Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

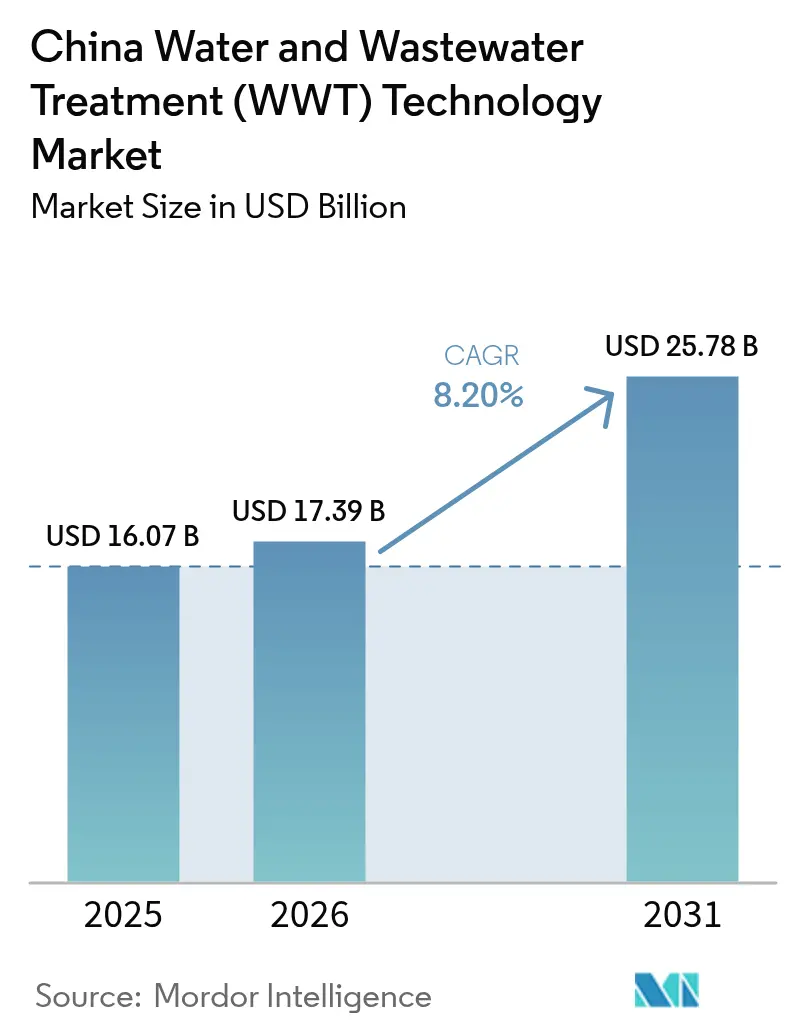

| Base Year Market Size (2025) | USD 16.07 Billion |

| Market Size (2026) | USD 17.39 Billion |

| Market Size (2031) | USD 25.78 Billion |

| Growth Rate (2026 - 2031) | 8.20% CAGR |

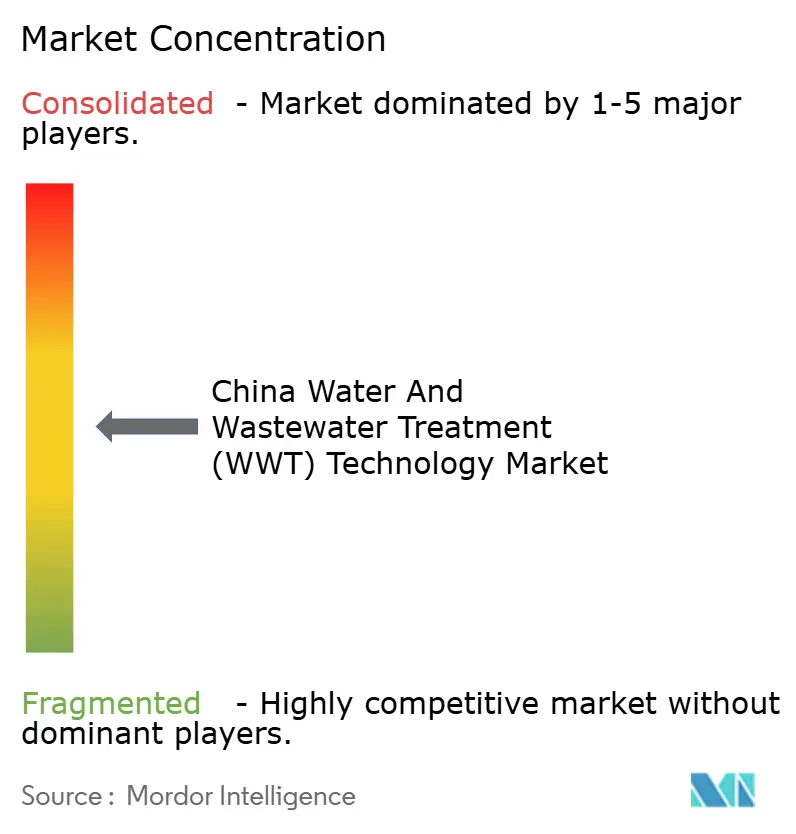

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Water And Wastewater Treatment (WWT) Technology Market Analysis by Mordor Intelligence

The China Water and Wastewater Treatment Technology Market size was valued at USD 16.07 billion in 2025 and estimated to grow from USD 17.39 billion in 2026 to reach USD 25.78 billion by 2031, at a CAGR of 8.20% during the forecast period (2026-2031). Rapid urbanization, strict zero-liquid-discharge (ZLD) mandates, and a USD 50 billion public-private-partnership (PPP) pipeline are the primary forces expanding treatment capacity and pushing advanced membrane adoption. Industrial operators now view wastewater as a recoverable resource that can yield biogas, nutrients, and deionized water, turning cost centers into revenue generators and improving project bankability. Regional tariff incentives in the Yangtze and Pearl River deltas deliver 20-30% higher internal rates of return, prompting technology vendors to prioritize eastern provinces for pilot roll-outs and joint ventures. Competitive intensity remains moderate as domestic manufacturers accelerate ceramic-membrane scaling while international suppliers focus on turnkey resource-recovery solutions, creating scope for hybrid partnership models that blend global know-how with local execution.

Key Report Takeaways

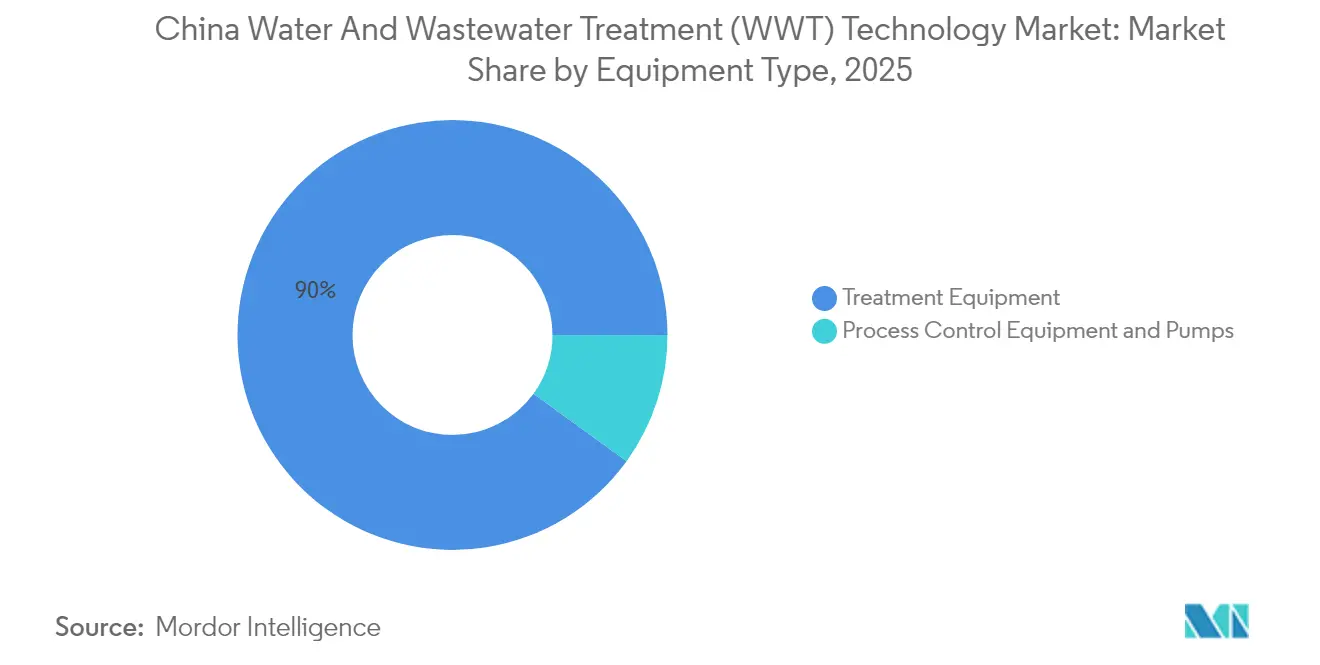

- By equipment type, treatment equipment captured 90.02% of the China water and wastewater treatment technology market share in 2025 and will expand at an 8.39% CAGR through 2031.

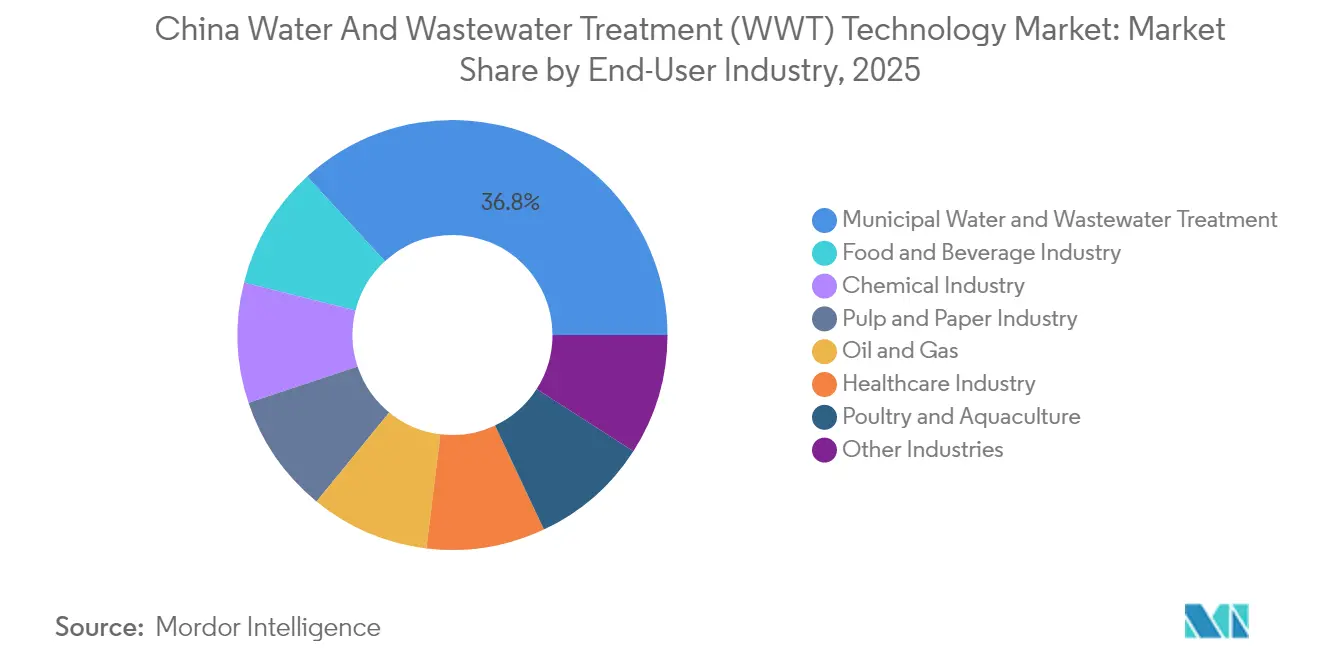

- By end-user sector, municipal facilities held 36.82% of the China water and wastewater treatment technology market size in 2025, whereas the food and beverage sector is forecast to grow the fastest at a 9.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Water And Wastewater Treatment (WWT) Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial zero-liquid-discharge mandates | +2.10% | Yangtze & Pearl River deltas | Short term (≤ 2 years) |

| Strong municipal PPP pipeline under 14th Five-Year Plan | +1.80% | Tier 2–3 cities nationwide | Medium term (2–4 years) |

| Rising semiconductor and EV water-purity requirements | +1.20% | Guangdong, Jiangsu, Shanghai | Medium term (2–4 years) |

| Carbon-neutral goals driving energy-efficient WWT tech | +1.10% | Early adoption in Beijing, Shenzhen, Hangzhou | Long term (≥ 4 years) |

| Waste-to-resource (biogas, nutrient recovery) economics | +0.90% | Shandong, Hebei, Liaoning | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industrial Zero-Liquid-Discharge Mandates Drive Technology Upgrades

ZLD regulations compel more than 15,000 chemical, pharmaceutical, and textile sites to recover 95% of process water or face penalties up to USD 1.5 million. Mandatory compliance resets procurement criteria toward reverse-osmosis, evaporation, and crystallization trains that deliver near-complete water recovery. Ceramic ultrafiltration membranes command 40-50% price premiums yet deliver longer life cycles and lower fouling, reducing the total cost of ownership beyond year 4. The GB 18918-2002 framework synchronizes provincial inspections, turning enforcement into a predictable demand cycle that sustains supplier order books. Domestic firms close the technology gap by licensing thin-film composite chemistries, while international vendors differentiate through integrated energy-recovery modules that cut operating kilowatt-hours by 25-30%.

Municipal PPP Pipeline Under 14th Five-Year Plan Accelerates Infrastructure Investment

The 14th Five-Year Plan allocates USD 75 billion specifically to water infrastructure, with 60% slated for PPPs that guarantee 20–30-year service payments anchored to performance indices. Tier 2 and Tier 3 municipalities tendered over 200 wastewater projects in 2024, each valued at USD 50-150 million, creating an addressable backlog attractive to foreign operators offering EPC-plus-O&M models[1]Beijing Enterprises Water Group Limited, “2024 Interim Report,” bewg.net . Standardized contract templates lower legal costs and compress bid-to-award cycles from 18 months to 9 months, improving cash-flow visibility for equipment suppliers. The PPP momentum stabilizes tariff regimes, which is pivotal for lenders that previously discounted variable pricing risk. Consequently, the China water and wastewater treatment technology market experiences steadier capital inflows that fund advanced oxidation and membrane bioreactor upgrades over conventional lagoons.

Semiconductor and EV Manufacturing Drive Ultra-Pure Water Demand

China’s push for 70% chip self-sufficiency by 2030 adds more than 50 new fabs, each requiring 10,000–50,000 m³/day of water at 18 megohm-cm resistivity[2]China Semiconductor Industry Association, “Ultrapure Water Requirements for Semiconductor Manufacturing,” csia.net.cn . Treatment trains integrating electrodeionization units, double-pass RO, and 0.05 µm filtration cost 3–5 times standard systems but lock in supply contracts upward of 10 years, underpinning long-term revenue for specialty providers. EV battery output scaling to 600 GWh demands equally stringent deionized process water, further widening the high-margin ultrapure segment. Bundled offerings that pair water polishing with wastewater metal-recovery units extract nickel, cobalt, and lithium worth USD 1,000–3,000/ton, supporting circular-economy objectives and reducing raw-material intensity by 4-6 percentage points. Provincial subsidies on “green-fab” certification expedite such installations, accelerating adoption in the China water and wastewater treatment technology market.

Waste-to-Resource Economics Transform Wastewater into Revenue Streams

Anaerobic digesters, which monetize 0.3–0.4 m³ biogas per cubic meter of influent, generate annual revenues of USD 2–5 million for large-footprint plants and cut methane emissions by 80-90%[3]China Biogas Society, “Anaerobic Digestion & Biogas Recovery in Wastewater Treatment,” chinabiogas.org . Nutrient-recovery modules crystallize phosphate salts worth USD 500-800/ton, allowing facilities to sell fertilizer into premium organic channels. Food processors lead adoption because high-BOD effluent yields triple biogas volumes relative to municipal sewage, while lowered sludge volumes reduce disposal fees by up to 35%. Government tax credits for 50% resource-recovery rates and subsidized development-bank loans shorten investment cycles to six years. These economics reposition the China water and wastewater treatment technology market toward circular-economy value capture instead of compliance alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for advanced membranes and AOP systems | -1.50% | Central & western provinces | Short term (≤ 2 years) |

| Slow standardisation for IIoT cybersecurity in plants | -0.80% | Large municipal plants nationwide | Medium term (2–4 years) |

| Provincial tariff gaps limiting private ROI | -0.60% | Rural municipalities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Requirements Constrain Market Entry

Ceramic membranes enabling ZLD run USD 800–1,200 per m³/day versus USD 300–500 for activated-sludge units, pushing smaller plants to defer upgrades. Bank debt typically covers 60–70% of project cost, yet ten-year amortization proves too short for cash-flow breakeven, especially in western provinces with lower tariffs. Leasing and build-operate-transfer schemes could fill the gap but remain unevenly regulated, adding legal risk premiums that raise overall borrowing costs. The capex hurdle delays penetration of AOP units that eliminate micropollutants, thereby slowing the pace at which the China water and wastewater treatment technology industry can align with emerging toxicity rules.

IIoT Integration Faces Cybersecurity Challenges

Water utilities seek sensor networks and predictive analytics to cut chemical dosing 10–15%, but disparate cybersecurity protocols elevate the threat of operational downtime. The Multi-Level Protection Scheme mandates localized data and extensive penetration testing, obligations that smaller operators struggle to finance. Vendor-specific communication stacks further complicate interoperability, inflating engineering budgets by 20-30% and elongating commissioning schedules by up to a year. Until standardized frameworks emerge, IIoT rollouts will progress sporadically, tempering digital-service revenue potential within the China water and wastewater treatment technology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Treatment Equipment Maintains Technological Leadership

Treatment equipment accounted for 90.02% of the China water and wastewater treatment technology market share in 2025 and is projected to expand at an 8.39% CAGR through 2031. Membrane bioreactors, advanced oxidation units, and multi-stage filtration lines form the backbone of ZLD compliance as well as ultrapure-water fabrication demands. Biological systems dominate subsegment revenue, leveraging anaerobic and membrane integration to balance high removal efficiency with energy recovery. Oil-water separators now target 95% separation thresholds, boosting demand in petrochemical belts along the Yangtze. Metal-recovery skids, still niche, benefit from electronics manufacturers reclaiming gold and palladium worth USD 1,000–3,000/ton, providing ancillary returns that offset capex.

Digitalized control modules, although a small slice of the China water and wastewater treatment technology market size, synchronize pump curves and blower speeds, shaving 12–18% off energy bills. Disinfection units pivot toward UV-LED clusters that eliminate chlorine transport hazards and avoid carcinogenic byproducts. As PPP contracts shift to performance-based remuneration, operators bundle membranes with sensors and cloud dashboards to lock in after-sales revenue, thus elevating lifetime value per installation.

By End-User Industry: Municipal Dominance Faces Food & Beverage Disruption

Municipal utilities commanded 36.82% of the China water and wastewater treatment technology market size in 2025, anchored by urban coverage targets that now exceed 70% population connectivity. Upgrades from Class 1 B to Class 1 A effluent drive retrofits toward MBR and energy-neutral digestion lines. Yet, food and beverage sites post the fastest 9.30% CAGR as export-oriented processors chase pharmaceutical-grade water to satisfy overseas audits. Breweries and dairy plants adopt anaerobic membrane digesters that slash chemical oxygen demand while yielding power offsets covering 25% of plant electricity.

In chemical parks, zero-liquid-discharge clusters absorb high-recovery evaporators paired with crystallizers to meet 95% water-reuse mandates. Hospitals accelerate deployment of membrane-based nanofiltration to achieve 99.9% pathogen attenuation. Oil-and-gas fields invest in produced-water softening units, reusing over 90% of treated flows for enhanced-oil-recovery injections, reinforcing circular resource trends in the China water and wastewater treatment technology market.

Geography Analysis

Eastern provinces—Guangdong, Jiangsu, and Zhejiang—collectively generated a significant share of the China water and wastewater treatment technology market size in 2025, supported by export-oriented industry clusters and stringent discharge norms. Semiconductor fabs in Suzhou and Nanjing escalate ultrapure-water installation counts, while Shenzhen’s carbon-net-zero pledges raise demand for energy-efficient digester retrofits.

Central provinces such as Henan, Hubei, and Hunan witness industrial migration from coastal areas. PPP incentives, lower land costs, and newly streamlined environmental approvals shrink project lead times by 20–30% and elevate market attractiveness. Waste-to-resource projects in these provinces recover nutrients for regional grain belts, forging industrial-agricultural symbiosis.

Western provinces struggle with lower tariffs and limited financing channels, yet targeted subsidies under the Western Development Strategy propel mining and coal-chemistry wastewater projects. Modular skids suited for remote, high-altitude locales gain traction, as do solar-coupled reverse-osmosis units that hedge against grid unreliability. Overall, geographic dispersion ensures the China water and wastewater treatment technology market remains opportunity-rich, but technology mix and financing structures diverge widely by region.

Competitive Landscape

The China water and wastewater treatment technology market exhibits moderately fragmented concentration. Domestic champions Beijing OriginWater and Beijing Enterprises Water Group exploit government rapport and low-cost manufacturing to anchor municipal PPP bids, while international heavyweights Veolia, Xylem, SUEZ, and DuPont capture ultrapure-water and high-end membrane niches. Joint ventures proliferate: Veolia’s partnership with Shandong-based Jingshui delivers French oxidation know-how via local fabrication, trimming landed cost by 18%. Technology packages now bundle OT cybersecurity, predictive maintenance, and resource-recovery analytics, creating sticky service revenues that dilute pure-capex competition.

Digital platforms differentiate entrants; firms offering cloud dashboards with real-time energy and chemical optimization secure multiyear service annuities worth 8–10% of project value. Fragmentation persists in low-tier equipment, but high-barrier segments such as ceramic membranes, electrode-deionization, and AnMBR units see consolidation around fewer than ten suppliers. White-space innovators integrate AI-driven sludge digesters that improve gas yield by 12% and lower polymer usage by 15%, attacking pain points of older municipal plants. Taken together, the China water and wastewater treatment technology market shows a moderate concentration level with increasing premium on integrated, digital-ready offerings.

China Water And Wastewater Treatment (WWT) Technology Industry Leaders

Beijing Enterprises Water Group Limited (BEWG)

DuPont

Veolia

Xylem

Ecolab Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Veolia has finalized the acquisition of CDPQ's 30% stake in Water Technologies & Solutions (WTS) for USD 1.75 billion, strengthening its position in China's industrial water treatment market. This transaction boosts Veolia's membrane technology portfolio and manufacturing capacity for advanced treatment systems in the semiconductor and pharmaceutical industries.

- June 2025: DuPont announced that the Foshan Jialida Dyeing Minimal Liquid Discharge (MLD) project in China has been recognized as the Industrial Water Project of the Year at the 2025 Global Water Awards, hosted by Global Water Intelligence. The project utilizes DuPont's advanced water treatment technologies to enable efficient treatment, reuse, and resource recovery.

China Water And Wastewater Treatment (WWT) Technology Market Report Scope

Water and wastewater treatment is mainly beneficial in various industries, such as power generation, chemicals, oil and gas, mineral processing, municipal water treatment, and pulp and paper, which require water for day-to-day activities. The market is segmented based on equipment type and end-user industry. The market is segmented by type into treatment equipment, process control equipment, and pumps. The end-user industry segments the market into municipal, food and beverage, pulp and paper, oil and gas, healthcare, poultry and agriculture, chemical, and other end-user industries. The report offers market size and forecasts for the China water and wastewater market in revenue (USD million) and for all the above segments.

By Equipment Type

| Treatment Equipment | Oil/Water Separation |

| Suspended Solids Removal | |

| Dissolved Solids Removal | |

| Biological Treatment | |

| Metal Recovery | |

| Disinfection/Oxidation | |

| Others | |

| Process Control Equipment and Pumps |

By End-user Industry

| Municipal Water and Wastewater Treatment |

| Food and Beverage Industry |

| Pulp and Paper Industry |

| Oil and Gas |

| Healthcare Industry |

| Poultry and Aquaculture |

| Chemical Industry |

| Other Industries |

| By Equipment Type | Treatment Equipment | Oil/Water Separation |

| Suspended Solids Removal | ||

| Dissolved Solids Removal | ||

| Biological Treatment | ||

| Metal Recovery | ||

| Disinfection/Oxidation | ||

| Others | ||

| Process Control Equipment and Pumps | ||

| By End-user Industry | Municipal Water and Wastewater Treatment | |

| Food and Beverage Industry | ||

| Pulp and Paper Industry | ||

| Oil and Gas | ||

| Healthcare Industry | ||

| Poultry and Aquaculture | ||

| Chemical Industry | ||

| Other Industries |

Key Questions Answered in the Report

What is the current value of the China water and wastewater treatment technology market?

The market is valued at USD 17.39 billion in 2026 with an 8.20% CAGR through 2031.

Which segment holds the largest share within Chinese treatment equipment?

Treatment equipment dominates with 90.02% share, largely due to membrane bioreactors and advanced oxidation units.

Which end-user sector is growing fastest?

Food and beverage sites post a 9.30% CAGR as export standards demand ultrapure and nutrient-recovery systems.

How are ZLD mandates influencing technology choices?

ZLD rules enforce 95% water recovery, pushing facilities toward multistage RO, evaporation, and ceramic membranes.

Why is ultrapure-water demand rising in China?

Expansion of semiconductor fabs and EV battery plants requires resistivity above 18 megohm-cm, creating high-margin opportunities for specialty providers.

What factors shape regional investment patterns?

Eastern provinces benefit from stricter regulations and higher tariffs, while central regions gain from industrial relocation and PPP incentives.

Page last updated on: