Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.64 Billion |

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 8.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Motor Insurance Market Analysis by Mordor Intelligence

The Indonesia motor insurance market size is expected to grow from USD 1.64 billion in 2025 to USD 1.78 billion in 2026 and is forecast to reach USD 2.69 billion by 2031 at 8.6% CAGR over 2026-2031. Mandatory third-party liability (TPL) cover is set to draw more than 120 million vehicles into formal protection once delayed, but is still expected within the forecast horizon. Digital distribution is accelerating as insurers adapt to a tech savvy population. At the same time, rising vehicle ownership in Java and Sumatra, the growth of ride-hailing fleets, and a fast growing electric-vehicle parc add fresh premium pools.Moreover, stricter capital regulations, the swift rise of digital-only insurers, and increased tech investments by established players are intensifying competition in Indonesia's motor insurance market. Moving forward, the industry's trajectory hinges on regulatory clarity from the Financial Services Authority and insurers' success in broadening coverage to include uninsured motorcycles and second-hand vehicles, especially in underserved provinces.

Key Report Takeaways

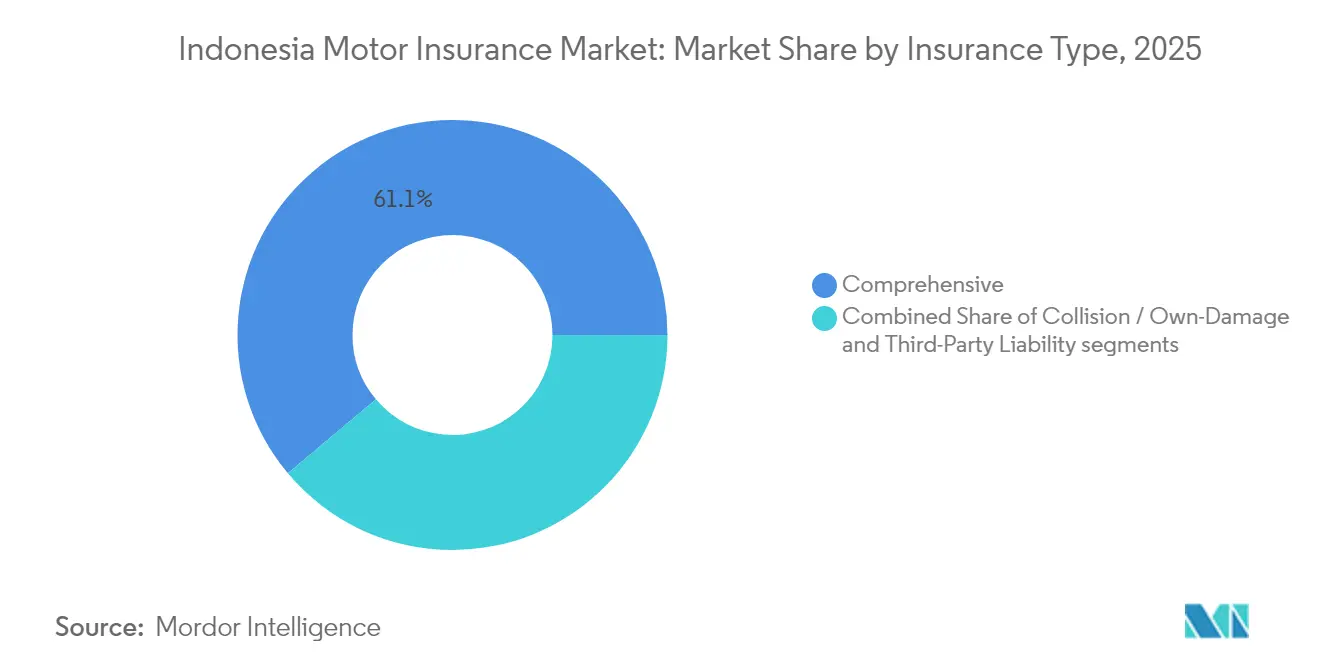

- By insurance type, comprehensive coverage dominated the market in 2025, representing 61.12% of the total motor insurance market size. Meanwhile, third-party liability (TPL) premiums are expected to grow significantly, with a projected CAGR of 18.95% between 2026 and 2031

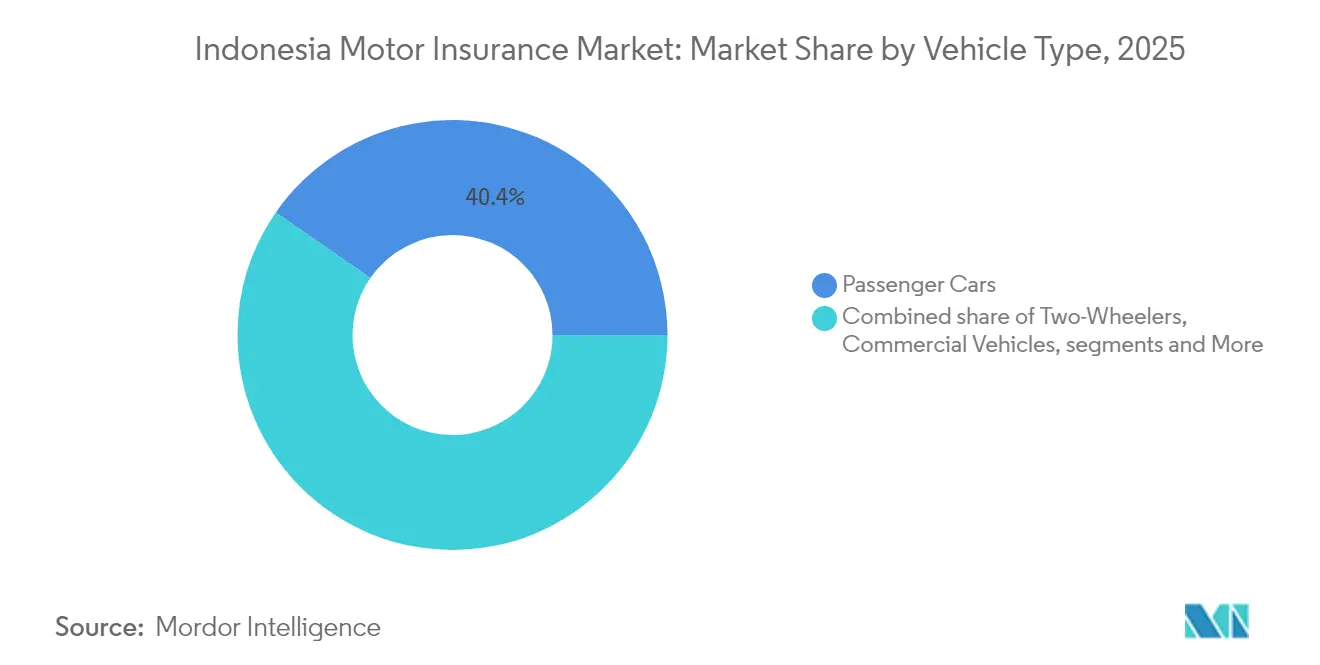

- By vehicle type, passenger cars contributed 40.35% to the total market size in 2025. However, electric vehicles (EVs) are anticipated to experience the highest growth, expanding at a CAGR of 25.85% through 2031.

- By distribution channel, agents and brokers accounted for 33.45% of total written premiums in 2025. Direct digital platforms, however, are gaining momentum and are expected to grow rapidly at a CAGR of 23.70% by 2031

- By region, the western cluster, comprising Java, Sumatra, and nearby islands accounted for 57.95% of Indonesia’s motor insurance market share in 2025. In contrast, the eastern cluster is projected to register the fastest growth, with a CAGR of 10.95% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Motor Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory & digital cover mandate | +7.6% | Nationwide (early focus on Java) | Medium term (2–4 years) |

| Rising middle-class vehicle sales | +3.2% | Java, Sumatra | Short term (≤ 2 years) |

| Ride-hailing fleet expansion | +2.8% | Major cities | Short term (≤ 2 years) |

| Usage-based telematics adoption | +4.2% | Urban areas | Medium term (2–4 years) |

| Jakarta flood events | +1.5% | Jakarta and surrounding areas | Short term (≤ 2 years) |

| Takaful motor insurance expansion | +1.9% | Nationwide (Muslim-population dense regions) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government Push for Mandatory & Digital Motor Cover in Indonesia

The Financial Services Authority is finalizing rules that will require every motorist to purchase at least TPL cover, creating the single biggest catalyst for the Indonesia motor insurance market. Once enforcement begins, a USD 15.5[1]Erfan Maruf, “OJK Delays Mandatory Vehicle Insurance Program Pending Government Regulation,” Jakarta Globe, jakartaglobe.id annual premium applied to even 75% of the registered fleet would almost double the premium pool, pushing insurers to overhaul distribution and claims workflows to handle mass-market volumes. Larger carriers are beta-testing fully digital onboarding journeys that link police databases, payment gateways, and e-registration certificates, while smaller firms seek white-label platforms to remain compliant. Early pilots in Java confirm strong demand when premiums can be paid in monthly instalments.

Rising Automotive Sales among Middle-Class Consumers in Java & Sumatra

A growing middle class continues to buy cars and motorcycles despite a temporary dip in wholesale deliveries. Astra retained 56% share in car sales and 78% in motorcycles, putting insurers linked to the Astra ecosystem in a favourable underwriting position[2]Jardine Matheson, “Astra 2024 Annual Report,” ar.jardines.com. New vehicle purchases commonly bundle multi-year comprehensive coverage, prompting higher average premiums than renewals. Banks and multi-finance firms that provide vehicle loans are tightening covenants that require full-risk protection, adding incremental premium inflow. As household disposable income rises outside Jakarta, insurers anticipate fresh demand for add-ons such as personal-accident riders and natural disaster extensions. The Indonesia motor insurance market, therefore, benefits directly from each uptick in showroom traffic and consumer credit disbursements.

Ride-Hailing Boom Accelerating Commercial Motor Coverage Demand

Platforms such as Gojek and Grab have turned millions of private cars and motorcycles into commercial vehicles, spawning new risk profiles that the Indonesia motor insurance market is now pricing separately. Usage-based policies are activated only during working hours, keeping premiums affordable for drivers who work part-time. Aggregated fleet data enables insurers to refine underwriting on accident hotspots, peak-hour risk, and driver behavior. Partnerships between ride-hailing apps and insurers allow real-time policy issuance, seamless claims initiation, and cashless repairs at network workshops. As the gig-economy labor force grows, insurers expect commercial motor premiums to rise faster than personal-lines equivalents, bolstering overall market momentum.

Growth of Usage-Based (Telematics) Policies via Insur-Tech Platforms

InsurTechs such as PasarPolis and Qoala embed telematics devices or mobile SDKs in customer smartphones, scoring driving habits to offer personalized discounts that appeal to younger demographics[3]Ari Susanto, “Digital Transformation of the Insurance Industry,” ResearchGate, researchgate.net. Although still a niche, telematics products record retention rates that are 10-15% points higher than traditional policies, lowering long-run acquisition costs. Data feeds enable real-time intervention push alerts warn against harsh braking or speeding, supporting accident-prevention efforts that regulators endorse. As connected-vehicle penetration rises and 5G coverage extends outside Jakarta, the Indonesian motor insurance market is likely to see a sharper shift toward behavior-based pricing models, reducing cross-subsidies and boosting underwriting margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-sensitive motorcycle lapses | -4.2% | Nationwide, rural focus | Medium term (2-4 years) |

| Uninsured second-hand vehicles | -3.8% | Sumatra, Kalimantan, Sulawesi | Long term (≥ 4 years) |

| Fraudulent Claims & Spare-Part Cost Inflation | -2.5% | National, with higher incidence in Sumatra | Medium term (2-4 years) |

| Absence of Centralised Accident Database Limiting Risk Pricing | -1.9% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Price-Sensitivity & Policy Lapse Rates in the Motorcycle Segment

Motorcycles dominate Indonesian roads but contribute modestly to premium volume because owners often cancel policies once loan obligations end. Surveys show lapse rates near 30% in rural districts, undermining efforts to broaden the Indonesian motor insurance market. Insurers testing micro-duration policies priced at Rp 500 per day report higher uptake, yet profit margins remain thin. Education campaigns led by industry associations stress post-accident financial risks, but converting awareness into sustained renewals is slow. Without targeted subsidies or embedded cover in fuel or service-station transactions, motorcycles will continue to drag on overall market growth.

Large Pool of Uninsured Second-Hand Vehicles Outside Java

In provinces beyond Java, second-hand cars and pickup trucks change hands informally, bypassing registration channels where insurance could be promoted. Lower financial literacy and fewer repair networks deter buyers from seeing value in coverage. Claim ratios in Sumatra underscore the risk: accidents are more frequent, yet fewer policies exist to absorb losses, leading to social pressure for ex-gratia payments rather than formal claims. Digital marketplaces that broker used-vehicle sales are starting to embed instant-quote widgets, but broadband gaps slow adoption. Until access barriers fall and road-safety awareness rises, uninsured vehicles will constrain the Indonesia motor insurance market’s long-term potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Third-Party Liability Set to Surge with Regulatory Push

The comprehensive class generated 61.12% of the Indonesia motor insurance market size in 2025, reflecting strong demand among higher-income motorists seeking protection against theft, collision, and natural disasters. Premium growth in this class remains stable because vehicle prices, repair costs, and extreme weather risks continue to rise. Yet, regulatory momentum behind mandatory TPL is reshaping product portfolios. Insurers are recalibrating underwriting systems to manage an expected influx of low-ticket policies, while lobbying for actuarially sound tariff bands to remain profitable.

Third-party liability premiums are projected to compound at 18.95% through 2031, well above the overall Indonesia motor insurance market CAGR, once the mandate is fully enforced. Carriers are bundling bodily injury and property damage extensions, anticipating consumer upgrades once compulsory coverage becomes a sunk cost. Collision/own-damage protection retains a niche among middle-income owners who balance cost and risk, but its share is likely to erode as buyers either downshift to basic TPL or step up to all-risk packages. Over time, richer data from centralized accident reporting should allow for more granular pricing, narrowing down loss-ratio gaps across product tiers.

By Vehicle Type: Electric Vehicles Charging Ahead Despite Small Base

Passenger cars delivered 40.35% of 2025 written premiums, benefiting from higher average insured values and bank-financed purchases that require full cover. Two-wheelers, while numerous, still lag because low asset values and price-sensitive riders limit average premiums. Commercial vehicles maintain a steady base tied to logistics and infrastructure activity, often insured under fleet programs that bundle multiple trucks under one policy.

Electric vehicles account for less than 1% of units on the road, yet their premium pool is forecast to expand at a 25.85% CAGR, outpacing every other sub-class in the Indonesia motor insurance market. Government incentives, import-duty waivers and expanding charging networks underpin demand. Early adopters tend to select comprehensive cover that addresses battery-specific risks and scarce spare-part supply, lifting average premiums. Insurers are partnering with automakers to offer integrated after-sales service and telematics monitoring, thereby mitigating high repair-cost uncertainty and encouraging broader risk adoption.

By Distribution Channel: Digital Platforms Disrupting Traditional Networks

In 2025, agents and brokers secured 33.45% of the total written premiums, underscoring the pivotal role of personal relationships in the intricate world of insurance sales. Older consumers and rural buyers, especially those less versed in insurance jargon, still favor face-to-face advisory sessions. In a bid to uplift service standards, the Indonesian General Insurance Association has rolled out an e-certification initiative. This move not only aims to professionalize the intermediary workforce but also bolsters adherence to fit-and-proper standards and enhances claims-handling skills across the industry.

Conversely, direct digital portals such as mobile apps and insurer websites are registering a 23.70% CAGR, steadily enlarging their slice of the Indonesia motor insurance market. Simple quotation engines, instant issuance, and transparent pricing appeal to millennials accustomed to cashless retail experiences. Carriers report lower acquisition costs via self-service channels, freeing resources to invest in AI-based claim triage and fraud detection. Bancassurance and dealer-led sales continue to thrive at the point of vehicle purchase or financing, while price-comparison marketplaces attract savvy shoppers seeking policy bundles and promotional vouchers.

Geography Analysis

Java, Sumatra, and adjacent islands commanded 57.95% of the Indonesian motor insurance market in 2025 supported by higher household incomes, dense traffic conditions, and well-developed repair ecosystems. Jakarta alone posts loss frequencies that outstrip national averages, encouraging motorists to favor comprehensive cover and value-added services like on-site claim assessment. Fierce rivalry among national and regional brands keeps premiums competitive, while digital channels find fertile ground in a population with near-universal smartphone penetration.

The central belt, Kalimantan, Sulawesi, and Nusa Tenggara contributes to a modest but rising share. Rapid urbanization around new nickel-processing hubs and the planned national capital in East Kalimantan is boosting vehicle registrations. Insurance uptake hinges on trust built through community leaders; once religious or civic influencers endorse a provider, neighborhood adoption accelerates. Insurers deploying mobile claim vans and cashless repair networks report higher satisfaction scores, which bode well for retention and cross-selling.

Papua, Maluku, and eastern Nusa Tenggara comprise the smallest yet fastest-growing slice, set to climb at an 10.95% CAGR through 2031. Long distances, rugged terrain, and limited workshop infrastructure elevate logistical costs, but app-based kiosks and partner garages are reducing service gaps. The Indonesian motor insurance market benefits from government infrastructure programs that draw construction fleets requiring motor cover. As 4G coverage deepens, digital onboarding becomes feasible even in remote districts, opening a new frontier for mass-market penetration.

Competitive Landscape

The top five players holds close to 40% of written premiums in 2024, leaving ample room for mid-tier firms and niche Sharia underwriters. Market leader Asuransi Astra Buana held major share in 2024, leveraging its parent’s dominance in auto distribution to sell embedded cover at the point of sale. Premium income climbed 16.6% in 2024. Allianz and state-run PT Jasa Raharja (Persero) round out the top tier, each deepening digital alliances with ride-hailing apps and fintech lenders.

Digital-only entrants and aggregator platforms intensify rivalry by undercutting legacy pricing and offering instant claims cash-outs. Traditional insurers respond with omnichannel strategies, hybrid agency models, and application-programming-interface partnerships that embed cover in e-commerce checkouts. The Indonesia motor insurance industry faces a watershed as minimum capital thresholds rise in 2026 and 2028; smaller firms must recapitalize, merge, or exit. Early consolidation talks center on bolstering data analytics capabilities, expanding geographic footprints, and securing bancassurance pipelines.

Product innovation is another battleground. Several carriers launched pay-per-mile options for low-usage drivers and multi-year warranties tied to electric vehicle battery life. Sharia units are refining surplus sharing schemes to attract faith-based savers. At the same time, insurers are investing in anti-fraud tech, including license-plate recognition and blockchain claim ledgers, to rein in inflated spare-part costs. Taken together, these forces are set to reshape competitive dynamics and elevate service expectations across the Indonesia motor insurance market.

Indonesia Motor Insurance Industry Leaders

PT Asuransi Astra Buana

Asuransi Sinar Mas

PT Asuransi Central Asia

PT Jasa Raharja (Persero)

Allianz

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The Financial Services Authority (OJK) has delayed the roll out of mandatory third-party liability (TPL) insurance, which was set to launch in January 2025. OJK is holding off until a pertinent government regulation is issued.

- January 2025: MSIG Indonesia partnered with PT Arthaasia Finance to provide two-wheeler EV cover, positioning itself early in the high-growth electric segment.

- March 2025: OJK Regulation 37/2024 took effect, shifting supervision to a risk-based sanction framework, compelling insurers to strengthen governance.

- October 2024: AM Best upgraded the non-life segment outlook for Indonesia to stable, citing strengthened motor demand.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Indonesia's motor insurance market as all direct-written premiums for road-worthy passenger cars, two-wheelers, and commercial vehicles that purchase third-party liability, collision/own-damage, or comprehensive covers. The value base is gross premiums written in U.S. dollars at prevailing exchange rates, captured at the insurer level.

Scope exclusion: this sizing excludes extended service warranties, roadside-only assistance plans, and any marine, agricultural, or off-highway vehicle policies.

Segmentation Overview

- By Insurance Type

- Third-Party Liability

- Comprehensive

- Collision / Own-Damage

- By Vehicle Type

- Passenger Cars

- Two-Wheelers

- Commercial Vehicles (LCV & HCV)

- Electric Vehicles

- By Distribution Channel

- Agent / Broker Channel

- Bancassurance

- Automotive Dealer-Led

- Direct Digital (Insurer Web / Mobile)

- Digital Aggregators & Marketplaces

- By Region (Indonesia)

- Western

- Central

- Eastern

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed underwriting heads at large domestic insurers, regional insurtech founders, auto-dealer finance managers, and fleet owners across Java, Sumatra, and Sulawesi. These conversations tested loss-ratio assumptions, policy mix shifts, and average selling price (ASP) corridors that secondary sources could not fully surface.

Desk Research

We began by gathering national insurance statistics from Otoritas Jasa Keuangan, Bank Indonesia vehicle loan data, and Directorate-General of Customs import tallies that signal new-vehicle inflows. Trade-body white papers from the Indonesian General Insurance Association, accident frequency reports from the National Police, and macro indicators from BPS Statistics informed baseline demand and risk pricing.

To enrich firm-level insights, we drew on D&B Hoovers for carrier financials, Dow Jones Factiva for deal flow, and Questel patent feeds on telematics devices that shape usage-based products. Company 10-Ks, investor decks, and reputable press articles rounded out trend validation. This list is illustrative; many additional open and subscription sources were tapped along the way.

Market-Sizing & Forecasting

We anchored 2024 premiums by reconciling regulator-reported written premiums with a top-down "vehicle parc x penetration x ASP" construct, which is then sense-checked through sampled carrier roll-ups and channel checks. Key variables include registered vehicle stock, new-sales growth, mandate timing for compulsory TPL, average premium inflation, accident frequency, and EV share-drive forecast deltas. A multivariate regression with ARIMA overlays projects each driver through 2030, while bottom-up carrier samples plug residual gaps.

Data Validation & Update Cycle

Outputs face two analyst reviews; variance flags above +/-5% trigger model reruns, and every report is refreshed yearly with mid-cycle updates when regulatory or catastrophe events materially move the market.

Why Our Indonesia Motor Insurance Baseline Commands Reliability

Published estimates often diverge because firms frame coverage differently, choose distinct base years, or refresh at uneven intervals.

Key gap drivers include whether compulsory TPL uptake is modeled from 2025 or phased, how motorcycle policies (over 120 million units) are weighted, ASP escalation techniques, and currency conversion cut-off dates that we, at Mordor Intelligence, standardize but others may not.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.64 B (2025) | Mordor Intelligence | - |

| USD 1.72 B (2024) | Regional Consultancy A | Applies flat CAGR to historical BI data, limited expert validation |

| USD 11.8 B (2024) | Industry Journal B | Bundles life & accident riders, counts extended warranties, unclear FX basis |

In sum, our disciplined scoping, mixed-method modeling, and annual refresh cadence give decision-makers a dependable, transparent baseline that traces every figure back to observable vehicles, regulations, and premium flows.

Key Questions Answered in the Report

What is the forecast size of Indonesia’s motor insurance market by 2031?

The market is projected to reach USD 2.69 billion by 2031, expanding at an 8.6% CAGR.

How soon is mandatory third-party liability (TPL) cover expected to become effective?

Regulations are delayed but still anticipated within the 2026–2028 window, once the government issues the final implementing rule.

Which product segment will grow the fastest over the next five years?

TPL premiums are set to rise at a 18.95% CAGR through 2031 as compulsory cover is phased in nationwide.

How large is the opportunity in electric vehicle insurance?

Premiums linked to electric cars and two-wheelers are forecast to grow at a 25.85% CAGR, making EV cover the most dynamic sub-class despite a small current base.

Page last updated on: