Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.64 Billion |

| Market Size (2026) | USD 4.71 Billion |

| Market Size (2031) | USD 5.22 Billion |

| Growth Rate (2026 - 2031) | 2.06% CAGR |

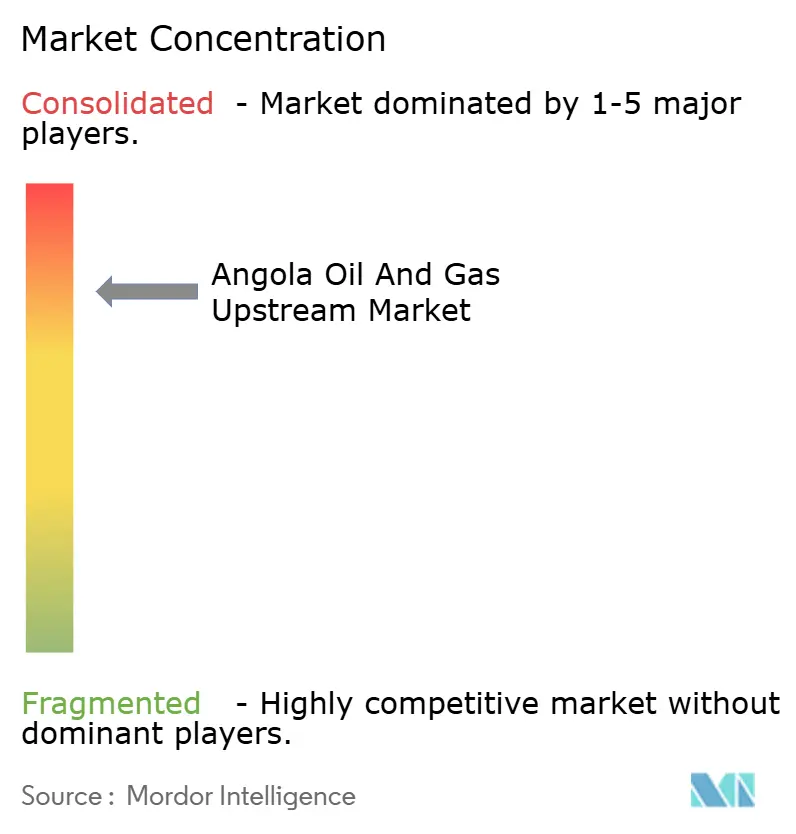

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Angola Oil And Gas Upstream Market Analysis by Mordor Intelligence

The Angola Oil And Gas Upstream Market size is projected to expand from USD 4.64 billion in 2025 and USD 4.71 billion in 2026 to USD 5.22 billion by 2031, registering a CAGR of 2.06% between 2026 to 2031.

Rising investment in ultra-deepwater projects, a lighter fiscal regime, and the country’s freedom from OPEC quotas are combining to stabilize output despite a 6-8% annual decline in mature fields. Deep- and ultra-deepwater final investment decisions (FIDs) now close in under 30 months, shortening cash-flow cycles for super-majors and independents alike. Natural-gas monetization is accelerating as the Northern Gas Complex supplies feedstock to the under-utilized Angola LNG plant, while onshore tight-oil pilots in the Kwanza basin broaden the resource base. A depreciating kwanza and high sovereign-debt servicing still inflate dollar-denominated service costs, but tax cuts on marginal fields now offset part of that burden.

Key Report Takeaways

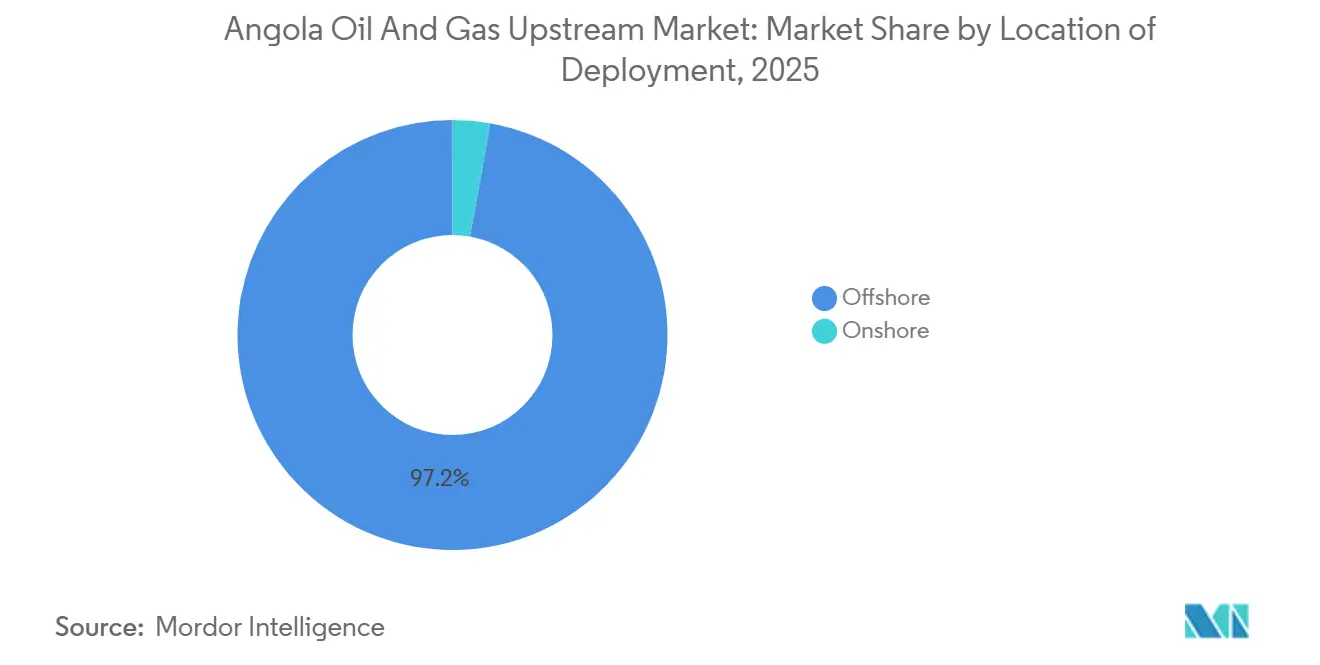

- By location of deployment, offshore operations held 97.2% of the Angola oil & gas upstream market share in 2025, whereas onshore exploration is expected to advance at 2.9% CAGR through 2031.

- By resource type, crude oil generated 90.3% of 2025 revenue, yet natural gas is the fastest-growing resource is projected to expand at 6.6% CAGR to 2031.

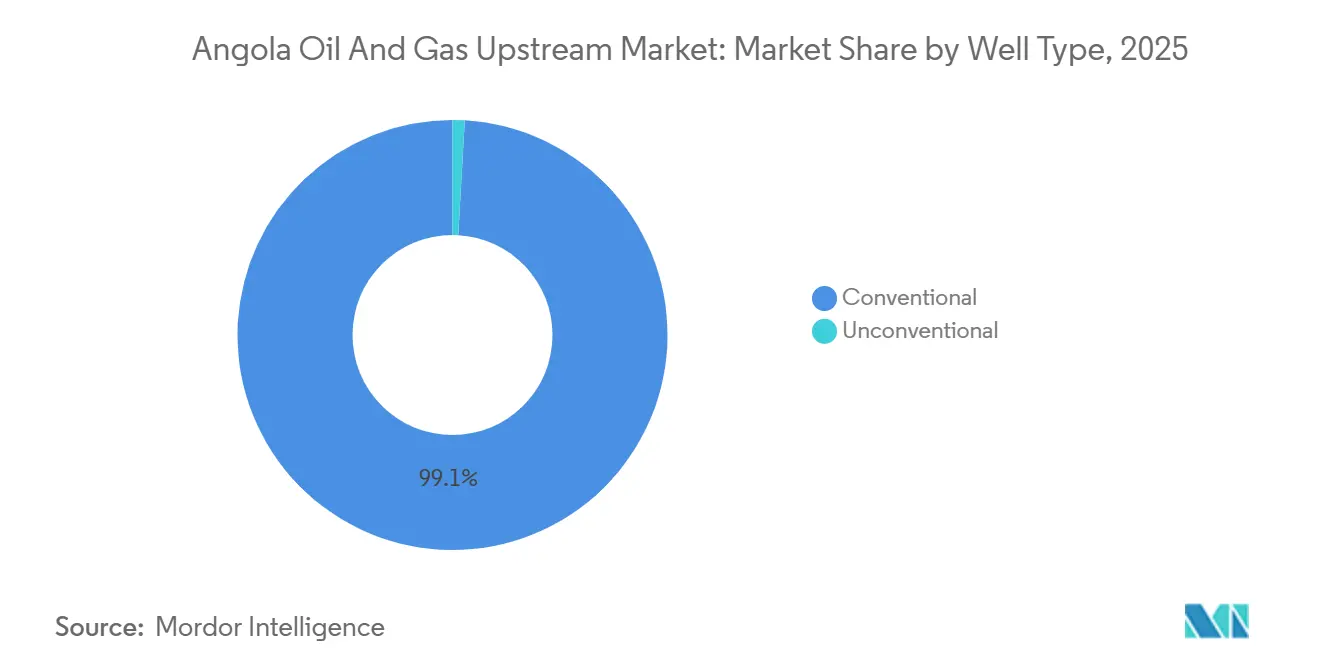

- By well type, conventional wells accounted for 99.1% of 2025 activity; unconventional wells are projected to rise at 11.7% CAGR, lifting their contribution to 3-5% of total wells by 2031.

- By service, development and production services captured 85.6% revenue in 2025, while exploration services are projected to expand at 5.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Angola Oil And Gas Upstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Licensing-round momentum attracting super-majors | 0.4% | National, with concentration in Kwanza and Benguela offshore basins, onshore Kwanza, Namibe, and Kassanje basins | Medium term (2-4 years) |

| Deep- and ultra-deepwater FIDs (e.g., Kaminho, Agogo) accelerating near-term output | 0.6% | National, focused on Blocks 15/06, 17, 20/11, 48, and Lower Congo Basin deepwater concessions | Short term (≤ 2 years) |

| Fiscal & regulatory reforms (ANPG set-up, tax cuts on marginal fields) | 0.3% | National, with highest uptake in mature blocks (0, 14, 15, 17) and marginal-field concessions | Medium term (2-4 years) |

| Exit from OPEC gives production-quota flexibility | 0.2% | National, enabling unconstrained export optimization across all producing blocks | Short term (≤ 2 years) |

| Non-associated gas push (Northern Gas Complex, Sanha LGC) monetises stranded reserves | 0.4% | National, concentrated in Block 15/06 (Quiluma, Maboqueiro) and Sanha fields, with downstream impact at Angola LNG Soyo | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Licensing-Round Momentum Attracting Super-Majors

ANPG’s 2025 limited tender covering ten offshore blocks and a year-round permanent offer platform together aim to award 50 blocks by 2026, channeling USD 60-70 billion of upstream spending before 2030.[1]Reuters Staff, “Angola Plans Multi-Year Licensing Rounds to Attract Super-Majors,” reuters.com Shell’s return via Block 33/24 and Chevron’s parallel entry validate the upgraded fiscal terms and condensed licensing timetable. The continuous-offer structure has replaced multi-year cycles, letting operators lodge unsolicited bids and close farm-ins quickly. ExxonMobil’s Arturus-1 wildcat in the Namibe basin illustrates early-stage interest in pre-salt reservoirs that could trigger multi-billion-dollar hubs if commercial. ReconAfrica’s 5.2 million-acre MoU in the Etosha-Okavango basin pushes frontier exploration inland, while Afentra’s Block 3/05 acquisition shows smaller independents can leverage leaner balance sheets under the new terms.

Deep- and Ultra-Deepwater FIDs Accelerating Near-Term Output

TotalEnergies sanctioned the USD 6 billion Kaminho project in 2024, targeting 70 000 bpd from 1,700-meter waters with first oil slated for 2028.[2]Agência Nacional de Petróleo Gás e Biocombustíveis, “Incremental Production Decree,” anpg.ao Saipem, Subsea 7, and Yinson finalized over USD 10 billion in linked EPCI and FPSO contracts, each integrating all-electric topsides that cut routine flaring to zero. Azule Energy beat schedule by four months when Agogo began flowing 120 000 bpd in July 2025, and Ndungu added 60 000 bpd in 2026, confirming that modular FPSO leasing can compress payback periods by about one year. The projects together inject roughly 250 000 bpd gross new capacity by 2028, offsetting legacy decline and stabilizing national output around 1.1 million bpd.

Fiscal and Regulatory Reforms Cut Taxes on Marginal Fields

The November 2024 Incremental Production Decree halved petroleum income tax under production-sharing agreements to 25% and lifted cost-recovery ceilings to 70%. Chevron’s South N’dola tie-back and TotalEnergies’ CLOV Phase 3 infill plan both clear internal-rate-of-return hurdles mainly because of that relief. Faster amortization of subsea capex also improves net present value for high-cost ultra-deepwater schemes such as Kaminho. Separating the regulator from Sonangol’s commercial arm has shortened contract-approval time from 18 months in 2020 to nine months in 2025, lowering pre-FID holding costs for operators.

Exit from OPEC Providing Production-Quota Flexibility

Angola’s January 2024 withdrawal from OPEC removed the 1.11 million bpd cap, letting exports touch 1.23 million bpd in August 2024 during high-price windows. Although geological decline persists, flexible scheduling allows incremental barrels from Agogo and Kaminho to flow without offsetting cuts. The policy particularly benefits back-loaded fiscal regimes because Brent backwardation favors earlier production; at 50 000 bpd extra throughput, the Treasury captures an estimated USD 200-400 million additional annual revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decline of mature deep-water fields | -0.8% | National, concentrated in Blocks 0, 14, 15, 17, 32 (Cabinda, Kizomba, Dalia, Pazflor, Kaombo fields) | Short term (≤ 2 years) |

| High capex / break-even for ultra-deep projects under price volatility | -0.5% | National, affecting ultra-deepwater blocks beyond 1,500m depth in Kwanza and Lower Congo basins | Medium term (2-4 years) |

| Persistent FX, debt-servicing and sovereign-risk pressures | -0.4% | National, with macroeconomic impact on all upstream investment decisions and dollar-denominated service contracts | Long term (≥ 4 years) |

| Limited high-resolution subsurface data for frontier onshore & pre-salt blocks | -0.2% | National, primarily affecting onshore Kwanza, Namibe, Benguela, Kassanje, and Etosha-Okavango basins | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline of Mature Deep-Water Fields

Natural decline runs 10-15% gross in Angola’s oldest clusters, trimmed to 6-8% once operators add water injection and gas lift.[3]International Monetary Fund, “Angola Economic Outlook 2025-2026,” imf.org ExxonMobil’s Kizomba assets are about 85% depleted, and TotalEnergies’ Kaombo is already 60% mature, forcing heavier infill drilling to stay on a plateau. License extensions to 2045 buy time, yet sustaining Block 17 above 250 000 bpd still demands USD 2-3 billion in enhanced-oil-recovery spend. Mandatory escrow funding for future decommissioning, introduced by Presidential Decree 91/18, also raises the holding cost of aging FPSOs.

High Capex and Break-Even for Ultra-Deep Projects Under Price Volatility

Ultra-deepwater schemes need Brent in the USD 60-70 range for 15% returns because per-barrel capital intensity exceeds USD 80 000 at Kaminho levels. Sovereign yields above 15% in 2025 inflame the cost of local financing, and an 11% kwanza slide in 2024 inflated imported equipment bills. Budget oil-price assumptions for 2026 sit at only USD 62.2, below the threshold required to trigger FIDs on the next wave of Blocks 29, 31, and 46, making timing highly price sensitive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Deepwater Dominance Anchors Offshore Share

Offshore activity captured 97.2% of 2025 revenue in the Angola oil & gas upstream market, while onshore is pacing growth at 2.9% CAGR through 2031. Deepwater reservoirs in the Kwanza and Lower Congo basins, lying 400-2 200 meters below sea level, sustain this dominance. Azule Energy’s Agogo FPSO and TotalEnergies’ Kaminho will together contribute about 190 000 bpd by 2028, and the existing infrastructure of 15 FPSOs with 1.5 million bpd capacity further entrenches offshore economics.

Onshore pilots in Namibe and Kwanza now benefit from the lower entry cost of tight-oil wells priced at USD 15-25 million. ExxonMobil’s Arturus-1 and ReconAfrica’s seismic campaign indicate potential to lift onshore to 5-7% of the Angola oil & gas upstream market size by 2031. Infrastructure gaps, such as the absence of a Kassanje-to-Lobito pipeline, still pose logistical hurdles that may temper the near-term ramp-up.

By Resource Type: Crude Oil Maturity Versus Gas Monetization

Crude oil supplied 90.3% of the 2025 value, yet gas is growing fastest at 6.6% CAGR.[4]Azule Energy, “Agogo FPSO First Oil Achievement,” azule-energy.com The Northern Gas Complex now funnels 400 MMscfd into Angola LNG, pushing plant utilization toward 75%. These flows could raise gas to 12-15% of the Angola oil & gas upstream market size by 2031.

Legacy oil reservoirs remain key, but new barrels from Kaminho, Agogo, and Ndungu will offset roughly 200 000 bpd of decline to keep net liquids output slightly positive. The flaring ban embedded in all-electric FPSOs also channels more associated gas into commercial streams, diversifying revenue amid decarbonization pressures.

By Well Type: Conventional Base Meets Unconventional Emergence

Conventional wells controlled 99.1% of 2025 activity, reflecting high-permeability deepwater sandstones that flow without stimulation. Infill programs on Block 15 and CLOV Phase 3 illustrate ongoing spend to maintain rates above 150 000 bpd.

Unconventional wells, chiefly tight-oil horizontals in onshore Kwanza, are projected to expand at 11.7% CAGR, lifting their share to as much as 5% by 2031. Lower per-well costs and faster paybacks attract independents, and successful pilots could raise unconventional representation within the Angola oil & gas upstream market share beyond today’s niche position.

By Service: Development Scale Versus Exploration Momentum

Development and production services generated 85.6% of 2025 revenue, embodying multi-billion-dollar FPSO programs such as Kaminho and Agogo. Saipem’s USD 3.7 billion EPCI award for Kaminho underscores the scale of ongoing construction.

Exploration services, growing 5.4% CAGR, are buoyed by shorter licensing cycles and frontier onshore seismic. TGS’s re-processing of 2 589 kilometers of legacy data in Kwanza illustrates opportunities to lower dry-hole risk and build sustained workloads for seismic and drilling contractors.

Geography Analysis

The Kwanza and Lower Congo basins together supply more than 95% of Angola’s current liquids. Kwanza’s ultra-deepwater Blocks 20/11 and 15/06 host Kaminho and Agogo, respectively, underpinning national growth forecasts. Lower Congo’s shallower Block 0 and Block 14 continue to provide base volumes despite high maturity.

Cabinda and Zaire provinces jointly account for roughly 70% of national throughput, signaling concentration risk if infrastructure outages occur. Provincial projects to expand Lobito port aim to de-bottle-neck logistics for emerging onshore ventures. The Soyo hub in Zaire now serves 12 FPSOs and the LNG plant, reinforcing its role as Angola’s offshore command center.

Frontier onshore zones, Namibe, Benguela, Kassanje, and the Etosha-Okavango extension, offer upside diversification. ExxonMobil’s Namibe wildcat and ReconAfrica’s acreage prove the geologic concept, though a lack of evacuation pipelines means early production will rely on trucking or rail until larger volumes justify midstream builds.

Competitive Landscape

Roughly 75% of Angola’s upstream capacity sits with the top five operators, TotalEnergies, Azule Energy, ExxonMobil, Chevron, and Eni, yet newer independents are carving niches in marginal and onshore blocks. Super-majors are extending asset life by upgrading FPSOs and adopting subsea boosting, while Azule’s project delivery ahead of schedule highlights integrated execution strengths.

Yinson’s fully electric FPSO design for Agogo reduces operating expenditure by up to 20%, setting a new cost-benchmark for charters. Schlumberger’s subsea processing pilots on Block 17 aim to stretch plateau performance by an extra three-to-five years. Service-company alliances such as Subsea 7-TechnipFMC’s Forsys Subsea bundle are gaining traction among independents that prefer turnkey solutions.

Mandatory decommissioning escrow rules favor operators with strong balance sheets, but tax cuts on marginal barrels have improved asset-handover economics, allowing firms like Afentra and BW Energy to extract residual value from clusters considered non-core by majors.

Angola Oil And Gas Upstream Industry Leaders

ExxonMobil Corporation

TotalEnergies SE

Eni SpA

BP Plc

Chevron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Azule Energy confirmed the Algaita-01 discovery in Block 15/06, adding around 500 million barrels in place within tie-back distance of the Olombendo FPSO.

- February 2026: Ndungu began flowing 60 000 bpd, completing the Agogo Integrated West Hub’s ramp-up.

- November 2025: The Northern Gas Complex was officially inaugurated six months ahead of plan.

- September 2025: Shell and Chevron signed exploration agreements for Block 33/24, marking Shell’s Angola return.

Angola Oil And Gas Upstream Market Report Scope

The oil and gas upstream market encompasses the exploration and production (E&P) segment of the petroleum industry. This includes activities such as locating, drilling, and extracting crude oil and natural gas from underground or underwater reservoirs.

The Angola oil and gas upstream market is segmented into location of deployment, resource type, well type, and service. By location of deployment, the market is segmented into onshore and offshore. By resource type, the market is divided into crude oil and natural gas. By well type, the market is segmented into conventional and unconventional. By service, the market is divided into exploration, development, production, and decommissioning. The market sizes and forecasts are provided in terms of value (USD billion).

By Location of Deployment

| Onshore |

| Offshore |

By Resource Type

| Crude Oil |

| Natural Gas |

By Well Type

| Conventional |

| Unconventional |

By Service

| Exploration |

| Development and Production |

| Decommissioning |

| By Location of Deployment | Onshore |

| Offshore | |

| By Resource Type | Crude Oil |

| Natural Gas | |

| By Well Type | Conventional |

| Unconventional | |

| By Service | Exploration |

| Development and Production | |

| Decommissioning |

Key Questions Answered in the Report

What is the 2026 value of Angola's upstream sector?

The Angola oil and gas upstream market is valued at USD 4.71 billion in 2026.

How fast will national upstream revenue grow to 2031?

Revenue is projected to reach USD 5.22 billion by 2031, reflecting a 2.06% CAGR over 2026-2031.

Which resource shows the highest growth?

Natural gas leads with a 6.6% CAGR as the Northern Gas Complex feeds Angola LNG.

Why are onshore blocks drawing attention now?

Lower drilling costs and favorable fiscal terms make tight-oil plays in the Kwanza basin attractive to independents.

How did exiting OPEC affect production?

The move removed quota limits, letting exports rise to 1.23 million bpd in 2024 during favorable price windows.

Which upcoming project will add the most new oil?

TotalEnergies' Kaminho project targets 70,000 bpd from 2028 and anchors ultra-deepwater growth.

Page last updated on: