Tractors Market Size

| Study Period | 2019 - 2029 |

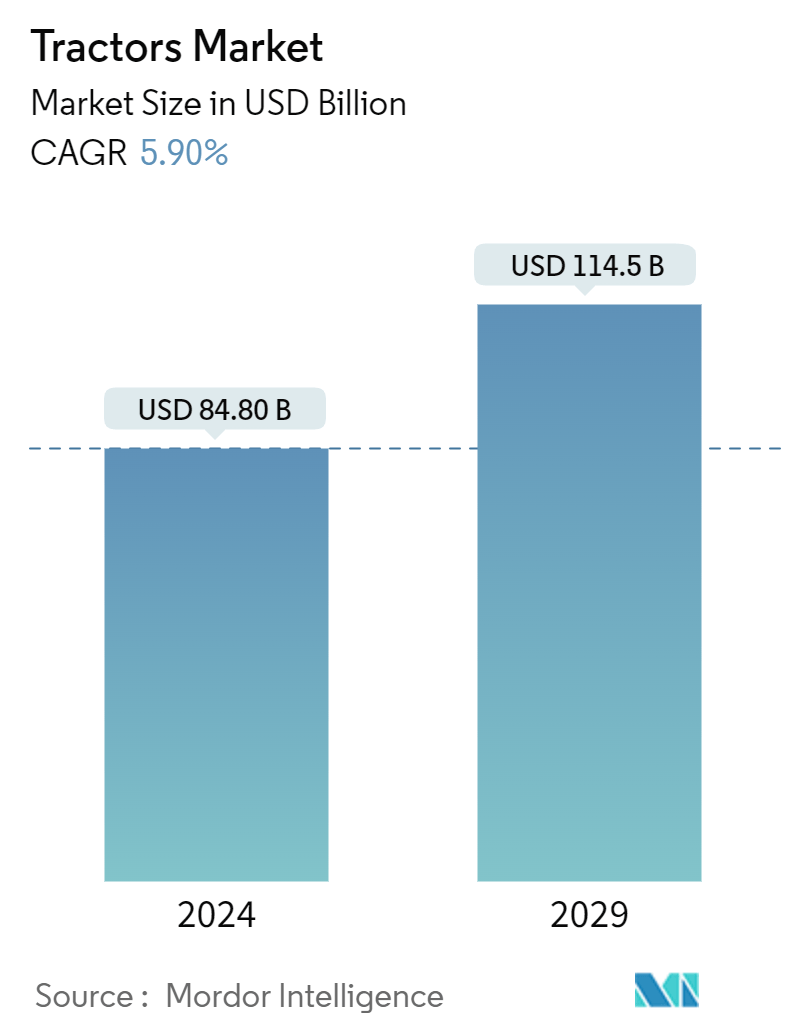

| Market Size (2024) | USD 84.80 Billion |

| Market Size (2029) | USD 114.5 Billion |

| CAGR (2024 - 2029) | 5.90 % |

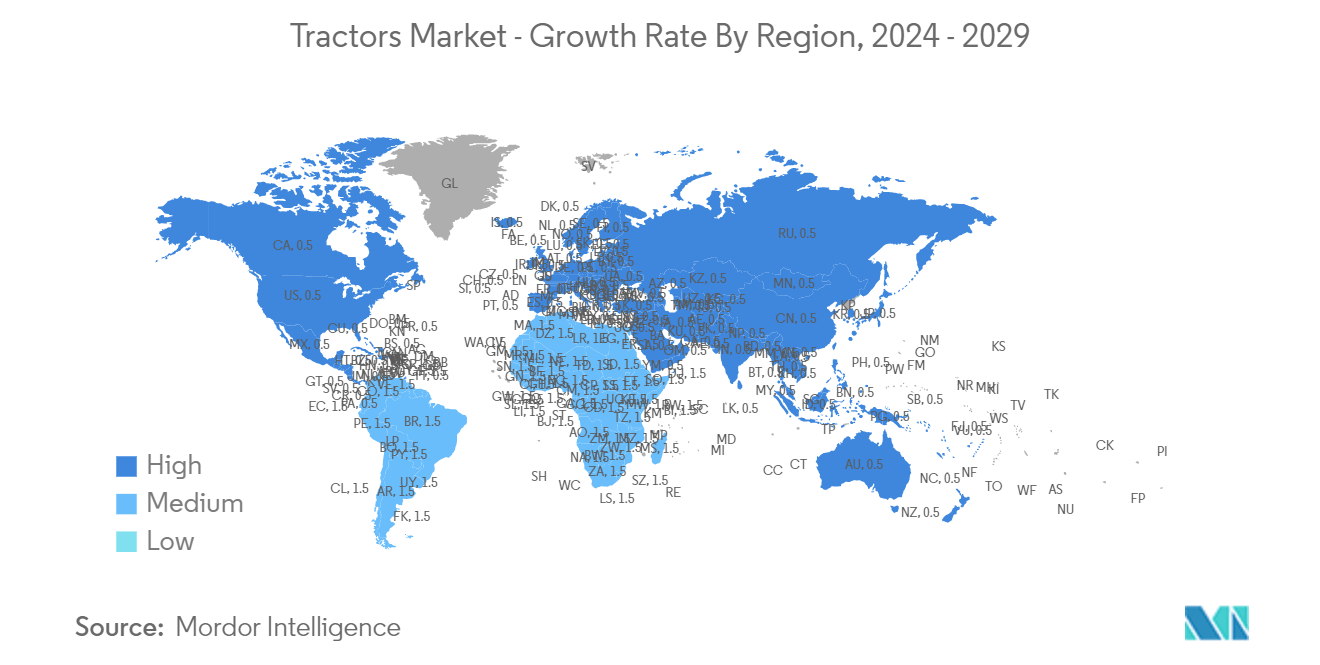

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Tractors Market Analysis

The Tractors Market size is estimated at USD 84.80 billion in 2024, and is expected to reach USD 114.5 billion by 2029, growing at a CAGR of 5.90% during the forecast period (2024-2029).

The tractor market has experienced steady growth in recent years, driven by factors such as increasing mechanization in agriculture, rising demand for high-horsepower tractors, and government initiatives supporting farm mechanization. The market size is substantial, reflecting the essential nature of tractors in enhancing agricultural efficiency. The adoption of precision farming techniques and the need for sustainable farming practices further contribute to the growth trajectory of the tractor market.

The market is characterized by the presence of leading global players, including John Deere, CNH Industrial (Case IH and New Holland), AGCO Corporation (Massey Ferguson and Fendt), and Kubota. These companies compete intensely, offering a diverse range of tractors with varying power capacities and features to cater to the diverse needs of European farmers. The competition is not only centered around product offerings but also involves service and support networks, as after-sales services play a critical role in the agricultural machinery sector.

Over the long term, the key factors contributing to the increase in worldwide tractor sales are increasing farm mechanization rates, especially in developing nations, rising farm labor costs, seasonal labor shortages, and shorter tractor replacement cycles. However, some of the prominent players in the industry are focusing on mergers and acquisitions and new product development in the market. For instance,

- The French start-up Seederal announced its venture into the development of an electric tractor in 2023. The company is currently in the process of constructing the electric tractor prototype, which is expected to possess a formidable power capacity of 160 hp. This initiative aligns with the global trend toward sustainable farming practices and the adoption of electric-powered agricultural machinery.

- In October 2022, At Kubota Connect, the manufacturer gave dealers a sneak peek at the new products. Series M7 Generation 4 The Kubota M7s are the company's largest tractors, aimed at livestock and forage producers.

Advancements in tractor technology have significantly influenced the European market. Precision farming technologies, such as GPS guidance systems, telematics, and automated steering, are increasingly integrated into modern tractors. These technologies enhance operational efficiency, optimize input usage, and contribute to sustainable agriculture by minimizing environmental impact. The adoption of precision farming practices is a notable trend, and farmers are investing in tractors equipped with smart technologies to improve productivity.

Asia-Pacific is expected to witness significant growth in the next five years as emerging key economies like India, China, and Japan are encouraging farmers in their countries by offering subsidized farm equipment and low credit rates to encourage tractor adoption. Such developments are likely to drive the demand for tractors in these regions.

Tractors Market Trends

The Below 40 HP Tractors Segment's Growth is Expected to be Bolstered over the Next Five Years

The global tractor market is witnessing a fascinating trend: while there's a continued interest in larger, high-horsepower tractors for superior performance in difficult terrains and diverse applications, the segment below 40 horsepower (HP) is also expected to experience significant growth in the coming five years.

These tractors, often referred to as compact tractors, are typically less than 1500 cc in engine displacement and occupy less space. This makes them ideal for smaller farms, maneuvering tight spaces, and handling basic agricultural tasks like mowing, tilling, and light-duty transport.

Major tractor markets like India and China have reported positive growth in the sub-40 HP segment in recent years. Small and medium-scale farms are increasingly adopting compact tractors to improve efficiency and productivity compared to traditional manual labor. Some governments offer subsidies or loan programs to encourage small farmers to invest in these tractors, further boosting adoption.

Manufacturers are recognizing this increasing demand and launching new models specifically catering to the sub-40 HP segment. For instance:

- Mahindra Gio (India): A compact tractor known for its maneuverability and affordability, targeting small farms and hobbyists.

- John Deere 1025R (United States): A versatile sub-compact tractor designed for mowing, landscaping, and light utility tasks.

Asia-Pacific is Anticipated to Lead the Market Between 2024 and 2029

Asia-Pacific stands out as a leader in the global tractor market due to its vast and diverse agricultural landscape. The region encompasses a wide range of climates and topographies, supporting a variety of crops and farming practices. With agriculture being a primary economic activity in many Asia-Pacific countries, the demand for tractors is inherently high. Small-scale and large-scale farmers alike rely on tractors for plowing, planting, and harvesting, driving sustained demand across diverse agricultural sectors.

Asia-Pacific is home to a significant portion of the world's population, and ensuring food security is a top priority for many nations in the region. Tractors play a crucial role in increasing agricultural productivity, allowing farmers to cultivate larger areas efficiently. The need to feed growing populations has spurred investments in mechanization, making tractors indispensable for enhancing farm output and overall food security in Asia-Pacific.

Many governments in Asia-Pacific have recognized the importance of mechanized agriculture for economic development and food production. As a result, they have implemented supportive policies, subsidies, and financial incentives to encourage the adoption of modern agricultural machinery, including tractors. Government initiatives aimed at improving farm efficiency and promoting sustainable practices contribute significantly to the leadership of Asia-Pacific in the tractor market.

Asia-Pacific has embraced technological advancements in agriculture, leading to the widespread adoption of modern and technologically advanced tractors. Precision farming techniques, GPS-guided tractors, and smart farming solutions have gained traction in the region. Farmers are increasingly investing in tractors equipped with cutting-edge technologies to optimize resource utilization, reduce environmental impact, and enhance overall agricultural productivity.

- In August 2023, VST Tillers Tractors, a Bengaluru-based manufacturer specializing in tractors and tillers, declared its intention to invest INR 100 crore in establishing a dedicated research and development center. This substantial investment is aimed at advancing research and fostering innovation in the global agricultural sector. The initiative underscores VST Tillers Tractors' commitment to staying at the forefront of technological advancements and contributing to the evolution of farming practices worldwide.

- In August 2023, in a collaborative effort with Mitsubishi Mahindra Agriculture Machinery, Japan, Mahindra and Mahindra launched a new line of tractors under the OJA platform in Cape Town, South Africa. This partnership led to the introduction of a series of sub-compact, compact, and small utility tractors, ranging from 20 hp to 40 hp (14.91–29.82 kW). With an investment of INR 1,200 crore in the OJA platform, Mahindra and Mahindra plans to unveil large utility tractors next year, highlighting their commitment to delivering a comprehensive range of technologically advanced tractors.

Tractors Industry Overview

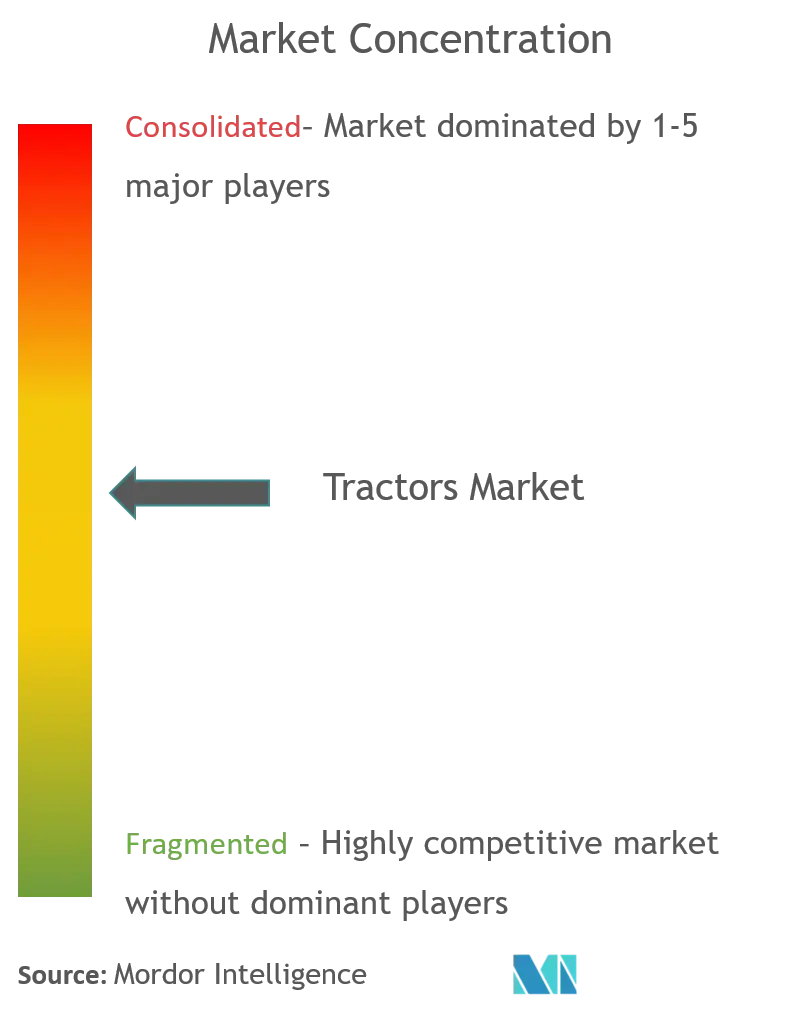

The tractor market is moderately consolidated as it witnesses active engagement from several global and regional players. Major players such as Mahindra & Mahindra, Tractor, Kubota Corporation, Farm Equipment Limited, and HMT Limited are adopting agreements and product launches as key developmental strategies to improve the product portfolio of tractor products. For instance,

- In December 2023, AutoNxt Automation unveiled its latest innovations at Krishithon 2023, the largest agricultural exhibition in the country. During the event, Kaustubh Dhonde, the company's Founder and CEO, proudly introduced a new Loader application in a 45HP tractor and presented the prototype of a 20HP Electric Tractor. Krishithon 2023, now in its 16th edition, served as a pivotal platform for AutoNxt Automation to showcase its dedication to transforming the agricultural sector.

- In July 2023, Monarch Tractor, renowned for its MK-V, a fully electric, driver-optional, and connected tractor, announced the expansion of its operations in Singapore. This move signifies substantial growth and a strong interest in the company's AI, robotics, and smart farming technology within Asia Pacific. The decision to extend operations reflects Monarch Tractor's strategic positioning to capitalize on the burgeoning demand for advanced agricultural technologies in Asia-Pacific.

- In November 2022, At SIMA 2022, New Holland debuted the T8 tractor with Raven Autonomy, a driverless grain cart harvest application. It incorporates OMNiDRIVE, the world's first driverless agriculture technology for grain cart harvesting. The cutting-edge technology stack allows the farmer to monitor, synchronize, and operate a driverless tractor from the harvester's cab.

Tractors Market Leaders

Deere and Company

Kubota Corporation

Mahindra Tractors

CNH Industrial

AGCO Corporation

*Disclaimer: Major Players sorted in no particular order

Tractors Market News

- March 2024: Hyster Company announced an agreement to provide APM Terminals with 10 battery-powered terminal tractors for their location at the Port of Mobile in Alabama. The electric terminal tractors, which are scheduled to be delivered in 2024, are part of a USD 60 million investment in port equipment electrification pilots by APM Terminals.

- October 2023: International Tractors Limited (ITL) made noteworthy strides in the global market by unveiling three new series of Solis tractors. This expansion aligns with ITL's vision of providing cutting-edge agricultural equipment worldwide. Among the new offerings is the SV Solis electric tractor, a groundbreaking addition to the lineup. This electric tractor boasts a rapid charging capability, allowing it to be charged from 0 to 100% in an impressive 3 to 3.5 hours. The introduction of the SV Solis electric tractor reflects ITL's dedication to sustainable farming practices and the integration of advanced technologies to meet the evolving demands of global agriculture.

- May 2023: Italian-American construction and agriculture firm CNH is set to make a significant investment of up to USD 50 million in the Indian farm machinery sector this year. The strategic move aims to strengthen CNH's presence in the Indian agricultural landscape. As part of this investment, the company was gearing up to launch a robust 105HP tractor in May 2023, catering to the diverse needs of Indian farmers. This development underscores CNH's commitment to contributing to the modernization of agriculture in India through innovative machinery solutions.

- September 2022: KAMAZ PJSC announced its plans to expand the model range of gas vehicles. KAMAZ continued to carry out plans for the development of gas-powered vehicles. This includes the completion of K4 generation vehicle production, the modernization of K3 generation vehicles using an alternative component base, and the development of K5 generation vehicles. The company's plans include bringing the most popular LNG-powered KAMAZ-54901 long-haul tractors, as well as CNG-powered transport vehicles, to the market.

- August 2022: Hon Hai Technology Group (Foxconn) signed a contract manufacturing agreement with Zimeno Inc. (dba Monarch Tractor) to manufacture next-generation autonomous tractors and battery packs at the Foxconn Ohio facility in Lordstown.

- July 2022: In the 4x2 Tractor segment, Ashok Leyland introduced the AVTR 4220 with 41.5T GCW and the AVTR 4420 with 43.5T GCW. These tractors have an H6 Engine - a 6-cylinder engine with i-Gen6 technology, GCW options of 41.5T and 43.5T, and a suitable two-axle trailer.

Tractor Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Drivers

4.2 Market Challenges

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size in USD billion)

5.1 By Horsepower

5.1.1 Below 40 HP

5.1.2 40 HP - 100 HP

5.1.3 Above 100 HP

5.2 By Drive Type

5.2.1 Two-wheel Drive

5.2.2 Four-wheel Drive/All-wheel Drive

5.3 By Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Spain

5.3.2.5 Italy

5.3.2.6 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 South Korea

5.3.3.5 Rest of Asia-Pacific

5.3.4 Rest of the World

5.3.4.1 South America

5.3.4.2 Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Vendor Market Share

6.2 Company Profiles*

6.2.1 Deere and Company

6.2.2 CNH Global NV (includes New Holland and Case IH)

6.2.3 AGCO Corporation (includes Massey Ferguson, Valtra, Fendt, and Challenger)

6.2.4 CLAAS KGaA mbH

6.2.5 Mahindra and Mahindra Corporation

6.2.6 Kubota Corporation

6.2.7 Escorts Limited

6.2.8 Tractors and Farm Equipment Limited (TAFE)

6.2.9 Kuhn Group (Subsidiary of Bucher Industries)

6.2.10 Yanmar Company Limited

6.2.11 Deutz-Fahr

Tractors Industry Segmentation

A tractor is a vehicle usually available with one or two small wheels in front and two large wheels at the back. It is used in agriculture, construction, and logistics applications to move attached implements such as rotavators, plowing, tilling, sowing, cultivation, and harvesting.

The tractors market is segmented by horsepower (below 40 HP, 40 HP - 100 HP, and above 100 HP), by drive type (two-wheel drive and four-wheel drive/all-wheel drive), and by geography (North America, Europe, Asia-Pacific, and the Rest of the World). For each segment, market sizing and forecast are given on the basis of value in USD billion.

| By Horsepower | |

| Below 40 HP | |

| 40 HP - 100 HP | |

| Above 100 HP |

| By Drive Type | |

| Two-wheel Drive | |

| Four-wheel Drive/All-wheel Drive |

| By Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Tractor Market Research FAQs

How big is the Tractors Market?

The Tractors Market size is expected to reach USD 84.80 billion in 2024 and grow at a CAGR of 5.90% to reach USD 114.5 billion by 2029.

What is the current Tractors Market size?

In 2024, the Tractors Market size is expected to reach USD 84.80 billion.

Who are the key players in Tractors Market?

Deere and Company, Kubota Corporation, Mahindra Tractors, CNH Industrial and AGCO Corporation are the major companies operating in the Tractors Market.

Which is the fastest growing region in Tractors Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Tractors Market?

In 2024, the Asia-Pacific accounts for the largest market share in Tractors Market.

What years does this Tractors Market cover, and what was the market size in 2023?

In 2023, the Tractors Market size was estimated at USD 79.80 billion. The report covers the Tractors Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Tractors Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

What are the key drivers of the Tractors Market?

Key factors driving the Tractors Market are: a) Rising demand for food due to the growing global population b) Technological advancements in farming practices c) Government subsidies for agricultural machinery

Tractors Industry Report

The Global Tractor Market is on an upward trajectory, fueled by increased mechanization in agriculture, a surge in government infrastructure spending, and the rising demand for compact tractors. Key drivers include advancements in technology, such as telematics integration, and a preference for tractors in the 30-50 HP range for their efficiency and affordability. The Asia-Pacific region leads, due to precision farming adoption and government initiatives. The market, analyzed by Mordor Intelligence™, is segmented by power output, drive type, and application, highlighting a trend towards high-performance tractors by the largest tractor manufacturers for challenging conditions. These tractors, often exceeding 100 HP, cater to the agricultural, construction, and logistics sectors' needs. With statistics on market share, size, and revenue growth, this industry analysis offers a comprehensive forecast and historical overview. For detailed insights, a free report PDF download is available, showcasing the market's lucrative growth opportunities.