Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

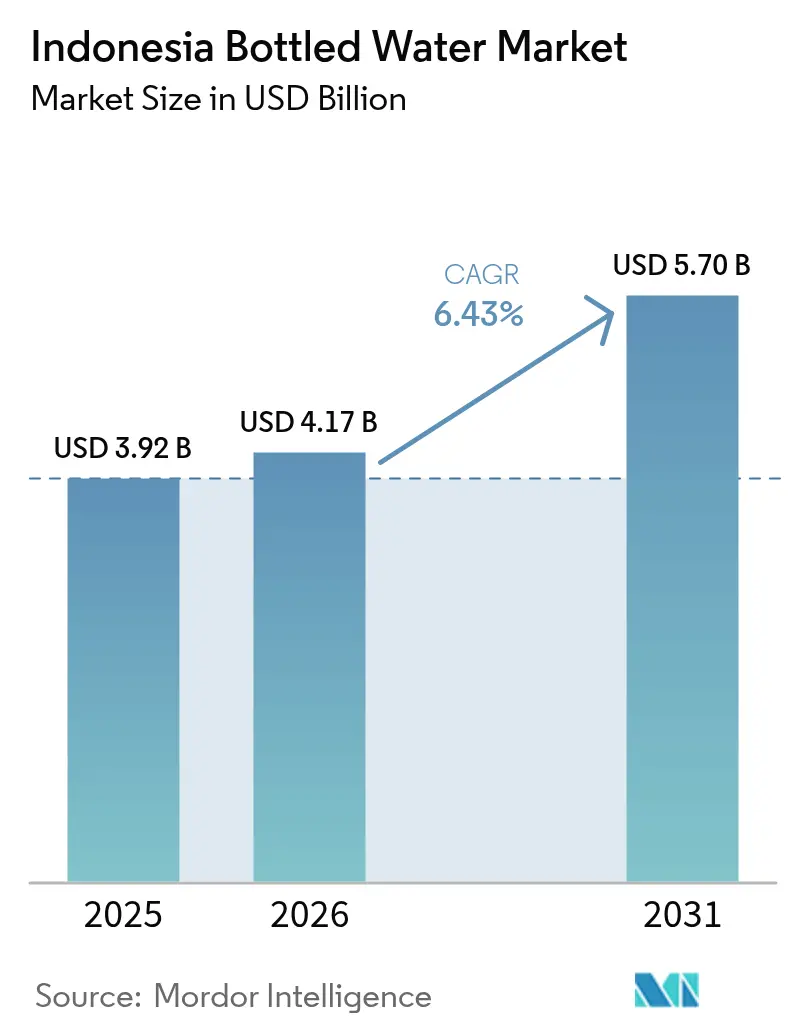

| Base Year Market Size (2025) | USD 3.92 Billion |

| Market Size (2026) | USD 4.17 Billion |

| Market Size (2031) | USD 5.7 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

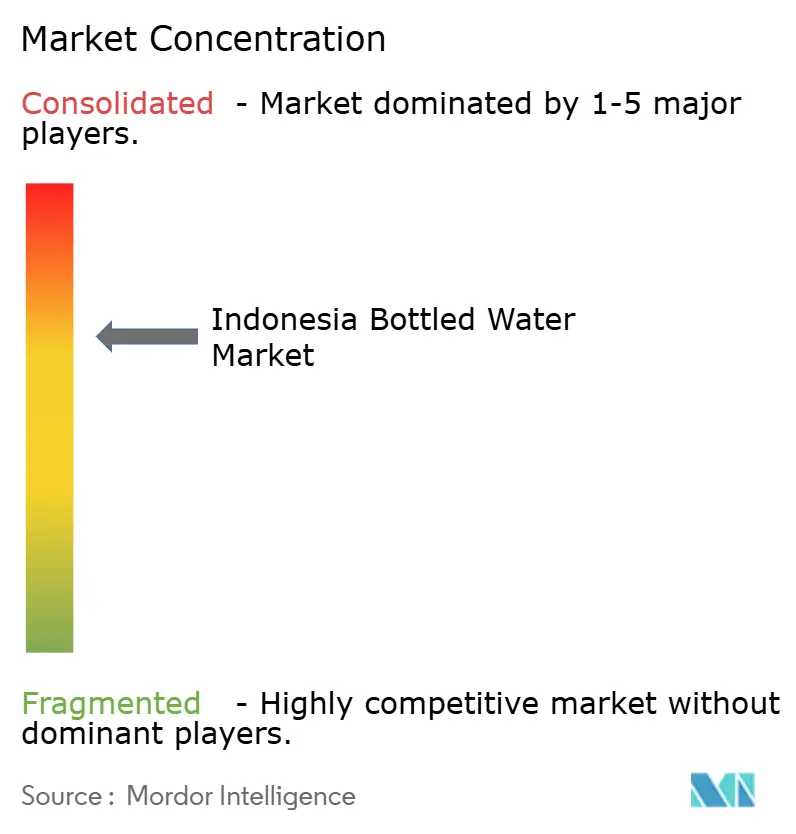

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Bottled Water Market Analysis by Mordor Intelligence

The Indonesian bottled water market size was valued at USD 3.92 billion in 2025 and estimated to grow from USD 4.17 billion in 2026 to reach USD 5.7 billion by 2031, at a CAGR of 6.43% during the forecast period (2026-2031). Today's demand showcases a significant pivot: most households now predominantly turn to branded or refillable drinking water, moving away from conventional sources. This shift is bolstered by rapid urbanization, heightened health consciousness, and enhanced distribution networks spanning the nation's 17,000 islands. While still water retains its dominance, there's a swift ascent in demand for functional and flavored variants, especially among health-conscious millennials. PET packaging leads the pack, but alternatives like recycled resin, label-free bottles, and glass formats are emerging, driven by growing sustainability concerns. To navigate the archipelago's diverse landscape, competitors are honing in on eco-design, establishing regional production hubs, and leveraging digital commerce to tap into both mass and premium market segments.

Key Report Takeaways

- By product type, still water led with an 88.15% revenue share in 2025; functional and flavored water together are projected to expand at an 8.32% CAGR through 2031.

- By packaging, PET commanded 88.68% of the Indonesian bottled water market share in 2025, while glass bottles recorded the fastest growth at an 8.05% CAGR.

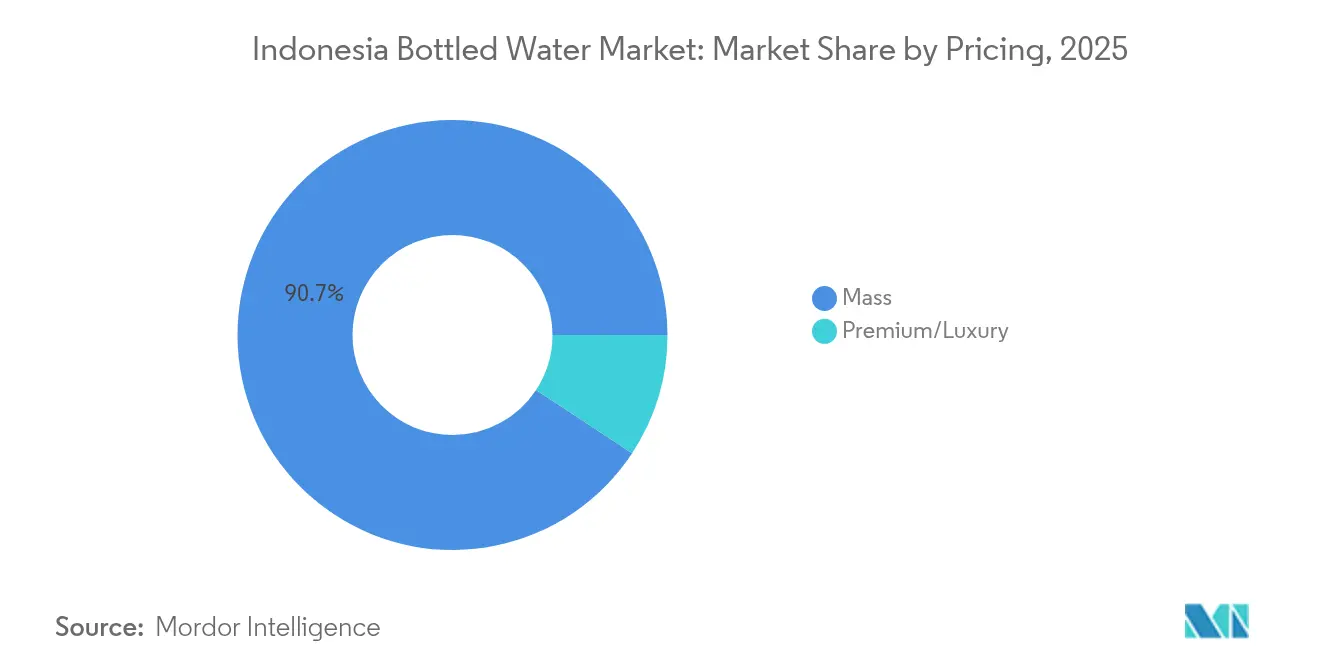

- By pricing tier, the mass segment captured 90.74% of the Indonesian bottled water market size in 2025; premium and luxury are set to rise at a 7.79% CAGR to 2031.

- By distribution, off-trade outlets held 77.95% share in 2025, whereas on-trade is recovering at a 7.44% CAGR on the back of hospitality growth.

- By region, Java accounted for 61.88% of the value in 2025, while Kalimantan represents the fastest-growing geography at a 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Bottled Water Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of premium and functional bottled water products | +1.2% | Java, Bali, urban centers nationwide | Medium term (2-4 years) |

| Innovative packaging solutions for convenience and environmental impact | +0.8% | National, with early adoption in Jakarta, Surabaya | Short term (≤ 2 years) |

| Rapid urbanisation boosting on-the-go hydration needs | +1.5% | Java, Sumatra, Kalimantan major cities | Long term (≥ 4 years) |

| Adoption of advanced purification and bottling technologies | +0.6% | National, concentrated in Java production hubs | Medium term (2-4 years) |

| Increasing health consciousness with shift from sugary drinks | +1.1% | Urban areas across all regions | Medium term (2-4 years) |

| Expansion of tourism and hospitality sector | +0.9% | Bali, Java, emerging destinations in Sulawesi | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth of premium and functional bottled water products

In Indonesia, the rise of premium and functional water segments is transforming traditional mass-market dynamics. Health-conscious consumers are increasingly gravitating towards alkaline and vitamin-enhanced products. A case in point is PT Sariguna Primatirta's foray into the high-pH market with its SuperO2 and Vio8+ offerings. Meanwhile, brands like Pristine 8.6+ are honing in on specific health benefits[1]Source: “10 Rekomendasi Mineral Water Terbaik,” Mybest, id.my-best.com. This segment's expansion is fueled by growing disposable incomes and marketing campaigns that tout functional water as a form of preventive healthcare. Niche brands, such as Kangen Water, are leveraging digital marketing, especially on platforms like Instagram and Facebook, to make inroads into urban markets. As a result of this premiumization trend, established players are discovering new revenue streams, while specialized brands find fertile ground among value-conscious consumers seeking more than just basic hydration.

Innovative packaging solutions for convenience and environmental impact

As environmental regulations tighten and consumers increasingly favor sustainability, packaging innovation has emerged as a key differentiator. MOUNTOYA has pioneered Indonesia's first label-free bottled water packaging, marking a significant step in curbing plastic waste without compromising product integrity or brand visibility. In a notable move, Coca-Cola, in collaboration with PT Amandina Bumi Nusantara, has rolled out bottles made entirely from recycled PET. This initiative underscores Coca-Cola's robust commitment to circular economy principles, with an ambitious target of achieving 50% rPET content across its entire portfolio by 2025[2]Source: Tijmen Veltkamp, “Recycled PET for Coca-Cola’s First 100 % rPET Bottles in Indonesia,” Recycling Inside, recyclinginside.com. Responding to the Indonesian government's new warning requirements on BPA leaching, innovators are pivoting towards BPA-free packaging materials, granting them a competitive edge. While premium brands champion sustainability messaging, driving an 8.16% CAGR growth in glass bottle segments, cost considerations pose challenges for broader market adoption.

Rapid urbanisation boosting on-the-go hydration needs

As commuting patterns and lifestyle changes shift consumption away from home, Indonesia's accelerating urbanization is driving a surge in demand for convenient, portable hydration solutions. With Indomaret and Alfamart boasting over 36,146 outlets nationwide, the expansion of convenience store networks is providing bottled water brands with an unprecedented distribution reach, as highlighted by Lloyds Bank Trade. In cities like Medan, where only 68% of fresh water needs are met, urban water infrastructure challenges are nudging consumers towards dependable bottled alternatives, according to the Journal of Economics and Behavioral Studies. E-commerce platforms are seizing this opportunity, with projections indicating significant growth in Indonesia's online retail market, thereby establishing new distribution channels for bottled water brands. Furthermore, a noticeable shift towards smaller packaging formats and multi-pack offerings underscores the evolving consumption patterns of urban professionals and students.

Adoption of advanced purification and bottling technologies

Bottled water producers are enhancing product quality and cutting operational costs through technology adoption. Dumai City Water Treatment Plant's use of NX Filtration's hollow-fibre nanofiltration technology exemplifies how advanced filtration can transform challenging sources, like peat water, into safe drinking water. PT Tirta Sukses Perkasa's ozone treatment system, paired with UV disinfection, highlights a multi-barrier approach. This method not only ensures consistent water quality but also optimizes monitoring intervals to every 4 hours, all while upholding safety standards, as noted by the Journal of Food Engineering. Thanks to these technological strides, producers are tapping into previously unusable water sources, all while adhering to stringent quality mandates. The adoption of ISO 22000:2005 certification is becoming the norm. PT Sariguna Primatirta has set a new industry benchmark as the first Indonesian bottled water company to secure this pivotal food safety certification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Microplastic and nanoplastic health concerns | -0.7% | National, particularly urban areas | Short term (≤ 2 years) |

| Water scarcity and sustainability issues | -1.1% | Bali, Java, drought-prone regions | Long term (≥ 4 years) |

| Price sensitivity and intense competition | -0.9% | Rural areas, price-conscious segments | Medium term (2-4 years) |

| Strict regulatory compliance and costs | -0.5% | National, affecting all producers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Microplastic and nanoplastic health concerns

Research by Buletin Keslingmas highlights a concerning trend: sun-exposed PET bottles contain 175 microplastic particles per liter, outpacing the 132.25 particles found in their unexposed counterparts[3]Source: Atyaf Umi Faizah, “A Comparative Study About The Amount Of Microplastic,” Buletin Keslingmas, ejournal.poltekkes-smg.ac.id. In Makassar, assessments by the Global Journal of Environmental Science and Management identified risk quotients exceeding 1 for PET microplastic exposure, indicating potential organ inflammation and shifts in the immune system[4]Source: S. Kasim et al., “Environmental Health Risks from PET Microplastics,” Global Journal of Environmental Science and Management, gjesm.net. These alarming findings are prompting consumers to opt for pricier glass packaging and more sophisticated filtration systems. Responding to this heightened awareness, the Indonesian government has mandated warnings for BPA leaching, underscoring the mounting regulatory focus on packaging safety. This move could hasten the shift to alternative materials. In tandem, companies are investing significant resources in research and development for safer packaging solutions, although the associated transition costs pose challenges, particularly for smaller entities, which may compromise their short-term profitability.

Water scarcity and sustainability issues

Water resource constraints are intensifying across Indonesia's key markets. In Bali, the tourism sector consumes 65% of available fresh water resources, creating conflicts between commercial and community needs, according to the Global Sustainable Tourism Council. Surabaya faces a projected water deficit of 3,062 liters per second by 2024, highlighting infrastructure limitations that could restrict bottled water production capacity, as reported by IOP Conference Series: Earth and Environmental Science. Climate change impacts are worsening seasonal water availability variations, compelling producers to diversify source locations and invest in water conservation technologies. The Indonesian government's Indonesia Emas 2045 vision prioritizes sustainable water management, which may result in stricter extraction regulations and higher compliance costs for bottled water companies, according to the Persatuan Perusahaan Air Minum Seluruh Indonesia. These sustainability requirements are driving innovation in water recycling and conservation technologies, though implementation costs may limit growth for resource-intensive operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Still Water Dominance Amid Functional Innovation

In 2025, still water commands a dominant 88.15% market share, underscoring Indonesian consumers' preference for pure hydration. Yet, the functional and flavored water segments are surging, boasting an 8.32% CAGR through 2031. This growth is largely fueled by health-conscious millennials and Gen Z, who are on the lookout for added nutritional benefits. While sparkling water has traditionally occupied a niche, it's now gaining momentum, especially in urban locales and upscale dining, with expatriates leading the charge. The functional water realm, which includes alkaline, vitamin-enhanced, and oxygenated variants, sees brands like SuperO2 and Pristine 8.6+ making waves with targeted health claims.

Companies are redefining the functional water arena with premium positioning strategies, using scientific research as a tool to command higher prices and stand apart from standard still water. PT Sariguna Primatirta's foray into diverse functional variants is a testament to how industry stalwarts are capitalizing on the premiumization trend. Digital marketing, especially on social media, plays a pivotal role in this segment's growth, enlightening consumers about health benefits and resonating particularly with younger audiences. Meanwhile, BPOM's stringent food safety regulations bolster quality assurance across all water types, instilling consumer confidence and bolstering premium pricing for functional variants.

By Packaging Material: PET Dominance Challenged by Sustainability

In 2025, PET bottles dominate the market with an 88.68% share, thanks to their cost efficiency, lightweight nature, and well-established supply chains spread across Indonesia's diverse geography. Meanwhile, glass bottles are rapidly gaining traction, boasting the fastest growth rate at an 8.05% CAGR. Their rise is fueled by a premium market positioning, heightened sustainability concerns, and their ability to preserve taste, making them a favorite among discerning consumers. Although aluminum cans and bottles hold a smaller market share, they're witnessing growth, especially in the functional and sparkling water segments. Here, the metallic packaging not only boosts perceived quality but also enhances shelf appeal.

As environmental regulations tighten and awareness of plastic pollution rises, the packaging industry is witnessing a significant transformation. In a notable move towards circular economy principles, Coca-Cola, via PT Amandina Bumi Nusantara, has rolled out 100% recycled PET bottles. This initiative sees the company processing a substantial 3,000 tonnes of used PET bottles monthly, as highlighted by Starlinger. Further underscoring the industry's shift, AQUA has pledged to incorporate 50% recycled content by 2025, while MOUNTOYA is making waves with its label-free packaging innovation. These moves highlight how sustainability is evolving into a key competitive edge. Additionally, with the Indonesian government mandating warnings on BPA leaching, there's a swift pivot towards BPA-free materials. This shift not only underscores a commitment to health and safety but also opens doors for innovative packaging solutions that harmonize cost, convenience, and environmental stewardship.

By Pricing: Mass Market Stability with Premium Growth

In 2025, mass market segments command a dominant 90.74% share, underscoring Indonesia's price-sensitive consumer landscape where affordability drives household purchases. Meanwhile, premium and luxury segments are on a growth trajectory, expanding at a 7.79% CAGR through 2031. This surge is buoyed by rising disposable incomes within Indonesia's burgeoning middle class, projected to swell to 135 million by 2030, as reported by Food Export. The pricing dynamics mirror the nation's economic stratification: urban consumers are increasingly inclined to pay a premium for perceived health benefits, enhanced taste, and eco-friendly packaging. Companies are honing their pricing strategies, adeptly segmenting portfolios to harness value across diverse income brackets.

PT Sariguna Primatirta exemplifies this nuanced approach with its multi-brand strategy. Cleo caters to the mass market, while SuperO2 and Vio8+ are tailored for health-conscious premium consumers, as highlighted by IDN Financials. The premium segment's ascent is bolstered by educational marketing, spotlighting quality differentiators, source purity, and cutting-edge processing technologies. E-commerce platforms are revolutionizing premium product distribution, slashing traditional retail markups and fostering direct-to-consumer ties that justify elevated price points. However, BPOM's halal certification mandates, as per PP No. 42 Tahun 2024, introduce added compliance costs. While these may squeeze margins in price-sensitive segments, they simultaneously bolster the premium stature of certified products.

By Distribution Channel: Off-Trade Dominance with On-Trade Recovery

In 2025, off-trade channels command a dominant 77.95% market share, led by convenience stores, supermarkets, and traditional retail outlets, ensuring widespread accessibility across Indonesia's varied landscape. Meanwhile, on-trade channels are witnessing a robust growth rate of 7.44% CAGR through 2031, fueled by a resurgence in the hospitality sector, a boom in tourism, and modernizing foodservice initiatives. Convenience giants, Indomaret and Alfamart, are pushing their boundaries beyond Java island, unlocking fresh distribution avenues for bottled water brands in regions previously deemed underserved.

The distribution scene is undergoing a seismic shift, with e-commerce platforms taking center stage. TikTok Shop, now a formidable e-commerce contender, finds a significant foothold in Indonesia, boasting nearly 70% of its regional user base, thus paving the way for novel digital distribution avenues for bottled water brands. While traditional markets still command a hefty 76% share of the food and beverage sector, they're gradually ceding territory to modern retail formats. These newer formats, as highlighted by the USDA, excel in inventory management and boast cold chain capabilities, both crucial for effective bottled water distribution. Looking ahead, the Indonesian retail sector anticipates a 5% growth in 2025, spurred by collaborations between modern retailers and traditional outlets. This partnership is forging integrated distribution networks, amplifying market reach for bottled water brands.

Geography Analysis

In 2025, Java island commands a dominant 61.88% market share, capitalizing on its dense population, advanced infrastructure, and well-established distribution networks for efficient market penetration. Kalimantan, with a robust 7.12% CAGR projected through 2031, is reaping rewards from its natural resource developments, infrastructure investments, and initiatives aimed at economic diversification, all of which are broadening its consumer base. Sumatra boasts a diverse economic landscape, spanning agriculture to manufacturing, while Sulawesi is poised for growth, driven by tourism and budding industrial hubs. As companies look to expand beyond the saturated markets of Java, regional growth strategies are becoming paramount. PT Sariguna Primatirta is making a bold move with a planned Rp 600 billion capital expenditure in 2025, setting up new facilities in Palu, Pontianak, and Pekanbaru, underscoring its commitment to geographic diversification and cutting logistics costs.

Indonesia's Proyek Strategis Nasional has not only generated a whopping Rp 1,993 trillion in economic output but also created 5.4 million jobs, enhancing market access in previously neglected areas, according to ERIA. As the tourism sector flourishes, emerging destinations are witnessing a surge in demand. Notably, Bali's tourism, which accounts for 65% of the island's fresh water consumption, underscores the sector's profound influence on bottled water trends. The "Rest of Indonesia" segment includes a myriad of smaller islands and budding markets. Here, infrastructure advancements and economic growth are paving the way for new bottled water distribution avenues. However, these regions present logistical hurdles and sparser populations, necessitating tailored market entry approaches.

Competitive Landscape

In the competitive landscape, Danone-AQUA, Le Minerale, and Cleo dominate with the largest volumes. Leveraging a legacy of half a century, AQUA boasts a distribution network that spans 97% of modern retail outlets and has committed to incorporating 50% recycled content by 2025. PT Mayora Indah capitalizes on snack-beverage synergies, promoting Le Minerale through strategic cross-promotions. Cleo sets itself apart with a low-TDS positioning and has unveiled an ambitious IDR 600 billion expansion plan, establishing plants in Palu, Pontianak, and Pekanbaru.

Sustainability has emerged as a pivotal focus. Coca-Cola's introduction of a 100% rPET bottle and MOUNTOYA's innovative label-free packaging have set new benchmarks for consumer expectations. Meanwhile, smaller regional players are weaving artisanal spring narratives and community initiatives into their branding to cultivate loyalty. While larger firms leverage technology, like real-time quality monitoring, to bolster their credibility, newcomers are finding success with compact modular lines, allowing them to align production with demand. Regulatory changes, such as BPA labeling and halal mandates, pose challenges. These shifts not only benefit well-capitalized incumbents but also highlight innovators whose compliance stories resonate with the millennial demographic in Indonesia's bottled water sector.

E-commerce is reshaping traditional retail dynamics, enabling direct-to-consumer brands to emerge swiftly through targeted advertising. TikTok's algorithm, with its emphasis on storytelling, is successfully converting trend-focused youth into product trialists. Bottlers are forging strategic partnerships with logistics-tech companies, ensuring the integrity of last-mile cold-chain deliveries. Industry associations are advocating for incentives on recycled content to mitigate associated cost premiums. Despite these developments, opportunities remain in functional water, rural market penetration, and package-free dispensers. Brands that can seamlessly blend environmental responsibility with affordability are poised to influence market share trends leading up to 2030.

Indonesia Bottled Water Industry Leaders

The Coca-Cola Company

Nestle SA

Danone SA

PT Mayora Indah Tbk

PT Sariguna Primatirta Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: PT Sariguna Primatirta Tbk (CLEO) announced Rp 600 billion capital expenditure allocation for 2025 to enhance production and distribution capacity, focusing on expanding existing factories and developing new facilities in Palu, Pontianak, and Pekanbaru.

- November 2024: Coca-Cola launched 100% recycled PET bottles in Indonesia through a partnership with PT Amandina Bumi Nusantara, marking a significant sustainability milestone for the beverage industry. The initiative processes 3,000 tonnes of used PET bottles monthly and supports Coca-Cola's target of 50% rPET content across its portfolio by 2025.

- April 2024: PT Amandina Bumi Nusantara received the SNI Marking Product Certificate as the first PET recycling firm to meet national quality standards for food and beverage packaging. The certification enables the production of food-grade recycled PET for major beverage companies, including Coca-Cola's sustainability initiatives.

- February 2024: Kementerian Perindustrian issued Permenperin No. 8 Tahun 2024, governing procedures for technical considerations and import recommendations for upstream chemical industry commodities. The regulation affects the bottled water industry supply chains by establishing a framework for import compliance and industry capability verification.

Indonesia Bottled Water Market Report Scope

Bottled water is drinking water packaged in plastic or glass bottles. Bottled water may be carbonated or not. Sizes range from small single-serving bottles to large carboys for water coolers. The Indonesian bottled water market is segmented by product type and distribution channel. By product type, the market is segmented into still water, sparkling water, and functional water. By distribution channel, it is segmented into supermarkets and hypermarkets, convenience stores, online retailers, on-trade, and other distribution channels. The report offers market size and forecasts for the bottled water market in terms of value (USD million) for all the above segments.

By Product Type

| Still Water |

| Sparkling Water |

| Functional Water |

| Flavoured Water |

By Packaging Material

| PET Bottles |

| Glass Bottles |

| Aluminum Cans and Bottles |

| Others |

By Pricing

| Mass |

| Premium/Luxury |

By Distribution Channel

| On-trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Home and Office Space | |

| Online Retail | |

| Other Off-trade channels |

By Region

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Rest of Indonesia |

| By Product Type | Still Water | |

| Sparkling Water | ||

| Functional Water | ||

| Flavoured Water | ||

| By Packaging Material | PET Bottles | |

| Glass Bottles | ||

| Aluminum Cans and Bottles | ||

| Others | ||

| By Pricing | Mass | |

| Premium/Luxury | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Home and Office Space | ||

| Online Retail | ||

| Other Off-trade channels | ||

| By Region | Java | |

| Sumatra | ||

| Kalimantan | ||

| Sulawesi | ||

| Rest of Indonesia | ||

Key Questions Answered in the Report

What is the current value of the Indonesia bottled water market?

The market is valued at USD 4.17 billion in 2026 and is forecast to reach USD 5.7 billion by 2031.

Which product type leads sales in Indonesia?

Still water dominates with an 88.15% share in 2025, though functional and flavored waters post the fastest growth.

How fast is the premium bottled water segment expanding?

Premium and luxury offerings are advancing at a 7.79% CAGR, driven by rising disposable incomes and health awareness.

Which region is the fastest-growing market inside Indonesia?

Kalimantan leads with a projected 7.12% CAGR through 2031, supported by infrastructure development and rising incomes.

Page last updated on: