Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

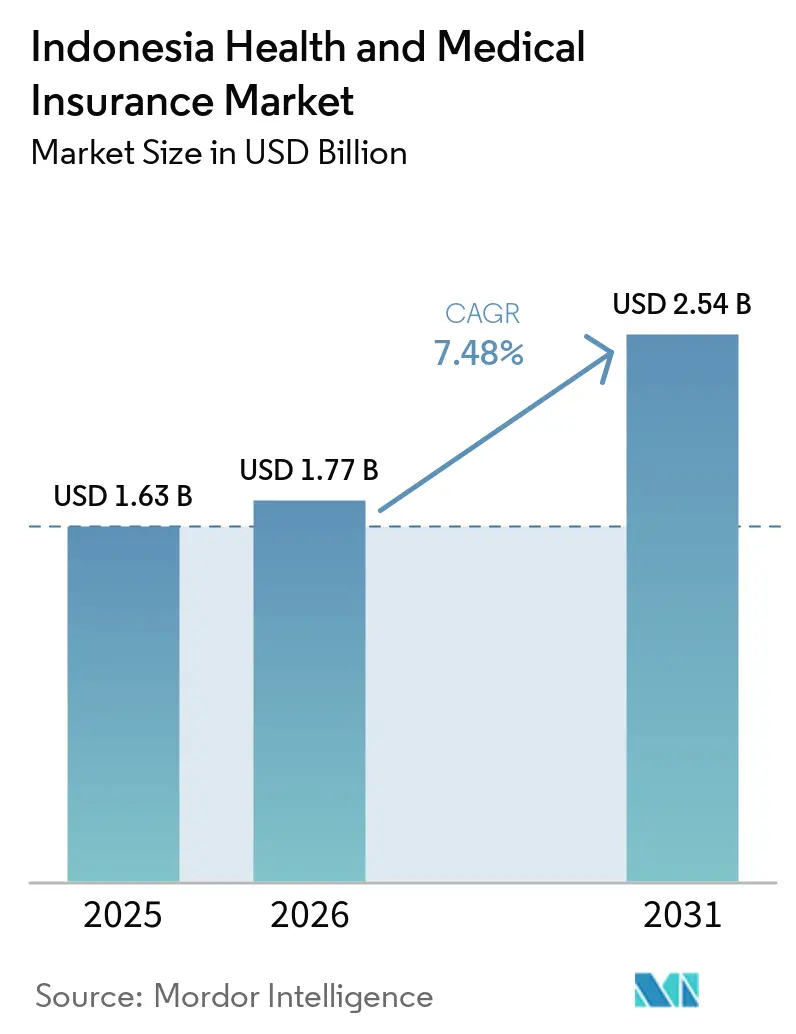

| Base Year Market Size (2025) | USD 1.63 Billion |

| Market Size (2026) | USD 1.77 Billion |

| Market Size (2031) | USD 2.54 Billion |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Health and Medical Insurance Market Analysis by Mordor Intelligence

The Indonesia Health And Medical Insurance Market size was valued at USD 1.63 billion in 2025 and is estimated to grow from USD 1.77 billion in 2026 to reach USD 2.54 billion by 2031, at a CAGR of 7.48% during the forecast period (2026-2031).

Growth is shaped by near-universal coverage under BPJS Kesehatan’s JKN, where 283 million participants, equal to 99.34% of the population by October 2025, have baseline protection. Private health insurance demand concentrates on supplementary benefits that enable access to private hospital amenities and faster specialist visits once patients choose to upgrade beyond JKN entitlements under the coordination of benefits framework. Distribution is modernizing through Financial Service Aggregators licensed by OJK, which reached 20 registered providers with 1,172 institutional partnerships and serving 13.10 million users in August 2025. Conduct standards and product governance will strengthen as OJK implements POJK Number 36 of 2025 in January 2026, which mandates medical governance, utilization review, and digital capabilities across all health insurers. Employer-sponsored group coverage strengthens as medical cost inflation persistently exceeds headline inflation, with peer-reviewed evidence of 26.5% in 2022 and 20.48% in 2023 for employer retiree populations.

Key Report Takeaways

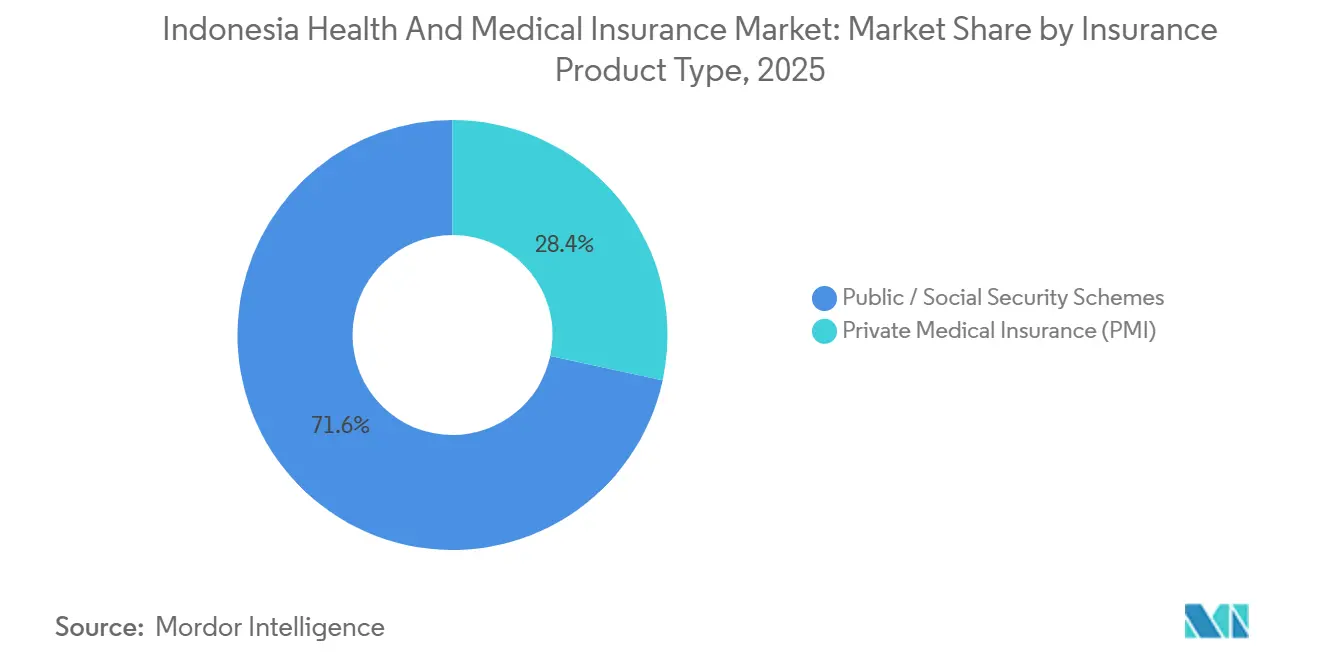

- By insurance product type, public and social security schemes led the Indonesian Health and Medical Insurance Market with a 71.62% share in 2025, while private medical insurance is projected to expand at a 9.02% CAGR through 2031.

- By distribution channel, brokers and agents held a 36.22% market share of the Indonesian Health and Medical Insurance Market in 2025, while direct‑to‑consumer is forecasted to grow at an 8.56% CAGR through 2031.

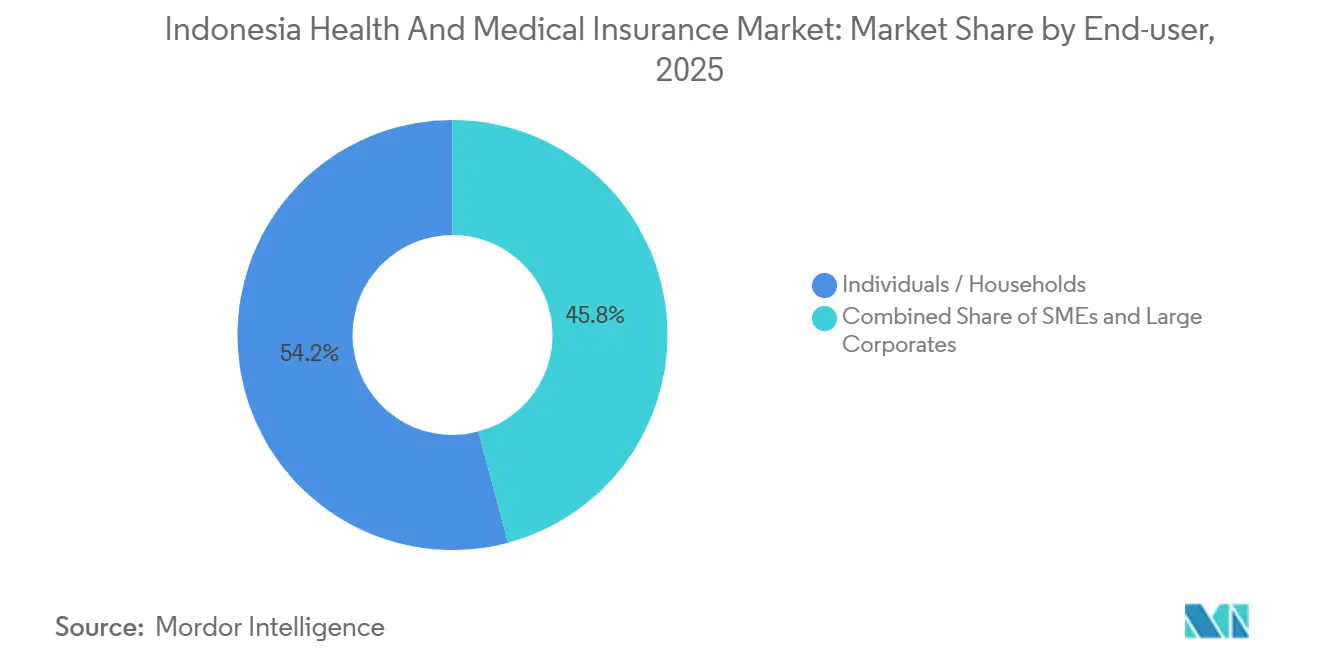

- By end‑user, individuals and households accounted for 54.16% of the Indonesian Health and Medical Insurance Market in 2025, while SMEs are set to record the highest CAGR at 9.39% through 2031.

- In Indonesia's health and medical insurance market, competition is fierce, and no single player holds a dominant position. However, insurers boasting robust bancassurance partnerships and advanced digital capabilities are poised to leverage significant scale advantages.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Health and Medical Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-universal JKN coverage and coordination of benefits | +1.8% | Global relevance, with near-term gains in Java, Bali, and urban Sumatra, where private hospital density is higher | Medium term (2-4 years) |

| Rising middle-class demand for private top-up access to superior amenities | +1.2% | Java, Bali, and major cities in Sumatra and Kalimantan | Medium term (2-4 years) |

| Double-digit medical inflation is pushing formal employer group benefits | +2.1% | National, with early concentration in industrial zones in West Java, Banten, and East Java | Short term (≤ 2 years) |

| Stricter OJK conduct rules improving transparency and confidence | +0.9% | Global | Medium term (2-4 years) |

| Digital bank and e-wallet distribution enabling embedded micro-insurance | +1.5% | Urban Java initially, then broader digitally connected populations in Sumatra, Sulawesi, and Kalimantan | Short term (≤ 2 years) |

| Government-funded annual health check-ups expanding risk awareness | +1.2% | National, strongest in provinces with higher screening participation, aided by SATUSEHAT app uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Near-Universal JKN Coverage Establishing Baseline Insurance Literacy

BPJS Kesehatan reached 99.34% population coverage, or 283 million participants, by October 2025, which establishes near-universal access to primary and catastrophic care and shifts private insurance interest toward enhancements in service quality and speed[1]Ministry of Health Indonesia, “Coordination Among Guarantee Providers, KMK 1366 of 2024,” Policy Brief, badankebijakan.kemkes.go.id. The Ministry of Health set a coordination of benefits framework under Decree KMK 1366 of 2024 that legitimizes private cover for cost differences when JKN participants upgrade hospital class or seek services beyond national tariffs, with caps designed to prevent excessive balance billing. This policy standardizes how commercial supplements integrate with JKN, which reduces consumer confusion and establishes a clear role for private plans as enhancement layers rather than substitutes for the universal base. With universal coverage in place, private products compete primarily on network breadth, referral flexibility, and non-formulary medication access that JKN may not prioritize due to tariff constraints. As the coordination framework matures, insurers can design standardized top-up offers tied to specific hospital class upgrades, which supports product clarity and reduces claims friction across providers.

Rising Middle-Class Demand for Private Healthcare Network Access

Indonesia’s middle class has been central to household spending, even as its headcount moved from 57.33 million in 2019 to 47.85 million in 2024[2]Statistics Indonesia (BPS), “Indonesia’s Middle Class, A Crucial Pillar for National Economic Stability,” bps.go.id. Higher-income professionals in financial and insurance services earned above the national average, which sustains paying capacity for supplementary cover that improves access and convenience. Middle-class households tend to value shorter waiting times and cashless access in private hospitals, reinforcing demand for private plans that bypass referral protocols and offer broader specialist choices. Consistent growth in digital financial services and aggregator platforms also reduces frictions in price discovery, which nudges middle-class buyers toward transparent, comparable plans from multiple insurers. These conditions allow the Indonesian health insurance market to attract first-time supplementary buyers who want predictable out-of-pocket costs when receiving higher-tier services than those covered by JKN.

Double-Digit Medical Inflation Pressuring Employers to Formalize Group Benefits

Medical cost inflation for employer retiree populations increased 26.5% in 2022 and 20.48% in 2023 in Indonesia, which exceeded general inflation and intensified corporate interest in risk transfer and utilization controls[3]. In the life segment, individual health policies experienced loss ratios of more than 200% in the first half of 2025, underscoring the immediate mismatch between claims costs and premiums that catalyzed repricing and product redesign[4]IFG Progress, “Insurance Quarterly Update 2025,” ifgprogress.id. In the general segment, health products also showed elevated loss ratios during 2025, which encouraged tighter managed care protocols and group plan economies of scale. Cost drivers reflect chronic disease burdens where inpatient care generates risk far above clinic visits, and where medicine and treatment represent significant shares of overall expense. As employers standardize benefit designs and adopt third-party administration, the Indonesian health insurance market gains stable group premium pools that support preventive programs and utilization review.

Digital Bank & E-Wallet Distribution Unlocking Micro-Insurance

Smartphone penetration is topping 89%, and the ubiquity of e-wallets is accelerating direct-to-consumer policy issuance.[3]Healthcare Costs for Employer-Sponsored Retiree Populations in Indonesia,” Narra J via PubMed Central, pmc.ncbi.nlm.nih.govMicro-premiums as low as IDR 3,000 per week, paid via one-click deductions, resonate with gig-economy workers and rural smallholders previously unreachable by agents. Regulatory sandbox approvals permit real-time pricing engines that ingest telemedicine consultation records, enabling instant micro-claims settlements. Such frictionless experiences build trust among first-time buyers and are scaling nationally as digital banks cross-sell protection to transaction-heavy customers. The growth momentum is strongest on Java, but early adoption in secondary islands signals nationwide potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| JKN funding pressures are affecting provider reimbursements and sustainability | -0.7% | National, with higher severity in regions with lower contribution to collection | Long term (≥ 4 years) |

| Accelerating medical inflation far above headline inflation | -1.1% | National, with higher intensity in urban markets with greater private hospital utilization | Long term (≥ 4 years) |

| Data localization and PDP Law compliance costs | -0.5% | Global, affecting multinational and domestic carriers with cross-border data architectures | Medium term (2-4 years) |

| Low insurance literacy and inclusion, with urban concentration | -0.9% | Eastern Indonesia and rural provinces in Sumatra, Kalimantan interior, and Sulawesi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating medical inflation far above headline inflation

Health care cost trends continue to diverge from consumer prices, with medical inflation for employer retiree populations rising 26.5% in 2022 and 20.48% in 2023. Elevated loss ratios in 2025 in both life and general segments show that repricing lags claim growth, compelling tighter underwriting and benefit redesign. Inpatient care drives substantially higher risk than clinic visits, with medicines and treatment forming large shares of mean expense, which pushes carriers toward formulary management and network steerage. These pressures lead employers to formalize group coverage and invest in managed care and wellness programs, which gradually improve trend lines but take time to manifest in claims experience. The Indonesian health insurance market experiences mixed effects, with short-term premium increases offset by more sustainable product constructs over the forecast.

Data localization and PDP Law compliance costs

Data localization policies in Indonesia allow offshore storage only under specific approvals and require insurers operating digital platforms to register with authorities before systems are accessible to local users. The Personal Data Protection Law enforces strict rules for data collection, processing, and cross-border transfers, requiring equal protection levels or approved mechanisms and increasing governance costs. Health data receives special treatment under newer regulations that tighten localization for health information systems, pushing carriers to invest in domestic infrastructure and local IT teams. These requirements increase capital and operating expenses for multinational and domestic insurers that rely on global cloud architectures. Over time, standardization of data governance improves consumer trust but adds drag to short-term digital scaling economics in the Indonesian health insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Product Type: Private Insurance Captures Growing Supplementary Demand

Public and social security schemes are expected to account for 71.62% of the Indonesian health insurance market in 2025, with private medical insurance projected as the fastest-growing segment at a 9.02% CAGR through 2031. The coordination of benefits framework under KMK 1366 of 2024 allows private insurers to cover capped cost differences when JKN participants upgrade hospital classes or seek services beyond standard tariffs. This framework positions private insurance as an enhancement layer, enabling products focused on room class upgrades, access to medications beyond JKN formularies, and faster specialist consultations, appealing to households seeking higher service levels. Elevated loss ratios in individual products during 2025 have increased repricing pressures and driven the adoption of utilization reviews and clinical governance to manage costs. The market benefits from stable public coverage as a universal base, with private plans addressing service quality gaps valued by households and employers.

Group health pools remain central as employers prioritize predictable budgets and structured care pathways. Individual products are evolving with clearer co-payment terms and simplified benefits. Enhanced medical governance under POJK 36 of 2025 and insurer-level Medical Advisory Boards improve clinical consistency and consumer confidence. Managed care strategies, pharmacy controls, and negotiated provider arrangements help private insurers curb high-cost inpatient episodes. Rising product literacy through JKN participation boosts upgrade-oriented private plans in urban centers, sustaining private segment growth while public schemes dominate enrollment.

By Distribution Channel: Digital Platforms Disrupting Traditional Intermediaries

Brokers and agents held 36.22% of the market share in 2025, while the direct-to-consumer (D2C) channel is projected to grow at a compound annual growth rate (CAGR) of 8.56% through 2031. This mix reflects the need for advice-driven sales in complex cases and the rise of digital self-service for simpler products. By August 2025, 20 OJK-licensed financial service aggregators facilitated 1,172 partnerships and transactions across 13.10 million users, highlighting the momentum of digital distribution. Exclusive bancassurance agreements, such as AIA Financial Indonesia’s renewal with Bank Central Asia through 2038, position large banks as key channels for protection products, including health riders. Agents remain essential for middle-aged and older demographics, where customization and claims support are valued, while younger consumers prefer digital platforms for comparisons and instant issuance.

Qoala’s platform expansion, supported by insurer partnerships, demonstrates a hybrid model combining agent advisory with mobile-first digital processing to enhance service speed and convenience. The market benefits from this multi-channel approach, as intermediaries handle complex cases, while standardized D2C plans improve accessibility for first-time buyers. Standardized co-payment features and stronger clinical governance improve product comparability, aiding aggregators in presenting like-for-like options. Omnichannel models reduce acquisition barriers and enhance retention through banking auto-debits, in-app renewals, and straight-through claims processing, increasing transparency and expanding market reach across demographics and regions.

By End-user: SMEs Drive Fastest Segment Expansion

Individuals and households accounted for 54.16% in 2025, SMEs are projected to grow fastest at a 9.39% CAGR, and large corporates hold a meaningful share in the Indonesian health insurance market. Households use private policies to upgrade hospital class and secure broader networks, while the universal public base remains their primary safety net. In 2025, higher loss ratios in individual products drove sector-wide repricing and stricter policy wording, which aimed to align premiums with claim intensity while maintaining value. Consumers respond well to simpler structures with transparent co-pays and clear exclusions when presented through mobile-first journeys with instant policy issuance. Over the forecast, household adoption continues to rise in urban corridors as service quality differentials and referral flexibility justify supplementary premiums.

SMEs add insured employees as competition for talent intensifies and as health protection becomes a core component of compensation packages. Carriers tailor SME plans to balance affordability and adequacy, often bundling standardized benefits with simple co-pay designs that are easier for smaller HR teams to administer. Large corporations maintain customized schemes that blend insured and self-funded arrangements and increasingly use third-party administrators for utilization management. As governance rises under POJK 36 of 2025, the Indonesia health insurance market size benefits from steadier group premium pools and better claim oversight across employer categories. The end-user mix, therefore deepens with steady household demand, faster SME adoption, and stable corporate renewals.

Geography Analysis

Urban corridors in Java and Bali anchor adoption due to higher middle-class density, deeper private provider networks, and concentrated distribution capacity that supports faster plan comparisons and issuance. Higher average wages in financial and insurance centers strengthen purchasing power for supplementary plans, which amplifies upgrade-driven demand. As universal coverage standardizes baseline access through JKN, urban households place a premium on shorter waiting times and broader specialist choice that private networks can provide. The Indonesian health insurance market benefits from this concentration because advisory networks, bancassurance branches, and digital aggregators are more active in metropolitan areas. Over the forecast, coordination of benefits will reinforce Java and Bali as early adoption zones for standardized upgrade products.

Sumatra and Kalimantan’s major cities expand through bank-led cross-sell and growing aggregator reach, which improve plan awareness and simplify shopping journeys beyond agent networks. These regions benefit as SMEs adopt group policies to compete for talent and as banks digitize collections that reduce lapses. Wage levels in key urban areas remain lower than Jakarta’s core, yet steady employment in services and trade supports modest premium budgets for supplementary cover. Aggregators and embedded distribution via digital wallets and e-commerce platforms widen reach, while hybrid agent support remains important for complex cases. Over time, the Indonesia health insurance market size in these provinces grows with improving digital infrastructure and rising product literacy.

Eastern Indonesia, including Sulawesi, Maluku, Nusa Tenggara, and Papua, shows slower uptake because private hospital density is lower and agent networks are less extensive. Insurance literacy gaps also reduce voluntary supplementary adoption despite JKN’s near-universal reach, which highlights the need for targeted education and digital inclusion. Government-backed free screening and primary care programs increase health awareness, which supports gradual adoption once service access improves and purchasing power rises. As mobile coverage and app-based services extend further, embedded offers in payments and mobility apps can provide on-ramps for first-time buyers. These trends suggest a widening, multi-speed expansion for the Indonesia health insurance market across the archipelago.

Competitive Landscape

Indonesia’s carrier set includes life insurers offering health riders, general insurers with standalone health products, and insurtech platforms that aggregate or embed protection offers, each contributing to underwriting, distribution, and claims administration. Multi-year bancassurance partnerships remain central to scale, as seen in AIA Financial Indonesia’s extended exclusivity with Bank Central Asia through 2038, which secures access to a large client base for protection plans that include health benefits. Insurtechs such as Qoala support both direct and agent-assisted journeys, with partnerships and mobile tools that help advisors process policies and claims faster. Together, these models support a hybrid future where advice remains essential for complex cases while simple products scale digitally.

Regulatory reforms shape competition in 2026 as OJK’s POJK 36 of 2025 raises requirements for medical governance, utilization review, and digital capabilities, promoting stronger claim oversight and product clarity. OJK’s strengthened reporting regime from Q2 2026 increases transparency on claims and performance, which pressures underperforming products to improve or exit. Capital standards are also on an upward glide path, which favors well-capitalized incumbents and encourages consolidation among smaller carriers that lack scale. Carriers respond with standardized co-pay designs, more precise clinical pathways, and tighter provider contracting to improve loss ratios. The Indonesia health insurance market therefore rewards those with strong bancassurance anchors, efficient digital funnels, and robust medical governance.

Strategic moves in 2025 and 2026 highlight distribution lock-ins and digital operating upgrades. AIA’s partnership renewal with BCA secures long-term access to a top retail bank channel, which helps sustain protection sales momentum that includes health benefits. Insurtech partnerships and tools that speed up issuance and claims settlement continue to expand, supported by insurer collaborations and technology vendors. As regulatory oversight tightens, carriers invest in data quality, integration with providers, and reporting systems that can satisfy OJK’s quarterly requirements starting in 2026. The combined effect is a more transparent and professionally governed Indonesia health insurance market that is better positioned for sustainable growth.

Indonesia Health and Medical Insurance Industry Leaders

BPJS Kesehatan

Prudential Indonesia

Allianz Life Indonesia

AIA Financial Indonesia

AXA Mandiri Financial Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Danantara proposed a broader consolidation plan to merge 15 state-owned asuransi and reasuransi entities into three large insurance groups under the Indonesia Financial Group (IFG) umbrella. While this includes general insurance, the restructuring could have downstream effects on health and medical insurance portfolios.

- February 2025: The government launched Cek Kesehatan Gratis, a nationwide free health screening program that reached tens of millions of citizens by year-end and raised preventive care awareness.

- January 2025: AIA Financial Indonesia extended its exclusive bancassurance partnership with Bank Central Asia to 2038, reinforcing bank-led distribution for protection and health products.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Indonesian health and medical insurance market as every rupiah of gross written premium collected by the public Jaminan Kesehatan Nasional program and by licensed private medical insurers, whether the policy is sold to an individual or through an employer, and whether benefits cover inpatient, outpatient, or outpatient drug therapies. Premiums are recorded at original value, net of any re-insurance recoveries.

Scope exclusion: Personal-accident riders, stand-alone critical-illness, micro-travel, and accident-only policies are kept outside our calculation.

Segmentation Overview

- By Insurance Product Type

- Private Medical Insurance (PMI)

- Individual Policy Coverage

- Group Policy Coverage

- Public / Social Security Schemes

- Private Medical Insurance (PMI)

- By Distribution Channel

- Brokers / Agents

- Banks (Bancassurance)

- Direct-to-Consumer

- Other Channels (Affinity, Associations, etc.)

- By End-user Segment

- Individuals / Households

- SMEs

- Large Corporates

Detailed Research Methodology and Data Validation

Primary Research

We interview regulators, hospital procurement heads, actuaries, and digital-broker founders across Java, Sumatra, and Kalimantan. Their insights on penetration rates, average premium progression, and emerging product mixes close data gaps flagged during desk work and sharpen scenario inputs.

Desk Research

Mordor analysts first map the regulatory, demographic, and cost environment using sources such as Indonesia's OJK solvency returns, BPJS Kesehatan enrollment dashboards, Ministry of Health hospital-utilization datasets, World Bank income series, and peer-reviewed studies on medical inflation. Annual reports and investor presentations from leading carriers enrich channel-split assumptions, while D&B Hoovers and Dow Jones Factiva supply structured premium and claims time series. The list is illustrative; many additional datasets inform cross-checks and contextual understanding.

Market-Sizing & Forecasting

The model blends one top-down reconstruction of premiums drawn from regulator and trade data with selective bottom-up carrier roll-ups to verify product splits. Key inputs include GDP per capita growth, medical cost inflation, JKN membership trend, private-bed additions, and digital channel uptake. A multivariate regression projects these variables, and scenario analysis adjusts for currency swings and benefit reforms.

Data Validation & Update Cycle

Outputs pass automated variance checks against independent health-spend ratios; then a senior analyst reviews anomalies before sign-off. Reports refresh each year, with interim updates triggered by material policy or macro events.

Why Mordor's Indonesia Health and Medical Insurance Baseline Is Dependable

Published market values regularly diverge because firms differ on compulsory-scheme inclusion, data vintage, currency conversion, and price-inflation multipliers. Our disciplined variable selection, yearly refresh, and transparent scope give decision-makers a stable, timely baseline.

Key gaps typically arise from whether JKN premiums are counted, how claim reimbursements are treated, and the breadth of ancillary covers folded into totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.65 billion (2025) | Mordor Intelligence | - |

| USD 21.82 billion (2024) | Global Consultancy A | Bundles life, accident, and ancillary covers; records claim payouts as revenue |

| USD 1.8 billion (2024) | Market Research Firm B | Omits JKN premiums and multi-employer group schemes |

This side-by-side view shows how our transparent scope choices let clients trace every number back to observable premiums, making Mordor Intelligence the dependable starting point for planning.

Key Questions Answered in the Report

What is the Indonesia health insurance market size and growth outlook to 2031?

The Indonesia health insurance market size is USD 1.77 billion in 2026 and is projected to reach USD 2.54 billion by 2031 at a 7.48% CAGR.

How does universal JKN coverage affect demand for private policies in Indonesia?

Near-universal JKN coverage shifts demand toward supplementary plans that fund hospital class upgrades, faster specialist access, and non-formulary medicines through coordination of benefits.

Which channels are set to drive the next wave of growth in Indonesia?

Direct-to-consumer and aggregator-led distribution will expand fastest, supported by OJK’s licensed Financial Service Aggregators and omnichannel bancassurance extensions.

Which end-user segments show the strongest momentum through 2031 in Indonesia?

SMEs record the fastest growth as formal benefits become a core hiring lever, while individuals and households remain the largest share due to upgrade-oriented needs.

How are OJK’s 2026 rules changing health insurance operations in Indonesia?

POJK 36 of 2025 requires medical governance, Medical Advisory Boards, utilization review, and stronger reporting, which improves transparency and product clarity.

What is pressuring health insurance pricing and design in Indonesia?

Persistent medical inflation and high inpatient cost intensity elevate loss ratios, prompting repricing and tighter managed care and pharmacy controls.

Page last updated on: