Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

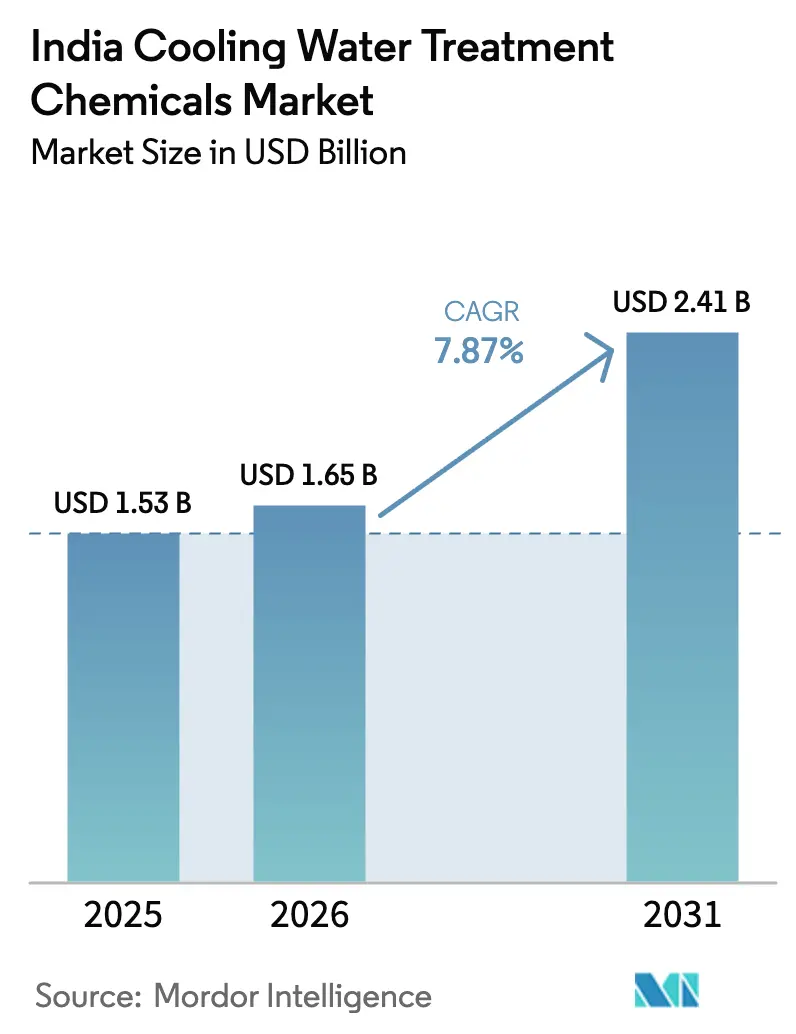

| Base Year Market Size (2025) | USD 1.53 Billion |

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 7.87% CAGR |

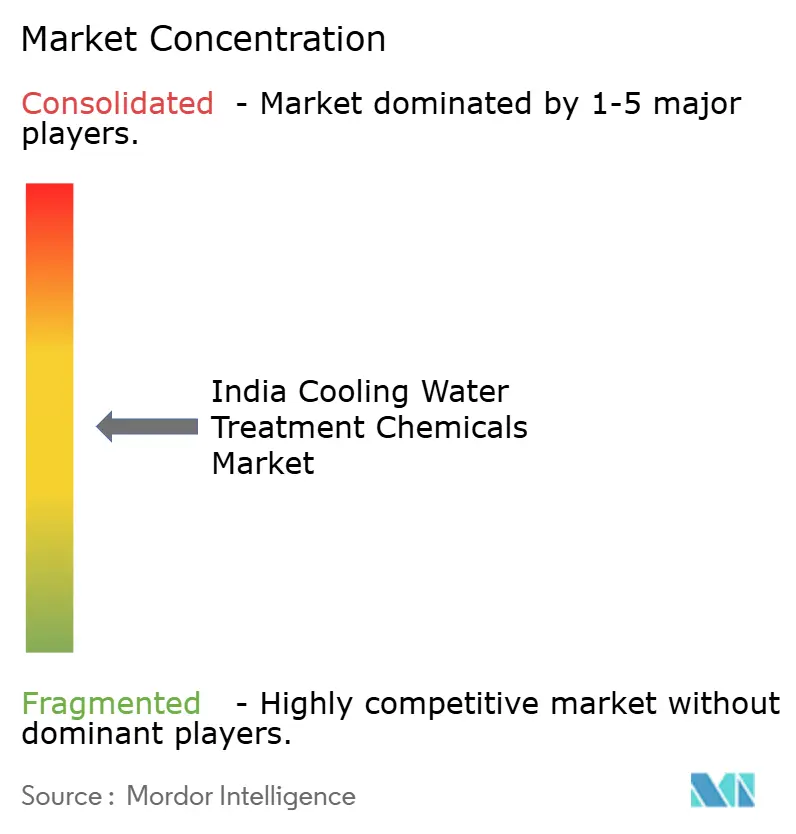

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Cooling Water Treatment Chemicals Market Analysis by Mordor Intelligence

The India Cooling Water Treatment Chemicals Market size is projected to be USD 1.53 billion in 2025, USD 1.65 billion in 2026, and reach USD 2.41 billion by 2031, growing at a CAGR of 7.87% from 2026 to 2031. Stricter discharge norms, expanding zero-liquid-discharge (ZLD) mandates, and large-scale capacity additions in power, steel, petrochemicals, and data centers are lifting chemical demand. The Tariff Policy 2016 requirement that thermal stations within 50 km of cities switch to treated sewage water is accelerating municipal-to-industrial reuse, which in turn is boosting consumption of biocides, scale inhibitors, and corrosion-control chemistries formulated for high-recycle cooling environments. Suppliers are differentiating through IoT-enabled dosing, OCEMS-ready monitoring, and service bundles that guarantee compliance. Intensifying data-center investment, already adding 228 MW in 2025, is further stimulating specialty chemical uptake because hyperscale facilities can draw up to 2 million L per day for evaporative cooling. Headline risks include raw-material price volatility and the gradual penetration of membrane-based or physical alternatives that reduce conventional chemical volumes, yet enforcement momentum by state pollution control boards is maintaining a structurally positive outlook.

Key Report Takeaways

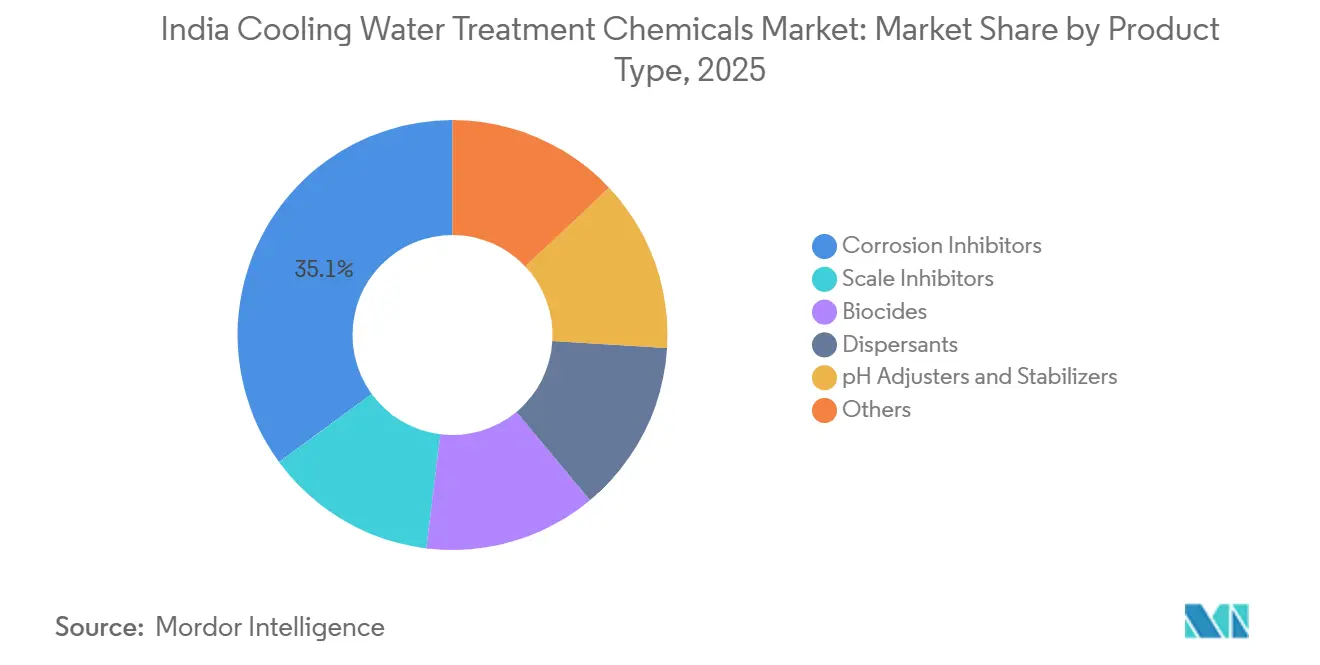

- By product type, corrosion inhibitors led with 35.06% value share in 2025; biocides are projected to grow at an 8.12% CAGR through 2031.

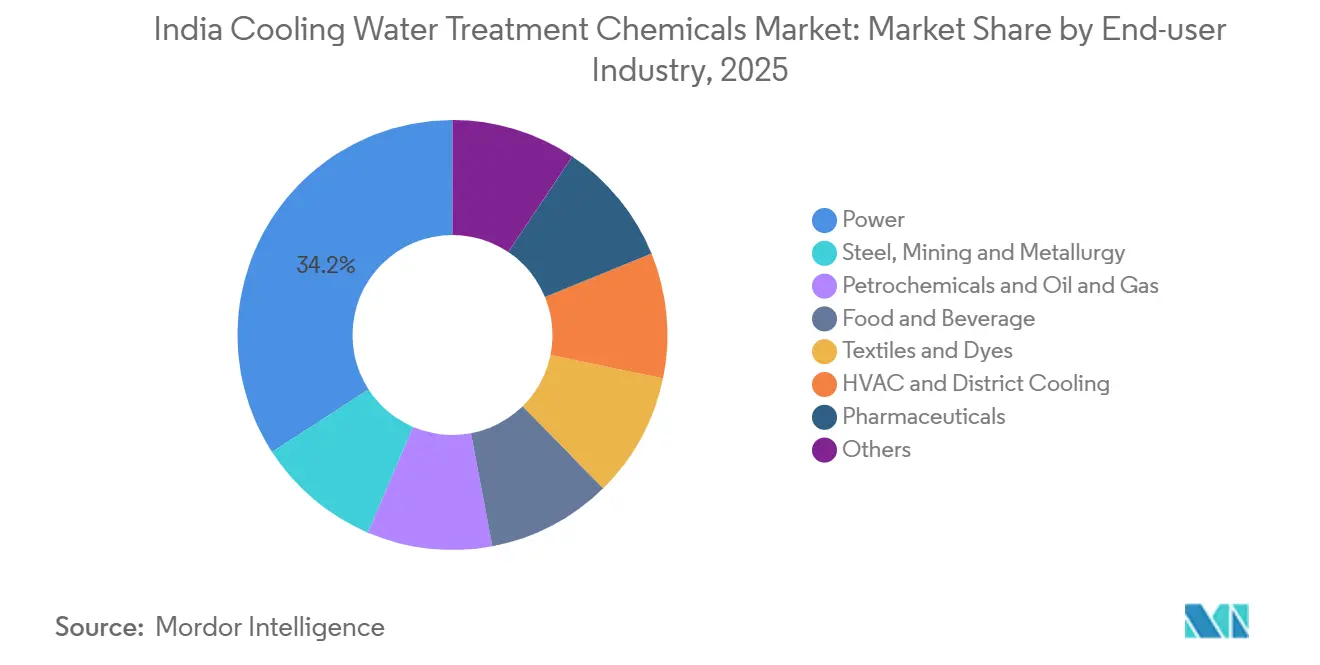

- By end-user industry, the power sector commanded 34.15% of the India Cooling Water Treatment Chemicals market size in 2025, while HVAC and district cooling are poised for the fastest expansion at an 8.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Cooling Water Treatment Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of thermal and renewable power generation capacity | +2.1% | National, concentrated in Gujarat, Maharashtra, Tamil Nadu, Odisha | Medium term (2-4 years) |

| Rising industrial water-reuse and ZLD mandates | +2.5% | National, with early enforcement in Maharashtra, Gujarat, Tamil Nadu, Andhra Pradesh | Short term (≤2 years) |

| Growth in steel, cement and metallurgy capacity additions | +1.4% | National, focused on Odisha, Karnataka, Chhattisgarh, Jharkhand | Medium term (2-4 years) |

| Stricter CPCB discharge norms for cooling towers | +1.3% | National, stringent enforcement in MPCB, GPCB, TNPCB, KSPCB jurisdictions | Short term (≤2 years) |

| Rapid adoption of IoT-enabled real-time dosing and analytics | +0.5% | National, led by hyperscale data centers, large power plants, and Tier-1 industrial hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of Thermal and Renewable Power Generation Capacity

India operated 226 GW of coal capacity in 2025, and flexible ramping to accommodate 135.8 GW of solar is heightening thermal cycling that intensifies corrosion, scaling, and microbiological fouling in cooling loops[1]Ember, “India Power Tracker 2026,” ember.climate. Central Electricity Authority guidelines pushing coal units to a 40% minimum-load target by 2030 increase transient stresses, prompting higher-performance corrosion inhibitors that tolerate rapid temperature swings. Battery-storage retrofits at legacy plants are shifting water-duty profiles, necessitating product chemistries stable across variable flow regimes. Simultaneously, case-by-case exemptions from mandatory cooling-tower installation under the Environment (Protection) Third Amendment Rules 2025 will create a patchwork of once-through, hybrid, and recirculating systems, each demanding tailored chemical programs. The resulting complexity underpins service-bundle contracts that guarantee performance across heterogeneous cooling assets.

Rising Industrial Water-Reuse and ZLD Mandates

Central Pollution Control Board (CPCB)’s ZLD (Zero Liquid Discharge) mandate for 17 highly polluting sectors has made high-recovery treatment trains, reverse osmosis, MVR (Mechanical Vapor Recompression) evaporation, and crystallization standard for new capacity, particularly in textiles and pharmaceuticals[2]Central Pollution Control Board, “General Standards for Discharge of Environmental Pollutants,” cpcb.nic.in. These circuits require robust antiscalants capable of stabilizing calcium sulfate and silica at TDS levels above 70,000 ppm, plus antifoams and sludge conditioners to optimize MVR and crystallizer operation. ZLD operating costs of INR 80-150 per m³ compared with INR 15-30 per m³ for conventional treatment are intensifying the customer focus on high-efficacy formulations that extend membrane life and cut cleaning frequency. Rajasthan’s Data Centre Policy 2025 goes beyond industrial norms by mandating ZLD, rainwater harvesting, and groundwater recharge at every new facility, setting a template other states are expected to follow.

Growth in Steel, Cement and Metallurgy Capacity Additions

JSW Steel is expanding from 34.2 MTPA (million tonnes per annum) to about 50 MTPA by FY 2031, anchored by its 19 MTPA Vijayanagar upgrade, Dolvi Phase III expansion, and a 30 MTPA greenfield plant in Odisha. Blast-furnace and casting operations will lift regional demand for oxygen scavengers, filming amines, and heavy-metal precipitants needed to comply with CPCB limits for zinc, chromium, and phosphate in blowdown streams. Closed-loop cooling adoption is growing to meet those discharge thresholds, intensifying reliance on phosphate-free formulations and biodegradable dispersants that maintain heat-transfer performance under higher recycle ratios.

Stricter CPCB Discharge Norms for Cooling Towers

CPCB’s 2026 standards tightened Biochemical Oxygen Demand (BOD) to 10 mg/L, Chemical Oxygen Demand (COD) to 50 mg/L, and TSS to 10 mg/L, and narrowed pH to 6.5-8.5, all verified by 15-minute Online Continuous Effluent Monitoring Systems (OCEMS) data uploads. Plant operators are integrating membrane bioreactors and advanced oxidation to achieve the new thresholds, which reduces bulk coagulant volumes but raises demand for biocompatible pH agents, micronutrients, and frequent membrane cleanings. Textile mills trialing bioaugmentation recorded 70% lower chemical use and 60% less sludge, demonstrating substitution pressure on traditional chemistry, yet the same mills invested in online corrosion monitors and fluorometer-based polymer analyzers, reinforcing the market for precision-dosing additives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of specialty chemical raw materials | -0.8% | National, with acute exposure in import-dependent formulations | Short term (≤2 years) |

| Uptake of physical / membrane-based non-chemical alternatives | -0.6% | National, concentrated in high-TDS applications and water-scarce regions | Medium term (2-4 years) |

| Shortage of skilled cooling-water chemists and operators | -0.3% | National, more acute in Tier-2/3 industrial clusters | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Specialty Chemical Raw Materials

Phosphonate, polycarboxylate, and isothiazolinone inputs are exposed to swings in phosphorus, acrylic acid, and zinc prices, which suppliers pass through via quarterly formulas. Ion Exchange’s INR 450 crore (USD 4.95 billion) Roha plant will localize part of the supply chain, yet its ramp-up to 25% utilization by FY 2027 means import-linked exposure persists in the near term. Volatility complicates budgeting for thermal power stations operating under regulated tariffs, occasionally prompting a reversion to legacy chemistries that trade off performance for lower upfront cost.

Uptake of Physical or Membrane-Based Non-Chemical Alternatives

Electrodialysis reversal, forward osmosis, and capacitive deionization concentrate blowdown with minimal chemical input. Ion Exchange’s new hollow-fiber Ultrafiltration (UF) and Membrane Bioreactors (MBR) membrane venture with MANN+HUMMEL exemplifies supplier hedging, while Thermax’s Chinchwad plant now assembles CDI modules alongside conventional softeners. Although membranes still need specialty antiscalants and clean-in-place reagents, net volumes of conventional dispersants and coagulants fall in facilities that adopt high-recovery trains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Corrosion-Control Dominance, Biocide Acceleration

Corrosion inhibitors accounted for a 35.06% India Cooling Water Treatment Chemicals market share in 2025, and the segment is expected to register decent growth as multi-metal systems run under higher conductivity regimes. Nitrite-based passivators with tracer dyes allow quick leak detection in closed-loop HVAC circuits, lowering water loss and chemical make-up. Integrated blends with polymers and phosphonate-free dispersants are simplifying inventories in steel and petrochemical complexes.

Biocides, advancing at an 8.12% CAGR during the forecast period (2026-2031), are benefiting from CPCB’s sub-10 mg/L BOD and TSS (Total Suspended Solids) thresholds that force tighter microbial control. Dual-biocide regimens combining oxidative agents with isothiazolinone or glutaraldehyde are common in ZLD installations where recycled condensate elevates bio-load. IoT (Internet of Things) dosing skids that trend Oxidation-Reduction Potential (ORP) and residual oxidant maintain narrow setpoints, reducing overfeed risk yet driving consistent baseline consumption. Scale inhibitors and dispersants, though growing more slowly, remain indispensable in Mechanical Vapor Recompression (MVR) and crystallizer circuits where silica, calcium sulfate, and mixed-salt scaling risk is acute above 70,000 ppm Total Dissolved Solids (TDS). pH adjusters, antifoams, and oxygen scavengers round out specialty demand tied to boiler blowdown segregation, high-temperature condensate loops, and dewatering operations.

By End-user Industry: Power Leads, HVAC Surges on Digital Infrastructure

The power sector generated 34.15% of India Cooling Water Treatment Chemicals market revenue in 2025, buttressed by 226 GW of coal capacity and the rule mandating sewage-treated water for plants near urban centers. Variable load operations are creating cyclic corrosion stresses, spurring uptake of advanced filming amines and polymer dispersants. The India Cooling Water Treatment Chemicals industry is also witnessing bundled service contracts that guarantee specific water consumption below 3.5 m³/MWh at a competitive cost.

HVAC and district cooling are the fastest-growing verticals, climbing at an 8.09% CAGR during the forecast period (2026-2031) as India’s data-center footprint is projected to hit 1.7 GW by end-2026. Hyperscale operators are piloting immersion and direct-to-chip cooling that require dielectric fluids blended with corrosion inhibitors compatible with copper and aluminum cold plates. Steel and metallurgy expansion, led by JSW, underpins multi-year demand for oxygen scavengers and heavy-metal precipitants, while petrochemical mega-projects such as BPCL’s INR 49,000 crore (USD 592.9 billion) Bina upgrade will add continuous heat-exchanger loads that depend on polymer phosphonate blends for deposit control. Food, beverages, textiles, and pharmaceuticals provide steady demand for NSF-certified, food-contact-safe additives, particularly where ZLD mandates intersect with product safety standards.

Geography Analysis

Western and southern states dominate consumption. Maharashtra’s MPCB (Maharashtra Pollution Control Board) enforcement teams have installed OCEMS across Thane-Belapur and Pune belts, compelling operators to adopt digital dosing platforms that log residuals every 15 minutes. Gujarat targets 100% water reuse by 2030, so refineries in Jamnagar and petrochemicals in Dahej are retrofitting high-recovery RO trains that elevate demand for silica-tolerant antiscalants. Tamil Nadu’s textile hub in Tiruppur relies on bioaugmentation and sludge-minimization programs to stay within ZLD adequacy guidelines issued in January 2025.

Odisha and Chhattisgarh are rising fast as JSW and NMDC (National Mineral Development Corporation) commission new steel and mining lines, bringing demand for high-temperature corrosion inhibitors and heavy-metal precipitants. Karnataka and Andhra Pradesh are emerging data-center and semiconductor clusters; Bengaluru’s 2025 data-center policy offers 10-year power-duty exemptions that are attracting hyperscale investments, each requiring closed-loop chilled-water conditioning. Rajasthan’s policy mandating wastewater recycling and ZLD for every new data center is steering chemical suppliers toward bundled offerings that include RO, MVR, and crystallizer chemistry along with IoT analytics.

Northern growth pockets include Uttar Pradesh, where 100% transmission-duty exemption is catalyzing Noida’s edge data-center boom and lifting demand for packaged cooling-tower programs. Coastal Andhra Pradesh and Tamil Nadu are piloting seawater cooling for colocation campuses, stimulating specialty corrosion inhibitors resistant to 19,000 ppm chloride and biocides active against marine microbes. Across all zones, the India cooling water treatment chemicals market benefits from uniform CPCB standards, yet state-level incentive variations steer supplier deployment strategies and warehouse footprints.

Competitive Landscape

The India Cooling Water Treatment Chemicals market is moderately fragmented. Long-term contracts are shifting from volume-based to performance-indexed, with penalties linked to water-use efficiency or corrosion-rate exceedances. Ecolab’s digital twin platform and Solenis’s Solenis One advanced analytics exemplify moves toward outcome-based sales. Service capacity in Tier-2 cities is the next battleground: firms expanding technician networks and remote-monitoring centers in Bhubaneswar, Lucknow, and Indore are poised to win emerging MSME (Micro, Small, and Medium Enterprises) accounts.

India Cooling Water Treatment Chemicals Industry Leaders

Solenis

Kemira

SUEZ

Ecolab Inc.

Chembond Chemicals Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Tata Chemicals Limited announced plans to set up a new greenfield manufacturing facility in Tamil Nadu as part of its capacity expansion for the production of Iodised Vacuum Salt Dried (IVSD). Such expansion can help boost the demand for cooling water treatment chemicals in India.

- March 2025: India, in a bid to shield its domestic industry, levied an anti-dumping duty of up to USD 986 per tonne on 'Trichloro isocyanuric acid.' This chemical, primarily used for water treatment, is imported from China and Japan. According to a notification from the Ministry of Finance, this duty will be in place for a duration of five years.

India Cooling Water Treatment Chemicals Market Report Scope

Cooling water treatment chemicals prevent scale, corrosion, and biological fouling in cooling towers and heat exchangers to maintain heat transfer efficiency.

The India Cooling Water Treatment Chemicals market is segmented into product type and end-user industry. By product type, the market is segmented into corrosion inhibitors, scale inhibitors, biocides, dispersants, pH adjusters and stabilizers, and others. By end-user industry, the market is segmented into power, steel, mining and metallurgy, petrochemicals and oil and gas, food and beverage, textiles and dyes, HVAC and district cooling, pharmaceuticals, and others. The report also covers the market size and forecasts for cooling water treatment chemicals in value (USD).

By Product Type

| Corrosion Inhibitors |

| Scale Inhibitors |

| Biocides |

| Dispersants |

| pH Adjusters and Stabilizers |

| Others |

By End-user Industry

| Power |

| Steel, Mining and Metallurgy |

| Petrochemicals and Oil and Gas |

| Food and Beverage |

| Textiles and Dyes |

| HVAC and District Cooling |

| Pharmaceuticals |

| Others |

| By Product Type | Corrosion Inhibitors |

| Scale Inhibitors | |

| Biocides | |

| Dispersants | |

| pH Adjusters and Stabilizers | |

| Others | |

| By End-user Industry | Power |

| Steel, Mining and Metallurgy | |

| Petrochemicals and Oil and Gas | |

| Food and Beverage | |

| Textiles and Dyes | |

| HVAC and District Cooling | |

| Pharmaceuticals | |

| Others |

Key Questions Answered in the Report

What is the projected value of the India cooling water treatment chemicals market by 2031?

The India Cooling Water Treatment Chemicals market is forecast to reach USD 2.41 billion by 2031 growing at a CAGR of 7.87% during the forecast period (2026-2031).

Which product category currently holds the largest share?

Corrosion inhibitors led with a 35.06% share in 2025.

Which end-user segment is expanding the fastest?

HVAC and district cooling are growing at an 8.09% CAGR through 2031.

Why are biocides witnessing rapid growth?

Tighter CPCB effluent norms require stricter microbiological control, driving biocide demand at an 8.12% CAGR.

Page last updated on: