India Spectator Sports Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.77 Billion |

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.56 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

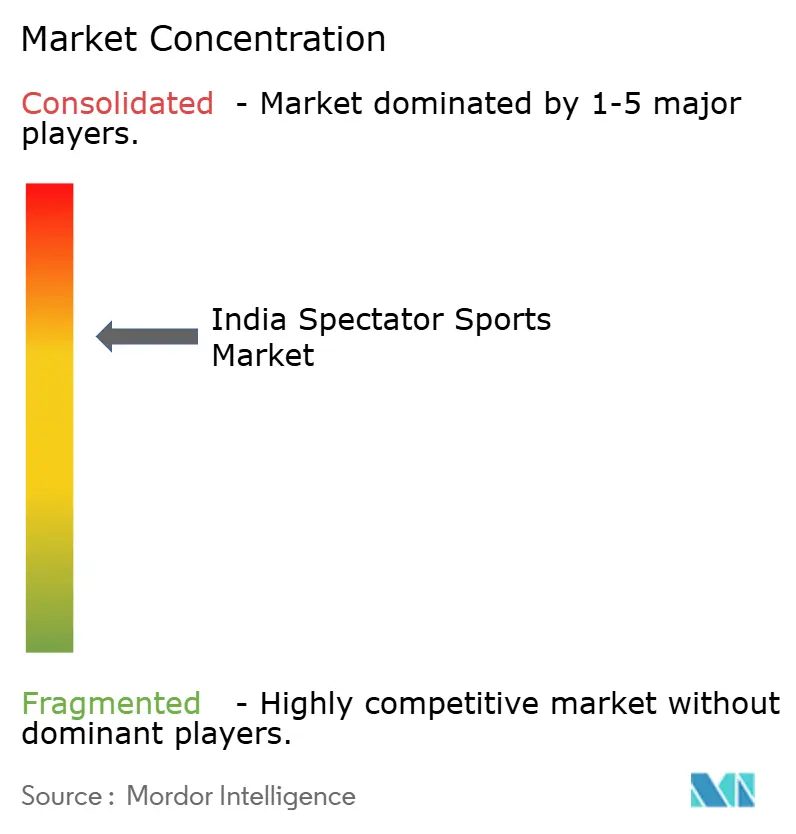

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Spectator Sports Market Analysis by Mordor Intelligence

India spectator sports market size in 2026 is estimated at USD 1.88 billion, growing from 2025 value of USD 1.77 billion with 2031 projections showing USD 2.56 billion, growing at 6.32% CAGR over 2026-2031. Growth momentum stems from digital streaming consolidation, rising disposable income in metropolitan areas, and government-backed infrastructure programmes that raise stadium capacity and fan accessibility. Corporate sponsorship budgets continue to migrate from traditional advertising into live sports because broadcast reach and emotional resonance remain unrivalled. At the same time, fantasy-sports engagement and smart-stadium rollouts convert passive viewers into high-spending participants, thereby diversifying revenue beyond media rights. Although piracy and rising player costs weigh on profitability, technology-enabled per-ticket yield uplift and bundled streaming packages mitigate these headwinds.

Key Report Takeaways

- By type, sports teams and clubs commanded a 48.74% share of the India spectator sports market size in 2025, while individual sports are on track for a 16.1% CAGR between 2026 and 2031.

- By revenue source, media rights contributed 42.85% of the India spectator sports market share in 2025; merchandising is projected to accelerate at a 18.55% CAGR through 2031.

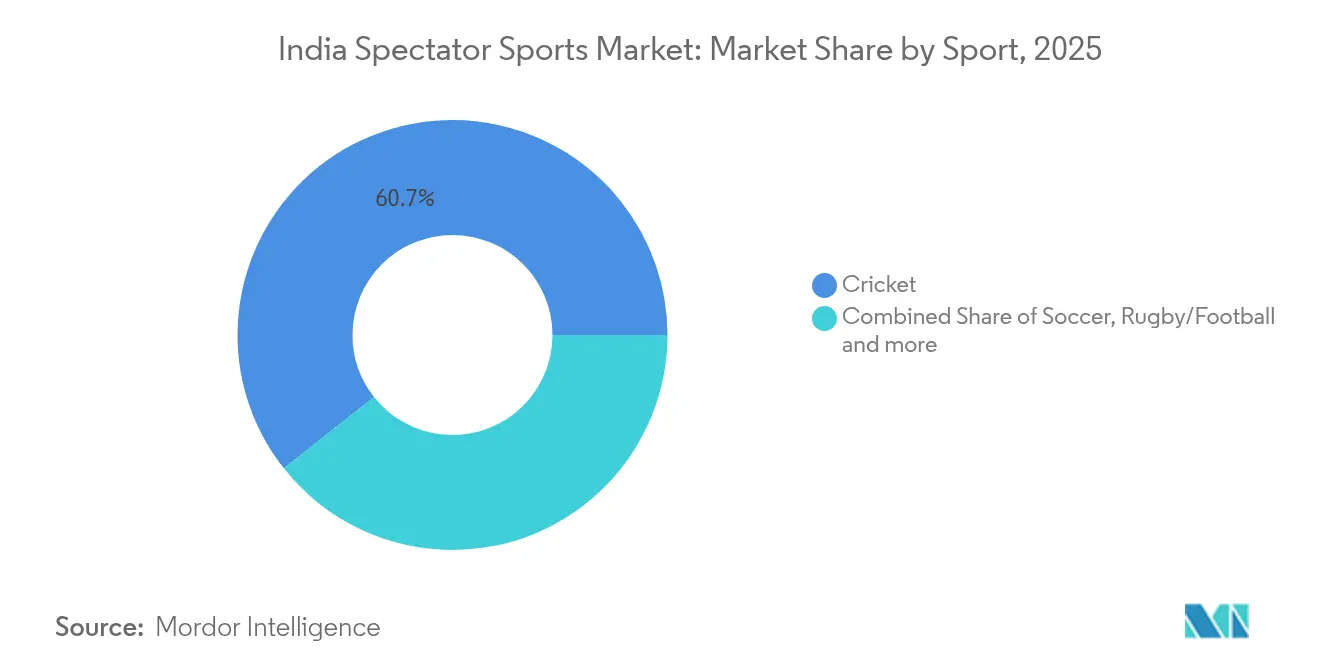

- By sport, cricket retained a 60.65% share of the India spectator sports market in 2025; women’s cricket is estimated to expand at a 23.85% CAGR through 2031.

- By geography, West India led with 29.05% revenue contribution of the India spectator sports market in 2025; East India is poised for a 14.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India contributes to a system defined not by any single country or region but by the interaction of many. The global spectator sports market data by Mordor Intelligence represents that combined structure.

India Spectator Sports Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & urban middle-class spend | +1.2% | Metros & Tier-1 cities | Medium term (2-4 years) |

| Expansion of digital streaming platforms | +1.8% | National, faster in South & West | Short term (≤2 years) |

| Government programmes supporting infrastructure | +0.9% | Nationwide, focus on North & Central | Long term (≥4 years) |

| Escalating corporate sponsorship anchored by IPL | +1.4% | National, dense in the West & South | Medium term (2-4 years) |

| Fantasy-sports engagement converting to live attendance | +0.7% | Urban markets | Short term (≤2 years) |

| Smart multi-purpose stadium projects | +0.5% | Metros & state capitals | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Urban Middle-Class Spend

Acceleration in salaried employment across technology and financial-services hubs is lifting discretionary budgets and shifting entertainment habits toward premium live experiences. Ticket packages that include hospitality lounges, curated food services, and merchandise bundles sell out faster than general admission, indicating willingness to pay for exclusivity. The trend also fuels higher average selling prices for replica jerseys and licensed collectibles that celebrate franchise identity. Metropolitan consumers demonstrate stronger brand loyalty when experiential value aligns with aspirational lifestyles, a fact reflected in consistently higher per-capita gate receipts in Mumbai, Bengaluru, and Delhi [1]Source: Business Standard Staff, “India’s urban consumption story intact despite some softness: Report,” business-standard.com . Growing disposable income, therefore, supports top-line resilience even when macroeconomic volatility curbs other discretionary categories.

Expansion of Digital Streaming Platforms

The Disney-Reliance combination of Hotstar and Viacom18 amasses roughly 750 million monthly users, enabling national reach and granular audience targeting. Free-to-view IPL matches on JioCinema rewired viewer expectations in 2024, forcing rivals to innovate around freemium tiers, regional-language commentary, and augmented-reality statistics overlays. Consolidated buying power is already influencing future media-rights tenders as leagues gauge whether fewer bidders will cap escalation in contract value. Meanwhile, advertisers benefit from cross-platform frequency capping and unified measurement dashboards that reduce wastage. The rapid shift toward connected-TV consumption in smaller cities shortens monetization cycles for niche sports once limited to pay-TV windows, accelerating revenue diversification.

Government Programmes Supporting Infrastructure

Khelo India financing and state-level allocations are converting outdated grounds into multi-sport arenas equipped with LED floodlights, automated ticketing, and athlete support facilities. Odisha’s INR 1,000 crore (USD 120 million) outlay for the 2025 National Games exemplifies long-horizon investment that boosts local employment, tourism, and venue utilization[2]Source: Times of India Sports Desk, “National Sports Policy 2025 to be launched soon,” timesofindia.indiatimes.com . Improved supply chains for turf management and broadcast infrastructure lower operating costs for event organizers, permitting more competitive pricing in markets previously constrained by poor facilities. Over time, quality assets in Tier-2 cities unlock fresh fan bases, balancing the geographic skew toward legacy metros.

Escalating Corporate Sponsorship Anchored by IPL Success

Tata’s record INR 2,500 crore (USD 300 million) title-sponsorship renewal through 2028 reset valuation benchmarks across all Indian sport properties [4]Source: SportBusiness Staff, “Tata retains IPL title sponsor rights in record deal,” sportbusiness.com . Brands outside endemic categories, such as fintech wallets and electric-vehicle OEMs, now commit to multi-year deals to secure marquee inventory. Cross-platform activations that mix television, streaming, and on-ground engagements deliver measurable lift in brand affinity among 18-34-year-olds, prompting boardrooms to reallocate budgets away from traditional television. Sponsorship fee inflows improve league working capital and encourage expansion into women’s formats and new geographies, compounding the growth flywheel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Piracy of live broadcasts eroding media rights value | -1.1% | Urban markets with high internet penetration | Short term (≤2 years) |

| Franchise fees & player salaries compressing margins | -0.8% | Premium leagues nationwide | Medium term (2-4 years) |

| Tier-2 city transport bottlenecks are limiting events | -0.6% | Tier-2 & Tier-3 cities | Long term (≥4 years) |

| Cybersecurity risks for ticketing/fantasy platforms | -0.4% | Digital-first markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Piracy of Live Broadcasts Eroding Media-Rights Value

Unofficial streaming platforms divert advertising impressions, distort audience measurement metrics, and reduce broadcasters' motivation to increase bids for broadcasting rights. A notable proportion of Indian viewers reportedly engage in password sharing or access illegal streaming links, resulting in substantial annual revenue losses amounting to hundreds of millions. This directly impacts the profitability of the most lucrative segment within the Indian spectator sports market. The enforcement of anti-piracy measures is further challenged by the rapid reappearance of mirror sites shortly after takedown efforts. Consequently, rights holders are compelled to allocate significant resources toward technologies such as watermarking and legal interventions, which escalate operational costs. Additionally, advertisers increasingly scrutinize audience reach claims, prompting the inclusion of stricter contractual terms and contributing to a decline in cost-per-thousand impressions (CPMs).

Franchise Fees & Player Salaries Compressing Margins

In 2024, the Indian Premier League (IPL) experienced a notable increase in player salaries, attributed to rising auction prices. This upward trend reflects the growing financial competitiveness within the league. Concurrently, the introduction of new leagues witnessed a significant rise in team entry fees, driven by heightened media attention and market enthusiasm. These developments underscore the expanding commercial landscape of cricket and its increasing appeal to investors and stakeholders. These outlays challenge cash flows because revenue sharing from central pools often lags by a season, requiring bridge financing at high interest rates. Women’s Premier League clubs, though enjoying rapid fanfare, already face cap-hit ratios that mirror early-era men’s IPL, signalling sustainability risks if sponsorship softens. Smaller disciplines such as kabaddi and hockey encounter similar wage inflation as they strive to retain marquee athletes against overseas offers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Franchise Models Drive Commercial Success

The sports teams and clubs segment held 48.74% of the India spectator sports market in 2025, powered by the franchise model that blends local fandom with corporate governance standards. Individual sports collectively posted a 16.1% CAGR outlook, signalling diversified appetites beyond team formats. Franchise cricket remains the reference point for operational best practice, but kabaddi, football, and volleyball leagues emulate its revenue sharing, salary caps, and marquee-player auctions. Enhanced broadcast packages and fixture uniformity foster appointment viewing, boosting advertiser demand. Meanwhile, individual-sport promoters leverage athlete storytelling to ignite fan passion and command premium appearance fees.

Commercial frameworks under the franchise system deliver predictable income streams, central media pools, licensing payouts, and hospitality share, mitigating seasonality. Conversely, individual sports rely on marquee event calendars, necessitating strong sponsorship pipelines and nimble cost management. Both tracks benefit from digital collectibles that turn highlights into monetizable non-fungible tokens, adding incremental revenue without stadium overheads. The coexistence of these models broadens the India spectator sports market, ensuring that local heroics in boxing or badminton can secure national airtime alongside cricket blockbusters.

By Revenue Source: Media Rights Dominance Faces Digital Disruption

Media rights accounted for 42.85% of 2025 revenue but intensified streaming consolidation is already moderating auction fever. Merchandising, projected at 18.55% CAGR to 2031, exploits e-commerce reach, influencer marketing, and rapid-design supply chains to convert emotional fandom into year-round purchasing. Sponsorship remains the steady second pillar as brands see rising ROI from real-time engagement metrics and data-driven activation. Ticket income, though still cyclical, is benefitting from smart-stadium value-adds that lift spend per head.

The India spectator sports market size tied to media rights will still edge higher in absolute terms because more properties reach broadcast quality; however, its share may dip as ancillary streams accelerate. Merchandise strategies now include limited-edition drops, sustainable fabrics, and athlete-signed items sold via live commerce during matches. Sponsorship bundling across men’s and women’s leagues encourages advertisers to lock multi-property deals, reducing renewal risk for rights holders. Taken together, these shifts enhance revenue stability while lowering systemic exposure to any single channel.

By Type of Sport: Cricket Hegemony Faces Demographic Challenges

Cricket preserved a 60.65% share in 2025, yet its dominance no longer implies exclusivity. The India spectator sports market size for women’s cricket is forecast to rise at 23.85% CAGR, reflecting progressive social attitudes and purposeful investment in female athlete pathways. Football’s youthful following expands during international tournaments, offering broadcast windows that complement the domestic cricket calendar. Kabaddi and badminton thrive on cultural familiarity and school-level participation, enabling audience acquisition at modest marketing spend.

Emergent sports leverage shorter formats and mixed-gender showcases to attract social-media-native fans who prefer bite-sized content. Simultaneously, cricket boards experiment with rule tweaks and night-match scheduling to combat format fatigue and protect viewership. From an advertiser's viewpoint, multi-sport portfolios hedge concentration risk while leveraging common fan data sets, driving incremental value across rights deals. Diversification thus signals market maturity and greater resilience to any single sport’s rating fluctuations.

Geography Analysis

West India generated 29.05% of revenue in 2025 owing to Mumbai’s financial heft, robust transport links, and deep sponsor pool. East India presents the fastest growth prospect at 14.05% CAGR, propelled by stadium upgrades in Kolkata and Bhubaneswar that unlock pent-up demand. South India’s technology-rich demographics sustain premium pricing, whereas North India’s populous states offer scale once infrastructure and marketing bridge historical under-provision. Central India shows green shoots as smart-city programmes bundle sports precincts into urban-renewal budgets.

Regional differentiation compels leagues to customize scheduling, language commentary, and school outreach. For example, Bengali commentary boosts TVR ratings in East India, while Kannada narration lifts engagement in Karnataka. The affordability of cricket tickets demonstrates significant regional variation, with prices in Ahmedabad being comparatively lower than those in Mumbai. This pricing disparity enhances accessibility for a broader audience and fosters the growth of cricket fandom in emerging markets. Such tailored micro-strategies ensure that the India spectator sports market remains inclusive while maximising local revenue capture.

The spectator sports market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Asia, Europe, and North America. This is complemented by country-specific insights for United Kingdom, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The competitive environment is oligopolistic, with the top conglomerates, Reliance-Disney, Sony-Zee, Star Sports, Dream Sports, and JSW-GMR, controlling a significant share of market revenue. Their vertical integration across content production, distribution, and technology underpins negotiating leverage with leagues and advertisers. The Disney-Reliance merger, for instance, pools linear TV and OTT assets to deliver national footprint at unrivalled scale, compressing bargaining power of smaller broadcasters.

Digital disruptors such as Dream11 reduce dependence on broadcast intermediaries by monetizing direct-to-consumer relationships. Data analytics gleaned from gameplay inform targeted merchandise drops and event cross-sell offers, creating a virtuous loop of engagement and revenue. Franchise owners diversify into overseas properties, GMR’s Hampshire County Cricket Club acquisition being a recent example, to globalize brand equity and hedge domestic volatility.

Sustainable competitive advantage increasingly hinges on technology adoption. Smart-stadium partnerships with telecom operators enable micro-betting and ultra-high-definition streaming, heightening fan immersion and sponsor visibility. Cybersecurity and regulatory compliance capabilities form additional competitive moats, deterring undercapitalized entrants. Overall, incumbents’ breadth across revenue streams buffers them against single-channel shocks, solidifying their dominance.

India Spectator Sports Industry Leaders

Disney Star (Star Sports)

Viacom18 Media

Sony Pictures Networks India

Zee Entertainment Enterprises

Board of Control for Cricket in India (BCCI)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Disney Star and Reliance Industries completed the merger of Indian media assets, forming the country’s largest sports broadcaster.

- September 2024: GMR Group acquired a 49% stake in Hampshire County Cricket Club for INR 1,200 crore (USD 144 million).

- August 2024: JioCinema launched an augmented-reality stats overlay for live IPL streams, allowing viewers to toggle real-time player speed and shot-placement data on mobile devices.

- July 2024: Gautam Adani and Torrent Group purchased controlling ownership of IPL franchise Gujarat Titans, continuing the consolidation of cricket teams under diversified conglomerates.

India Spectator Sports Market Report Scope

Spectator sport is a sport that features the existence of a spectator because its competition is organized at a stadium or specific venue. It has its own set of cultures, for instance, cheerleading, pre-game, and halftime entertainment like fireworks. Cricket, tennis, volleyball, football, golf, and boxing are some of the most popular spectator sports. Spectator sports exist on a huge band of popularity ranging from extremely unique to ubiquitous.

India's Spectator Sports Market is segmented by type of Sports (Cricket, Hockey, Football, Badminton, Racing, and Others) and by Revenue Source (Media Rights, Merchandising, Tickets, Sponsoring). The report offers market size and forecasts for the India Spectator Sports Market in value (USD) for all the above segments.

| Sports Team and Clubs |

| Racing |

| Individual Sports |

| Media Rights |

| Merchandising |

| Tickets |

| Sponsorship |

| Soccer |

| Cricket |

| Rugby/Football |

| Tennis |

| Other Types of Sports |

| North India |

| South India |

| West India |

| East India |

| Central India |

| By Type | Sports Team and Clubs |

| Racing | |

| Individual Sports | |

| By Revenue Source | Media Rights |

| Merchandising | |

| Tickets | |

| Sponsorship | |

| By Type of Sport | Soccer |

| Cricket | |

| Rugby/Football | |

| Tennis | |

| Other Types of Sports | |

| By Geography | North India |

| South India | |

| West India | |

| East India | |

| Central India |

Key Questions Answered in the Report

What is the current value of the India spectator sports market?

The market is valued at USD 1.88 billion in 2026 and is projected to reach USD 2.56 billion by 2031.

Which segment generates the highest revenue?

Media rights contribute 42.85% of total revenue, making it the dominant stream.

Which sport is growing fastest in India?

Women’s cricket is forecast to expand at a 23.85% CAGR through 2031, the highest among all sports.

Which region offers the fastest growth potential?

East India is expected to post a 14.05% CAGR between 2026 and 2031 due to new infrastructure investments.

How are fantasy-sports platforms impacting live attendance?

Fantasy sports participants demonstrate higher engagement with live events, contributing to increased revenue through ticket and merchandise sales.

Page last updated on: