Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

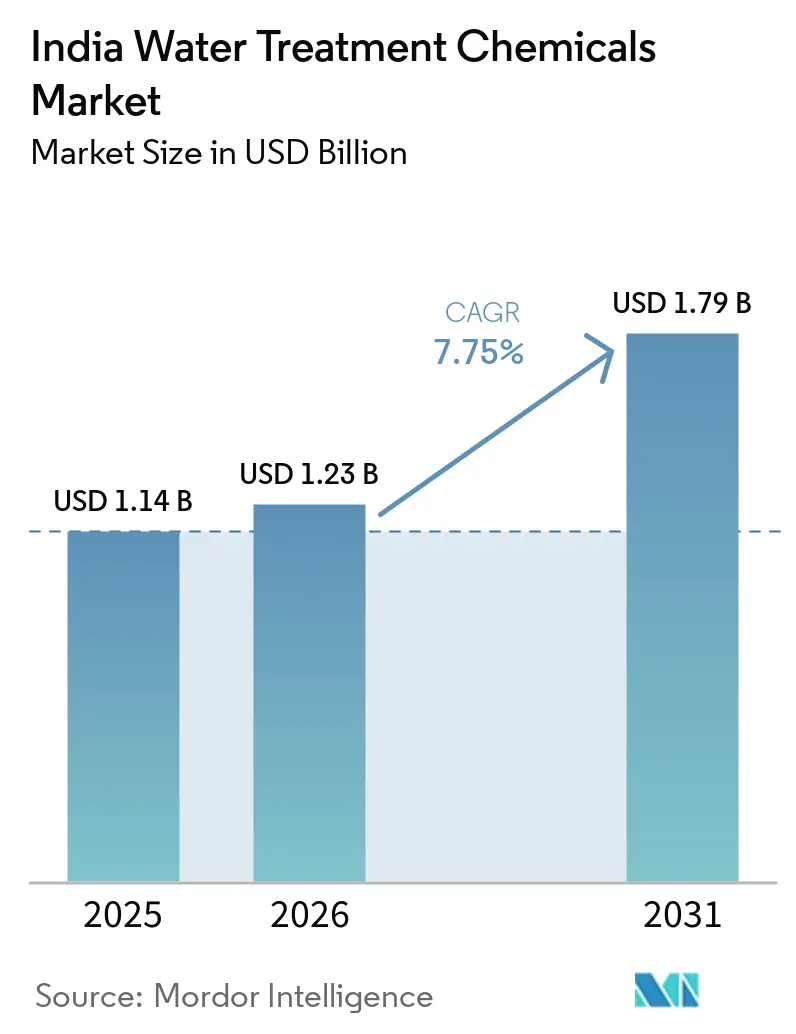

| Base Year Market Size (2025) | USD 1.14 Billion |

| Market Size (2026) | USD 1.23 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 7.75% CAGR |

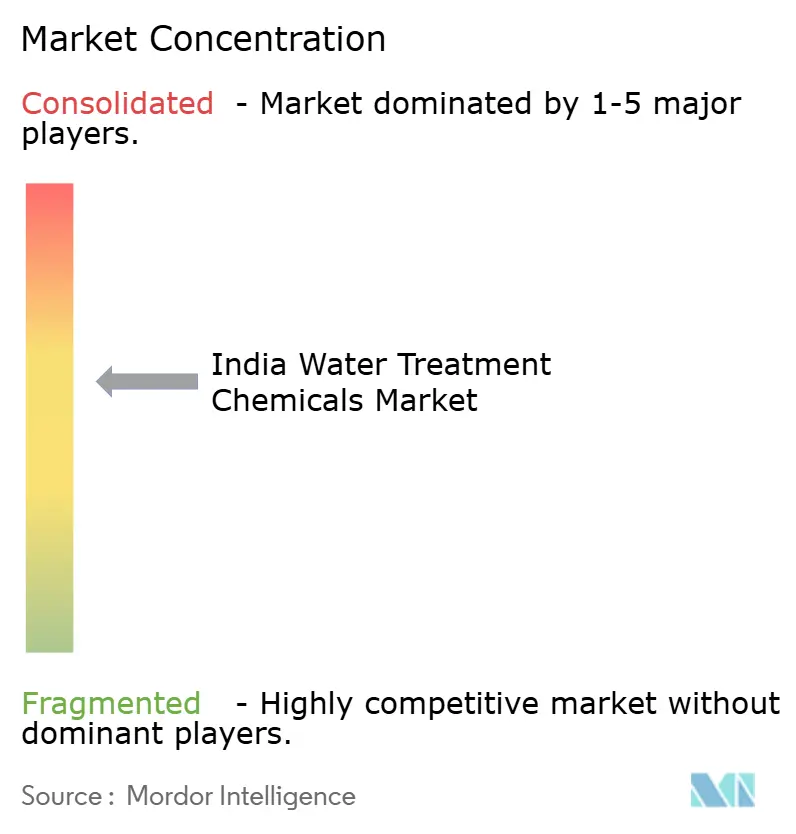

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Water Treatment Chemicals Market Analysis by Mordor Intelligence

The India Water Treatment Chemicals Market size was valued at USD 1.14 billion in 2025 and is estimated to grow from USD 1.23 billion in 2026 to reach USD 1.79 billion by 2031, at a CAGR of 7.75% during the forecast period (2026-2031). Government infrastructure mandates and industrial zero-liquid-discharge (ZLD) rules are converging with groundwater-quality challenges, rapidly broadening municipal and industrial demand. Large federal programs, including Jal Jeevan Mission and AMRUT 2.0, are awarding multi-year chemical supply contracts that favor suppliers able to meet Bureau of Indian Standards specifications and execute at scale. High-silica groundwater across western and northern states is raising antiscalant consumption even as digital dosing cuts waste at pilot sites in Bangalore and Pune. Multinationals are localizing production to hedge China-centric supply chains, while domestic firms expand phosphonate and polyacrylamide capacity under the Production-Linked Incentive (PLI) scheme. Bio-based coagulants derived from shrimp shells and Moringa oleifera seeds are gaining early traction among food processors eager to lower sludge-disposal fees, creating a differentiated growth pocket inside the wider India water treatment chemicals market.

Key Report Takeaways

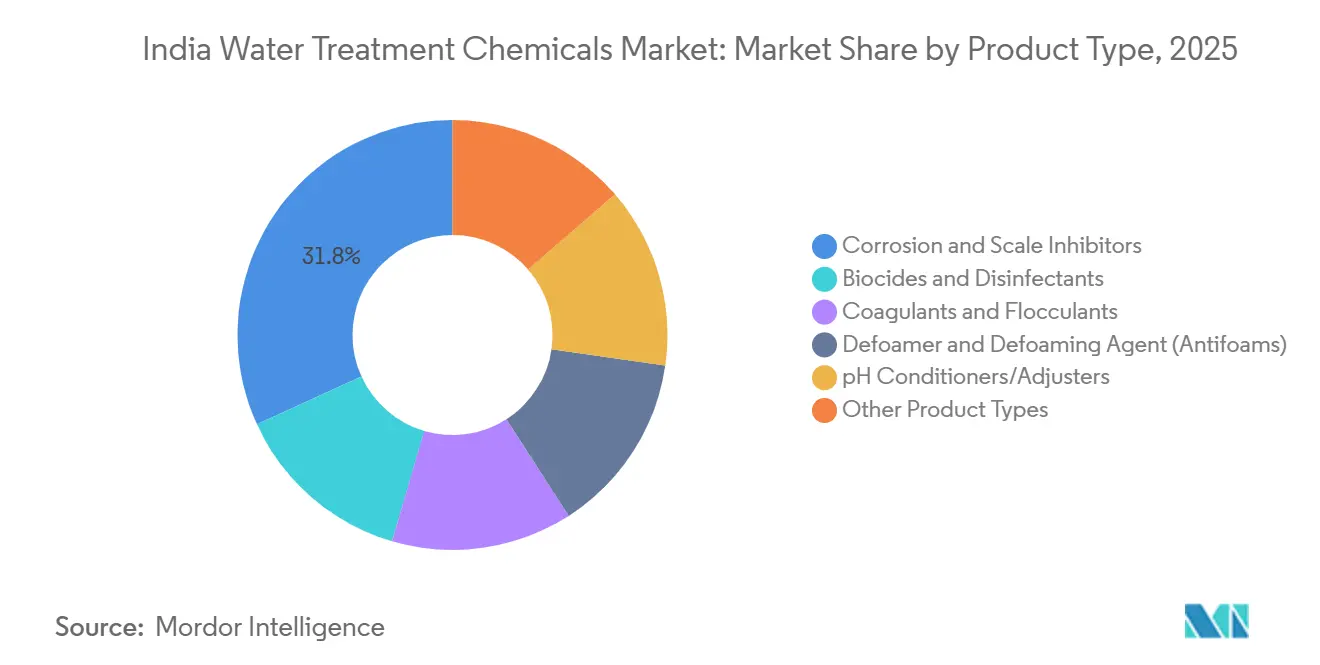

- By product type, corrosion and scale inhibitors led with 31.82% of the India water treatment chemicals market share in 2025, while coagulants are growing at a CAGR of 7.93% through 2031.

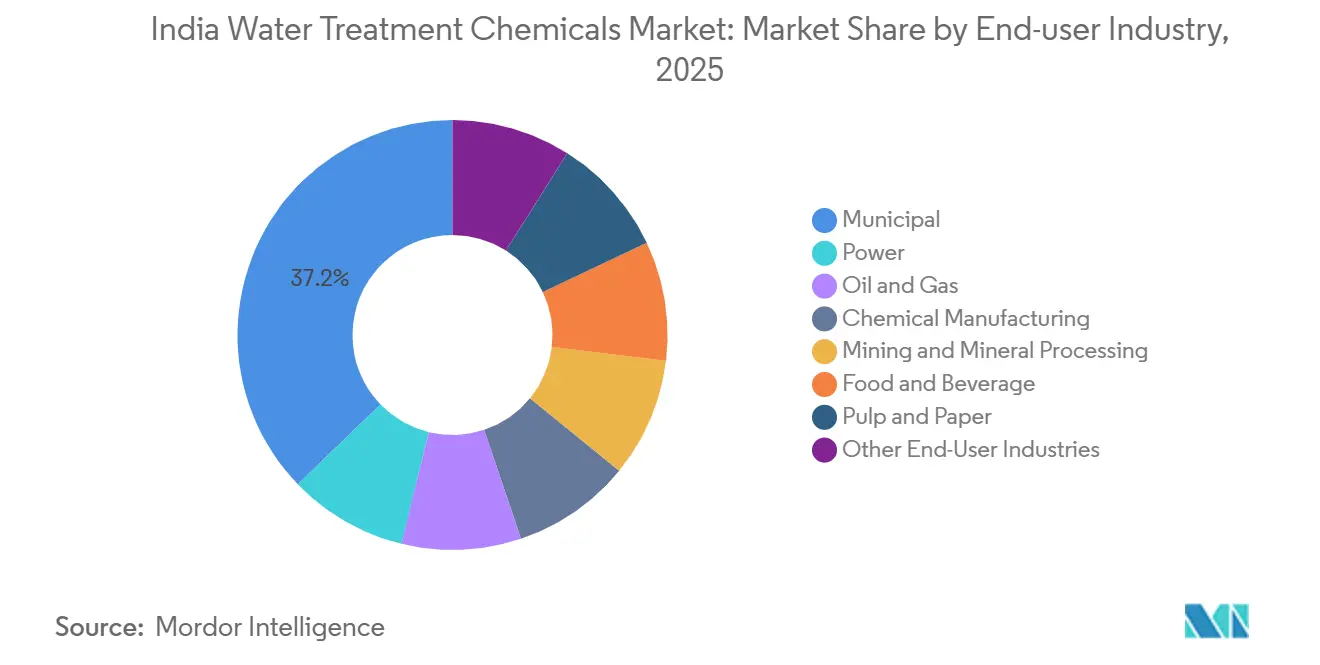

- By end-user industry, municipal applications held 37.22% of the India water treatment chemicals market size in 2025 and are advancing at a 8.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Water Treatment Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government capex (Jal Jeevan and Namami Gange) | +2.1% | National, with concentration in Uttar Pradesh, Bihar, Jharkhand, Odisha for rural tap connections | Medium term (2-4 years) |

| Stricter Zero-Liquid-Discharge mandates | +1.8% | Maharashtra, Gujarat, Tamil Nadu industrial clusters; Red-category zones nationwide | Short term (≤ 2 years) |

| Surge in AI-enabled smart-dosing platforms | +0.9% | Metropolitan municipal utilities and large industrial campuses in Bangalore, Pune, Chennai | Medium term (2-4 years) |

| Domestic specialty-chem capacity boost via PLI and China plus one strategy | +1.3% | Gujarat, Maharashtra chemical hubs; import-substitution gains across India | Long term (≥ 4 years) |

| Bio-based agro-waste coagulants cut sludge costs | +0.7% | Food-processing belts in Punjab, Maharashtra; pharmaceutical clusters in Hyderabad, Ahmedabad | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Capex Drives Rural and Urban Water Infrastructure Expansion

Fresh budgetary outlays are creating the single biggest structural pull on the India water treatment chemicals market. Jal Jeevan Mission’s allocation for 2025-26 dedicates a portion to continuous water-quality monitoring, translating into numerous laboratory and field tests each year, all of which consume reagent-grade coagulants, disinfectants, and pH adjusters. Namami Gange has sanctioned funding for sewage-treatment plants in the Ganga basin, while AMRUT 2.0 is adding urban sewage capacity across 500 cities[1]Ministry of Housing and Urban Affairs, “AMRUT 2.0: Mission Details,” Mohua.gov.in. Domestic formulators equipped with regional warehouses are capturing tenders by cutting delivery lead times, an emerging competitive edge inside the expanding India water treatment chemicals market.

Zero-Liquid-Discharge Mandates Reshape Industrial Water Management

Under the Draft Liquid Waste Management Rules 2025, red-category industrial zones must implement Zero Liquid Discharge (ZLD). This mandate pushes the textile, chemical, and pharmaceutical sectors to invest in evaporators and crystallizers, which heavily depend on antiscalants and corrosion inhibitors. In Tirupur, the textile cluster operates more than 18 common effluent treatment plants equipped with ZLD modules, leading to a surge in phosphonate demand. Firms achieving more than 90% water recovery can counterbalance elevated chemical expenses, highlighting the robust demand trajectory and the resilience of India's water treatment chemicals market, even in the face of fluctuating raw material costs.

AI-Enabled Smart-Dosing Platforms Optimize Chemical Consumption

Municipal utilities and industrial campuses are leveraging IoT-enabled dosing systems, achieving chemical savings by real-time adjustments to coagulant and disinfectant doses. At a hospital in Bangalore, FluxGen’s platform not only reduced overall water consumption but also halved the cooling-tower blow-down. While these achievements are driving significant tenders in Tier 1 cities, a shortage of skilled operators is hindering broader adoption. This nuance tempers, but doesn't overshadow, the positive influence of digitization on India's water treatment chemicals market.

Domestic Specialty-Chemical Capacity Expansion via PLI and China-Plus-One Sourcing

India relies on imports for roughly half of polyacrylamide and specialty phosphonates, exposing formulators to freight surcharges and supply disruption. The PLI scheme is triggering brownfield expansions by Atul Ltd and Chembond in Gujarat and Maharashtra, respectively. NITI Aayog forecasts India’s specialty-chemicals sector to grow substantially, implying significant domestic substitution potential and new scale economies that can stabilize prices within the India water treatment chemicals market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile feedstock prices and China supply shifts | -1.2% | National, with acute impact on Gujarat, Maharashtra chemical manufacturing hubs | Short term (≤ 2 years) |

| High-silica Indian waters accelerate membrane fouling | -0.8% | Rajasthan, Gujarat, Haryana, Punjab groundwater-dependent regions | Medium term (2-4 years) |

| Skilled-labour gap in digital dosing/analytics | -0.5% | Tier-2 and Tier-3 cities; smaller municipal utilities and mid-scale industrial units | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility and China-Centric Supply Disruptions Compress Margins

Export quotas, power tariffs, and shipping bottlenecks cause caustic soda and chlorine prices to swing. Smaller formulators, without hedging mechanisms, must pass these price increases on after 60-90 days. This delay erodes their competitiveness against global incumbents that source from multiple regions. While the short-term squeeze complicates financial planning, it's unlikely to derail medium-term growth. A wave of domestic chlor-alkali capacity, coming online under PLI incentives, is set to gradually insulate the Indian water treatment chemicals market from external shocks.

High-Silica Groundwater Drives Up Antiscalant Consumption and Operating Expense

In Rajasthan, Gujarat, Haryana, and Punjab, high silica concentrations are causing colloidal fouling on RO membranes, leading to a significant drop in permeate flux[2]Central Ground Water Authority, “Groundwater Quality Assessment 2025,” Cgwb.gov.in. As a result, industrial plants are now resorting to chemical cleanings more frequently than the global standard, resulting in heightened chemical and energy expenses. Meanwhile, municipal utilities, in a bid to cut costs, often underdose antiscalants. This practice not only diminishes recovery rates but also escalates per-unit treatment costs, posing a medium-term challenge for the broader Indian water treatment chemicals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Phosphonate-Polymer Blends Dominate Cooling and Boiler Applications

Corrosion and scale inhibitors commanded 31.82% of the India water treatment chemicals market in 2025. This segment's significance is closely tied to India's expansive thermal fleet and the bustling chemical hubs of Gujarat and Maharashtra, where phosphonate-polymer blends play a crucial role in protecting heat-exchange equipment. An industry-wide shift from zinc compounds, driven by stringent environmental regulations, has significantly boosted the adoption of phosphonates. On the other hand, coagulants and flocculants, riding the wave of an expanding sewage-treatment infrastructure, are projected to achieve a 7.93% CAGR, thereby contributing substantially to the overall size of India's water treatment chemicals market. Meanwhile, bio-based alternatives like chitosan and Moringa extract, though still niche, are establishing lucrative subsegments, thanks to their impressive sludge-reduction capability.

Biocides and disinfectants maintain a consistent demand from municipal utilities, driven by the need to adhere to IS 10500 drinking-water standards, which mandate a residual chlorine level of 0.2-1 mg/L. In industrial settings, cooling towers utilize non-oxidizing biocides, such as DBNPA, to prevent biofilm formation, with usage intensifying in response to rising ambient temperatures and higher recycled-water ratios. Other additives like defoamers, oxygen scavengers, and pH adjusters, while contributing to the portfolio's profitability, command smaller absolute volumes. Together, these trends underscore the robust growth potential of India's water treatment chemicals market.

By End-User Industry: Municipal Sector Leads on Infrastructure Capex

Municipal utilities held 37.22% of 2025 revenue, the largest slice of the India water treatment chemicals market size, and are advancing at a 8.15% CAGR through 2031. With capacity additions under AMRUT 2.0 and the ongoing Jal Jeevan connections, there's an upward push in chemical intensity. Power generation, the second-largest sector, utilizes corrosion inhibitors and antiscalants in both cooling-tower and boiler feedwater systems. India's coal and gas fleet operates at moderate load factors, ensuring a strong baseline demand.

In the oil and gas sector, operations treat produced water, often rich in total dissolved solids, necessitating the use of specialty demulsifiers and antiscalants. The chemical manufacturing boom, driven by "China-plus-one" sourcing strategies, is spurring a heightened demand for corrosion inhibitors and pH adjusters in multi-effect evaporators. Meanwhile, mining operations in Jharkhand and Odisha utilize high-molecular-weight polyacrylamide flocculants for tailings pond dewatering, and pulp and paper mills employ defoamers to enhance aeration stability. These diverse applications underscore the resilience and breadth of the Indian water treatment chemicals market.

Geography Analysis

In northern states like Rajasthan, Haryana, Punjab, and Uttar Pradesh, groundwater silica levels frequently surpass standard thresholds, leading to a disproportionate consumption of antiscalants. Meanwhile, the Jal Jeevan Mission is channeling coagulants and disinfectants into rural districts of these states, where the baseline tap-connection ratios lag behind the national average. In western India, Gujarat and Maharashtra stand out with their bustling chemical, pharmaceutical, and textile sectors, positioning them as the foremost contributors to India's water treatment chemicals market. Notably, these regions have already achieved significant enforcement of Zero Liquid Discharge (ZLD), bolstering the demand for corrosion inhibitors and biocides.

In southern metros like Bangalore, Chennai, and Hyderabad, the adoption of digital dosing is leading to chemical savings while enhancing overall efficacy. For instance, installations by Faclon Labs in Bangalore are showcasing data-driven advantages, drawing interest from additional municipal pilots. Over in eastern India's coal belt, flocculant consumption is on the rise, especially with Coal India aiming for substantial water reuse across its mines by 2028. Lastly, in the Ganga basin, more than 18 sewage plants in Uttar Pradesh are driving localized demand for polyaluminum chloride and sodium hypochlorite, further energizing the momentum of India's water treatment chemicals market.

Competitive Landscape

The Indian water treatment chemicals market remains moderately consolidated. Domestic players leverage price competitiveness, local inventory, and rapid formulation tweaks suited to high-TDS waters. Bio-based coagulants remain an under-penetrated but strategically important niche; firms stitching supply agreements with agro-processors could capture early-mover advantages before global giants scale similar solutions. Overall, digital capability, localization, and raw-material integration are the three strategic levers now shaping rivalry across the India water treatment chemicals market.

India Water Treatment Chemicals Industry Leaders

Ecolab Inc. (Nalco Water)

IEI

Thermax Limited

SNF

Kemira

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Buckman Laboratories (Asia) and Atul Ltd. formed the ‘Atul-Buckman’ joint venture to deliver advanced water-treatment chemistries with integrated digital monitoring in India.

- June 2024: Kurita Water Industries established Kurita AquaChemie India Private Limited to broaden its local chemical-supply and service footprint.

India Water Treatment Chemicals Market Report Scope

Water treatment chemicals are widely used in various end-user industries, such as chemicals (including petrochemicals), power generation, and others. These end-user industries generate wastewater from their facilities as a byproduct, which needs to be treated before reuse or disposal, considering the longer shelf life of the equipment and government regulations to protect the environment. Some of the water treatment chemicals include corrosion inhibitors, biocides, flocculants, and others.

The Indian water treatment chemicals market is segmented by product type and end-user industry. By product type, the market is segmented into biocides and disinfectants, coagulants and flocculants, corrosion and scale inhibitors, defoamers and defoaming agents, pH adjusters and softeners, and other product types (oxygen scavengers, etc.). In the end-user industry, the market is segmented into power, oil and gas, chemical manufacturing, mining and mineral processing, municipal, food and beverage, pulp and paper, and other end-user industries (pharmaceuticals, etc.). For each segment, the market sizing and forecasts were made on the basis of value (USD).

By Product Type

| Biocides and Disinfectants |

| Coagulants and Flocculants |

| Corrosion and Scale Inhibitors |

| Defoamer and Defoaming Agent (Antifoams) |

| pH Conditioners/Adjusters |

| Other Product Types |

By End-user Industry

| Power |

| Oil and Gas |

| Chemical Manufacturing |

| Mining and Mineral Processing |

| Municipal |

| Food and Beverage |

| Pulp and Paper |

| Other End-User Industries |

| By Product Type | Biocides and Disinfectants |

| Coagulants and Flocculants | |

| Corrosion and Scale Inhibitors | |

| Defoamer and Defoaming Agent (Antifoams) | |

| pH Conditioners/Adjusters | |

| Other Product Types | |

| By End-user Industry | Power |

| Oil and Gas | |

| Chemical Manufacturing | |

| Mining and Mineral Processing | |

| Municipal | |

| Food and Beverage | |

| Pulp and Paper | |

| Other End-User Industries |

Key Questions Answered in the Report

How large will the India water treatment chemicals market be by 2031?

The India Water Treatment Chemicals Market size was valued at USD 1.14 billion in 2025 and is estimated to grow from USD 1.23 billion in 2026 to reach USD 1.79 billion by 2031, at a CAGR of 7.75% during the forecast period (2026-2031).

Which segment contributes the most revenue?

Corrosion and scale inhibitors generated 31.82% of market revenue in 2025, the highest among all product types.

Why is municipal demand expanding faster than industrial demand?

Jal Jeevan Mission and AMRUT 2.0 are adding large-scale water and sewage infrastructure, driving chemical consumption at a 7.55% CAGR through 2031.

What is the main raw material risk?

Price volatility in caustic soda and chlorine, tied to Chinese export quotas and domestic power tariffs, can compress formulator margins.

Page last updated on: