Indonesia Cement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

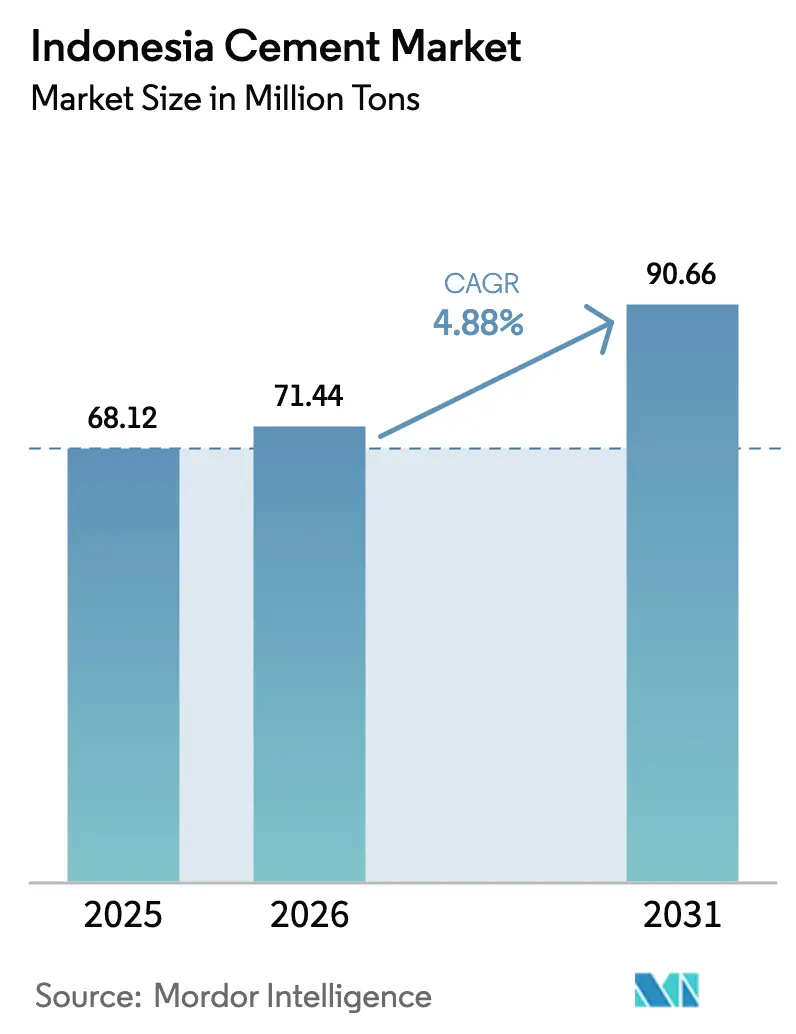

| Base Year Market Size (2025) | 68.12 Million tons |

| Market Volume (2026) | 71.44 Million tons |

| Market Volume (2031) | 90.66 Million tons |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

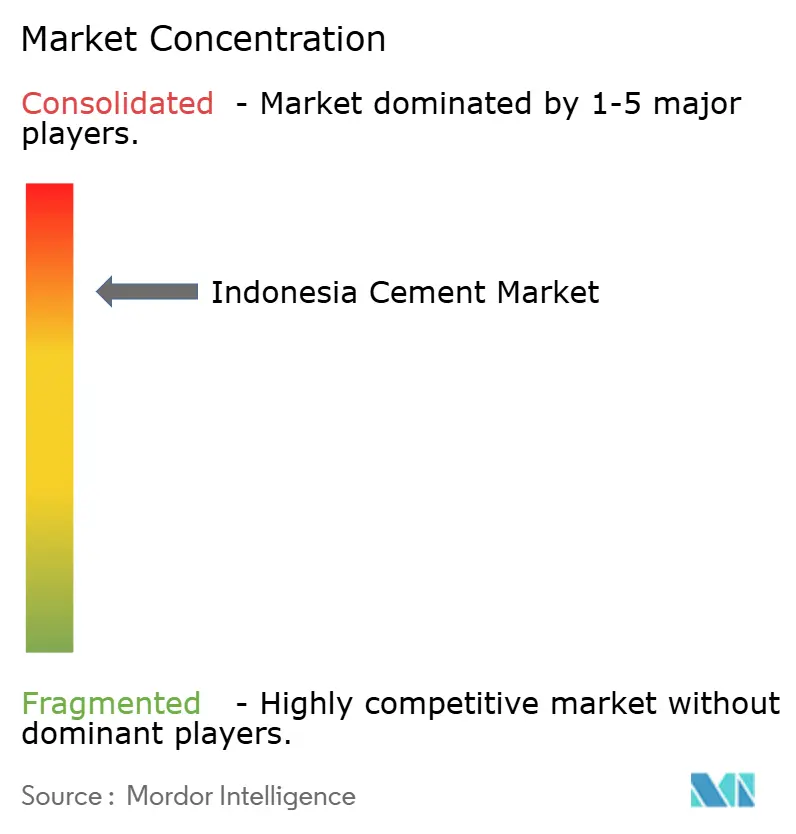

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Cement Market Analysis by Mordor Intelligence

Indonesia Cement Market size in 2026 is estimated at 71.44 million tons, growing from 2025 value of 68.12 million tons with 2031 projections showing 90.66 million tons, growing at 4.88% CAGR over 2026-2031. Volume growth rides on steady infrastructure spending, resilient urban housing demand, and a quickening pivot toward lower-carbon products that differentiate producers in an oversupplied environment. Competitive cost structures, abundant limestone reserves, and export-friendly logistics continue to anchor Indonesia’s regional supply advantage, yet chronic overcapacity and volatile coal prices keep margins thin and amplify the importance of operational efficiency. Large-scale public-works allocations, valued at USD 25.5 billion for 2025 alone, remain the single most reliable driver of bulk volumes as the government fast-tracks toll roads and the new capital city, Nusantara, while private investment in industrial estates supplies an additional demand lever. Concurrently, tightening emissions regulations push manufacturers to accelerate adoption of low-clinker and alternative-fuel technologies, aligning the Indonesia cement market with global decarbonization norms and elevating the strategic value of green cement.

Key Report Takeaways

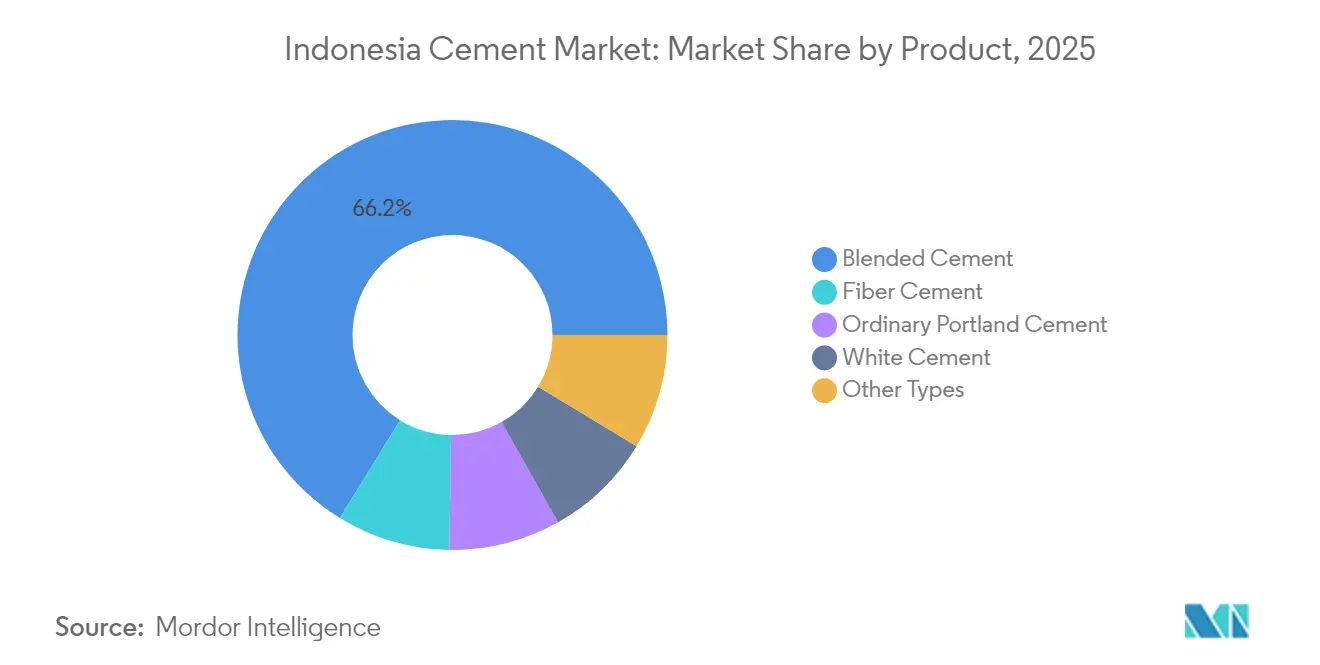

- By product category, blended cement led with a 66.22% Indonesia cement market share in 2025, while fiber cement recorded the fastest growth trajectory at a 5.61% CAGR through 2031.

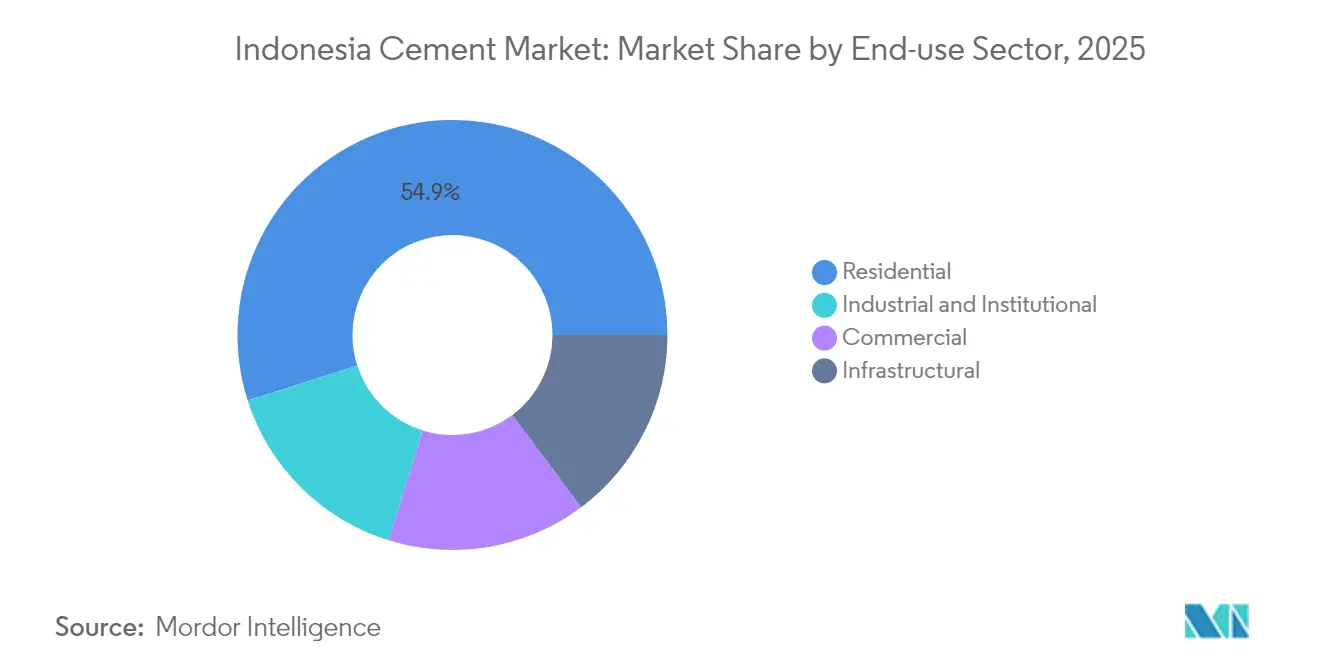

- By end-use sector, the residential segment accounted for 54.92% of the Indonesia cement market size in 2025, whereas industrial and institutional applications advanced at the highest 5.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Cement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government infrastructure push | +1.80% | National, Java & Kalimantan | Medium term (2-4 years) |

| Rapid urban housing demand | +1.40% | Java, Sumatra, key metros | Long term (≥ 4 years) |

| Capacity expansions with abundant limestone | +0.90% | National, strongest in Java & Sumatra | Short term (≤ 2 years) |

| Industrial-estate FDI inflows | +1.10% | Java industrial corridors, Batam, Bintan | Medium term (2-4 years) |

| Shift to low-clinker green cements | +0.60% | National, early uptake in Java | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure Push Accelerates Cement Demand

Public investment provides the Indonesia cement market with an unmatched demand floor as Parliament approved a USD 25.5 billion infrastructure allotment for 2025. Priority projects—Nusantara’s foundational works, 400 km of new toll roads, and expansion of Jakarta’s mass-rapid-transit network—consume substantial volumes of blended cement, concrete aggregates, and specialty binders. Nusantara’s Phase 1 development alone requires roughly 2.5 million tons of cement each year through 2027, setting a consistent pull on the Indonesia cement market even as private construction cycles fluctuate. Funding certainty shortens contractor payment schedules and lowers working-capital risk, giving producers a predictable sales pipeline. The push also spurs auxiliary demand for ready-mix facilities and bulk-haul logistics, prompting producers to modernize distribution fleets to capture time-sensitive orders.

Rapid Urban Housing Demand Outpaces Supply Capacity

Indonesia’s urban population grows at 2.3% annually, concentrating mainly in Jakarta, Surabaya, and emerging secondary cities where high-rise apartments outnumber traditional landed houses[1]Ministry of Public Works and Housing, “National Housing Program Update 2024,” PU.GO.ID . The 12.75 million-unit housing backlog intensifies pressure on developers to build vertically, thereby increasing cement use per square meter relative to low-rise dwellings. Vertical construction employs heavier concrete columns and shear-wall systems, utilizing up to 40% more cement per dwelling than single-story designs. Subsidized mortgage schemes and public-private partnerships accelerate presales, translating demand into actual ground-breakings that consume cement swiftly. Long-term urbanization also increases per-capita cement intensity beyond residential structures, as expanded utilities, mass transit, and commercial amenities embed additional cement in the built environment. These combined factors sustain multi-year demand visibility for the Indonesia cement market.

Capacity Expansions Backed by Abundant Limestone

Indonesia hosts plentiful limestone reserves proximate to Java and Sumatra industrial belts, enabling producers to add brownfield capacity with relatively low capital intensity. New grinding units and kiln upgrades come online within 18-24 months, a short window that can rapidly amplify national capacity. Producers leverage shorter lead times to capture anticipated demand from infrastructure contracts and export opportunities. While additions risk aggravating supply gluts, efficient new lines often replace older kilns, keeping operating costs competitive. Simultaneously, proximity to reserves cuts quarry-haul distances, moderating logistics expenses even amid fuel price swings. The continual refresh of asset bases underscores the dynamic nature of competition in the Indonesia cement market, where unit-cost leadership forms a core survival strategy.

Shift to Low-Clinker “Green” Cements

The Ministry of Industry’s decarbonization roadmap mandates a 30% emissions cut by 2030, compelling producers to reduce clinker factors and adopt alternative fuels. Early movers like SCG’s “Bezt Eco Friendly Cement” demonstrate commercial viability, registering 50 kg lower CO₂ per ton and meeting a 95% green-label score[2]SCG Indonesia, “Sustainable Cement Products Launch 2024,” SCG.COM . Small yet rising procurement preferences by property developers and multinational contractors already favor products that meet ESG criteria, giving compliant manufacturers an edge in tender bidding. Adoption of supplementary cementitious materials, such as fly ash and pozzolan, capitalizes on abundant local by-products, balancing cost and sustainability. The regulatory tempo signals permanence, motivating capital allocation toward calcined-clay trials, biomass co-firing, and waste-heat recovery systems that enhance competitiveness in the Indonesia cement market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic over-capacity and price wars | -0.70% | National, intensified in Java | Short term (≤ 2 years) |

| Volatile coal and power prices | -0.40% | National, coal-dependent regions | Medium term (2-4 years) |

| Stricter quarry-haulage limits | -0.30% | Limestone belts facing environmental zoning | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Overcapacity Triggers Price Competition

Installed capacity currently exceeds domestic demand by 15-20%, pressuring producers to protect utilization rates even at the expense of margins. Discounted spot pricing, free freight promotions, and flexible credit terms proliferate, eroding profitability throughout the Indonesia cement market. Smaller region-bound mills lacking export channels struggle to match price cuts, intensifying financial distress and potentially catalyzing further consolidation. The oversupply situation simultaneously fuels a 20.30% annual rise in clinker exports, where Indonesia leverages logistical proximity to Australia and South Asia. While exports relieve inventory build-ups, shipment volatility ties domestic producers to global price movements, complicating long-term planning.

Stricter Quarry-Haulage Limits

Environmental regulations increasingly impose haulage distance caps and dust-mitigation requirements on limestone trucking in Java and environmentally sensitive zones. New limits increase transport costs per ton, particularly for kilns sited far from quarries. The restrictions force an optimization of supply chains, including the relocation of grinding units closer to raw-material sources and the adoption of conveyor belts and closed-loop transport systems. Compliance investment raises capital needs, stretching balance sheets already pressured by price competition. Although stricter regulations ultimately curb community opposition and allow smoother permitting, the near-term impact curtails expansion enthusiasm and modestly dampens growth in the Indonesia cement market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Blended Cement Dominance Faces Green Innovation

Blended cement held a 66.22% Indonesia cement market share in 2025, a position built on reliable supply chains and cost-effective pozzolan mixes that align with mass-market contractor needs. At current trajectory, blended products will still form the bulk of the Indonesia cement market size in 2031, even as fiber cement expands at a 5.61% CAGR on the back of seismic-resilient public structures and light-weight panel systems. Moving beyond volumes, producers increasingly tweak blended recipes to integrate rice husk ash and calcined clays, cutting clinker content while maintaining compressive strength standards up to 40 MPa. These tweaks lower emissions and qualify for green-building credits that developers use to market eco-friendly housing projects.

Manufacturers also target higher margins through specialty binders. White cement appeals to decorative architects despite its small share, whereas sulfate-resistant and rapid-setting types find niche demand in marine infrastructure and accelerated repair work. PT Cemindo’s adoption of CarbonCure injection reduces cement use by 4% in select mixes, signaling how innovation can translate into cost savings even within mainstream segments. Over the forecast horizon, the Indonesia cement market will likely witness continued blended-cement primacy but with a progressive tilt toward low-carbon variants that align with national decarbonization pledges.

By End-Use Sector: Residential Leads While Industrial Accelerates

Residential construction captured 54.92% of the Indonesia cement market size in 2025, supported by mortgage subsidies and public-sector housing programs aiming for 3 million new units, which anchor baseline demand even during private-sector slowdowns. Demand spikes in mega-city suburbs spur larger condominium complexes that consume concrete at scale, while townhouses across satellite cities leverage standardized precast panels to cut build times. Though dominant, residential growth edges lower as developers pace new launches to absorb completed units.

Industrial and institutional construction, meanwhile, advances at a 5.74% CAGR through 2031, the fastest among all end-uses. Foreign capital inflows drive greenfield factories requiring heavy-load floors and chemical-resistant foundations, propelling specialized cement that carries premium pricing. Hospital and educational projects within public–private frameworks further widen institutional cement demand. Infrastructure applications—spanning roads, ports, and power plants—strengthen the Indonesia cement market by diversifying away from the cyclical property cycle, offering steadier, government-anchored procurement streams.

Geography Analysis

Java remains the principal demand hub, accounting for more than half of the Indonesia cement market in 2025 thanks to dense population centers, industrial clusters, and proximity to limestone reserves. Mature supply chains and multiple integrated plants allow just-in-time deliveries, bolstering contractor confidence in schedule adherence. Volume stability in Java encourages producers to pursue operational excellence, such as kiln-heat-rate optimization, as the primary avenue for cost reduction.

Sumatra follows as the significant consumer, fueled by palm oil processing capacity expansion and governmental road projects that require robust pavement designs. Although its logistics networks still develop, the island’s shorter transport routes between quarries and industrial towns present cost advantages that larger Java plants cannot easily match. Consequently, regional producers in Sumatra emphasize local sourcing and community engagement to secure long-term limestone concessions.

Kalimantan’s profile rises sharply due to the new capital, Nusantara, whose early-stage civil works create a fresh pull on the Indonesia cement market. Producers reconfigure shipping lanes and depot placements to accommodate demand in Balikpapan and Penajam, reducing transit time otherwise dominated by Java-borne supply. Sulawesi and Papua add modest but strategic volume increments, largely tethered to nickel smelters and mining infrastructure. Despite higher freight costs, these regions offer first-mover share capture opportunities, given sparse incumbent capacity. Collectively, regional variance in growth rates compels corporate strategies to balance asset utilization in Java with greenfield possibilities farther east, ensuring the Indonesia cement market retains a nationwide footprint.

Competitive Landscape

Indonesia cement market is consolidated in nature. Indocement’s 2024 acquisition of PT Semen Grobogan raised its individual share signaling an appetite for scale that can absorb fixed costs and negotiate better coal contracts. State-linked PT Semen Indonesia leverages extensive dealer networks and bulk transport fleets to keep volumes high despite price skirmishes, while regional specialists, such as PT Semen Tonasa, maintain footholds through local brand loyalty and government project ties.

International entrants Heidelberg Materials and Taiheiyo Cement Corporation inject technological expertise in kiln efficiency and low-clinker formulations, upping the innovation stakes. Digital control systems, predictive maintenance, and real-time quality analytics now differentiate operational leaders, trimming downtime and enhancing clinker-factor management. Export orientation further reshapes rivalry, as plants certified for Australia, Bangladesh, and the Philippines markets capture FX-denominated revenue that cushions domestic price dips. Environmental mandates accelerate differentiation; companies able to certify lower carbon footprints gain preferential status in government tenders and multinational supply chains, gradually shifting market share toward sustainability frontrunners.

Indonesia Cement Industry Leaders

Anhui Conch Cement Co., Ltd.

Heidelberg Materials (Indocement Tunggal Prakarsa)

PT Cemindo Gemilang Tbk

SIG

PT Semen Imasco Asiatic,

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Indonesia inaugurated the IDXCarbon trading platform at an opening price of USD 8 per ton CO₂, allowing cement producers to monetize verified emission reductions.

- July 2025: The Indonesian government is actively encouraging the domestic cement industry to explore export markets and develop environmentally friendly products as a strategy to address the oversupply challenge. This initiative is expected to enhance market competitiveness and drive sustainable growth within Indonesia's cement market.

Indonesia Cement Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Blended Cement, Fiber Cement, Ordinary Portland Cement, White Cement are covered as segments by Product.| Blended Cement |

| Fiber Cement |

| Ordinary Portland Cement |

| White Cement |

| Other Types |

| Residential |

| Commercial |

| Infrastructural |

| Industrial and Institutional |

| By Product | Blended Cement |

| Fiber Cement | |

| Ordinary Portland Cement | |

| White Cement | |

| Other Types | |

| By End-Use Sector | Residential |

| Commercial | |

| Infrastructural | |

| Industrial and Institutional |

Market Definition

- END-USE SECTOR - Cement consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of various types of cement such as ordinary portland cement, blended cement, white cement, fiber cement, etc. are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms