Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

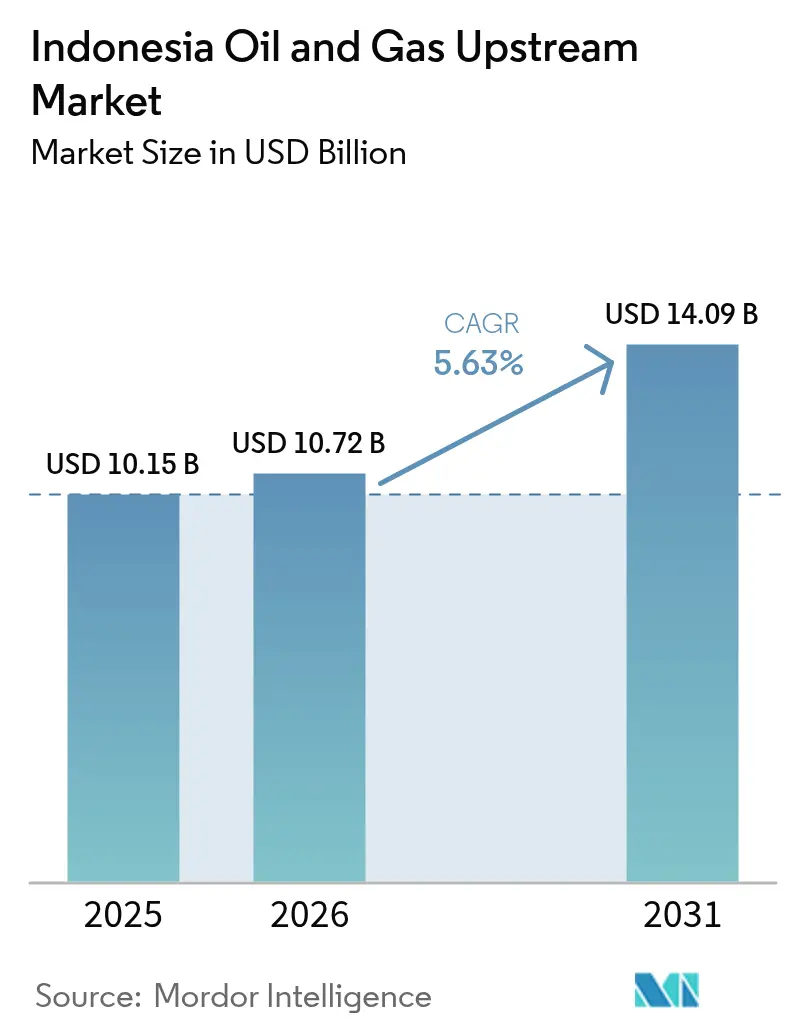

| Base Year Market Size (2025) | USD 10.15 Billion |

| Market Size (2026) | USD 10.72 Billion |

| Market Size (2031) | USD 14.09 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

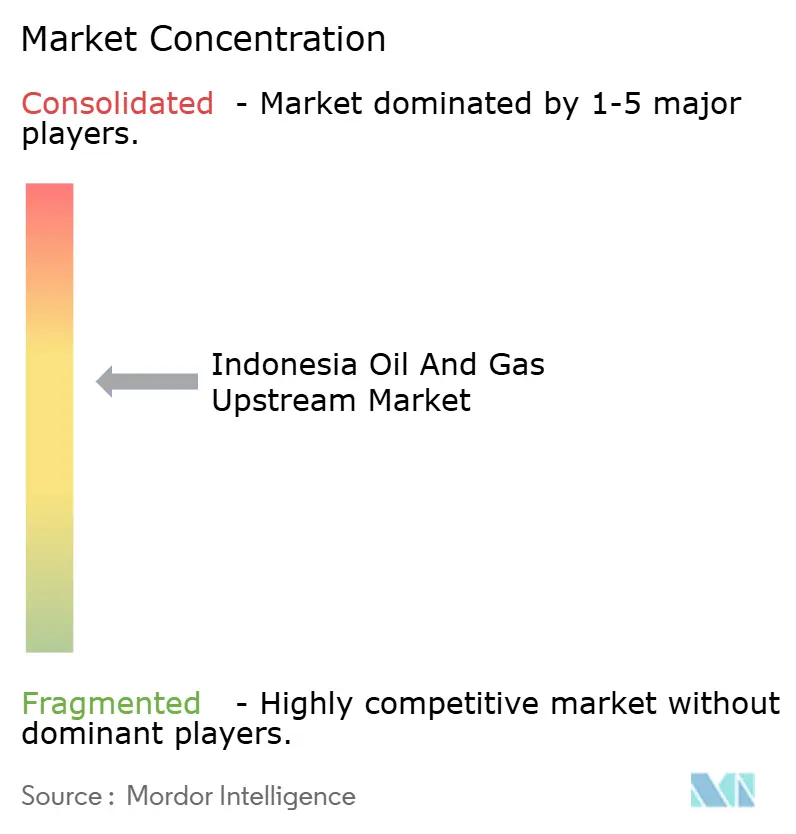

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Oil And Gas Upstream Market Analysis by Mordor Intelligence

The Indonesia Oil And Gas Upstream Market size is expected to grow from USD 10.15 billion in 2025 to USD 10.72 billion in 2026 and is forecast to reach USD 14.09 billion by 2031 at 5.63% CAGR over 2026-2031.

Deep-water gas discoveries, flexible gross-split fiscal terms, and accelerating digitalization collectively strengthen the outlook for growth. Offshore activities capture capital as operators prioritize high-impact prospects in the Abadi and Andaman blocks, while LNG price linkages continue to underpin revenue. The Indonesian oil & gas upstream market benefits from robust domestic demand and expanding export capacity, yet faces structural decline at mature onshore fields that require enhanced recovery investments. Technology adoption—from AI-guided seismic interpretation to real-time production analytics—reduces non-productive time and enhances safety, ensuring that efficiency gains help offset aging asset pressures. Moderate market concentration, anchored by Pertamina’s 24% share, supports competitive capital deployment without inhibiting new entrants that target unconventional and deep-water plays.

Key Report Takeaways

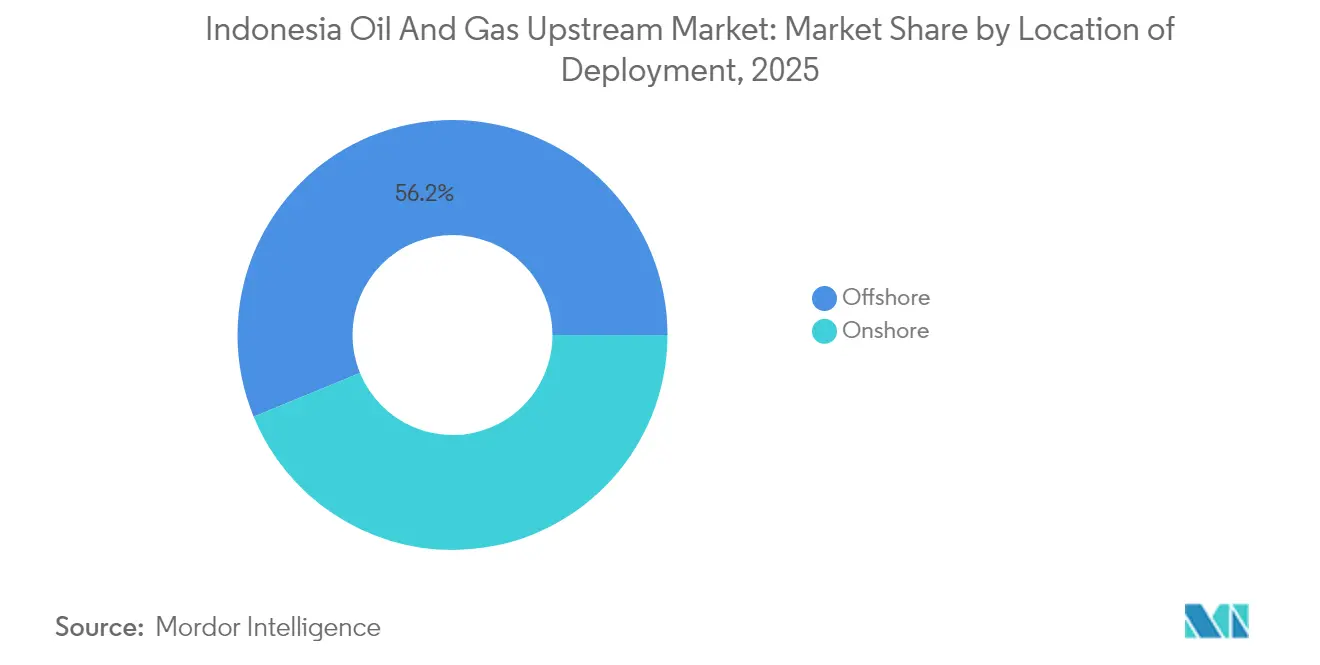

- By location of deployment, offshore operations led with a 56.20% revenue share in 2025; onshore operations are forecast to deliver the fastest growth, with a 6.14% CAGR through 2031.

- By resource type, crude oil commanded 52.35% of the Indonesian oil & gas upstream market share in 2025, while natural gas is projected to expand at a 6.05% CAGR to 2031.

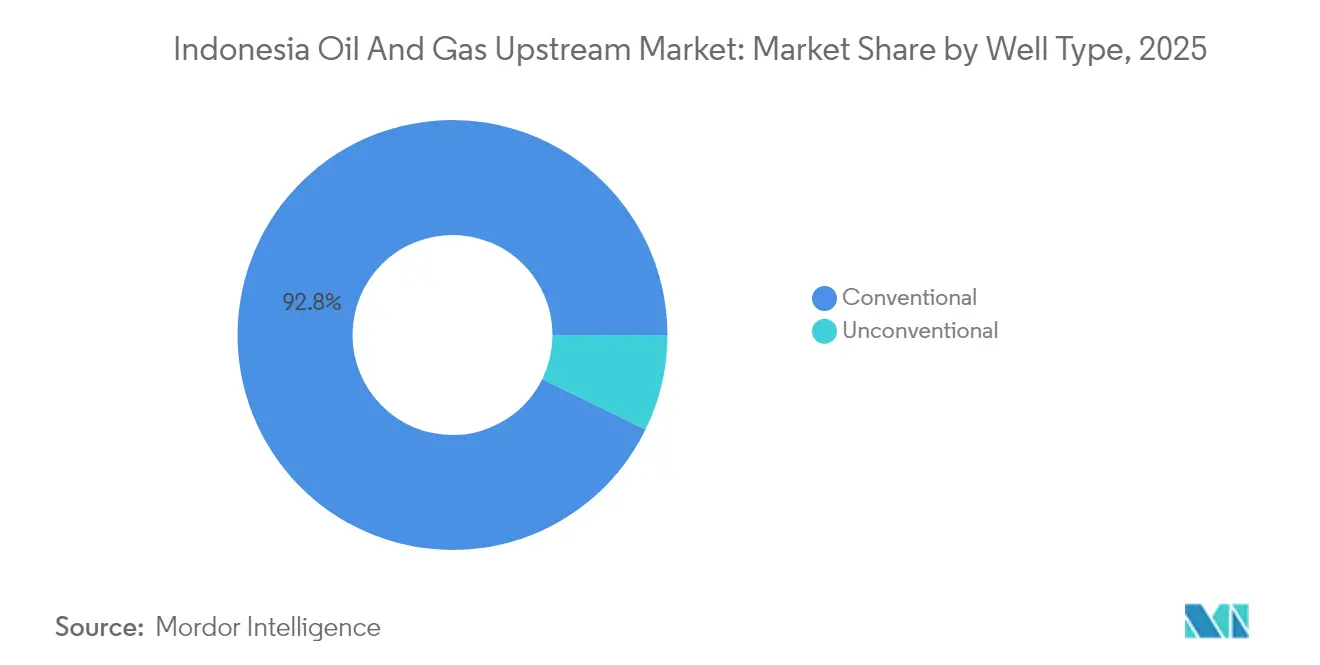

- By well type, conventional drilling accounted for a 92.75% share of the Indonesian oil & gas upstream market size in 2025 and is expected to advance at a 5.22% CAGR through 2031.

- By service, development and production services captured a 64.10% revenue share in 2025; decommissioning is projected to have the highest 7.74% CAGR between 2026 and 2031.

- Pertamina, ExxonMobil, Chevron, and TotalEnergies jointly held approximately 58% of 2024 production, reflecting a moderate level of concentration that preserves room for independent entrants.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Oil And Gas Upstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiscal & licensing reform (GR 35/2004 revisions) | 1.20% | National, with concentrated benefits in North Sumatra, East Kalimantan | Medium term (2-4 years) |

| Deep-water gas discoveries (Abadi, Andaman) | 1.80% | Offshore Maluku, North Sumatra, East Kalimantan | Long term (≥ 4 years) |

| LNG export price-linkage upside | 0.90% | National, with primary impact in Bontang, Tangguh export hubs | Short term (≤ 2 years) |

| Production-sharing contract (PSC) extensions | 0.70% | National, concentrated in mature producing basins | Medium term (2-4 years) |

| CCS-EOR hubs enabling tertiary recovery | 0.60% | Java, South Sumatra, East Kalimantan mature fields | Long term (≥ 4 years) |

| AI-led subsurface imaging accuracy | 0.40% | National, early adoption in Pertamina Hulu Rokan operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fiscal & Licensing Reform Accelerates Investment Flows

Revisions to Government Regulation 35/2004 introduce a selectable gross-split regime that awards contractors up to a 95% revenue share for unconventional projects, thereby improving the net present value and shortening the payback period. Operators now switch between cost-recovery and gross-split frameworks to match project risk, an option that has already attracted joint studies from Eni, Harbour Energy, ExxonMobil, and BP. The regulatory update directly addresses earlier investor concerns about fiscal rigidity and stimulates license uptake in frontier acreage, particularly in deep-water tracts where risk-weighted economics favor higher contractor shares. Concurrently, streamlined permitting under MEMR Regulation 13/2024 reduces license approval time from 24 months to 12 months, enabling faster exploration cycles.

Deep-Water Gas Discoveries Reshape Resource Portfolio

The Layaran-1 find in South Andaman validated a 6 TCF resource base and 30 MMSCFD test flow, while the Timpan-1 well holds 5-6 TCF and 27 MMSCFD output potential.[1]Reporting Team, “South Andaman Discovery Adds 6 TCF Gas,” Business-Indonesia, business-indonesia.id Alongside Eni's 5 TCF North Ganal discovery, Indonesia's proven reserves increased by roughly 30%, contingent upon appraisal.[2]Source: Research Unit, “Indonesia Deep-Water Round-Up 2025,” GBR, gbreports.com SKK Migas schedules the first gas between 2028 and 2030, necessitating subsea pipelines and floating LNG storage that anchor a new export corridor. INPEX's Abadi LNG, which completed FEED in 2024, targets 9.5 MTPA and USD 20 billion capex, reinforcing Indonesia's oil & gas upstream market leadership in regional LNG supply.

AI-Led Subsurface Imaging Transforms Operational Efficiency

Pertamina Hulu Rokan reduced candidate well identification time to one day by utilizing machine-learning-driven seismic analytics—an 86% efficiency increase that accelerates rig scheduling and reserve replacement. The SOPPRED model reduced non-productive rig hours from 82 to 12 and saved 30,000 liters of diesel per well by anticipating gumai shale hazards. Cloud-based AI services from Indosat Ooredoo Hutchinson deliver high-resolution wave measurements that can increase production by 10% and reduce potential fatal injuries by 95%. Such gains lower lifting costs, extend economic field life, and strengthen the Indonesian oil & gas upstream market against price volatility.

CCS-EOR Hubs Enable Tertiary Recovery Potential

Indonesia holds 572 gigatons of CO₂ storage capacity in saline aquifers and 4.85 gigatons in depleted reservoirs, positioning CCS as both an emissions solution and a recovery enabler. Pertamina identified 950 million STB of EOR potential across 12 projects, utilizing its proprietary surfactant, PHR-24, which proved commercially viable in mature Sumatran fields. The Tangguh CCS facility—Southeast Asia’s largest—anchors a network approach that enables high-CO₂ gas fields to move forward, while China-Indonesia technology cooperation accelerates the deployment of tertiary recovery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging onshore mature fields | -1.40% | Central Sumatra, South Sumatra, East Java onshore basins | Medium term (2-4 years) |

| Regulatory & contract uncertainty | -0.80% | National, affecting new exploration licensing rounds | Short term (≤ 2 years) |

| Deep-water talent gap | -0.50% | Offshore East Kalimantan, Maluku, North Sumatra | Long term (≥ 4 years) |

| ESG-driven capital scarcity | -0.70% | National, with heightened impact on new offshore projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Onshore Mature Fields Constrain Production Growth

Roughly 70% of Indonesia’s 44,985 oil wells are mature, declining at a rate of 21% annually, and leaving 16,990 idle sites that require workovers or permanent abandonment (P&A) decisions. The heavy oil dominance in Central Sumatra’s Duri and Rantau Bais fields, with API gravities below 25°, increases thermal and chemical EOR costs. Reactivation programs target 4,500 wells but face economic hurdles without further fiscal sweeteners. Consequently, sustaining base output diverts capital expenditures from exploration, moderating the growth curve of the Indonesian oil & gas upstream market.

ESG-Driven Capital Scarcity Pressures Project Financing

Domestic banks allocate only 1-3% of green portfolios to renewables, yet impose stricter ESG lending filters on hydrocarbons, requiring ISO 14001 compliance and SKUP certification.[3]Analysis Team, “Banks Tighten ESG Lending for Hydrocarbons,” Indonesia Business Post, indonesiabusinesspost.com Pertamina’s 2024 Sustainable Finance Framework secured ISS validation, opening up hybrid green-transition funding; however, the firm still drew USD 2.5 billion in short-term conventional loans during market uncertainty. Stricter ESG scrutiny raises the cost of capital and can delay frontier developments, particularly those with higher carbon dioxide (CO₂) content.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Offshore Momentum Sustains Growth

Offshore assets accounted for 56.20% of 2025 revenue and are expected to advance at a 5.88% CAGR, increasing the Indonesian oil & gas upstream market size for offshore assets to USD 8.01 billion by 2031. Massive gas clusters in Andaman and Masela underpin long-cycle cash flows, while brownfield subsea tie-backs around Mahakam preserve volume stability. Operators cite shorter sanction-to-first-gas timelines for jack-up re-entries, and flexible fiscal terms improve project IRR to double-digits under USD 65/bbl scenarios.

Onshore output trails, constrained by mature reservoirs but buffered by lower development costs and proximity to infrastructure. AI-aided workovers at Rokan achieved 152,161 bpd in June 2025, demonstrating that digital optimization can help narrow productivity gaps. Still, heavy crude viscosity and water-cut issues inflate lifting cost to USD 22/bbl versus offshore’s USD 16/bbl. The government’s aim to revive 4,500 idle wells should slow the decline; yet, offshore remains the main growth engine for the Indonesian oil & gas upstream market.

By Resource Type: Gas Ascendance Challenges Oil Supremacy

Crude oil held a 52.35% share in 2025, translating to USD 5.31 billion of the Indonesian oil & gas upstream market size, but expands modestly at a 3.95% CAGR as mature fields dominate the slate. Gas, in contrast, is expected to reach a 46.40% share by 2031, driven by a 6.05% CAGR, backed by startup schedules from Layaran, Timpan, and Abadi. Price-indexed LNG contracts enhance project netbacks when Asian spot prices trend above USD 16/MMBtu, attracting capital expenditure even amid debates about the energy transition.

Elevated CO₂ in Natuna D-Alpha kept bids away, underscoring the need for CCS to unlock mega-gas. Meanwhile, domestic gasification programs accelerate demand from fertilizers and power plants, ensuring offtake security. Collectively, the growth of natural gas materially reshapes the revenue mix within the Indonesian oil & gas upstream market.

By Well Type: Conventional Base Dominates, Unconventional Outlook Brightens

Conventional wells account for a 92.75% share, equivalent to USD 9.41 billion in 2025 revenue, and sustain a 5.22% CAGR through drilling campaigns that have doubled to 40 wells in 2024. This segment anchors near-term cash flow and underpins the Indonesia oil & gas upstream market share advantage for established operators.

Unconventional opportunities post the Gulamo DET-1 find are projected to achieve an 8.42% CAGR, targeting 233 TCF of shale potential across Sumatra. MEMR’s 95% gross-split for shale projects cuts break-even to USD 55/bbl oil equivalent, but hydraulic fracturing supply chains are nascent. Success hinges on technology alliances with North American specialists and water-management best practices, stages that could unlock a multi-billion-dollar upside for the Indonesian oil & gas upstream market.

By Service: Development & Production Lead, Decommissioning Accelerates

Development and production services captured 64.10% of 2025 spend, mirroring operators’ priority on short-cycle output and lifting cost reductions. Robotic process automation at PT Patra Drilling cut invoicing lag by 30 days and improved crew safety, proving digital ROI. The Indonesian oil & gas upstream market size for this service line is forecast to cross USD 9.26 billion by 2031.

Decommissioning services, although with a 4.68% share in 2025, are expected to surge at an 7.74% CAGR as 630 offshore platforms reach the end of their 40-year life. Government guidelines now require abandonment cost provisions in PSCs, spurring early engagement of specialized contractors. Exploration services maintain a stable 5.42% CAGR, driven by annual block auctions and 3D seismic commitments in the Andaman region.

Geography Analysis

East Kalimantan supplied 37.45% of national LNG in 2025 via the Bontang facility, validating the region’s infrastructure depth and export connectivity to Japan, South Korea, and China. Mahakam’s brownfield compression projects sustain plateau, while subsea tie-backs from North Ganal add incremental throughput. Planned CCS in the region further extends asset life and addresses shifts in carbon policy.

Central Sumatra remained Indonesia’s second-largest oil hub at 152,161 bpd in June 2025, driven by Rokan steam-flood optimization. Heavy-oil viscosity and high water-cut demand chemical EOR, which elevates unit costs but also yields upside through enhanced recovery factors. South Sumatra complements established pipeline networks feeding domestic refineries and power plants, anchoring demand certainty that underpins continuing infill drilling.

North Sumatra–Andaman and offshore Maluku mark Indonesia’s frontier axis. Layaran-1’s 6 TCF discovery and Abadi’s 9.5 MTPA LNG plan attract global capital, yet deep-water skills gaps and subsea infrastructure requirements prolong timelines. Still, the cumulative resource base positions these provinces as the future growth pole for the Indonesian oil & gas upstream market, shifting the production center of gravity eastward by the next decade.

Competitive Landscape

Pertamina controlled 24% of the 2024 upstream revenue, producing 69% of the nation's oil and 34% of its gas, leveraging integrated logistics and preferential acreage access. ExxonMobil Cepu remained the single largest field operator at 152,330 bpd, evidencing continued international relevance. Overall, the Indonesian oil & gas upstream market balances state participation with foreign expertise, fostering a moderately concentrated, innovation-oriented ecosystem.

Strategic alliances define recent moves. Eni and Petronas formed a joint venture targeting 3 billion barrels of oil equivalent (boe) of reserves and a 500,000 barrels of oil equivalent per day (boe/d) plateau, utilizing cash-flowing assets to fund exploration. Medco Energi's acquisition of Siak and Kampar blocks added 3,000 bpd and underscored consolidation trends among independents. Operators differentiate themselves by technology; AI rollouts, which claim 10% productivity gains and a 95% reduction in safety risks, present a competitive edge.

White-space opportunities surface in unconventional shale, deep-water floaters, and CCS hubs backed by 572 gigatons of storage headroom. Firms mastering these niches should capture above-average returns as Indonesia's oil & gas upstream market growth pivots from brownfield optimization to frontier monetization.

Indonesia Oil And Gas Upstream Industry Leaders

Chevron Corporation

Exxon Mobil Corp

PT Pertamina Persero

BP plc

INPEX Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Supermajor BP is in the market for vessels to support rig movements for its Tangguh UCC project in Indonesia, which is the next phase of its Tangguh liquefied natural gas project in the country's Papua Barat (West Papua) province.

- August 2025: Japan’s Inpex began FEED work for the Abadi LNG project in Indonesia, operated by INPEX Masela. The project includes an onshore LNG plant, an FPSO, SURF facilities, and a gas export pipeline, with major contracts already awarded.

- July 2025: Indonesia Energy announced plans to drill two new wells on the Kruh block before the end of the year, following a 60% increase in proven reserves from recent seismic surveys.

- October 2024: PT Energi Mega Persada (ENRG), a Bakrie Group-affiliated company, has officially acquired all participating rights in the Sengkang oil and gas block.

Indonesia Oil And Gas Upstream Market Report Scope

The Indonesian oil and gas upstream market report includes:

By Location of Deployment

| Onshore |

| Offshore |

By Resource Type

| Crude Oil |

| Natural Gas |

By Well Type

| Conventional |

| Unconventional |

By Service

| Exploration |

| Development and Production |

| Decomissioning |

| By Location of Deployment | Onshore |

| Offshore | |

| By Resource Type | Crude Oil |

| Natural Gas | |

| By Well Type | Conventional |

| Unconventional | |

| By Service | Exploration |

| Development and Production | |

| Decomissioning |

Key Questions Answered in the Report

What is the current value of the Indonesia oil & gas upstream market?

It was USD 10.72 billion in 2026 and is projected to hit USD 14.09 billion by 2031.

How fast is upstream spending growing in Indonesia?

The sector is forecast to post a 5.63% CAGR between 2026-2031, driven by offshore gas and digital efficiency gains.

Which segment leads upstream activities?

Development and production services hold 64.10% of spending, reflecting a focus on maximizing existing assets.

Where are the largest new gas finds located?

Deep-water South Andaman, North Ganal, and Masela blocks collectively add more than 15 TCF of gas resources.

How is technology improving field economics?

AI-guided seismic imaging and real-time analytics cut well identification time by 86% and reduce non-productive rig hours.

What role does CCS play in Indonesia?

With 572 gigatons storage capacity, CCS supports enhanced oil recovery and enables development of high-CO? gas fields.

Page last updated on: