Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

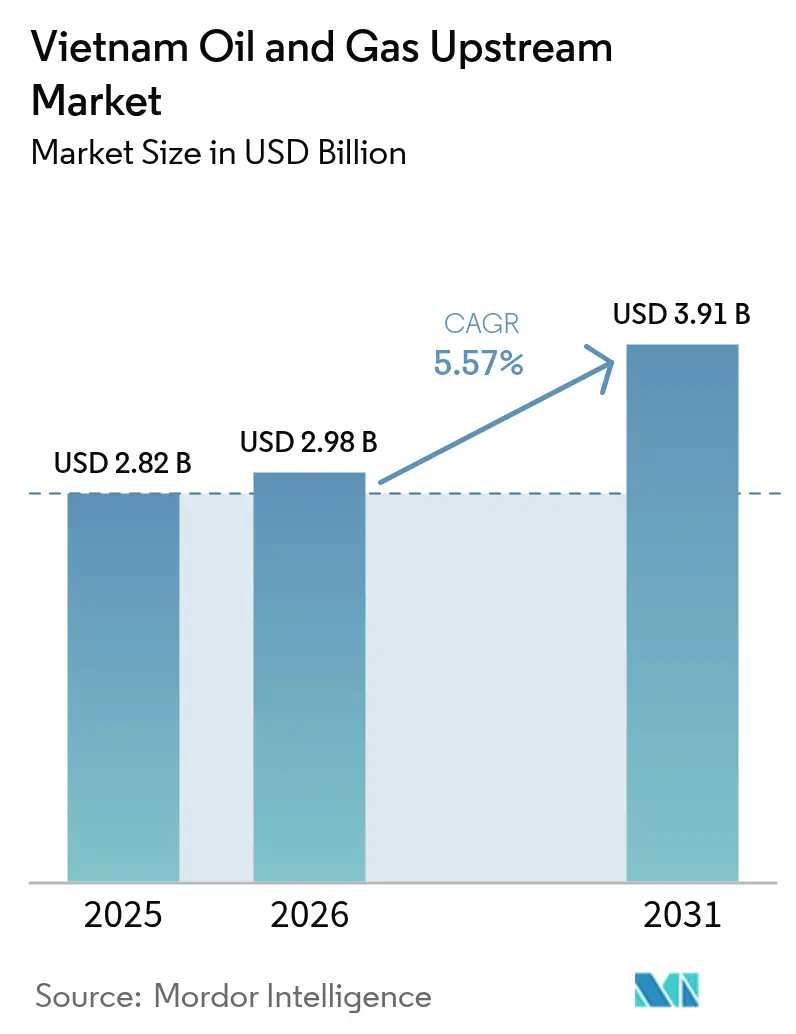

| Base Year Market Size (2025) | USD 2.82 Billion |

| Market Size (2026) | USD 2.98 Billion |

| Market Size (2031) | USD 3.91 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Oil And Gas Upstream Market Analysis by Mordor Intelligence

The Vietnam Oil And Gas Upstream Market size was valued at USD 2.82 billion in 2025 and estimated to grow from USD 2.98 billion in 2026 to reach USD 3.91 billion by 2031, at a CAGR of 5.57% during the forecast period (2026-2031).

The uptrend reflects Vietnam’s deliberate pivot from high-risk exploration to integrated project development, which maximizes recovery from proven reservoirs, utilizes digital subsurface imaging, and links offshore gas output to captive power demand. Operators are concentrating capital on technically demanding deep-water acreage while streamlining onshore portfolios that suffer from reservoir decline and urban encroachment. Strong domestic gas demand, export-credit-agency funding, and supportive fiscal terms are reshaping investment decisions even as South China Sea tensions and protracted permitting processes elevate execution risk. In response, PetroVietnam has lifted 2025 capital outlays by 67%, accelerated artificial-intelligence-guided seismic interpretation, and partnered with international majors to derisk complex subsea work scopes.[1]Soha, “PV Drilling Raises 2025 Capex,” soha.vn

Key Report Takeaways

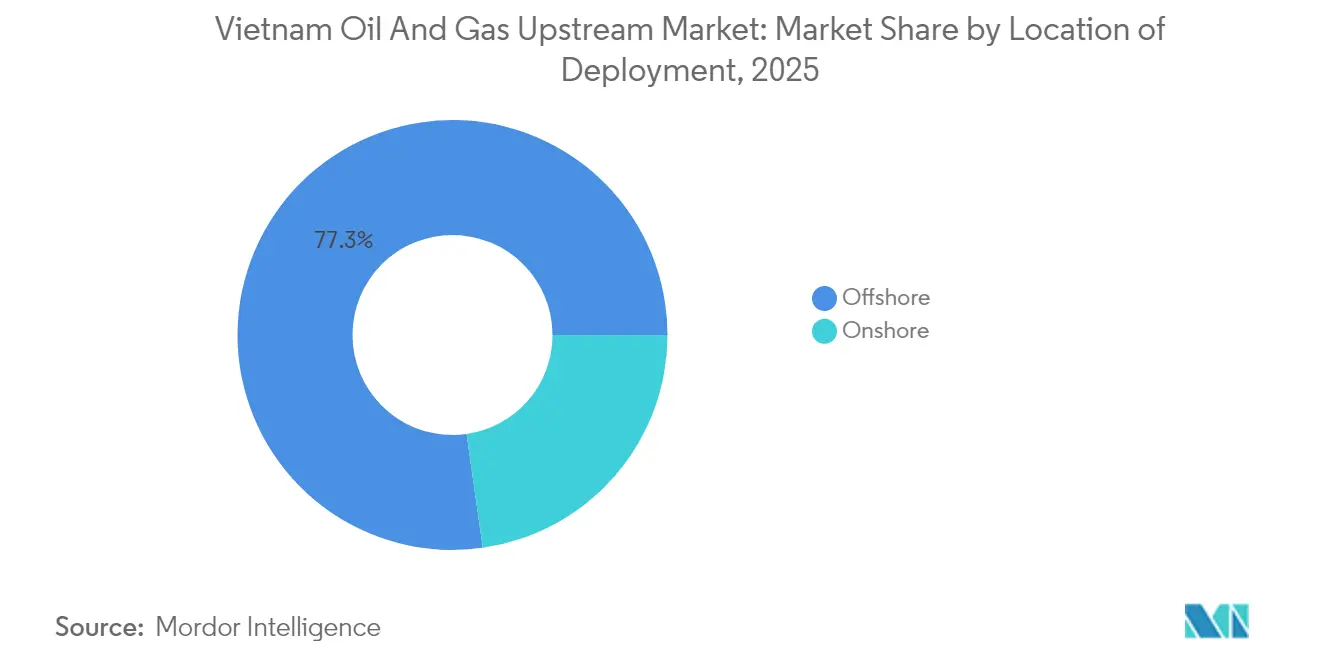

- By location, offshore deployments accounted for 77.25% of the Vietnam oil and gas upstream market share in 2025 and are projected to advance at a 5.84% CAGR through 2031.

- By resource type, natural gas accounted for 59.65% of the Vietnam oil and gas upstream market size in 2025 and is forecast to expand at a 6.02% CAGR through 2031.

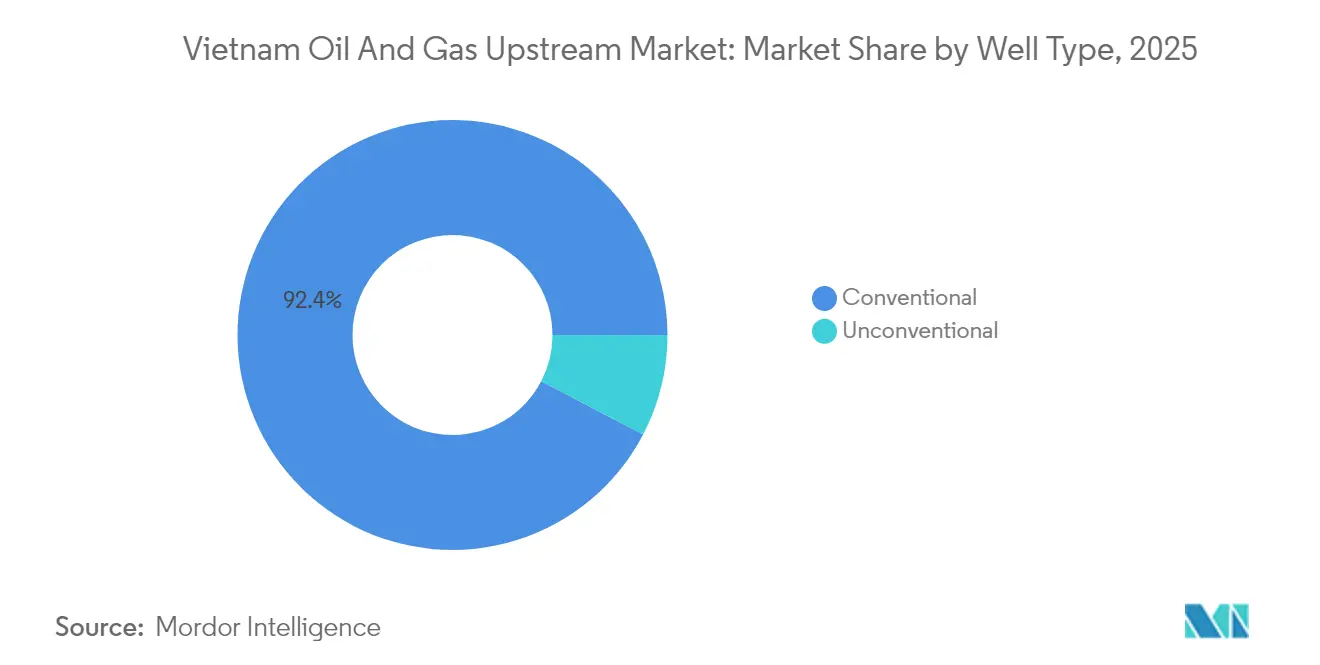

- By well type, conventional wells held 92.35% of 2025 output, while unconventional completions are poised for the fastest 6.69% CAGR between 2026 and 2031.

- By service, development and production activities generated 64.85% of 2025 revenue, whereas exploration services led growth at a 6.29% CAGR through 2031.

- PetroVietnam, ExxonMobil, TotalEnergies, and Jadestone Energy collectively accounted for approximately 42% of national production in 2024, indicating a moderately concentrated market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Oil And Gas Upstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing crude oil prices | +1.2% | Global, with concentrated impact on offshore Vietnam blocks | Short term (≤ 2 years) |

| Rising domestic gas demand for power | +1.8% | National, with primary demand centers in Ho Chi Minh City and Hanoi regions | Medium term (2-4 years) |

| New PSC licensing rounds | +0.9% | National, with focus on underexplored Song Hong and Phu Khanh basins | Long term (≥ 4 years) |

| Digital subsurface imaging adoption | +0.6% | National, with early adoption in mature Cuu Long Basin fields | Medium term (2-4 years) |

| Incentives for marginal gas fields | +0.4% | National, targeting previously uneconomic discoveries | Long term (≥ 4 years) |

| Export-credit agency funding for deep-water projects | +0.7% | National, concentrated on major offshore developments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Crude Oil Prices

Brent stability above USD 70 per barrel underpins the redevelopment of mature offshore fields, once hampered by high lifting costs. Operators now sanction enhanced-oil-recovery pilots in fractured reservoirs and justify long-reach sidetracks that increase incremental output without requiring new green-field infrastructure. PetroVietnam’s 2025 investment surge underscores renewed confidence in project economics, yet price support alone cannot counterbalance geological depletion. The Vietnam oil and gas upstream market, therefore, relies on both cost discipline and technology adoption to sustain margins.

Rising Domestic Gas Demand for Power

Electricity consumption is growing at an annual rate of 8%, and government policy mandates the retirement of coal between 2030 and 2040, creating an assured outlet for offshore gas. Decree 100/2025 compels power developers to source domestic gas under long-term contracts, stabilizing cash flows for upstream investors.[2]xaydungchinhsach.chinhphu.vn, “Decree 100/2025 on Gas-Fired Power,” chinhphu.vn Integrated projects, such as Ca Voi Xanh, exemplify the shift, pairing 3 GW of capacity with dedicated subsea supply and reducing LNG import exposure. The Vietnam oil and gas upstream market, therefore, aligns increasingly with downstream power strategies.

New PSC Licensing Rounds

Block 15-1 and other newly tendered tracts show Hanoi’s intent to maintain exploration momentum in frontier basins rich in pre-Tertiary plays. Fiscal incentives balance foreign participation with local content, while accelerated commercialization clauses shrink payback windows. Extensions for mature assets, such as TGT and CNV, confirm regulatory pragmatism in maximizing national take from legacy reservoirs. Such moves underpin long-term reserve renewal in the Vietnam oil and gas upstream market.

Digital Subsurface Imaging Adoption

Artificial-intelligence-assisted seismic inversion now achieves 80% accuracy in predicting fractured granite, slashing the odds of dry holes. Look-ahead VSP techniques cut depth uncertainty to 7 meters, a decisive margin in thin carbonate targets.[3]OnePetro, “Axial Oscillation Drilling Success in Vietnam,” onepetro.org Early adopters report double-digit drilling-time savings, positioning digital capacity as a critical differentiator across the Vietnam oil and gas upstream industry.

Restraints Impact Analysis*

| estraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex permitting and bureaucracy | -0.6% | National, with particular impact on new project approvals | Short term (≤ 2 years) |

| South China Sea territorial disputes | -0.9% | Offshore blocks in disputed waters, primarily eastern and southern areas | Long term (≥ 4 years) |

| Skilled labor shortages offshore | -0.4% | National offshore operations, with acute impact on drilling and production | Medium term (2-4 years) |

| ESG-driven financing constraints | -0.3% | Global, affecting international investment and financing decisions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Permitting and Bureaucracy

Multi-agency approvals can stretch final-investment-decision timelines by more than a year, inflating overhead on marginal prospects.[4]VietnamPlus, “Regulatory Bottlenecks Slow Investment,” vietnamplus.vn High compliance costs weigh heavily on smaller operators in the Vietnam oil and gas upstream market, prompting some to defer projects or seek alliances that share regulatory engagement burdens.

South China Sea Territorial Disputes

Cable-cutting and survey-vessel harassment episodes compel companies to factor geopolitical risk into their insurance and financing models. Certain majors have relinquished contested blocks to avoid diplomatic friction, curbing exploration breadth and leaving resource potential untapped.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Offshore Supremacy Drives Market Evolution

Offshore developments generated 77.25% of 2025 revenue and are expected to post a 5.84% CAGR through 2031, underscoring their centrality to the Vietnam oil and gas upstream market. The depths of 50–200 meters in Nam Con Son and Cuu Long host the bulk of the remaining reserves, requiring higher-specification rigs, subsea tie-backs, and floating processing units. Record 3-km horizontal sections drilled with axial-oscillation tools demonstrate how innovation offsets basement hardness.

Growth relies on integrated gas hubs connected to shore-based power plants, which monetize output through first oil capacity payments rather than volatile commodity pricing. First-oil at Dai Hung Phase 3—flowing 6,000 bpd ahead of schedule—illustrates project-management maturation and validates shared-infrastructure models that suppress unit costs. Even so, crew shortages and weather downtime complicate schedules, demanding robust contingency planning across the Vietnam oil and gas upstream industry.

Onshore acreage, constrained by urban expansion and the decline of mature fields, contributes modest and stable volumes but attracts limited new capital. Operators favor low-cost workovers and water-alternating-gas schemes to sustain plateaus; yet, the resource upside remains marginal compared to offshore prospects. Thus, offshore execution excellence will continue to determine value creation within the Vietnam oil and gas upstream market.

By Resource Type: Natural Gas Transformation Reshapes Industry Dynamics

Natural gas accounted for 59.65% of 2025 revenue and is forecast to grow at a 6.02% CAGR, solidifying its dominance in the Vietnam oil and gas upstream market. Output is slated to increase from 8 bcm in 2025 to more than 20 bcm by 2034, as Ca Voi Xanh, Block B, and Nam Du/U Minh ramp up production. Gas sale agreements featuring 80 mmcfd take-or-pay terms ensure predictable cash flows and facilitate project financing.

Crude oil, although still essential for refinery feedstock, is facing a gradual decline due to reservoir depletion and limited success in discoveries. Condensate streams linked to gas developments provide high-value naphtha for the petrochemical industry, partly offsetting oil volume erosion. The Vietnam oil and gas upstream industry is increasingly rewarding operators capable of orchestrating entire gas value chains, from subsea wellheads to power-plant burner tips.

By Well Type: Conventional Dominance with Unconventional Emergence

Conventional completions accounted for 92.35% of 2025 production, mirroring Vietnam’s structural-trap geology. Nonetheless, unconventional and enhanced-recovery projects are growing at a 6.69% CAGR as horizontal drilling, multi-stage fracturing, and polymer flooding unlock tight carbonates and attic oil. Pilot re-fracs in vintage Cuu Long wells have lifted recovery factors by 3–5 percentage points, signaling a meaningful additive stream for the Vietnam oil gas upstream market.

Scaling unconventional success will hinge on cost reductions, data analytics for high-grade candidates, and regulatory clarity on hydraulic-fracturing chemicals. As service providers accumulate experience, learning-curve benefits could accelerate adoption, diversifying the production base beyond traditional structures.

By Service: Development Focus with Exploration Growth

Development and production offerings generated 64.85% of market revenue in 2025, reflecting operators’ priority on maximizing output from sanctioned fields through digital well surveillance, artificial-lift optimization, and facility debottlenecking. Ten-year integrated-service contracts provide vendors with visibility to invest in specialized equipment suited to Vietnam’s metocean conditions.

Exploration service spending is expanding at a 6.29% CAGR as frontier seismic surveys and slim-hole appraisal wells target pre-Tertiary prospects in Phu Khanh and the deep Song Hong. Operators deploy multi-attribute AI workflows to tighten prospect ranking and cut dry-hole exposure. Decommissioning, although nascent, is poised to scale after 2030, when first-generation platforms reach their economic end-of-life, potentially opening a new revenue stream within the Vietnam oil and gas upstream market.

Geography Analysis

The Nam Con Son Basin accounted for 37.65% of the nation's hydrocarbon output in 2025, primarily driven by Dai Hung, Block B, and associated gas pipelines that supply power plants near Ho Chi Minh City. Cuu Long followed with 27.15%, where water-flood optimization and sidetrack drilling mitigate natural decline. Song Hong and Phu Khanh rank as high-risk, high-reward frontiers—initial 3-D surveys reveal promising carbonate buildups but also deep-water challenges.

Operators prefer areas firmly inside Vietnam's exclusive economic zone to minimize diplomatic friction. Blocks overlapping China's nine-dash line remain underexplored despite large gas shows because insurers and lenders demand punitive premiums. Joint development dialogues with Thailand in the Gulf of Thailand suggest pragmatic resource-sharing avenues that could replicate the successes of the mid-2020s between Malaysia and Thailand. Infrastructure dictates project timing: developers favor tie-backs to the Nam Con Son trunk line to curtail capex and accelerate first gas. Environmental permitting for new shore approaches is more stringent near tourism corridors, such as Nha Trang, steering pipeline landfalls toward industrial clusters. Cyclones north of Da Nang necessitate heavier FPSO moorings and evacuation protocols, which increase opex. As acreage shifts into deeper waters, gaps in helideck logistics and emergency response capabilities will need to be rectified to maintain safety records across the Vietnam oil and gas upstream market.

Regulatory Landscape

Vietnam's upstream governance is anchored by the 2022 Law on Oil and Gas. Under this framework, the Ministry of Industry and Trade (MOIT) oversees basic petroleum investigation and petroleum activities, including verification and appraisal steps, while Production Sharing Contracts (PSCs) remain the primary contracting vehicle between Vietnam National Oil and Gas Group (PetroVietnam/PVN) and investors, subject to MOIT processes and Prime Minister-level approvals for key terms. Offshore investment by state enterprises is also framed by Decree 132/2024/ND-CP, effective December 5, 2024, which specifies procedures and requires MOIT opinions on matters within its state-management scope, reinforcing multi-agency sequencing from exploration programs through reserve appraisal and commercialization decisions.

Technical compliance requirements tightened with Circular 57/2025/TT-BCT, effective January 20, 2026. The circular sets technical requirements across exploration, development, and production activities and increases reliance on documented standards for field execution and contractor qualification. Policy work continued in 2026, with MOIT's Oil, Gas and Coal Department assigned in May 2026 to lead drafting revisions to the petroleum law, indicating a push to align upstream investment procedures with broader investment and state-capital management rules, even as permitting complexity continues to constrain project cycle times.

Competitive Landscape

PetroVietnam secures carried interests in every PSC and supplies legacy infrastructure, anchoring the Vietnam oil and gas upstream industry. International majors—ExxonMobil, TotalEnergies, and Eni—bring deep-water know-how, long-term capital, and carbon-capture pilots. Independents such as Jadestone Energy and EnQuest exploit marginal fields through nimble decision chains and cost-efficient jack-up campaigns.

Digitalization marks the frontier of competitive advantage. Early adopters of real-time drilling analytics have reduced non-productive time by up to 20%, while predictive maintenance has cut unplanned shutdowns on production platforms. Service-sector consolidation is evident, as PV Drilling’s future PVD 9 rig will boost national jack-up capacity and align with PetroVietnam’s push for increased local content.

Strategically, companies are diversifying into gas-to-power to guarantee offtake and hedge price cycles. Aramco’s 2024 cooperation agreement envisions technology transfer and co-investment pathways in lower-carbon fuels. Export-credit-agency finance, exemplified by JBIC’s USD 415 million Block B loan, favors Japanese contractors and cultivates multi-tier supply chains that reinforce competitive positioning without breaching Vietnam’s foreign-ownership ceilings. Consequently, the Vietnam oil market, as an upstream market, rewards firms able to integrate subsurface excellence, capital efficiency, and geopolitical dexterity.

Vietnam Oil And Gas Upstream Industry Leaders

Vietnam Oil & Gas Group (PetroVietnam)

PTTEP

Jadestone Energy

ExxonMobil (incl. Ca Voi Xanh pre-first gas contribution)

Rosneft

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is centered on gas-led offshore developments that can be commercialized through contracted domestic offtake, with upstream milestones being paired with facility additions and gas sales agreements. Specific examples include the Su Tu Trang Phase 2B pathway on Block 15-1, where a GSPA was signed and the development plan includes a new Central Gas Facility (CGF) platform, and the Nam Du and U Minh gas discoveries, where the Vietnam Government approved the field development plan in March 2026. That approval enabled tenders for infrastructure and shifted the projects from appraisal into execution. These moves fit the report's described pivot from higher-risk frontier exploration toward integrated project development that links offshore gas supply to captive power demand.

Opportunities also arise from (i) appraisal and resource-upside confirmation that refreshes drillable inventory in mature basins, as indicated by Murphy's Hai Su Vang-2X appraisal result in Block 15-2/17, and (ii) fiscal and contractual incentives in the 2022 Law on Oil and Gas for deep-water, offshore, and unconventional blocks. Such provisions, including longer contract terms and extended prospecting periods, improve the investability of technically challenging acreage. In parallel, national upstream entities are expanding adjacent capabilities that can monetize subsurface and infrastructure advantages, including PVEP's stated expansion into CCUS-related scope such as CO2 transportation, which opens collaboration lanes for service providers alongside conventional development work.

Recent Industry Developments

- June 2026: PVEP and Petrovietnam commissioned the ST-9P well at the Su Tu Trang gas field (Block 15-1), bringing on new production at around 30.72 million cubic feet of gas per day and 6,096 barrels of condensate per day. The startup strengthens near-field development economics in the Cuu Long area and supports integrated gas commercialization efforts centered on domestic demand.

- May 2026: Petrovietnam launched an open international bidding process for exploration and production rights at offshore Block 17 in the Cuu Long Basin. The tender enlarges the near-term licensing pipeline and signals ongoing use of competitive rounds to attract partners into established offshore provinces.

- December 2024: Pharos Energy reported that licenses for two Vietnam oil and gas fields were extended to 2031 and 2032. The extensions preserve continuity for upstream operations and investment planning on existing assets, which is material in a basin where operators balance depletion with incremental redevelopment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value generated from upstream oil and gas activity in Vietnam. It includes exploration, field development, production, and end-of-life work for oil and gas assets, across both onshore and offshore locations.

Scope exclusions: This sizing does not include midstream transport and storage, downstream refining and retail fuels, and power generation from gas.

Segmentation Overview

- By Location of Deployment

- Onshore

- Offshore

- By Resource Type

- Crude Oil

- Natural Gas

- By Well Type

- Conventional

- Unconventional

- By Service

- Exploration

- Development and Production

- Decomissioning

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base on Vietnam upstream activity and to set realistic ranges for production, reserves, and project timing. We referenced public sources such as the General Statistics Office of Vietnam for macro and industry context, plus international energy statistics such as IEA and EIA releases for cross-checks on production and consumption balances.

To ground the upstream activity pipeline, we also reviewed public project and licensing information available through government and regulator communications, along with operator press releases, audited annual reports, and investor presentations. Patents and technical papers (where relevant to offshore development and well work) helped interpret which activity types were more likely to scale. In addition, we used paid subscriptions for company financials and intelligence, news and financials, and patent databases to speed up validation of timelines, asset ownership changes, and reported spend patterns. The desk sources mentioned are illustrative and not exhaustive, and many other public and paid sources were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating how upstream revenue is recognized across exploration, development and production, and decommissioning, then stress testing the assumptions behind activity levels by asset type. We spoke with a mix of operators, upstream service specialists, and industry advisors, and we balanced inputs between onshore and offshore viewpoints so gaps from public disclosures could be closed with practical checks.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 15% | |

| Mid tier: 45% | Functional/Unit leaders: 40% | |

| Smaller Players: 22% | Managers: 45% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where production outlook and field development schedules are translated into a realistic demand pool for upstream activity. Then, value is mapped using service mix and typical cost intensity by stage. In practice, exploration activity, development drilling cadence, offshore project sanctioning, and decommissioning timing are the key signals that shape the yearly totals.

Those totals were then checked using selective bottom-up approximations. This included sampled operator and contractor revenue cues, project-level spend markers from public announcements, and sanity checks on implied spend per well or per development phase. Where the bottom-up trail was incomplete, such as small contracts or bundled work scopes, we filled gaps using ratios derived from comparable projects and then re-checked them during calls.

For forecasting, scenario analysis was used so the model can reflect changes in project approvals, commodity price sensitivity for discretionary exploration, and offshore development lead times. The final forward view was adjusted only after primary inputs aligned on expected activity timing and a reasonable progression for service intensity and pricing.

Data Validation & Update Cycle

Outputs were validated through multiple passes against independent signals. These included implied spend versus announced project milestones, consistency of service mix shares over time, and year-on-year swings that require a clear operational reason. When outliers appeared, we traced them back to inputs such as delayed project start dates, unusually high drilling assumptions, or pricing steps that did not match feedback from market contacts.

Before sign-off, another analyst reviews the model logic, unit conversions, and key assumptions to catch calculation errors and scope creep early. Reports are refreshed annually, with interim updates when material events occur, including new project sanctions, large delays, or policy changes that alter upstream activity. Right before delivery, we run a final scan of recent announcements so clients receive the latest view available.

Mordor Intelligence's Vietnam Oil and Gas Upstream Market Size Compared With Other Published Estimates

Published numbers for Vietnam upstream often do not match because sources do not treat the same money flows as part of the market, and they also anchor forecasts to different activity timing. The spread usually comes from whether the estimate is closer to a spending view, a broader upstream activity view, or a mix of both, and from how pricing and currency timing are handled.

Some published figures lean toward a capex line-item view tied to announced budgets, which tends to exclude ongoing production-linked services and late-life work. Others use a wider upstream definition that can blend extra offshore systems beyond what is clearly attributable to Vietnam E&P in the year. Mordor Intelligence counts exploration, development and production, and decommissioning in Vietnam, while keeping midstream and downstream value out of the totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.82 B (2025) | |

| Global Consultancy A | USD 3.13 B (2026) | Uses a different base year and a longer horizon, and the scope description also appears to fold in a broader set of upstream infrastructure and service lines, which can lift the starting value. |

| Trade Journal B | USD 1.30 B (2025) | Tracks Vietnam E&P capex spending only, and it explicitly excludes some projects, so it misses production-linked services and decommissioning that still generate upstream market value. |

Taken together, the table shows that a spending-only lens can understate the market, while a wide upstream lens can overstate it when adjacent items are blended in. By keeping the scope tied to upstream life-cycle activities and cross-checking with project timing and activity intensity, the final number remains traceable to drivers that can be repeated year to year.

Key Questions Answered in the Report

What is the current value of the Vietnam oil gas upstream market?

The Vietnam oil gas upstream market is valued at USD 2.98 billion in 2026 and is projected to reach USD 3.91 billion by 2031.

Which segment holds the largest share of Vietnam’s upstream revenue?

Offshore projects dominate with 77.25% of 2025 revenue and remain the primary growth engine through 2031.

How fast is Vietnam’s natural-gas output expected to grow?

Natural gas revenue is forecast to expand at a 6.02% CAGR, taking market share to more than 59% by 2031.

What are the main barriers to upstream investment in Vietnam?

Prolonged permitting cycles and geopolitical risks in the South China Sea are the most significant obstacles.

Which companies lead integrated gas-to-power development?

PetroVietnam partners with ExxonMobil and TotalEnergies on projects such as Ca Voi Xanh and Block B that link offshore supply to onshore generation.

How will decommissioning impact service demand after 2031?

A growing number of first-generation platforms will reach end-life, creating new demand for specialized removal and site-remediation services.

Page last updated on: