Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

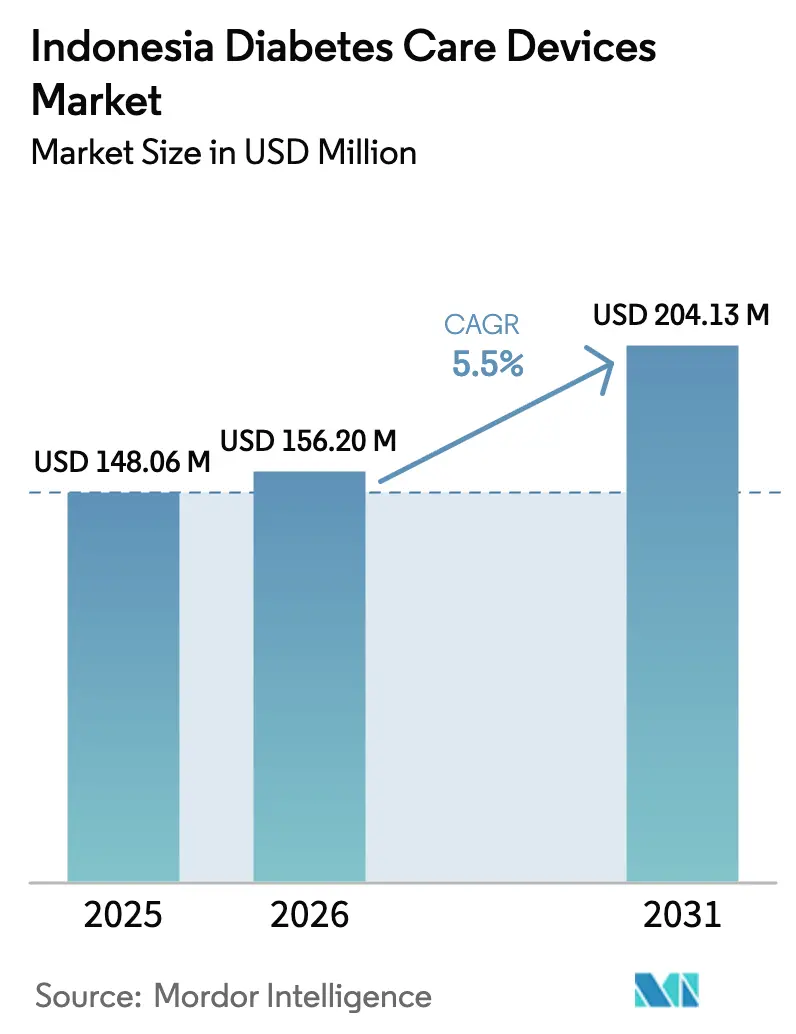

| Base Year Market Size (2025) | USD 148.06 Million |

| Market Size (2026) | USD 156.2 Million |

| Market Size (2031) | USD 204.13 Million |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Diabetes Care Devices Market Analysis by Mordor Intelligence

The Indonesia diabetes care devices market size was valued at USD 148.06 million in 2025 and estimated to grow from USD 156.2 million in 2026 to reach USD 204.13 million by 2031, at a CAGR of 5.50% during the forecast period (2026-2031). Demand accelerates as Indonesia registers 19.5 million diagnosed cases, a figure expected to climb to 28.5 million by 2045 [1]Source: Ministry of Health, “Cegah Dini Ancaman Diabetes,” indonesia.go.id. Rising public-sector health spending, expanded BPJS Kesehatan reimbursement, and government screening programs are expanding patient access to monitoring and management technologies. Universal Health Coverage, coupled with stronger local-content mandates, is creating a dual pathway of import substitution and multinational partnerships that support device affordability and supply security. At the same time, growing consumer interest in proactive health tracking is pushing wearable glucose technologies into mainstream retail channels, offering new growth levers for manufacturers that can align with Indonesia’s price-sensitive yet digitally engaged population

Key Report Takeaways

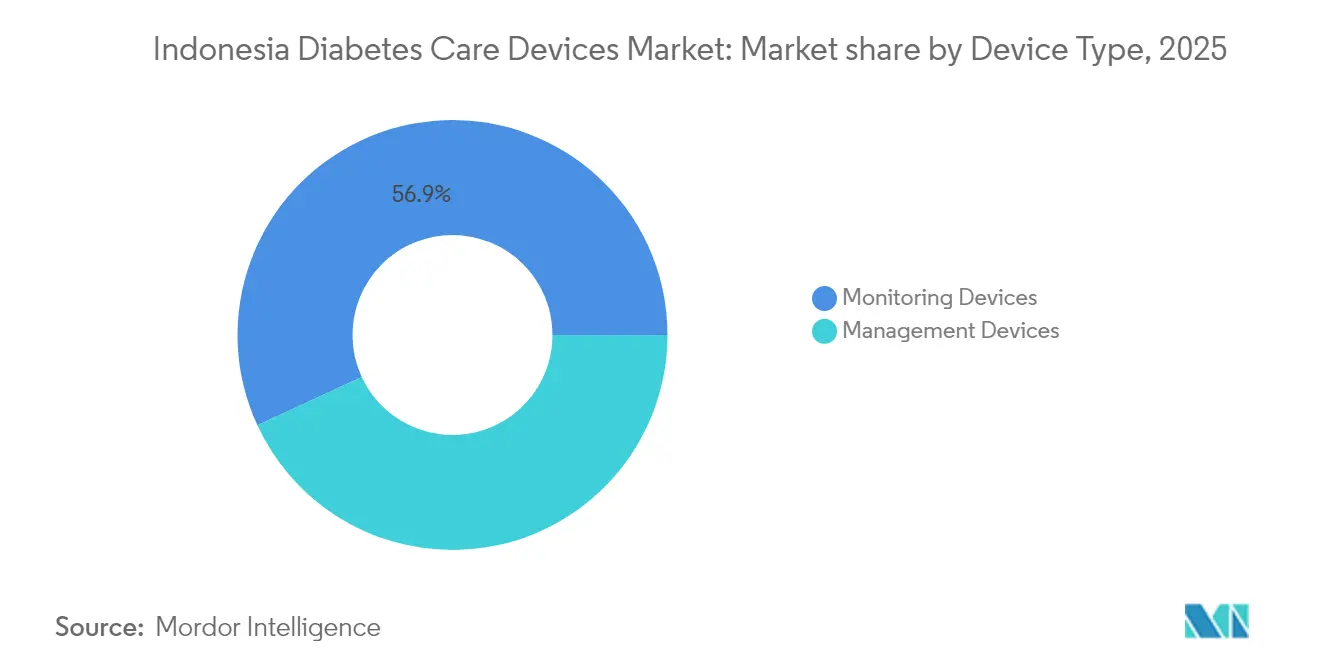

- By device type, Monitoring Devices accounted for 56.90% of the Indonesia diabetes care devices market share in 2025, while the Management Device is projected to expand at a 6.02% CAGR through 2031.

- By patient type, Type-2 diabetes accounted for 84.10% of the Indonesia diabetes care devices market share in 2025, while the Type-1 segment is projected to expand at a 6.95% CAGR through 2031.

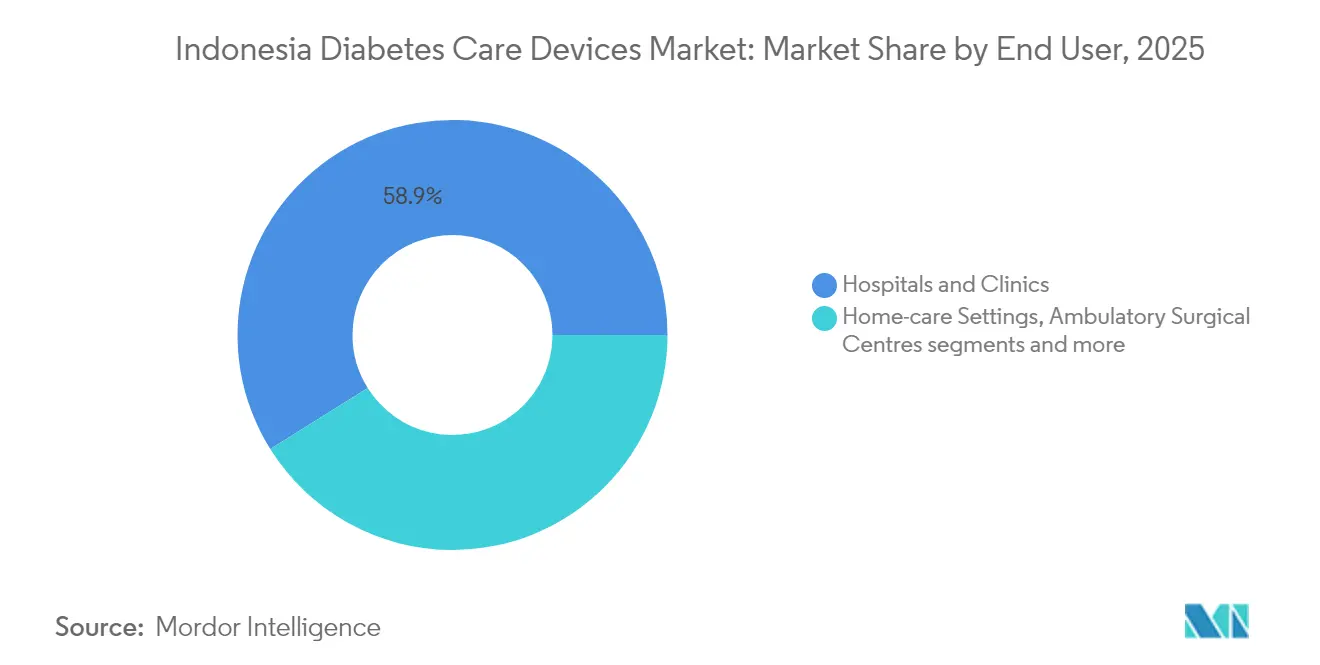

- By end user, hospitals and clinics held 58.90% share of the Indonesia diabetes care devices market size in 2025, whereas home-care settings are advancing at a 6.65% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Diabetes Care Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes prevalence & earlier diagnosis | +1.8% | National, concentrated in Java and urban centers | Medium term (2-4 years) |

| Expansion of BPJS national health insurance coverage | +1.2% | National, with stronger impact in rural areas | Long term (≥ 4 years) |

| Growing adoption of SMBG devices via awareness campaigns | +0.9% | National, with emphasis on Tier-2 and Tier-3 cities | Short term (≤ 2 years) |

| Shift to insulin-analog pens improving adherence | +0.7% | Urban centers, gradually expanding to rural areas | Medium term (2-4 years) |

| Local-content (TKDN) mandates spurring domestic production | +0.6% | National, with manufacturing hubs in Java | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence & Earlier Diagnosis

Indonesia ranks fifth globally for diabetes cases. IDF data show 19.5 million Indonesians living with diabetes in 2024, yet over 70% of cases were undiagnosed until recent screening initiatives[2]Source: DetikHealth, “Indonesia Peringkat Ke-5 dengan Kasus Diabetes Terbanyak di Dunia,” detik.com . Earlier detection programs in Java’s densely populated provinces are elevating demand for entry-level glucometers as well as next-generation continuous glucose monitors. As demographic ageing accelerates and lifestyles shift toward urban sedentary patterns, the Indonesia diabetes care devices market is likely to see sustained baseline growth in device volumes.

Expansion of BPJS National Health Insurance Coverage

BPJS Kesehatan now enrolls 98% of citizens and lists both Type-1 and Type-2 diabetes among its 144 reimbursable conditions. The abolition of inpatient class distinctions in 2025 further lowers out-of-pocket costs for glucose testing supplies. Reliable reimbursement is fostering broader distribution of test strips into rural clinics where private purchasing power remains limited.

Growing Adoption of SMBG Devices via Awareness Campaigns

Government free-screening drives under the “Cek Kesehatan Gratis” program emphasize routine blood glucose testing. Educational tools—such as game-based learning modules—have improved patient knowledge scores twofold and cut average blood glucose readings by nearly 73 mg/dL. Cheaper locally assembled meters and test strips are appearing in e-catalogs, meeting budget constraints while aligning with TKDN requirements.

Shift to Insulin-Analog Pens Improving Adherence

Clinical studies identify complex dosing regimens and cultural misperceptions as primary barriers to insulin use. Analog pens simplify administration, and local fill-finish tie-ups—Novo Nordisk with Bio Farma and PT Kalbe Farma’s Ezelin line—lower retail prices by shortening supply chains. Integration with Bluetooth-enabled CGM platforms is generating real-time feedback loops that sustain adherence gains and underpin growth in the Indonesia diabetes care devices market

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of imported CGM & insulin pumps | -1.4% | National, more pronounced in rural and lower-income areas | Medium term (2-4 years) |

| Fragmented distribution & counterfeit strips | -0.8% | National, particularly affecting rural supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Imported CGM & Insulin Pumps

Average per-capita diabetes spending is forecast to rise 33% from USD 323.8 in 2021 to USD 431.7 by 2045. Imported closed-loop pump systems retail well above annual median household healthcare budgets, constraining uptake to affluent urban cohorts. Although BPJS covers essential devices, reimbursement ceilings lag behind international list prices, limiting scale.

Fragmented Distribution & Counterfeit Strips

Indonesia’s maritime geography complicates cold-chain and quality assurance. Roche’s 2024 lawsuit revealed counterfeit Accu-Chek products stored in several e-commerce warehouses. Pharmacist shortages—121,000 practitioners versus the 251,000 required—reduce supervision, especially outside Java. CDAKB certification, mandatory from July 2024, aims to raise distribution standards, yet field enforcement across 17,000 islands remains resource-intensive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Management Devices Drive Innovation

The Indonesia diabetes care devices market continues to be anchored by self-monitoring blood glucose systems, yet software-enabled insulin delivery platforms are now the fastest-growing line. Test strips, lancets, and basic meters dominate unit volumes, serving millions of BPJS-covered patients who rely on routine finger-stick testing for glycemic control. Continuous glucose monitoring (CGM) adoption is advancing as domestic assemblers push prices down and health-app integration attracts younger users.

Management devices—including insulin pens, pumps, and jet injectors—are set for robust expansion throughout the forecast window. Local fill-finish capacity is lowering landed costs for analog insulin cartridges, while partnerships like Abbott-Medtronic bring automated basal-bolus algorithms to market. As reimbursement schedules are periodically revised, more sophisticated devices are expected to migrate from private specialty clinics into public tertiary hospitals, reinforcing the overall revenue mix of the Indonesia diabetes care devices market.

By Patient Type: Type-1 Growth Outpaces Prevalence

Type-2 patients constitute the broadest treatment base, propelled by lifestyle risk factors and ageing demographics. Universal coverage makes SMBG kits widely accessible, and public campaigns that target diet and exercise are expected to temper incident growth but will not materially shrink the addressable pool during the next decade. BPJS subsidies have also improved gestational diabetes management, an area gaining attention through expanded maternal-child health programs.

Type-1 diabetes represents a smaller cohort yet posts the highest incremental device spend per capita. Improved pediatric referral pathways and heightened clinician awareness reduced misdiagnosis cases in 2024, unveiling a latent user base for real-time glucose sensing and smart pumps. Dedicated Type-1 clinics in Jakarta and Surabaya are piloting closed-loop studies, results of which could accelerate premium-tier adoption across other urban centers. Growing parental acceptance of wearable technology is thus positioning the Indonesia diabetes care devices market for sustained high-value unit growth in this segment.

By End User: Home-Care Settings Gain Momentum

Hospitals and clinics remain the leading purchase points for meters, strips, and insulin supplies. Specialist endocrinology centers in Java drive early adoption of closed-loop systems and provide patient training modules that ensure safe device usage. Government stimulus, including infrastructure grants for regional hospitals, continues to widen institutional market depth.

Home-care, however, is registering the fastest CAGR as Indonesians gravitate toward self-management solutions. The “Cek Kesehatan Gratis” initiative is embedding screening stations in community venues, and telemedicine apps now deliver follow-up coaching to rural households. This digital pivot aligns with retail pharmacy expansion, where point-of-sale financing lowers upfront costs for starter kits. Integration of glucose data with national electronic medical records may further normalize at-home testing and therapy titration, broadening the distribution footprint of the Indonesia diabetes care devices market.

Geography Analysis

Java commands the lion’s share of national sales owing to its high population density, robust clinician base, and hospital network depth. Concentrated supply chains simplify distribution, allowing manufacturers to maintain tight inventory cycles and rapid device replacement programs. Urban consumers, familiar with wearable trackers, are piloting CGM adoption at a faster rate than the national average.

Sumatra and Kalimantan provide the next tier of opportunity. Rising household incomes and new provincial insurance top-ups are lifting demand for branded insulin pens. Government incentives to even out physician distribution—scholarships and rural service bonuses—are expected to improve patient education and bolster device adherence.

Eastern Indonesia, encompassing Maluku, Nusa Tenggara, and Papua, is under-penetrated yet offers long-run upside. Telehealth trials in these islands have demonstrated 18% mortality reductions for chronic disease patients engaging with mobile health platforms. As broadband connectivity expands and logistic nodes mature, the Indonesia diabetes care devices market will likely see a steeper diffusion curve for baseline monitoring kits, followed by gradual uptake of more advanced delivery devices

Competitive Landscape

The competitive field is moderately fragmented and influenced by localization policy. Abbott, Roche, and Medtronic provide globally recognized platforms, but their import pricing faces mounting pressure from TKDN rules that encourage sub-assembly partnerships. Abbott’s FreeStyle Libre sensor line offers strong brand pull, and its integration agreement with Medtronic’s pumps positions both firms to shape premium therapy segments.

Local players, notably PT Kalbe Farma, leverage cost advantages and public-sector procurement preferences. Kalbe’s Ezelin insulin range meets localization thresholds and enjoys stable e-catalog visibility, driving broader geographic reach than many imported brands. Bio Farma’s tie-up with Novo Nordisk further signals foreign interest in local fill-finish models.

Distribution integrity remains a differentiator. Roche’s anti-counterfeit litigation underscores the reputational stakes, prompting multinationals to fortify track-and-trace systems and invest in accredited wholesalers. As digital health ecosystems mature, companies that bundle devices, data dashboards, and tele-consult modules may secure sustainable defensibility in the Indonesia diabetes care devices market.

Indonesia Diabetes Care Devices Industry Leaders

Medtronic

Roche

Novo Nordisk

Abbott

Dexcom

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Indonesia launched the Rp 4.7 trillion “Cek Kesehatan Gratis” program, offering free check-ups for 280 million citizens

- July 2024: CDAKB certification became mandatory for device distributors.

Indonesia Diabetes Care Devices Market Report Scope

A glucose meter, commonly known as a "glucometer", is a device used in the medical field to estimate the concentration of glucose in the bloodstream. It can also involve a glucose paper strip that is immersed in a sample and then compared to a glucose chart. Thailand Diabetes Care Devices Market is segmented into devices. The report offers the value (in USD) and volume (in Units) for the above segments.

Monitoring Devices

| Self-monitoring Blood Glucose Devices | Glucometer Devices |

| Test Strips | |

| Lancets | |

| Continuous Blood Glucose Monitoring | Sensors |

| Durables |

Management Devices

| Insulin Pump | Insulin Pump Device |

| Insulin Pump Reservoir | |

| Infusion Set | |

| Insulin Syringes | |

| Insulin Cartridges | |

| Disposable Pens |

| Monitoring Devices | Self-monitoring Blood Glucose Devices | Glucometer Devices |

| Test Strips | ||

| Lancets | ||

| Continuous Blood Glucose Monitoring | Sensors | |

| Durables | ||

| Management Devices | Insulin Pump | Insulin Pump Device |

| Insulin Pump Reservoir | ||

| Infusion Set | ||

| Insulin Syringes | ||

| Insulin Cartridges | ||

| Disposable Pens | ||

Key Questions Answered in the Report

What is the current size of the Indonesia diabetes care devices market?

The market is worth USD 156.2 million in 2026 and is forecast to reach USD 204.13 million by 2031.

How fast is the Indonesia diabetes care devices market expected to grow?

The market is projected to post a 5.50% CAGR over 2026-2031.

Which patient segment is expanding the quickest?

Type-1 diabetes shows the fastest growth, advancing at a 6.95% CAGR as early diagnosis rates improve.

Why are home-care devices gaining momentum?

Government screening programs, telemedicine adoption, and retail financing are making self-management tools more affordable and convenient for patients.

How do local-content rules affect foreign manufacturers?

TKDN requirements push multinationals to localize sub-assembly or packaging, prompting strategic partnerships that balance compliance with technology transfer.

Page last updated on: