Defoamers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.49 Billion |

| Market Size (2031) | USD 9.23 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

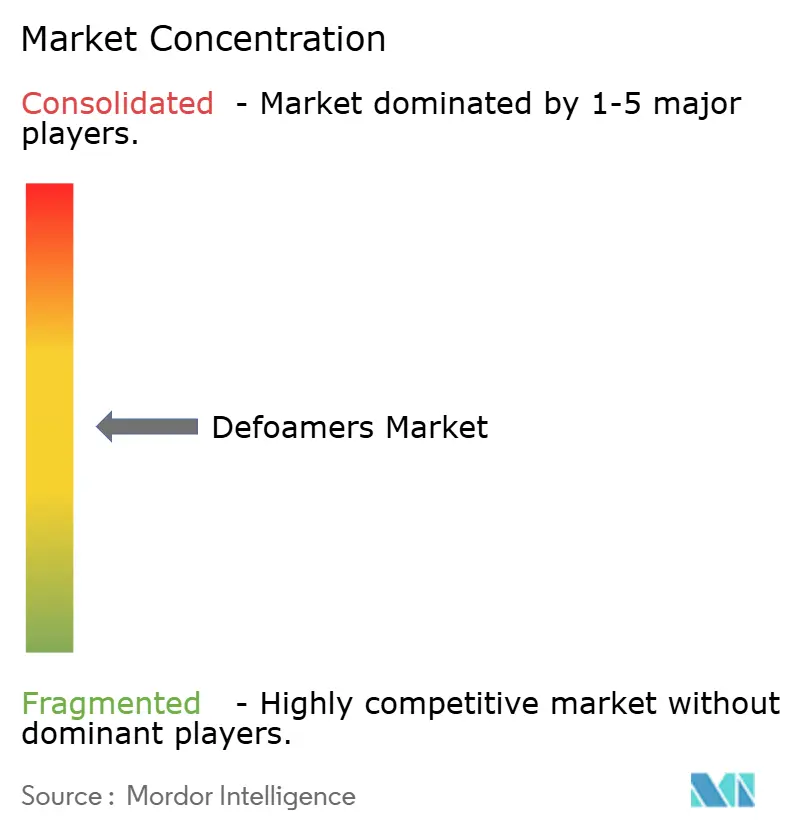

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Defoamers Market Analysis by Mordor Intelligence

The Defoamers Market size is expected to increase from USD 7.19 billion in 2025 to USD 7.49 billion in 2026 and reach USD 9.23 billion by 2031, growing at a CAGR of 4.26% over 2026-2031. Mounting industrial output across the Asia-Pacific, stricter environmental rules that limit volatile organic compounds, and wider use of inline process-control sensors are setting the growth trajectory. Silicone grades currently anchor performance at high temperatures, yet water-based formats are winning share as pulp mills, paint formulators, and membrane bioreactors pursue low-residue options. End-user demand is widening from legacy pulp operations toward paints, coatings, and precision fermentation, while regional producers in India, Indonesia, and Vietnam add new capacity that lifts specialty-chemical consumption. Pricing power is mixed: Shin-Etsu exerts leverage on silicone monomers, but regional blenders continue to tailor cost-effective polymer and vegetable-oil emulsions that fit local regulatory regimes.

Key Report Takeaways

- By type, Silicone-based products held 37.68% of the defoamers market share in 2025. Water-based grades are projected to advance at a 4.98% CAGR through 2031.

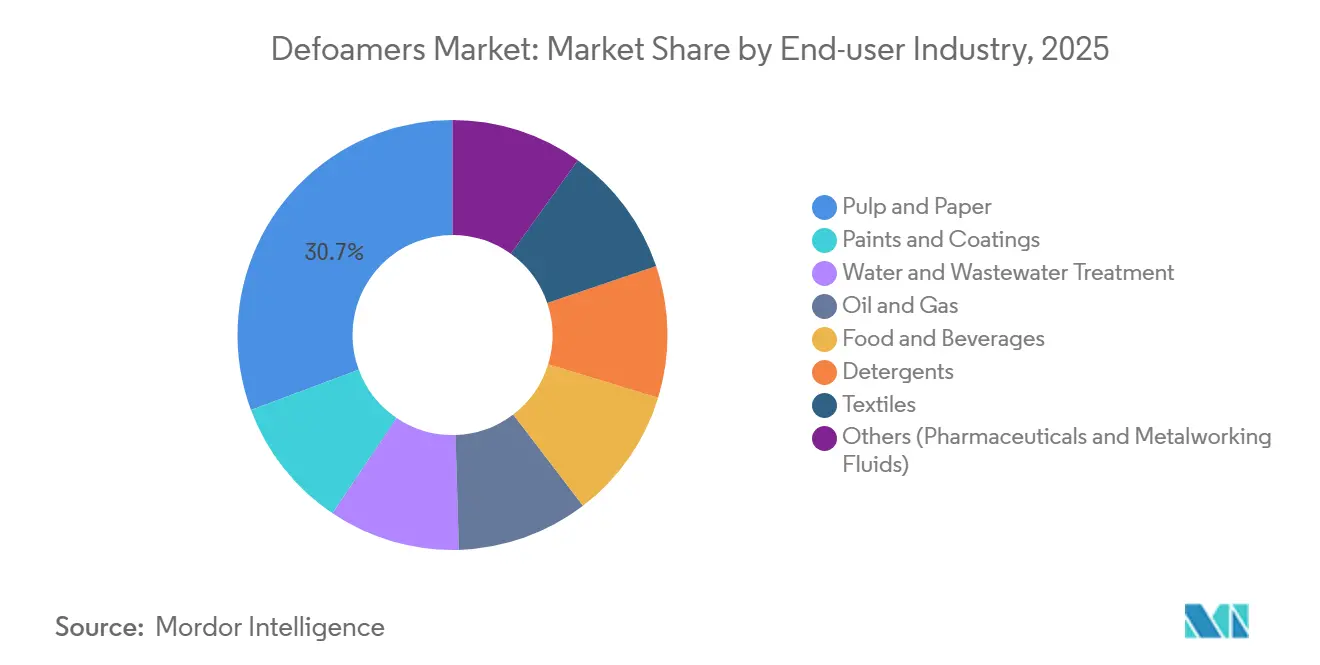

- By end-user industry, Pulp and paper accounted for 30.65% of total demand in 2025. Paints and coatings are set to expand at a 5.67% CAGR to 2031.

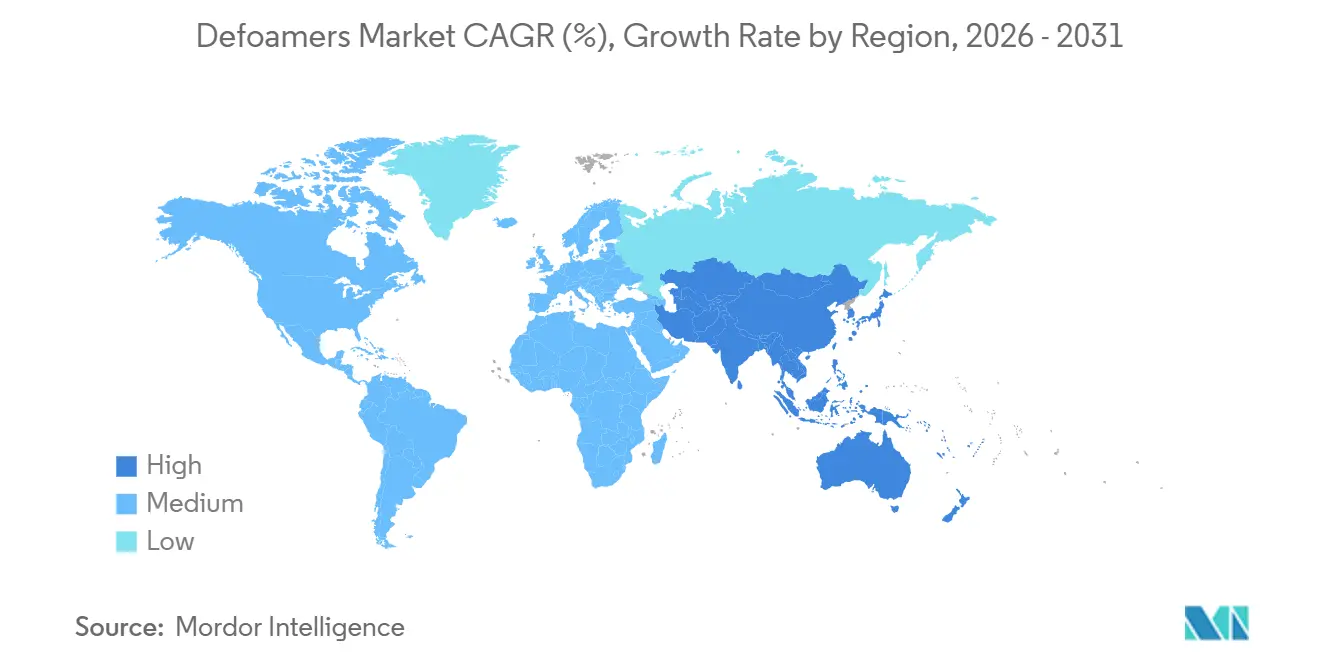

- By geography, North America led with 34.05% revenue share in 2025. Asia-Pacific is forecast to record the fastest regional CAGR at 5.04% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Defoamers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming paints and coatings output in Asia drives high-performance defoamer demand | +1.2% | China, India, Vietnam, spillover to Gulf states | Medium term (2-4 years) |

| Pulp and paper capacity additions in India and Indonesia expand process-chemical spend | +0.9% | India, Indonesia, selected South America | Medium term (2-4 years) |

| Wastewater reuse mandates spur antifoam use in MBR and RO plants | +0.7% | North America, Europe, Middle East, global roll-out | Long term (≥4 years) |

| Inline optical and ultrasonic sensors require non-fouling, low-silicone formulations | +0.5% | United States, Germany, Japan, South Korea | Short term (≤2 years) |

| Composite resins for offshore wind and green-hydrogen equipment specify ultra-low VOC antifoam | +0.4% | North Sea, Atlantic seaboard, East Asia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Booming Paints And Coatings Output In Asia Drives High-Performance Defoamer Demand

Asia-Pacific paint production exceeded USD 89.4 billion in 2024, and new decorative-paint lines in Indore and Mysore now draw significant volumes of specialty defoamers[1]Company Press Release, “Asian Paints Capacity Expansion,” asianpaints.com. Capacity additions in China and Vietnam echo this trend, while BASF’s neopentyl-glycol complex in Zhanjiang supplies powder-coating binders that need thermally stable antifoam above 180°C. Bio-renewable polyether-modified polysiloxanes help formulators hit GB 18582-2020 VOC limits and secure 15% price premiums over commodity emulsions. Suppliers note a two-tier market: low-cost silicone emulsions face shrinking margins, whereas polymer concentrates benefit from stricter quality benchmarks. Growing OEM demand for blemish-free automotive finishes further reinforces the premium tier, lifting average selling prices across the defoamers market.

Pulp And Paper Capacity Additions In India And Indonesia Expand Process-Chemical Spend

India’s 850 pulp mills are running near full capacity, pushing new investments that enlarge chemical budgets for antifoam. APRIL Group’s USD 2.1 billion folding-boxboard mill in Riau alone is expected to consume up to 4,000 tonnes of defoamer yearly. Closed white-water loops favor polyether-polyol emulsions, while membrane bioreactors require silicone-free alternatives to protect flux over seven-year design lives[2] Fraunhofer IVV, “Sensor-Based Foam Control Study,” ivv.fraunhofer.de. These technical pivots explain why water-based products are outgrowing the wider defoamers market. Indonesian forestry policy and India’s chemical incentive scheme further derisk greenfield spending, sustaining a positive outlook through 2031.

Wastewater Reuse Mandates Spur Antifoam Use In MBR And RO Plants

Zero-liquid-discharge rules in California, the Gulf, and India demand strict foam control inside membrane bioreactors. Operators typically dose 5-50 ppm of low-molecular-weight polyether polyols to keep trans-membrane pressure within specification. Silicone oils risk fouling polyvinylidene-fluoride modules, shortening life by two years and raising capital costs. ISO 14001 audits favor suppliers with documented aquatic-toxicity data, directing new orders toward vegetable oil and glycerin emulsions. Wider desalination build-outs across Saudi Arabia and the United Arab Emirates reinforce long-run consumption in this high-value niche.

Inline Optical / Ultrasonic Sensors Require Non-Fouling, Low-Silicone Formulations

Automated foam detectors in bioreactors and food fermenters lose signal accuracy once sensor faces collect silicone residue, a drop measured at roughly 12% after several weeks of operation. Polyether-polyol defoamers leave 80% less film on stainless steel than traditional polydimethylsiloxane. Pharmaceutical contract manufacturers, therefore, mandate silicone-free grades that meet FDA 21 CFR 173.340. BASF’s EFKA PB 2770 and Evonik’s TEGO Foamex 8850 exceed 50% bio-content, aligning with cleanroom validation needs. Precision fermentation for alternative proteins follows the same path, expanding the specialty share of the defoamers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silicone-monomer cost spikes and supply shocks | -0.8% | Asia-Pacific, Europe, global ripple effects | Short term (≤2 years) |

| Tightening PFAS-style scrutiny of persistent silicone chemistries | -0.5% | North America, Europe, regulatory spillover to Asia | Medium term (2-4 years) |

| Shift to closed-loop mechanical foam control in zero-discharge plants | -0.3% | India, China, Middle East, selective U.S. sites | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Silicone-Monomer Cost Spikes And Supply Shocks

Shin-Etsu holds half of global D4 and D5 capacity, creating a bottleneck that sharpened price jumps when Shandong’s energy costs rose in late 2024. Spot prices climbed 18% quarter over quarter, squeezing formulators tied to pulp, paper, and textile clients that resist pass-through increases. Wacker Chemie’s 40,000 tonne pyrogenic-silica line eases specialty grades but fails to balance bulk monomer supply. The volatility motivates converters to lock in glycerin, fatty-acid, and ethylene-oxide-based alternatives whose feedstocks are geographically diverse. BASF and Evonik price their bio-renewable products 10-15% above silicone emulsions yet offer steadier input costs, insulating margins in the defoamers market.

Tightening PFAS-Style Scrutiny Of Persistent Silicone Chemistries

EU chemical strategy discussions now consider certain cyclic siloxanes to be persistent and bio-accumulative. California’s PFAS ban in textiles, effective 2025, frames silicones as potential “forever chemicals,” spurring apparel and detergent brands to pre-emptively reformulate. Ecolab and Evonik patents offer vegetable-oil emulsions that cut persistent-chemical content by 95% while sustaining knock-down efficiency. Full product verification under ASTM D6866 and OECD aquatic tests adds up to USD 25,000 per SKU, a burden smaller regional blenders struggle to carry. The compliance cost, therefore, accelerates consolidation within the defoamers industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Bio-Renewable Chemistries Challenge Silicone Dominance

Silicone products still lead, yet water-based offerings are accelerating at 4.98% CAGR. In 2025, silicone held a 37.68% share of the defoamers market size and remains essential in high-temperature coatings. Polymer and vegetable-oil emulsions’ growth reflects end-users’ preference for low-VOC and sensor-friendly profiles. Powder formats for dry-mix mortars grow steadily with India’s construction boom. Tight supplies of D4 and D5 also encourage migration to glycerin and fatty-acid feedstocks that carry more stable pricing. The defoamers market, therefore, shows clear segmentation between commodity silicone emulsions under margin pressure and specialty bio-renewable grades capturing value premiums.

Water-based systems benefit from closed-loop pulp mills and membrane bioreactors that prohibit silicone residue. BASF’s EFKA PB 2770 and Evonik’s TEGO Foamex 8850 illustrate the shift, each commanding double-digit price premiums and winning early adoption in UV-curable and food-contact applications. Oil-based mineral emulsions retain share in brown-stock washing but face a slower 3.2% CAGR because of tightening VOC caps. Continued innovation around hybrid vegetable-oil and polyether blends is expected to reshape the competitive map as suppliers reposition portfolios toward high-margin concentrates.

By End-User Industry: Paints And Coatings Outpace Legacy Pulp Demand

Pulp and paper remain the single largest end-use at 30.65% of 2025 revenue, yet paints and coatings deliver the quickest expansion at 5.67% CAGR. Asian Paints’ recent expansions in Indore and Mysore alone lift regional demand by up to 10,000 tonnes yearly, favoring water-based and polymer concentrates that meet stricter VOC laws. Powder-coating resins from BASF’s Zhanjiang site also need high-temperature stability that only specialty defoamers provide.

Water and wastewater treatment's market share is expected to grow as global desalination and reuse projects multiply. Oil and gas, despite deep-water projects in Brazil and Guyana, record moderate growth because upstream budgets remain cautious. Food and beverages, detergents, textiles, and pharmaceutical cleanrooms together sustain steady mid-single-digit growth, driven by regulatory needs for clean-label and sterile formulations. Each of these uses rewards low-residue chemistry, reinforcing demand shifts within the defoamers market.

Geography Analysis

North America led revenues with a 34.05% share in 2025 as mature water-reuse assets and strict zero-discharge rules elevated antifoam dosing. California’s PFAS legislation pushes textile and detergent formulators toward bio-renewable solutions, reinforcing specialty demand. Canadian pulp mills retrofitting closed loops now specify silicone-free emulsions to protect membranes, while Mexican automotive paint shops adopt high-performance water-based defoamers to meet national VOC caps. Dow’s purchase of Circulus Holdings underlines a regional pivot toward circular and specialty materials that shape future product design.

Asia-Pacific is the growth engine, forecast at 5.04% CAGR through 2031. China anchors demand with new powder-coating resins, India scales capacity under its chemical incentive plan, and Southeast Asian mills add folding-boxboard and coatings output. Inline sensor adoption in Japan and South Korea accelerates trials of non-fouling defoamers. Across the region, stricter GB 18582-2020 and ASEAN standards steer buyers toward polymer and water-based technology. These factors consolidate the defoamers market as the essential process additive alongside dispersion and wetting aids.

Europe’s market growth is moderated by mature demand yet supported by the EU Industrial Emissions Directive and offshore-wind supply chain growth. Wacker Chemie’s backward integration improves local security of supply for specialty silicone intermediates. In-mold gelcoating further tightens specifications for ultra-low-VOC antifoam as blade manufacturers target recyclable composite systems. South America and the Middle East & Africa track mid-single-digit growth on the back of oil, gas, and agro-processing expansions, with GCC desalination plants adopting sensor-linked dosing that reduces overall volumes yet raises value per kilogram.

Competitive Landscape

The Defoamers Market is moderately consolidated. Shin-Etsu’s 50% share of D4/D5 monomer capacity affords raw-material leverage, yet downstream formulations remain fragmented across dozens of regional blenders. BASF, Dow, Evonik, and Wacker Chemie invest in bio-renewable and sensor-compatible grades that fetch 15-20% price uplifts. Moreover, offshore wind and green-hydrogen composites add further pull for ultra-low-VOC products. Suppliers able to certify bio-content and low ecotoxicity under global standards look set to capture expanding value pools inside the defoamers market.

Defoamers Industry Leaders

Evonik Industries AG

BASF

Dow

Wacker Chemie AG

Momentive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Evonik Coating Additives introduced TEGO Foamex 8051, the latest addition to its TEGO Foamex line of defoamers. This new siloxane defoamer is specifically designed for use in waterborne decorative coatings. It provides a cost-effective solution for high-performance applications while meeting strict environmental regulations.

- April 2025: PennWhite India (PWI) Private Limited, a company incorporated in India for specialty chemicals, a wholly owned subsidiary of PennWhite Limited, UK, announced its intent to build a manufacturing plant for the manufacture of foam control chemistry in Chennai, India. PWI is a manufacturer of antifoam chemistry under the FoamDoctor brand.

Global Defoamers Market Report Scope

Defoamers, commonly referred to as anti-foaming agents, are substances that prevent foam from forming during various industrial operations. Defoamer's low viscosity, fast spreading, and low affinity for air-liquid interfaces are some of its essential characteristics. The market is segmented based on type, end-user, and geography. The market is segmented by type into oil-based defoamer, emulsion defoamer, silicone-based defoamer, powder defoamer, polymer-based defoamer, and other types. End-users segment the market into paints and coatings, oil and gas, pulp and paper, food and beverages, water and wastewater treatment, and other end-user industries. The report offers market size and forecasts for 27 countries across major regions. For each segment, market sizing and forecasts are based on revenue (USD) for all the above segments.

| Silicone-based |

| Water-based |

| Oil-based |

| Powder Defoamers |

| By Other Types (Polymer / Vegetable-based) |

| Paints and Coatings | |

| Pulp and Paper | |

| Water and Waste-water Treatment | |

| Oil and Gas | |

| Food and Beverages | |

| Detergents | Homecare |

| Industrial | |

| Textiles | |

| Others (Pharmaceuticals, Metalworking Fluids) |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| Vietnam | |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Turkey | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Qatar | |

| Nigeria | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Type | Silicone-based | |

| Water-based | ||

| Oil-based | ||

| Powder Defoamers | ||

| By Other Types (Polymer / Vegetable-based) | ||

| By End-user Industry | Paints and Coatings | |

| Pulp and Paper | ||

| Water and Waste-water Treatment | ||

| Oil and Gas | ||

| Food and Beverages | ||

| Detergents | Homecare | |

| Industrial | ||

| Textiles | ||

| Others (Pharmaceuticals, Metalworking Fluids) | ||

| By Geography (Value) | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| Vietnam | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Turkey | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Qatar | ||

| Nigeria | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the defoamers market in 2026 and how fast is it growing?

How large is the defoamers market in 2026 and how fast is it growing?

Which product type leads demand in defoamers?

Which product type leads demand in defoamers?

What end-use segment is expanding the fastest?

What end-use segment is expanding the fastest?

Which region shows the highest near-term growth?

Which region shows the highest near-term growth?

How are regulations influencing product innovation?

How are regulations influencing product innovation?

Page last updated on: