Electrodeionization (EDI) Technology Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

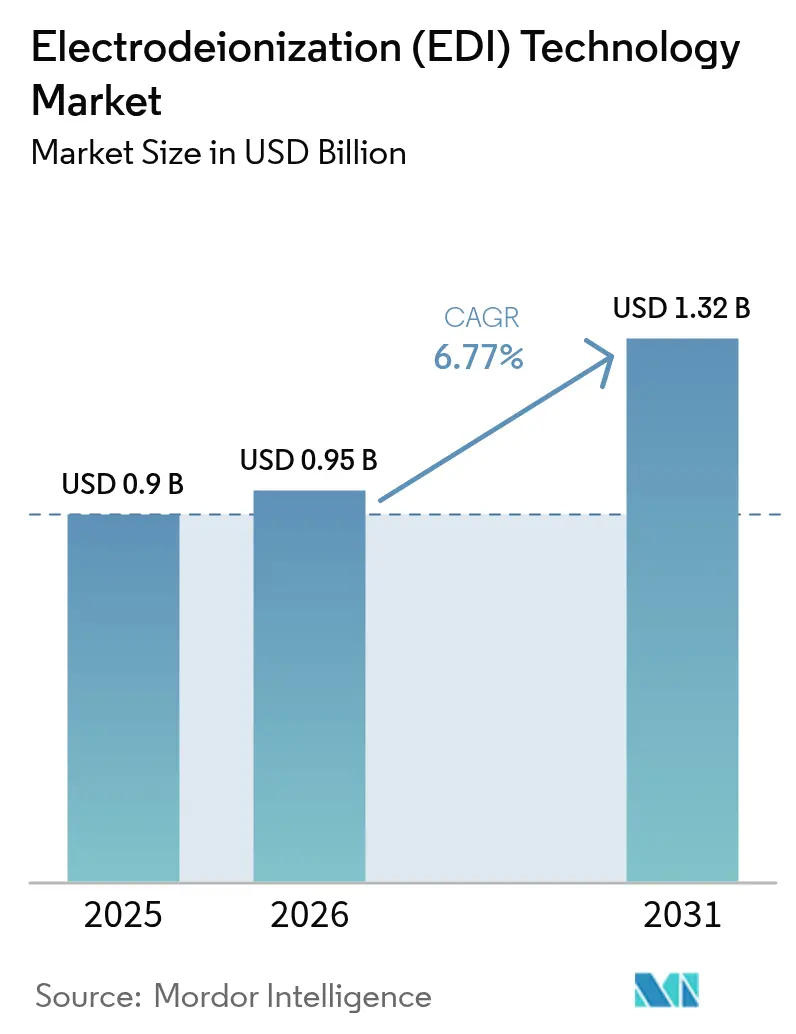

| Market Size (2026) | USD 0.95 Billion |

| Market Size (2031) | USD 1.32 Billion |

| Growth Rate (2026 - 2031) | 6.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

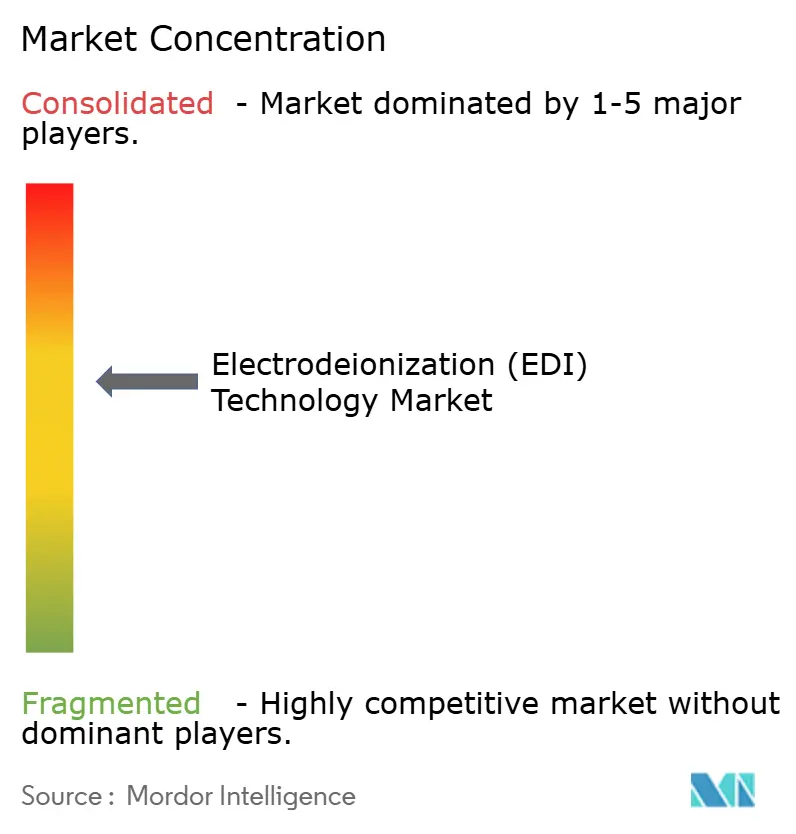

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrodeionization (EDI) Technology Market Analysis by Mordor Intelligence

The Electrodeionization Technology Market size is expected to increase from USD 0.9 billion in 2025 to USD 0.95 billion in 2026 and reach USD 1.32 billion by 2031, growing at a CAGR of 6.77% over 2026-2031. Five converging forces sustain this climb. Green-hydrogen electrolyzers require water conductivity below 0.1 µS/cm, positioning EDI as the polishing step after reverse osmosis. Continuous bioprocessing lines in cell- and gene-therapy facilities turn to chemical-free EDI modules to avoid batch resin downtime. Edge and micro data centers prefer modular skids that fit tight footprints and eliminate hazardous regenerants. Tougher PFAS discharge limits create a pull for EDI over mixed-bed ion exchange. Finally, direct-lithium-extraction plants in South American salars adopt ultra-low-conductivity makeup water to protect membranes. Taken together, these elements lock in double-digit annual additions across the electrodeionization technology market.

Key Report Takeaways

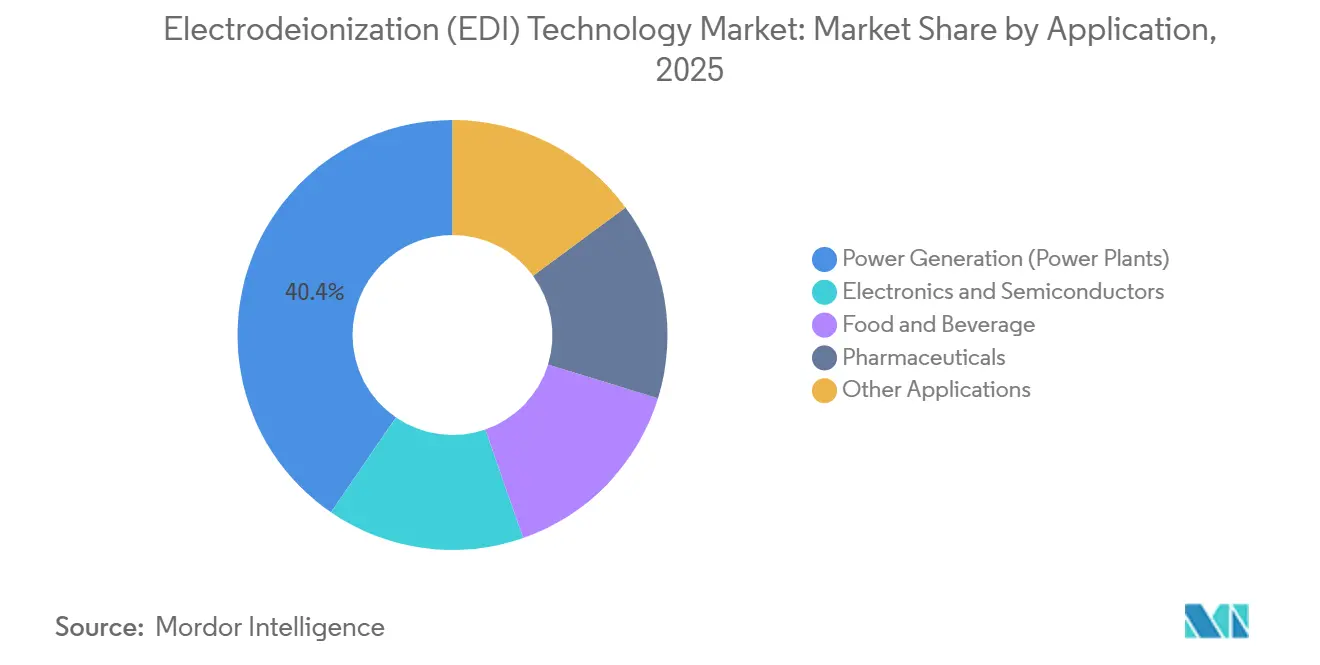

- By application, power generation led with 40.44% of the electrodeionization technology market share in 2025, while pharmaceuticals are forecast to expand at a 7.20% CAGR through 2031, the fastest pace among end users.

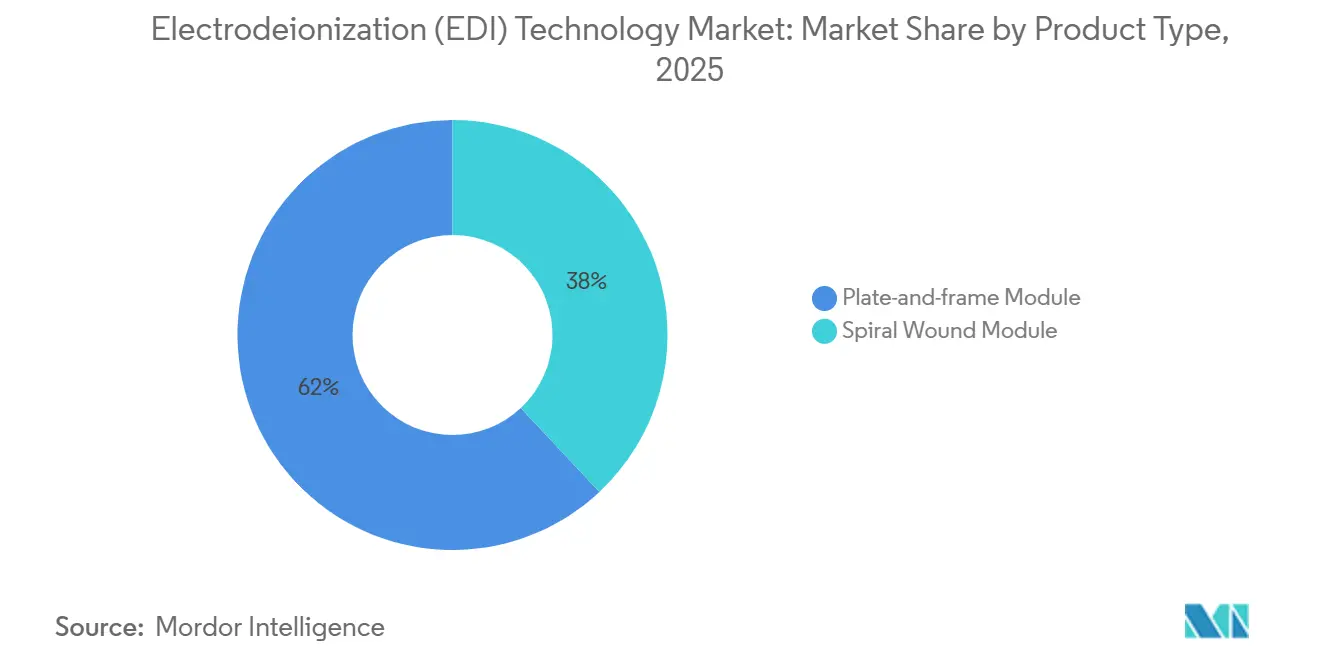

- By product type, plate-and-frame modules captured 61.97% revenue in 2025; spiral-wound modules are projected to post the highest 6.88% CAGR to 2031.

- By geography, Asia-Pacific commanded 41.69% of 2025 sales and is advancing at an 8.05% CAGR through 2031 on semiconductor self-sufficiency programs and hyperscale data-center builds.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electrodeionization (EDI) Technology Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-Hydrogen Electrolyzer Demand for Ultrapure Water | +1.8% | Europe, North America, APAC hydrogen hubs | Medium term (2-4 years) |

| Continuous Bioprocessing Adoption in Cell and Gene-Therapy Plants | +1.5% | Global, concentrated in U.S., Germany, Switzerland | Medium term (2-4 years) |

| Modular EDI Skids for Edge-Cloud Micro-Data-Centers | +1.2% | APAC core, North America, spill-over to MEA | Short term (≤ 2 years) |

| PFAS Discharge Limits Favoring Chemical-Free Polishing | +1.0% | North America, early adoption in EU | Short term (≤ 2 years) |

| Direct-Lithium-Extraction (DLE) Plants Requiring Ultra-Low-Conductivity Water | +0.9% | South America (Chile, Argentina), expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Green-Hydrogen Electrolyzer Demand for Ultrapure Water

Global electrolyzer rollouts mandate feedwater below 0.1 µS/cm, a band that only EDI can hold after RO polish. Germany set a 10 GW domestic target under its National Hydrogen Strategy, matching the United States Hydrogen Shot cost goal of USD 1/kg, and each MW of capacity needs roughly 1–1.5 m³/h of ultrapure water[1]Federal Ministry for Economic Affairs and Climate Action, Germany, “National Hydrogen Strategy,” bmwk.de. Ørsted and bp began pairing offshore wind with coastal hydrogen hubs in 2025, hard-wiring seawater desalination plus EDI into every gigawatt module. The IEA sees global electrolyzer nameplate exceeding 90 GW by 2030, a five-fold rise from 2024 that multiplies demand for compact electrodeionization stacks[2]International Energy Agency, “Hydrogen Projects Database,” iea.org . With RO-EDI trains able to run chemical-free, developers cut logistics at remote renewables sites, lowering OPEX and permitting hurdles across the electrodeionization technology market.

Continuous Bioprocessing in Cell and Gene-Therapy Plants

The U.S. FDA endorsed continuous manufacturing for biologics in 2024, pushing drug makers toward single-use reactors that cannot tolerate regeneration acids or bases. Sartorius trials showed EDI-prepared buffers trimming total cycle times by 30% and reducing hold-step variability for CAR-T batches. Novo Nordisk and Eli Lilly enlarged fill-finish space in 2025 to meet surging GLP-1 demand, installing on-demand water-for-injection loops polished with EDI skids. As patient-specific therapies scale, every hour saved matters, making chemical-free EDI a default in new biologics suites. This shift funnels steady orders into the electrodeionization technology market through 2031.

Modular EDI Skids for Edge-Cloud Data Centers

Edge nodes from 500 kW to 2 MW IT load lack space or permits for acid/caustic regeneration. Equinix mapped 50 new Asia-Pacific metro sites in 2025 that each need make-up water under 10 µS/cm, a target that compact EDI skids hit without chemicals. Microsoft’s Azure for Operators rolls 5G cores into telecom towers where water quality swings daily, again favoring self-contained RO-EDI trains. IEC 62040 now references water parameters for immersion cooling, so system integrators specify EDI to avoid corrosion in backup power circuits. As real-time analytics and VR drive lower latency, every new pod widens the electrodeionization technology market.

PFAS Discharge Limits Favour Chemical-Free Polishing

The U.S. EPA set maximum 4 ppt thresholds for PFOA and PFOS in drinking water during 2024 compliance rounds, pushing industrial dischargers to drop resin waste that can leach trace PFAS. The EU amendment to its Drinking Water Directive caps the sum of 20 PFAS species at 0.5 µg/L, stricter than the U.S. rule. 3M exited PFAS foams in 2024 and pivoted toward fluorine-free chemistries, signalling market realignment. Chemours has invested USD 200 million to run closed-loop EDI polishing at its Fayetteville site to meet consent decree discharge terms. This regulatory drumbeat scales opportunities across the electrodeionization technology market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Risk for Fluoropolymer IEM Precursors | -0.4% | Global, acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Skilled-Labor Shortage for High-Pressure EDI Commissioning | -0.3% | North America, Europe, emerging in APAC | Medium term (2-4 years) |

| Upfront CAPEX Barrier for SMEs in Emerging Economies | -0.3% | South America, Middle East and Africa, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Risk for Fluoropolymer IEM Precursors

Chinese and EU crackdowns on PFAS production pushed Chemours and Solvay's lead times for membrane-grade resins from 12 to 20 weeks in early 2025. DuPont’s 2024 filings note 8% cost inflation on Nafion inputs, costs that cascade to EDI assemblers. The European Chemicals Agency also weighs broad PFAS restrictions with only narrow carve-outs, making long-range supply contracts risky. While firms trial non-fluorinated polymers, chemical stability lags under EDI voltage swings, leaving upstream volatility a short-term brake on the electrodeionization technology market.

Skilled-Labor Shortage for High-Pressure Commissioning

AWWA data show 30% of U.S. water operators hit retirement age by 2029, while trade-school enrollment fell 15% since 2020. Veolia poured EUR 45 million into digital training but still reports 15-20% schedule slips for large-scale start-ups. Xylem partnered with WEF in 2025 to certify just 500 EDI technicians per year, well below semiconductor and green-hydrogen project needs. Premium wages raise installed cost, delaying buys from mid-tier users and trimming growth in the electrodeionization technology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Power Generation Anchors While Pharma Accelerates

Power generation accounted for 40.44% of revenue in 2025 as combined-cycle plants and supercritical boilers require feedwater conductivity below 0.2 µS/cm to protect turbines. However, incremental growth slows because gas turbines consume less makeup water than legacy coal. Pharmaceuticals will post the fastest 7.20% CAGR as regulators endorse continuous manufacturing and the United States Pharmacopeia chapter 643 fixes resistivity above 1 MΩ-cm. Biologics suites adopting single-use bioreactors install compact EDI trains that deliver water-for-injection on demand without chemical regenerants, expanding the electrodeionization technology market across high-margin life-science nodes.

Electronics and semiconductors trail next, driven by Taiwan Semiconductor Manufacturing Company fabs hitting 18.2 MΩ-cm purity for 3 nm nodes. Food and beverage demand stays steady where breweries and dairy plants value uptime over 10 µS/cm conductivity ceilings. Lab, aquarium, and cosmetic users form a mid-single-digit block with consistent replacement orders.

By Product Type: Plate-and-Frame Leads, Spiral-Wound Gains

Plate-and-frame modules held 61.97% of the electrodeionization technology market share in 2025. Operators favor their cassette swaps for high-pressure power and pharma loops while the open architecture eases clean-in-place service. Spiral-wound designs, however, will clock a 6.88% CAGR to 2031 as edge data-center builders demand sub-2 m skid envelopes and food processors chase lower CAPEX. Latest winding machines shrink spacer gaps, lifting current efficiency by near 10% and improving the electrodeionization technology market economics in light-industrial lines.

Hybrid designs combining cassette serviceability with spiral density, launched by DuPont in 2024, target the 5-10 m³/h sweet spot. As hyperscale players bundle tens of micro-pods per metro zone, footprint pressure mounts, handing share to tight-coil elements. Nonetheless, plate-and-frame will remain the default above 10 m³/h where downtime and membrane cost trump space, anchoring over half the electrodeionization technology market through the forecast period.

Geography Analysis

Asia-Pacific booked 41.69% of 2025 revenue, underpinned by 18 new Chinese fabs, India’s USD 10 billion Production-Linked Incentives, and wave after wave of Singapore and Mumbai hyperscale builds. Taiwan Semiconductor’s 20 nm lines consumed 63,000 tons/day of ultrapure water in 2024, each liter polished by EDI, while Samsung’s Pyeongtaek plant recycles close to 90% of process water. Japan’s USD 6.8 billion subsidy for advanced packaging funnels orders toward Kumamoto and Hokkaido nodes, adding another lift. China’s 90% reuse mandate for electronics and chemical sites by 2030 embeds RO-EDI trains deep into coastal industrial parks, securing long-term demand across the electrodeionization technology market.

The North American market is driven by DOE Hydrogen Shot electrolyzer rollouts and semiconductor reinvestment. Intel’s Arizona Fab 42 pushes 30,000 L/min through EDI loops. Eli Lilly’s USD 2.1 billion Indiana campus couples single-use reactors with on-site electrodeionization skids. EPA’s 4 ppt PFAS limit guides industrial dischargers to chemical-free polishing, strengthening aftermarket demand across the electrodeionization technology market.

Europe rides the REPowerEU target of 10 Mt green hydrogen by 2030. Gigawatt projects in Germany, the Netherlands, and Spain each need 1–1.5 m³/h of ultrapure water per MW, fixing electrodeionization into every process line. South America and Middle East and Africa remain low-double-digit today, but Chilean and Argentinian DLE plants plus Saudi Arabia’s 4 GW NEOM electrolyzer site will bolt on hundreds of cubic meters per hour of RO-EDI trains by 2028. Power-grid reliability and skilled-labor gaps restrain broader uptake, yet once-through water bans in mining and petrochemicals tip more projects toward closed-loop electrodeionization technology market solutions.

Competitive Landscape

The electrodeionization technology market stays moderately consolidated. Xylem’s USD 7.5 billion Evoqua integration created a USD 7 billion water platform able to cross-sell EDI into Evoqua’s RO base. Veolia absorbed Suez in 2023, streamlining European offerings and bundling design-build-operate deals for pharma and chip fabs. DuPont rides vertical integration across Nafion ion-exchange and FilmTec RO to win semiconductor specs that favor single-vendor compatibility.

White-space openings bloom in edge data centers, DLE mining, and biologics suites. SnowPure’s cloud-linked controller trims EDI energy by 12% using machine-learning dispatch, an edge for cost-sensitive labs. Patent activity in 2025 shows hybrid electrodialysis-EDI stacks tolerating 5,000 mg/L TDS feeds, priming the electrodeionization technology market for brackish reuse. IEC-62040 water references hardwire EDI into UPS-cooled racks, spurring skid makers to pre-wire remote monitoring.

Regional independents still clinch niche wins. Aquatech sells zero-liquid-discharge EDI trains in U.S. shale plays. Mega secures laboratory contracts across central Europe. Lenntech targets brewery and dairy runs in Benelux. As digital twins and predictive analytics mature, service differentiation rather than hardware may decide margin spreads across the electrodeionization technology market.

Electrodeionization (EDI) Technology Industry Leaders

Veolia

DuPont

Xylem

Newterra

Lenntech B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Xylem committed USD 150 million to triple EDI stack output at its Heerhugowaard, Netherlands plant, opening Q3 2027 lines aimed at European hydrogen and semiconductor projects.

- November 2025: Veolia landed a USD 85 million design-build-operate deal for ultrapure-water systems, including EDI, at a 2 GW semiconductor fab in Karnataka under India’s incentive scheme.

- September 2025: BWT partnered with Siemens Energy to co-develop plug-and-play EDI skids tailored for sub-50 MW PEM electrolyzers in green-hydrogen plants.

Global Electrodeionization (EDI) Technology Market Report Scope

Electrodeionization (EDI) technology is a continuous, chemical-free water treatment process that uses electricity, ion-exchange membranes, and resin to remove ionized impurities (salts and minerals) from water.

The electrodeionization (EDI) technology market is segmented by application, product type, and geography. By application, the market is segmented into power generation (power plants), electronics and semiconductors, food and beverage, pharmaceuticals, and other applications. By product type, the market is segmented into plate-and-frame module and spiral wound module. The report also covers the market size and forecasts for the electrodeionization (EDI) technology market in 15 countries across major regions. For each segment, the market sizing and forecast have been done on the basis of revenue (USD).

| Power Generation (Power Plants) |

| Electronics and Semiconductors |

| Food and Beverage |

| Pharmaceuticals |

| Other Applications |

| Plate-and-frame Module |

| Spiral Wound Module |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Power Generation (Power Plants) | |

| Electronics and Semiconductors | ||

| Food and Beverage | ||

| Pharmaceuticals | ||

| Other Applications | ||

| By Product Type | Plate-and-frame Module | |

| Spiral Wound Module | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the electrodeionization technology market in 2026?

It stands at USD 0.95 billion and is projected to reach USD 1.32 billion by 2031, advancing at a 6.77% CAGR.

Which application segment is expanding the quickest?

Pharmaceuticals are forecast to grow at a 7.20% CAGR through 2031 as continuous bioprocessing drives demand for ultrapure water.

Why are green-hydrogen projects choosing EDI systems?

Proton-exchange-membrane electrolyzers need feedwater below 0.1 µS/cm, and EDI achieves that purity without chemical regenerants.

Which EDI product configuration is set to gain share?

Spiral-wound modules will register a 6.88% CAGR to 2031 because space-constrained data centers prefer their higher packing density.

How concentrated is the supplier landscape?

The five largest vendors control just under 50% of revenue, giving the field a moderate concentration score of 6.

What growth outlook does Asia-Pacific hold?

Asia-Pacific is expected to post an 8.05% CAGR to 2031 on rising semiconductor fabs, data-center builds, and electronics incentives.

Page last updated on: