Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

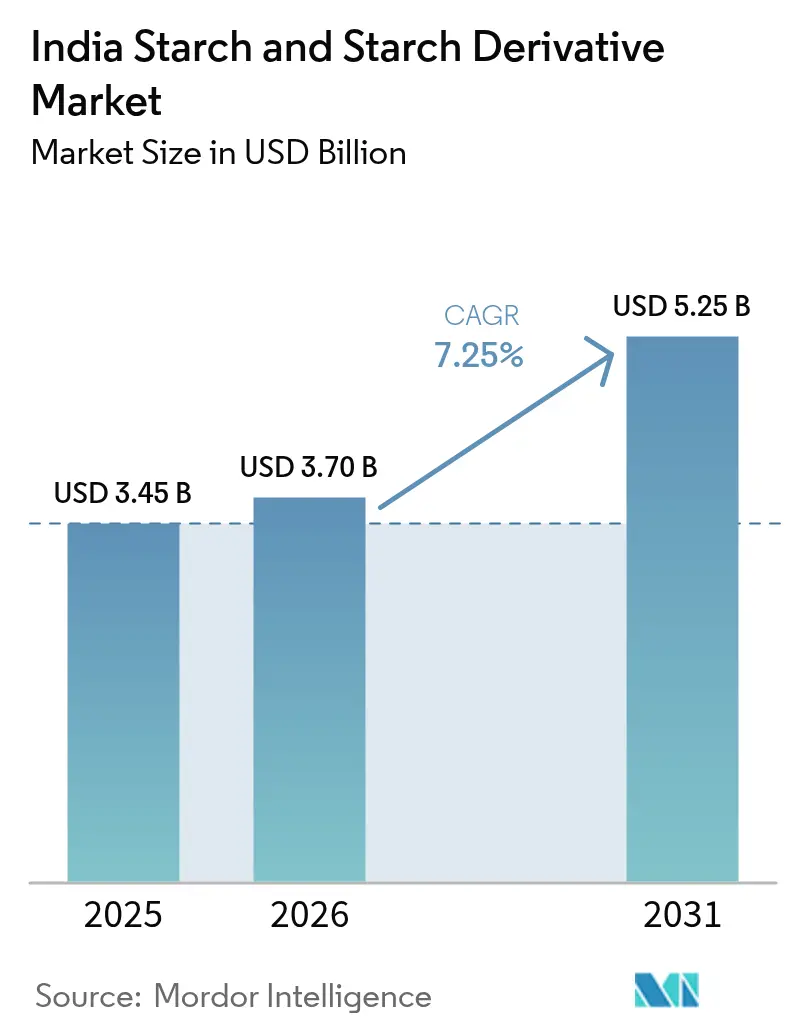

| Base Year Market Size (2025) | USD 3.45 Billion |

| Market Size (2026) | USD 3.7 Billion |

| Market Size (2031) | USD 5.25 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

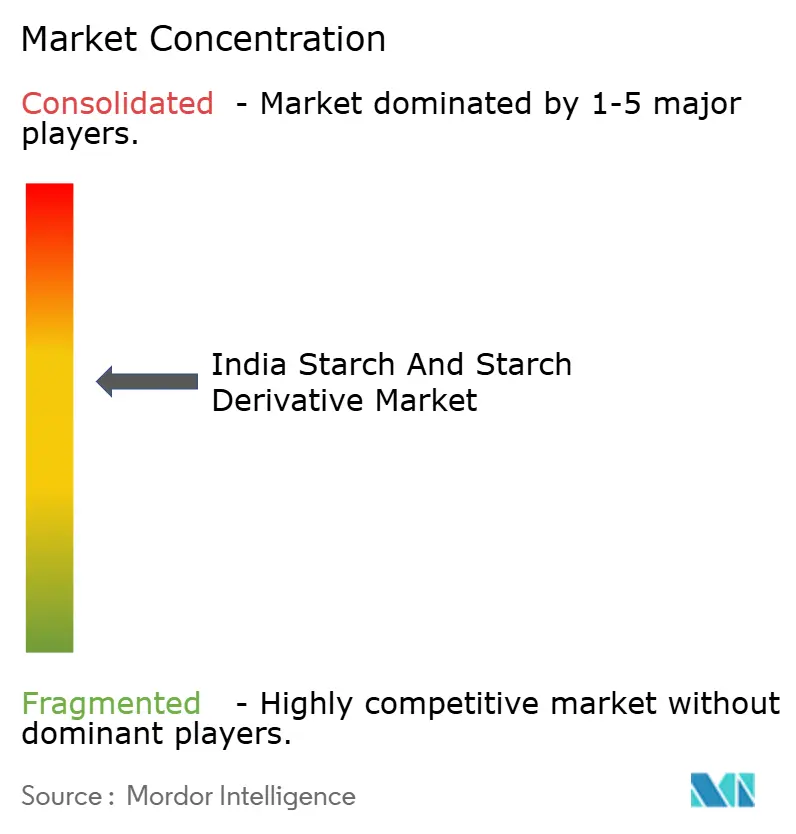

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Starch And Starch Derivative Market Analysis by Mordor Intelligence

The Indian starch and starch derivatives market size was valued at USD 3.45 billion in 2025 and estimated to grow from USD 3.7 billion in 2026 to reach USD 5.25 billion by 2031, at a CAGR of 7.25% during the forecast period (2026-2031). Growth stems from ethanol-blending policies that have lifted corn demand, rising adoption of clean-label modified starches across food and beverage categories, and policy-backed shifts toward starch-based bioplastics following the single-use plastic ban. Parallel expansion in pharmaceutical manufacturing, where cyclodextrins enhance drug-delivery performance, and in e-commerce packaging, where starch adhesives replace synthetic glues, further bolsters revenue opportunities. Key enabling factors include India’s integrated maize supply chain, the government’s 17.98% ethanol blend rate achieved by February 2025, and steady investment in new poly-lactic acid (PLA) projects that anchor latent starch demand. Nonetheless, corn-price volatility, GMO-related quality scrutiny, and sub-scale wet-milling capacity challenge near-term margins, underscoring the need for feedstock hedging and process upgrades.

Key Report Takeaways

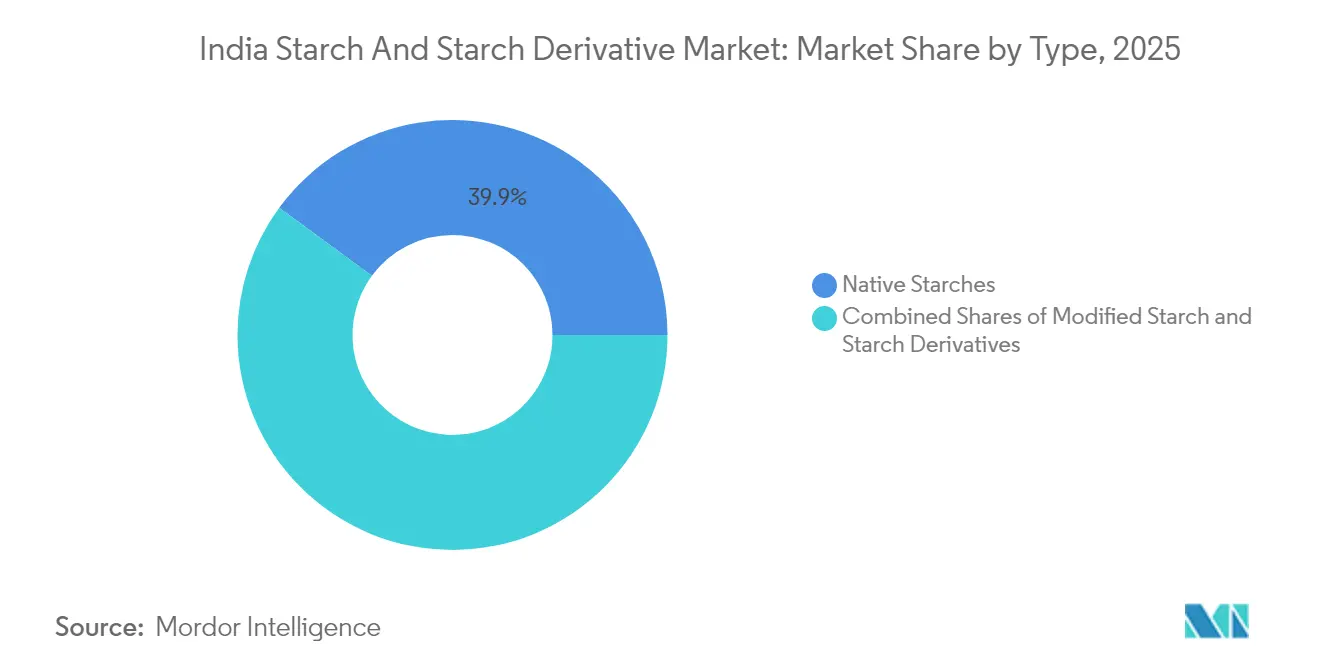

- By type, native starches led with 39.92% of the Indian starch and starch derivatives market share in 2025, while modified starches are projected to grow at an 7.90% CAGR to 2031.

- By source, maize commanded a 62.05% share of the Indian starch and starch derivatives market in 2025; wheat-based starches are poised to expand at an 8.41% CAGR.

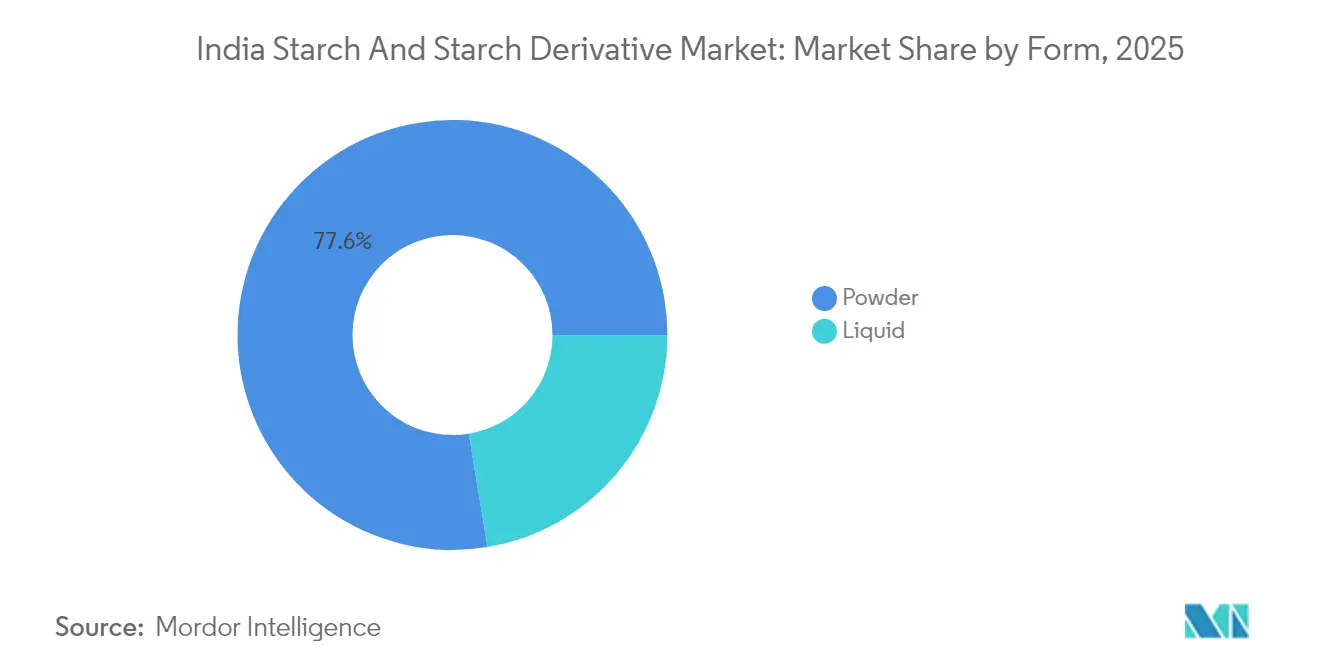

- By form, powder accounted for 77.61% market share in 2025, whereas liquid starch is forecast to rise at a 4.95% CAGR.

- By application, food and beverage held 52.94% of the Indian starch and starch derivatives market share in 2025, while pharmaceutical usage is advancing at an 8.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Starch And Starch Derivative Market Trends and Insights

Drivers Impact Analysis*

| Drivers | ~(%) Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant domestic maize supply chain integration | +1.2% | National, with concentration in Madhya Pradesh, Karnataka, Maharashtra | Medium term (2-4 years) |

| Surge in demand for clean-label modified starches | +1.5% | Urban centers, FMCG manufacturing hubs | Short term (≤ 2 years) |

| E-commerce-driven paper & packaging starch uptake | +1.8% | National, with early gains in Delhi NCR, Mumbai, Bangalore | Short term (≤ 2 years) |

| Government ethanol-blending push boosting glucose syrups | +2.1% | National, with focus on sugar-producing states | Medium term (2-4 years) |

| Emergence of starch-based bioplastics replacing single-use plastics | +0.9% | National, with regulatory compliance focus | Long term (≥ 4 years) |

| Cyclodextrin adoption in Indian pharma drug-delivery systems | +0.8% | Pharmaceutical manufacturing clusters in Gujarat, Hyderabad, Pune | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Abundant Domestic Maize Supply Chain Integration

In 2024/25, India's corn production is projected to hit 37 million metric tons, as reported by the USDA Foreign Agriculture Service [1]USDA Foreign Agriculture Service, "Production volume of corn across India", www.fas.usda.gov. This robust maize output offers strategic benefits to starch manufacturers. By integrating domestic supply chains, India not only curtails its reliance on imports but also gains a cost edge, especially amidst the backdrop of fluctuating global corn prices.In India, approximately 14% of maize production is directed towards starch manufacturing, setting a robust foundation for the industry's expansion. This segment benefits significantly from government initiatives such as the Digital Agriculture Mission, which aims to modernize the agricultural sector through technology integration. Additionally, advancements in post-harvest infrastructure, including storage and processing facilities, have strengthened the supply chain. These developments not only boost agricultural productivity but also position domestic manufacturers advantageously against their import-dependent counterparts, fostering long-term growth in the starch manufacturing industry.

Surge in Demand for Clean-Label Modified Starches

In India, a shift towards clean-label products is transforming the food processing sector, which is on track to hit USD 535 billion by 2025-26, as per the U.S. Department of Agriculture. Urban consumers, becoming more health-conscious, are turning to modified starches as natural substitutes for synthetic additives. Companies are now prioritizing clean-label formulations, heavily leaning on modified starch systems to enhance texture and mouthfeel, according to Food Ingredients First. Notably, cross-linked starches are emerging as favorites due to their superior stability and functional benefits in processed foods, showcasing better resistance to retrogradation and freeze-thaw challenges. Food manufacturers are not only adopting these modified starches to comply with regulatory standards but also to uphold product quality, driving consistent demand growth in the bakery, dairy, and convenience food sectors.

E-commerce-Driven Paper & Packaging Starch Uptake

India's paper and packaging industry is witnessing a remarkable surge, with exports skyrocketing sixfold from 2015-16 to 2021-22, largely fueled by the boom in e-commerce and a push for sustainability, as reported by Invest India. The corrugated board sector is reaping the rewards of the industry's pivot towards paper-based packaging, notably with a shift from synthetic to starch-based adhesives. Cargill is at the forefront, offering modified starches like C☆iGum™ and C☆iBond™, which not only boost production efficiency but also serve as eco-friendly substitutes for chemical additives in packaging, as highlighted by Cargill. With the industry now prioritizing 70% non-wood fiber sources, there's a burgeoning demand for specialized starch applications in paper manufacturing. As e-commerce continues its ascent and consumers increasingly favor sustainable packaging, there's a rising demand for biobased barrier coatings derived from starch. This trend positions the segment for robust growth throughout the forecast period.

Government Ethanol-Blending Push Boosting Glucose Syrups

As of September 2024, India's ethanol blending program has seen its production capacity surge to 1,623 crore liters, as reported by the Ministry of Petroleum & Natural Gas[2]Press Information Bureau, "India's Ethanol Push: A Path to Energy Security", www.pib.gov.in. The government's revamped ethanol interest subvention scheme is steering cooperative sugar mills towards multi-feedstock plants, now harnessing maize and damaged foodgrains. This shift is a boon for glucose syrup producers, as highlighted by PRS India. With a notable uptick in corn-based ethanol production, the government has responded by boosting procurement prices by 29%, steering the focus towards grain-based ethanol, sidelining its sugar-based counterpart, according to the U.S. Department of Agriculture. This strategic pivot opens up two avenues for starch manufacturers: they can either sell glucose syrup directly to ethanol producers or delve into producing value-added derivatives from processing residues.

Restraint Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact timeline |

|---|---|---|---|

| Corn-price volatility from rising ethanol diversion | -1.8% | National, with acute impact on processing centers | Short term (≤ 2 years) |

| Quality concerns due to genetically modified ingredient adulteration | -1.1% | National, with stricter enforcement in export-oriented units | Medium term (2-4 years) |

| Sub-scale wet-milling plants limiting quality consistency | -0.9% | Regional manufacturing clusters, particularly in Punjab, Gujarat | Long term (≥ 4 years) |

| Regulatory uncertainty on single-use plastic alternatives adoption | -0.7% | National, with varying state-level implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Corn-Price Volatility from Rising Ethanol Diversion

India's shift from being a corn exporter to a net importer has led to significant price fluctuations. Corn prices have jumped to USD 27.35 per quintal, driven by ethanol demand, which consumes 6-7 million tons annually. This surge in prices has a direct effect on the raw material costs for starch manufacturers, hitting smaller players with limited procurement power the hardest. In response to these challenges, the government is contemplating the import of genetically modified corn at reduced duties to address supply shortages. However, the timeline for regulatory approvals remains a gray area. Meanwhile, poultry producers are pushing for duty-free corn imports, highlighting the strain on the broader supply chain and its implications for the starch industry's competitiveness. With corn accounting for 60-70% of production costs for many starch derivatives, this volatility poses significant planning hurdles for manufacturers. As a result, companies are either resorting to advanced hedging strategies or passing the increased costs onto their downstream customers.

Quality Concerns Due to Genetically Modified Ingredient Adulteration

Despite regulatory prohibitions, the Food Safety and Standards Authority of India (FSSAI) found genetically modified ingredients in 32% of food samples it tested, posing quality assurance challenges for starch manufacturers, as reported by the Centre for Science and Environment[3]Centre for Science and Environment, "Genetically Modified Processed Foods in India", www.cdn.cseindia.org. FSSAI's draft regulations from November 2022, as highlighted by the U.S. Department of Agriculture, mandate stringent testing and labeling for GM-derived ingredients, leading to heightened compliance costs for manufacturers. While the regulatory ambiguity surrounding GM corn imports might alleviate supply constraints, it complicates quality control for starch producers catering to food-grade applications. Manufacturers focused on exports encounter intensified scrutiny from global clients demanding non-GM certification. This requirement compels them to establish segregated supply chains and adopt rigorous testing protocols. Such stringent quality assurance measures elevate operational costs and pose challenges for smaller manufacturers, especially those without advanced testing capabilities. This scenario could lead to market consolidation, favoring larger players with better resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Native Starches Lead Despite Modified Growth

In 2025, native starches command a dominant 39.92% market share, leveraging cost advantages and widespread applications in food processing and industrial sectors. Meanwhile, modified starches are the fastest-growing segment, projected to expand at an 7.90% CAGR through 2031. This surge is fueled by their specialized applications, which demand enhanced functional properties like improved stability, texture modification, and adherence to clean-label standards. Starch derivatives, such as glucose syrups and maltodextrin, are witnessing strong demand from both the ethanol and food processing industries. Notably, glucose syrups are reaping benefits from government mandates on ethanol blending.

These segment dynamics underscore India's evolving industrial landscape. While traditional native starches found their footing in textiles and paper, there's a notable shift towards higher-value modified products catering to pharmaceuticals and specialty foods. Cross-linked starches are becoming popular for their stability in processed foods. At the same time, cyclodextrin derivatives are seeing a rise in drug delivery system applications, as highlighted by RSC Pharm. Although high fructose corn syrup (HFCS) and dextrins cater to niche markets, they grapple with competition from natural sweeteners, reflecting a broader consumer shift towards clean-label products.

By Source: Maize Dominance with Emerging Alternatives

In 2025, maize accounts for 62.05% of the market share, supported by India's position as the 4th largest global producer by area and a robust wet-milling infrastructure concentrated in Gujarat, Punjab, and Maharashtra. Potato-based starches are the fastest-growing segment, with an expected CAGR of 8.41% through 2031. This growth is driven by their superior functional properties and increasing use in pharmaceutical excipients and specialty food products. Wheat-based starches continue to see steady demand in traditional applications, while tapioca starches cater to specialized industrial needs requiring specific viscosity characteristics.

The diversification of starch sources highlights manufacturers' efforts to manage risks and reduce reliance on single feedstocks amid concerns over price volatility. For example, Anil Limited operates one of India's largest corn wet-milling facilities, with a capacity of 550 tonnes per day, showcasing the scale advantages in maize processing. Additionally, alternative sources like barnyard millet starch are being explored for their sustainability and unique physicochemical properties, although their commercial scalability remains limited.

By Form: Powder Dominance with Liquid Growth

In 2025, powder form commands a dominant 77.61% market share, underscoring a well-established supply chain and customer preference for its convenience and storage stability. Meanwhile, liquid starch is emerging as the fastest-growing segment, boasting a 4.95% CAGR through 2031. This surge is largely attributed to industrial applications that prioritize direct-use convenience, especially in paper manufacturing and textile sizing operations. The liquid form not only streamlines handling but also boosts process efficiency in high-volume industrial settings.

Application-specific preferences are evident: pharmaceutical manufacturers lean towards powder forms for their precision in dosing and stringent quality control. In contrast, paper manufacturers are shifting towards liquid systems, capitalizing on the benefits for their continuous processing needs. This pivot towards liquid forms is a testament to the growing sophistication and automation in industries. Direct injection systems, a hallmark of this trend, promise reduced labor costs and enhanced process consistency. Notably, while the industry moves towards liquid, traditional practices persist. For instance, natural starches used in textile sizing, especially in the age-old process of traditional saree crafting, still rely on on-site mixed powder forms to achieve the perfect concentration.

By Application: Food & Beverage Leadership with Pharma Growth

In 2025, food and beverage applications command a dominant 52.94% market share, underscoring the robust growth of India's processed food sector, which is on track to hit USD 535 billion by 2025-26. Meanwhile, the pharmaceutical sector emerges as the fastest-growing segment, boasting an 8.62% CAGR through 2031. This surge is largely attributed to India's stature as a global pharmaceutical manufacturing powerhouse and the rising trend of incorporating starch-based excipients in drug formulations. As consumer preferences increasingly lean towards natural ingredients, personal care and cosmetics applications are witnessing a notable uptick. Conversely, the animal feed sector grapples with challenges, notably the volatility of corn prices, which has significant implications for the poultry industry's economics.

Reflecting India's burgeoning influence in the global drug manufacturing arena, the pharmaceutical segment's growth is underscored by strategic moves, such as Ingredion's acquisition of Amishi Drugs & Chemicals, bolstering their excipient portfolio. Textile applications continue to show consistent demand for sizing agents, although they now contend with competitive pressures from synthetic alternatives. Renewed growth in paper and corrugating applications is spurred by the rising demand for e-commerce packaging and a shift towards sustainability. This shift favors starch-based adhesives over their synthetic counterparts. Such diversification across applications not only mitigates the market's reliance on any single sector but also paves the way for specialized product development opportunities.

Geography Analysis

India's starch and starch derivatives market exhibits strong regional concentration patterns reflecting agricultural production zones and industrial clusters. The northern states of Punjab and Haryana lead in wheat-based starch production, leveraging proximity to grain supplies and established milling infrastructure. Gujarat and Maharashtra dominate maize-based starch manufacturing, with companies like Anil Limited operating large-scale wet-milling facilities that serve both domestic and export markets. These states benefit from port connectivity for raw material imports and finished product exports, creating logistics advantages that support market leadership positions.

The southern states of Karnataka, Andhra Pradesh, and Tamil Nadu are emerging as significant growth centers, driven by expanding pharmaceutical manufacturing clusters and food processing industries. Karnataka's biotechnology hub around Bangalore is driving demand for specialized starch derivatives in pharmaceutical applications, while Andhra Pradesh's agricultural base supports both feedstock supply and processing capacity expansion. The region's focus on high-value applications creates opportunities for premium product development and export-oriented manufacturing strategies.

Eastern states including West Bengal and Odisha represent emerging opportunities, particularly in tapioca-based starch production and traditional food applications. These regions benefit from lower labor costs and government incentives for industrial development, though infrastructure limitations constrain large-scale manufacturing expansion. The geographic diversification reflects India's federal structure, where state-level policies significantly influence industrial development patterns and create regional competitive advantages in specific starch applications and derivative products.

Competitive Landscape

The India starch and starch derivatives market demonstrates moderate concentration, indicating balanced competition between established multinational players and specialized domestic manufacturers. Global leaders like Archer Daniels Midland, Cargill, and Ingredion leverage technological expertise and integrated supply chains to serve high-value applications, while domestic players like Gulshan Polyols, Tirupati Starch, and Sukhjit Starch maintain competitive positions through regional market knowledge and cost advantages.

The competitive intensity has increased as ethanol blending policies create new demand patterns, forcing traditional starch manufacturers to adapt product portfolios and supply chain strategies. Strategic patterns reveal a shift toward vertical integration and application-specific specialization, with companies investing in downstream processing capabilities to capture higher margins.

Gulshan Polyols' Rs 994 crore ethanol supply contract with major oil marketing companies exemplifies this trend toward direct industrial customer relationships. Technology adoption focuses on process optimization and quality enhancement, with companies implementing advanced testing protocols to address GMO contamination concerns and meet export quality standards. White-space opportunities exist in bioplastics applications and pharmaceutical excipients, where specialized technical expertise creates barriers to entry and supports premium pricing strategies.

India Starch And Starch Derivative Industry Leaders

-

Archer Daniels Midland Company

-

Ingredion Incorporated

-

Gulshan Polyols Ltd

-

Tirupati Starch & Chemicals Ltd

-

Sukhjit Starch & Chemicals Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cargill Inc. opened a new corn milling plant in Gwalior, India. The company opened this plant in collaboration with Satvik Agro Processors. This plant was particularly built to provide the raw material for the production of starch derivatives.

- December 2024: Ingredion, Inc. introduced Novation Indulge 2940 starch to its clean-label texturizer portfolio, featuring a non-GMO functional native corn starch. The starch provides enhanced texture capabilities for gelling and co-texturizing applications in dairy products, dairy alternatives, and desserts.

India Starch And Starch Derivative Market Report Scope

Starch is a carbohydrate extracted from agricultural raw materials, which finds applications in literally thousands of everyday food and non-food products.

The Indian starch and starch derivatives market is segmented based on type, source, and application. By type, the market is segmented into maltodextrin, cyclodextrin, glucose syrups, hydrolysates, modified starch, and others. By source, the market studied is segmented into corn, wheat, cassava, and other sources. By application, the market studied is segmented into food and beverage, feed, paper industry, pharmaceutical industry, bioethanol, cosmetics, and other industrial applications.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Type

| Native Starch | |

| Modified Starch | |

| Starch Derivatives | Glucose Syrups |

| High Fructose Corn Syrup (HFCS) | |

| Maltodextrin | |

| Dextrins | |

| Others |

By Source

| Maize |

| Wheat |

| Tapioca |

| Others |

By Form

| Powder |

| Liquid |

By Application

| Food and Beverage |

| Pharmaceutial |

| Personal Care & Cosmetics |

| Animal Feed |

| Textile |

| Paper and Corrugating |

| Others |

| By Type | Native Starch | |

| Modified Starch | ||

| Starch Derivatives | Glucose Syrups | |

| High Fructose Corn Syrup (HFCS) | ||

| Maltodextrin | ||

| Dextrins | ||

| Others | ||

| By Source | Maize | |

| Wheat | ||

| Tapioca | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Food and Beverage | |

| Pharmaceutial | ||

| Personal Care & Cosmetics | ||

| Animal Feed | ||

| Textile | ||

| Paper and Corrugating | ||

| Others | ||

Key Questions Answered in the Report

What is the current value of India’s starch and derivative sector?

The India starch and starch derivatives market size stands at USD 3.7 billion in 2026.

How fast is demand expected to grow through 2031?

Revenue is forecast to rise at a 7.25% CAGR, reaching USD 5.25 billion by 2031.

Which product type is expanding the quickest?

Modified starches show the strongest momentum, advancing at 7.90% CAGR on clean-label and functionality trends.

Why are maize prices critical for starch processors?

Corn accounts for around two-thirds of conversion cost; ethanol diversion tightens supply, directly squeezing margins.

Page last updated on: