding, and other technologies. By application, the market is segmented into packaging, automotive and transportation, building and construction, electrical and electronics, furniture and bedding, and other applications. For each segment, the market sizing and forecasts were made based on volume (tons).

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.